English

English

Over the past decade, rapid and substantive changes to generally accepted accounting principles (GAAP) in the U.S. have generated a fierce debate regarding the accounting practices for public and private businesses alike. In particular, a growing consensus argued that the financial reporting needs of private companies are sufficiently different from those of public companies, warranting an accounting alternative for private companies. This debate ultimately resulted in the formation of a new group, the Private Company Council (PCC), which, in collaboration with the Financial Accounting Standards Board (FASB), is charged with developing, deliberating, and voting on proposed exceptions or modifications to U.S. GAAP. Upon the FASB’s endorsement, the exceptions or modifications became incorporated in U.S. GAAP.

This article highlights amendments to U.S. GAAP resulting from PCC consensus opinions and resulting FASB endorsements, including accounting for goodwill and accounting for identifiable intangible assets in a business combination, as well as implications to preparers and users of financial statements.

What Is a Private Company?

For the purposes of the PCC’s activities and resulting modifications to GAAP, a private company is defined as any entity other than a public business entity, a not-for-profit entity, or employee benefit plans. A public business entity is a business entity meeting any one of the following criteria.

- It is required by the U.S. Securities and Exchange Commission (SEC) to file or furnish financial statements, or does file or furnish financial statements (including voluntary filers), with the SEC (including other entities whose financial statements or financial information are required to be or are included in a filing).

- It is required by the Securities Exchange Act of 1934 (the “Act”), as amended, or rules or regulations promulgated under the Act, to file or furnish financial statements with a regulatory agency other than the SEC.

- It is required to file or furnish financial statements with a foreign or domestic regulatory agency in preparation for the sale of or for purposes of issuing securities that are not subject to contractual restrictions on transfer.

- It has issued, or is a conduit bond obligor for, securities that are traded, listed, or quoted on an exchange or an over-the-counter market.

- It has one or more securities that are not subject to contractual restrictions on transfer, and it is required by law, contract, or regulation to prepare U.S. GAAP financial statements (including footnotes) and make them publicly available on a periodic basis (for example, interim or annual periods). An entity must meet both of these conditions to meet this criterion.

An entity may meet the definition of a public business entity solely because its financial statements or financial information are included in another entity’s filing with the SEC. In that case, the entity is only a public business entity for purposes of financial statements that are filed with the SEC.

Of note, a company may currently be defined as a private company, but may become a public business entity in the future through an initial public offering, capital raise, an investment or acquisition by a public company, or other events. The current accounting alternatives do not provide clear transition guidance for entities that use the accounting alternatives and later become public business entities. All current signs indicate that these companies would need to retroactively “undo” application of the accounting alternatives, which can be burdensome and costly. Accordingly, companies that are currently eligible to apply the accounting alternatives should carefully weigh the current and future costs and benefits.

Overview of the PCC

Formed in 2012 by the Financial Accounting Foundation (FAF) Board of Trustees, the PCC has two principal responsibilities. First, the PCC determines whether exceptions or modifications to existing nongovernmental U.S. GAAP are required to address the needs of users of private company financial statements. Second, the PCC serves as the primary advisory body to the FASB on the appropriate treatment for private companies for items under active consideration on the FASB’s technical agenda.

The PCC is the product of prior working groups, committees, roundtables, and solicitations of input dating back to 2006. In connection with the formation of the PCC, the FAF’s outreach included the receipt of 7,367 comment letters, four nationwide roundtable discussions with 60 stakeholders, and a webcast that included 316 participants.

Accounting for Goodwill

The first PCC consensus opinion and resulting FASB endorsement was completed in January 2014, culminating in Accounting Standards Update (ASU) 2014-02, which amends Accounting Standards Codification (ASC) Topic 350, Intangibles — Goodwill and Other (ASC 350”) (the “Goodwill Accounting Alternative”). During its research and outreach efforts, the PCC obtained feedback from private company stakeholders that the benefits of the current accounting for goodwill after initial recognition do not justify the related costs as it pertains to the usefulness of the carrying amount and potential impairment losses, as well as the cost and complexity in performing the current goodwill impairment test.

The PCC and FASB noted in ASU 2014-02 that many users of private company financial statements disregard goodwill impairment charges from their quantitative analysis of a private company’s operating performance. Moreover, because the underlying events and conditions leading to goodwill impairment generally manifest themselves long before the impairment is reported, users that provided the PCC feedback indicated that they use other, more real-time information (including information obtained through their access to management). Some users acknowledged that an impairment loss (or lack of an impairment loss) can be an indicator of the failure (or success) of an acquisition; however, they noted that the usefulness of goodwill impairment accounting is diminished because most private companies do not issue GAAP interim financial statements, and they generally issue their year-end financial statements later than public business entities. Users further stated that the amount of the impairment is less relevant than the existence of impairment because the calculation of the impairment loss is not well understood.

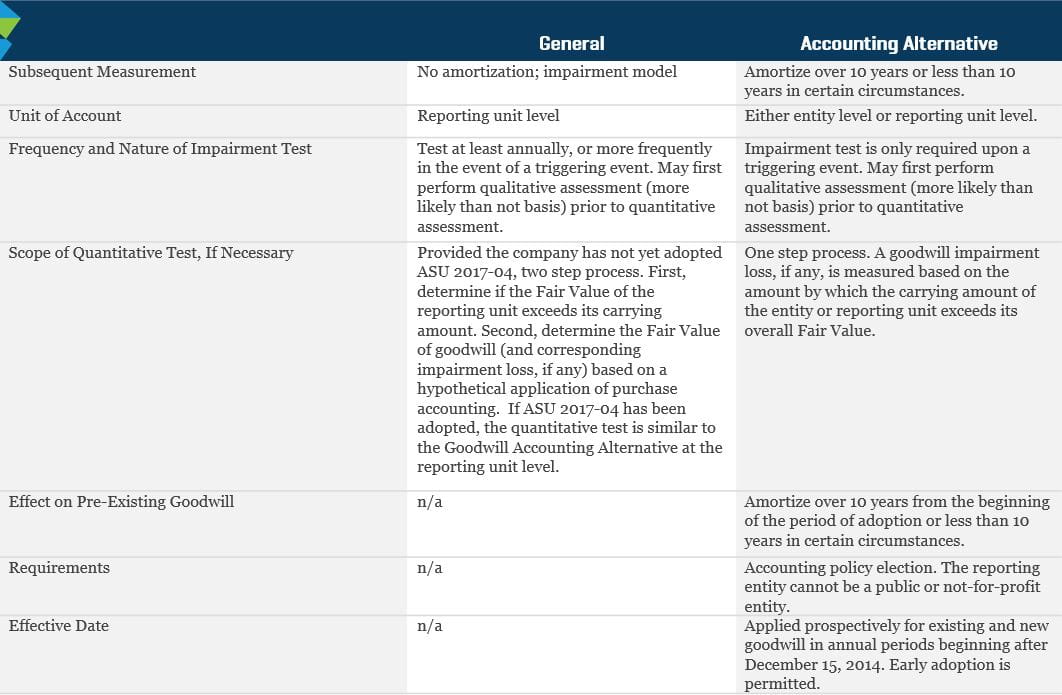

The main provisions of the Goodwill Accounting Alternative, if elected by a nonpublic entity, are outlined below and contrasted against the “general” accounting guidance in the following table.

- Existing goodwill and new goodwill recognized after the beginning of the annual period of adoption should be amortized on a straight-line basis over 10 years, or less than 10 years if the entity demonstrates that another useful life is more appropriate (e.g., the primary impetus for an acquisition was to obtain access to the target’s proprietary technology, in which case it may be appropriate to amortize goodwill over the life of the technology).

- Goodwill may be tested for impairment at either the entity level or the reporting unit level upon an entity’s accounting policy election.

- Impairment testing is only required when a triggering event occurs. The reporting entity may first perform a qualitative assessment. If the qualitative assessment indicates that it is more likely than not that goodwill is not impaired, further testing is unnecessary.

- A goodwill impairment loss, if any, is determined as the excess of the carrying amount of the entity or reporting unit over its Fair Value. Step two of the current impairment test, which requires the hypothetical application of purchase accounting to determine the goodwill impairment amount, is eliminated.[1]

Accounting for Identifiable Intangible Assets in a Business Combination

In December 2014, another PCC consensus opinion and FASB endorsement was completed, resulting in ASU 2014-18, which amends ASC Topic 805, Business Combinations (“ASC 805”) (the “Intangibles Accounting Alternative”). Similar to the Goodwill Accounting Alternative, the Intangibles Accounting Alternative was adopted in response to private company stakeholder responses that the benefits of the current accounting for identifiable intangible assets acquired in a business combination may not justify the related costs.

In the course of its outreach, the PCC noted that the Fair Value of some identifiable intangible assets is relevant to some users of private company financial statements. Intangible assets that are legally protected and that can be sold or generate discrete cash flows, such as technology, were characterized as most relevant. Some users, particularly lenders, indicated that intangible assets are most relevant when their cash flows can be reliably estimated or they can be sold in liquidation. Because customer-related intangible assets and noncompetition agreements are typically not capable of being sold or licensed independently from the other assets of a business, and because these assets are often the most subjective and difficult intangible assets to measure, stakeholders stated that the alternative should focus on those intangible assets.

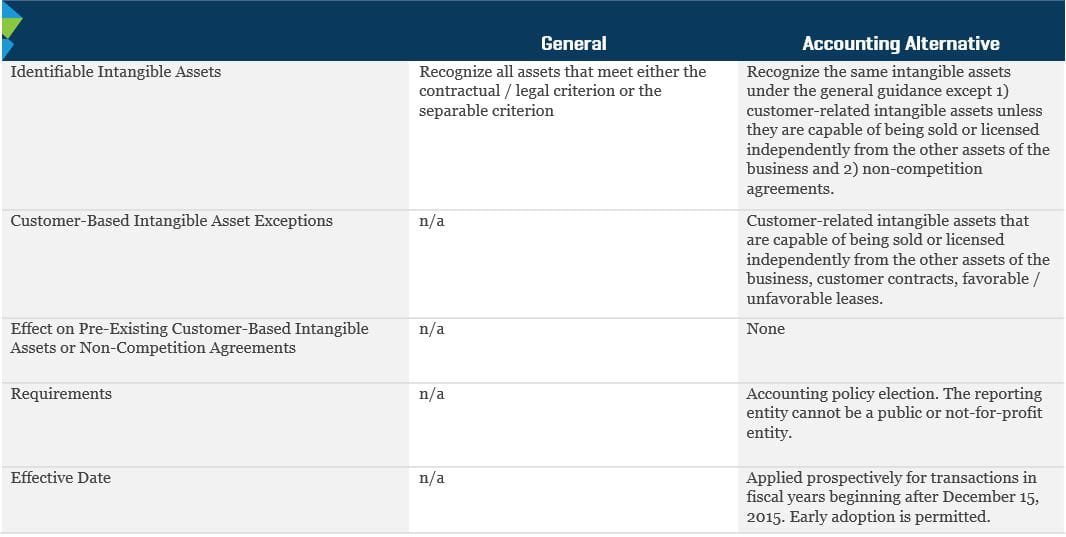

The main provisions of the Intangibles Accounting Alternative, if elected by a nonpublic entity, are outlined below and contrasted against the “general” accounting guidance in the following table. For entities that adopt the Intangibles Accounting Alternative, the amendments to ASC 805 will generally result in those entities separately recognizing fewer intangible assets in a business combination compared to entities that do not elect or are not eligible for this option.

- The following intangible assets are no longer required to be recognized separately from goodwill: 1) customer-related intangible assets unless they are capable of being sold or licensed independently from the other assets of the business and 2) noncompetition agreements.

-

Customer-related intangible assets that may still meet the criterion for recognition include, but are not limited to:

- Mortgage servicing rights

- Commodity supply contracts

- Core deposits

- Customer information (e.g., names and contact information)

- Contract assets, as used in ASC Topic 606 on revenue from contracts with customers, are not considered to be customer-related intangible assets for purposes of applying the Intangibles Accounting Alternative. Therefore, contract assets are not eligible to be subsumed into goodwill and will be recognized separately.

- Contract assets are defined as an entity’s right to consideration in exchange for goods or services that the entity has transferred to a customer when that right is conditioned on something other than the passage of time (e.g., the entity’s future performance).

- A lease is not considered to be a customer-related intangible asset for purposes of applying the Intangibles Accounting Alternative. Therefore, favorable and unfavorable leases are not eligible to be subsumed into goodwill.

- Pre-existing customer-related intangible assets and noncompetition agreements that exist at the beginning of the period of adoption are not affected by the Intangibles Accounting Alternative. That is, such existing assets may not be subsumed into goodwill.

- Other intangible assets will continue to be recognized.

- An entity that elects the Intangibles Accounting Alternative must adopt the Goodwill Accounting Alternative. An entity that elects the Goodwill Accounting Alternative is not required to adopt the Intangibles Accounting Alternative.

Related Considerations

Customer-based intangible assets often represent the primary identifiable intangible asset in a business combination, and accordingly this asset is frequently valued using the multi-period excess earnings method (MPEEM), whereby contributory asset charges attributable to supporting assets are applied to a stream of overall company economic benefits to derive the remaining cash flows attributed to the customer-based intangible. In the instance that another identifiable intangible asset constitutes the primary asset of an acquired business (e.g., trademarks or technology), customer-based intangibles would be valued via an alternative methodology, with the MPEEM applied to the primary asset of the business. As a consequence, while the Intangibles Accounting Alternative may not require recognition of customer-based intangible assets or noncompetition agreements, the Fair Value of these assets may still need to be measured in certain circumstances.

Additionally, in circumstances in which the primary customer-based intangibles are relationship-based in nature, and these customer relationships would meet the exclusion criteria of the Intangibles Accounting Alternative, we have noted an emphasis on recognition of the corresponding customer information (e.g., name and contact information) by certain audit firms. To this end, care should be exercised in evaluating whether such customer information could in fact be sold or licensed separately from the other assets of the business, or if the quantity and quality of the customer information would in fact be materially valuable to a market participant. The per-customer value of contact information is typically vastly lower than an ongoing business relationship, and often selling or licensing such information could irreparably damage the target’s relationship with the end customer. Additionally, there are often legal restrictions on selling or licensing such information. As an example, RadioShack's recent bankruptcy proceedings were challenged primarily due to the inclusion of more than 13 million e-mail addresses and 65 million customer names and physical address files in the sale. Prior to its bankruptcy, RadioShack’s privacy policy (displayed in RadioShack stores) stated: “We pride ourselves on not selling our private mailing list.” State law in Texas prohibits companies from selling personally identifiable information in a way that violates their own privacy policies. AT&T also challenged the sale of customer information on the basis that the information was not RadioShack’s to sell. The sale of RadioShack was ultimately completed in May 2015, but only after an agreement to limit its customer e-mail information to the last two years, and to allow access to only seven of the 170 fields of customer data.[2][3]

We would also note that in a taxable (asset) transaction, the value attributed to noncompetition agreements typically maintains different tax treatment for the seller than other intangible assets and goodwill (i.e., noncompetition agreements are often taxed at ordinary income tax rates whereas the gain on other intangible assets and goodwill is taxed at capital gains tax rates). Accordingly, noncompetition agreements may still require measurement in certain circumstances regardless of the nonrecognition alternative for reporting purposes.

Counterpoints

In January 2015, the CFA Institute — whose membership is comprised of investment professionals — published the results of a survey of its members in May 2014 titled “Addressing Financial Reporting Complexity: Investor Perspectives” (the “2014 Private Company Survey”).[4] In the view of the CFA Institute, outreach by the FAF to private company stakeholders was undertaken largely at the behest of the preparer community as it argued for changes in reporting requirements aimed at reducing preparer compliance costs. The CFA Institute contended that the perspectives of investors were missing from the discourse. The 2014 Private Company Survey sought investor insights on the impact of separate nonpublic company reporting requirements on investors’ financial analyses, how investors view extending such reduced requirements to public companies, and their perspectives on efforts related to changes in public company requirements.

- Respondents believed differential standards for public companies in relation to private companies will decrease comparability (82%), create greater complexity (73%), and result in the loss of decision-useful information (65%).

- Only 32% of respondents believed that access to management was sufficient to supplement the loss of information resulting from accounting alternatives.

- 65% of those surveyed did not believe that large, widely held private companies should be permitted to apply reduced private company reporting requirements.

- 78% of survey respondents believed that private company accounting standards will be perceived to be of a lower quality.

- The CFA Institute asserts that the creation of alternative accounting treatments for private companies will make financial statements less comparable, increasing the burden on users of financial statements and potentially also increasing the cost of capital.

- The 2014 Private Company Survey cites Dr. Aswath Damodaran, professor of corporate finance and valuation at the Stern School of Business at New York University, who contends that if investors perceive firms that disclose less information to be more risky, they are likely to attach higher risk premiums and cost of capital and lower values to these firms.[5]

- Only 6% of survey respondents believed that private company alternatives should be extended to public companies.

Weighing Costs and Benefits

New accounting and reporting options are now available to nonpublic business entities. While these alternatives may serve to decrease compliance costs and simplify reporting requirements, businesses that meet the criteria required to apply these accounting alternatives must carefully weigh the current and future costs and benefits of these amendments to U.S. GAAP, including the costs of compliance, a future transition to a public business entity, and the perspectives of its various stakeholders.

A previous version of this article was published in September 2015.

- The FASB has since adopted ASU 2017-04, which eliminates step two of the impairment testing process for all reporting entities.

- Joshua Brustein, “RadioShack’s Bankruptcy Could Give Your Customer Data to the Highest Bidder,” Bloomberg, March 24, 2015.

- Reuters, “Bankruptcy Judge Approves Sale of RadioShack Name and Data,” The New York Times, May 20, 2015.

- The author of this article is a member of the CFA Institute, but did not contribute to the 2014 Private Company Survey.

- Aswath Damodaran, “The Value of Transparency and the Cost of Complexity,” p. 30.