English

English

A primary concern that business owners should have (but often don’t) is what may happen if one of the owners is no longer involved in the business. What happens when a partner dies, becomes disabled, departs from the business, divorces his or her spouse, or becomes bankrupt? What happens when there is a major disagreement among the partners? These are some of the primary reasons that business owners should have a strong buy-sell agreement — ideally one that is drafted while the business is being formed. When forming a new venture, however, business partners tend to be focused (and rightly so) on starting the business. Ideas are being brainstormed about the company’s business model. Products are being designed. Employees are being hired. Facilities are being leased. At this point, all of the partners are typically on the same page regarding the vision of their company, and the last thing they want to think about is the potential that one of the partners may not always be a part of the team. But, they must! We have seen too many examples of unequitable results and broken friendships as a result of poorly drafted (or nonexistent) buy-sell agreements. In this article, we will share some of these war stories, and will highlight what should have initially been done to avoid them. First, however, we will present a brief primer on buy-sell agreements and their most important provisions.

Simply said, a buy-sell agreement is an agreement amongst the owners of a business and the company that provides a framework for the purchase and sale (the “buy” and the “sell” of buy-sell agreements) of units in the business if a triggering event (such as those mentioned) occurs. It should state under what circumstances a triggering event occurs, who will purchase the units of the departing partner (will it be the company or the other partners?), how the purchase will be funded, and how the value of the units will be determined. We recommend to our clients that the terms of their buy-sell agreement be as precise and inclusive as possible. It should seek to address all of the possible scenarios that may arise upon a triggering event and how those scenarios will be handled. We also recommend that a team of advisors (including an attorney, life insurance agent, and valuation professional) be involved in the creation of the buy-sell agreement.

Obviously, one of the biggest issues that any buy-sell agreement should fully address is the price that will be paid to the departing partner. Ironically, however, this is often the least thought-out area of buy-sell agreements. With the proper advisors, all of the issues regarding the pricing of the departing partners’ units can be addressed and any later calamities can be avoided.

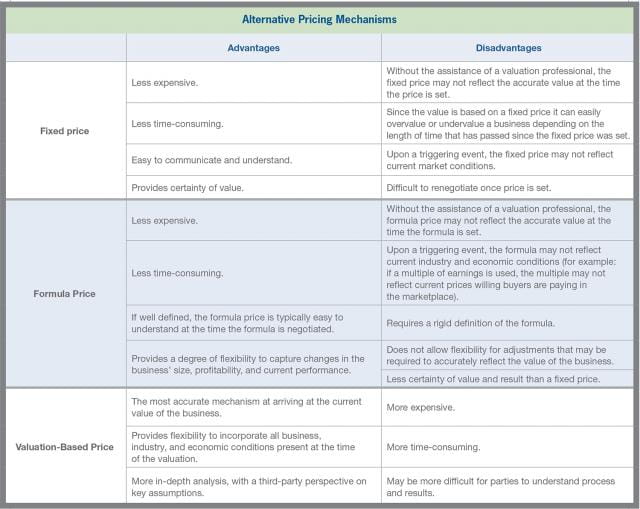

There are three main mechanisms that may be employed by buy-sell agreements for determining the purchase and sale price. The first is a fixed price mechanism, whereby the partners agree that upon a triggering event, a predetermined price per unit will be paid to the departing partner. The second is a formula price mechanism, under which the purchase price is based on a mathematical formula, often a multiple of book value or cash flow. Finally there is a valuation-based price mechanism, where a contemporaneous valuation by a business valuation expert is completed upon a triggering event. Some of the advantages and disadvantages of the three mechanisms are presented in the chart above.

While being inexpensive and generally easy to calculate, by their very nature, the fixed price and formula price mechanisms will generally result in a purchase price that doesn’t represent the fundamental value of the business. Businesses and market conditions are constantly changing. A fixed price will become out-of-date quickly (assuming the starting value was correct), especially for fast-growing companies.1 A formula price often won’t properly account for fluctuations in the capital markets, changes in the growth trajectory of the business, company-specific factors, non-recurring events, or changes in accounting methodologies or standards. In our opinion, a valuation-based pricing methodology is the most equitable and accurate approach.

Under a valuation-based pricing mechanism, it is imperative that the buy-sell agreement spells out what “value” will be paid to the departing partner. Will the value be on a 100% controlling interest basis? Will the value be on a Fair Market Value basis, which may reflect considerations for lack of marketability and minority-interest? Should the relative ownership percentages of the partners (pre- and post-triggering event) factor into the valuation? Should the value consider the personal goodwill of the departing shareholder?

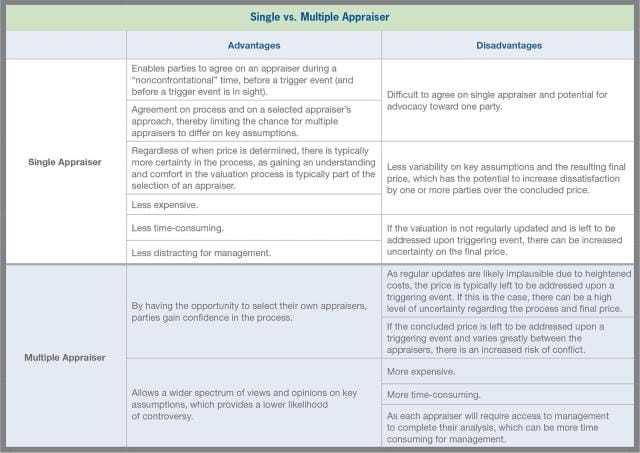

Again, a strong team of advisors can help business owners construct a buy-sell agreement that properly addresses all of these issues. The buy-sell agreement should also address who will determine the valuation of the units. Will it be a single appraiser or multiple appraisers? If a single appraiser, who will select the applicable valuation professional? If multiple appraisers, will the buyer(s) and seller separately select their own appraisers?

How will any price discrepancies be handled? Some of the advantages and disadvantages of using a single appraiser and multiple appraisers are presented in the chart below.

In addition to the determination of the value of the units of the departing partner, another significant factor of buy-sell agreements is how the purchase will be funded. It is often advisable for the company to purchase life insurance and/or disability insurance on its partners that can be used to fund the redemption of the units of a partner who has passed away or has become disabled. In the case of any other triggering event, such as retirement or termination, there are no insurance options available. For those events, buy-sell agreements should spell out the funding options available to the buyer(s) of the departing partner’s units. These options may include cash, bank debt, seller notes, or deferred compensation. It is important that all applicable terms and provisions be fully documented in the buy-sell agreement. In addition, the buy-sell agreement should also address whether the appraiser determining the value of the units consider the method of funding in their appraisal. For example, if the company is required to obtain a significant amount of bank debt to redeem a departing shareholder’s units, should that increased risk (caused by more leverage) be captured in the purchase price?

As mentioned previously, it is crucial that a strong buy-sell agreement be in place for businesses with multiple owners. It should address all of the possible issues that may arise upon a triggering event and how those issues will be resolved.

Surveys often show that an alarmingly large number of businesses have no, or inadequately thought-out, buy-sell agreements. Not having an agreement can cause terrible consequences to the business. It must always be remembered that when starting a business the buy-sell agreement will seem like an unimportant item, but unfortunately many authors of such agreements are not thinking about the problems that can be created when they are needed.

The following are several war stories that illustrate the potential issues discussed above, the problems that resulted from them, and what should have been done to avoid the ensuing fallout.

War Story I

A few years ago we had a client who started a business with a school friend. Both were married and in their thirties. Death or disability seemed impossible to conceive and they figured that they had plenty of time to write a buy-sell agreement when their business was stabilized. As fate would have it, one of the friends, who owned 50 percent of the business, died tragically — leaving his wife to control his half of the company. This would not have been, in and of itself, a problem since the surviving partner cared deeply for his partner’s family. Unfortunately for the future of the business, the deceased partner’s father-in-law had owned a business before and felt that he could step into his son-in-law’s shoes. One can only imagine the trauma caused by this situation. We tried to negotiate a buy-out of the deceased partner but it was not possible to deal with the new partner. After a period of about six months it was impossible to continue as all decisions regarding the business had to be agreed upon by both of the parties. In the end, the business was liquidated for a fraction of what the company may have been worth if allowed to be operated by the surviving founder.

Obviously the way the initial partners could have avoided these problems would have been to establish a strong buy-sell agreement at the outset of the business. Although this is an extreme example of what can happen when there is no agreement, given the statistics, it is likely a more common scenario than one might believe.

War Story II

Another situation arose with an employee of a company who was given shares in the company after being employed for one year. After a few years of employment, the employee was dismissed for reasons that were in dispute. He had the obligation to put (or sell) the stock to the company consistent with the articles of incorporation, which required a determination of Fair Market Value within 15 days of the put notice. In order to determine the Fair Market Value, the buy-sell agreement stipulated that both the company and the employee must appoint and engage their own qualified, independent appraiser knowledgeable in the valuation of private companies and the industry of the company. The appraisers would then jointly determine the Fair Market Value of the former employee’s shares in the company.

Although for many, the term Fair Market Value may imply a non-marketable, minority interest value, the language of the agreement can modify the definition. It is clear to us that many business owners and attorneys do not understand the levels of values used in the appraisal profession. The definition in this case included a mention of the minority holdings of the former employee, and other unspecified restrictions. This could imply either a minority interest value or a non-marketable, minority interest value.

Without further guidance, much is left to be interpreted by the appraiser. The range of differences in the possible interpretations of the level of value that should apply and the resultant range of concluded values in this case is significant. For example, as mentioned, the term could imply a non-marketable, minority interest value, which would require a discount for not only the minority nature of the employee’s shares, but also the lack of a readily available market for the employee to openly sell his shares. Alternatively, this could be interpreted simply as a minority interest value, and not on a non-marketable basis due to the ability of the employee to sell his shares to the company, which assumes that they are inherently marketable under this interpretation. The more judgments that are left for the appraiser, the more likely the chance of disagreement. Although we and the other appraiser had differences, we were able to reconcile and come to a conclusion of value, and avoided otherwise mandatory arbitration.

This process clearly illustrates a major requirement of well-written buy-sell agreements. Namely, the necessity of clearly defining the level of value to be considered at the time of a triggering event. Where the buy-sell agreement should have clearly stipulated the level of value as either marketable, controlling interest value, minority interest value; The potential for misinterpretation or, as was the case with this employee, the potential for multiple appraisers to interpret the definition in different ways, can cause a resolution to be delayed, or potentially leave the problem unresolved, which could result in litigation.

War Story III

When businesses are started, particularly professional service firms, the value of the enterprise consists predominantly of the personal goodwill of the founders. This generally leads to the use of book value in the drafting of the buy-sell agreement, as it is difficult to foresee at the beginning of a business venture what the future will bring and, consequently, what approach to valuing the company will apply over the life of the business. As the business grows and becomes more successful, the goodwill will evolve in nature from personal to corporate, which may require a change in the method to valuing the business.

Take a situation we encountered regarding two founding shareholders that were 20 years apart in age who started an accounting practice. The day they opened the doors the only value for the business was the book value of its tangible assets, which was a relatively small sum, since their business at that point was dependent on the personal relationships of the partners and not their corporate brand. Over the years they distributed all of the profit of the business and only purchased assets that were expensed immediately. Thus, as time progressed, the book value of the business remained nominal, while the enterprise value of the business grew with the success of the business.

This situation illustrates the need to consult a valuation professional, particularly one that is familiar with the industry in which your business operates, prior to drafting a buy-sell agreement. Doing so helps business owners avoid business valuations based on metrics, such as basing value on book value for a professional service firm, which, as illustrated in this article, can inaccurately value the business. Therefore, while we don’t generally recommend the use of a formula price mechanism approach, we do recommend, if one is used, a review and modification of the method as the business evolves. Additionally, consulting a valuation professional prior to establishing the valuation metric that will be the basis upon any future triggering event, helps business owners avoid potentially costly disagreements later.

Conclusion

All of the forgoing discussion points should serve to illustrate the importance of having a buy-sell agreement at the beginning of a new business venture; the importance of consulting a valuation professional to assist in making the decisions on how, who, and how often your business will be valued; and how any subsequent payment will be made with respect to the financial health of the business before and after the payout. We hope this illustrates the potentially devastating and lasting effects overlooking these actions can have on a privately held business and its owners and partners.