English

English

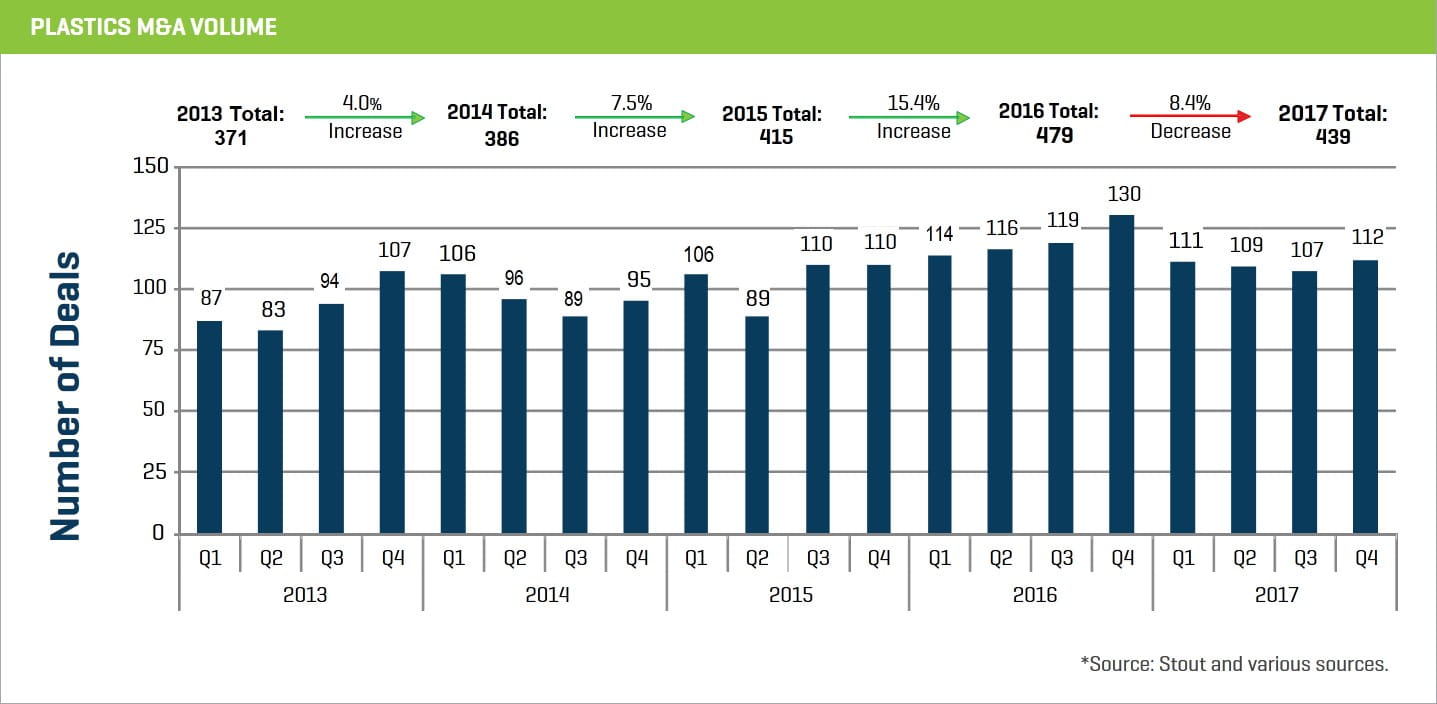

Plastics industry M&A activity totaled 439 transactions during 2017, second to only 2016 as the highest volume year that Stout has tracked. Despite an 8.4% decline in 2017, transaction activity was steady throughout the year with continued strong performance across most end markets and plastic processes. In addition, the 112 transactions posted during the fourth quarter of 2017 was a 5% increase from the third quarter, showing positive momentum going into 2018. Overall, there continues to be a strong M&A market within the plastics industry, with continued favorable financing and equity markets, generally low cost of capital, historically high valuation levels, and recent tax law changes that could drive further transaction activity.

Looking ahead, what are some factors to consider?

- Despite recent volatility, stock market and overall valuation levels remain high, as indicated by record highs achieved by the major market indices and plastics industry segments during 2017.

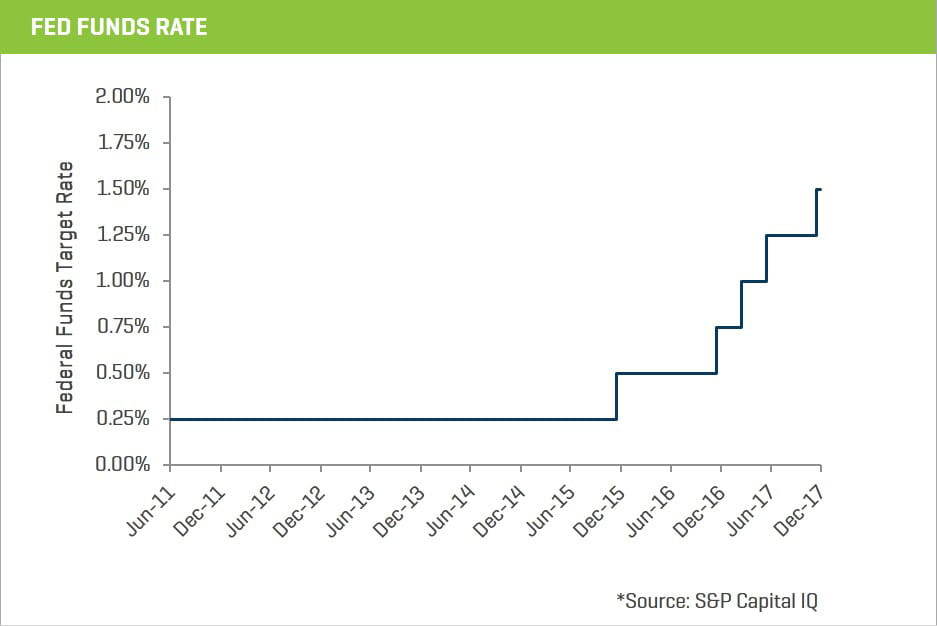

- Interest rates and overall cost of capital remains relatively low and there is ample debt and equity financing available to fund transactions.

- Strong strategic and financial buyer demand for plastics companies continues across most end markets and plastic processing types.

- Recent tax law changes resulting in lower corporate and personal income taxes could benefit businesses with increased capital and disposable income available to purchase a wide range of consumable and durable plastics goods.

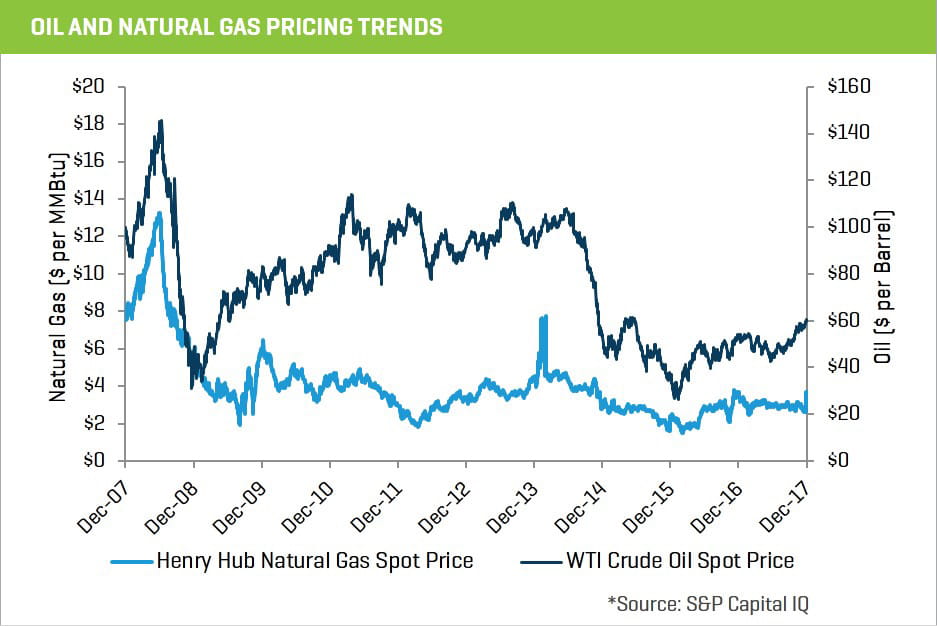

- Despite some volatility during 2017, crude oil and natural gas prices remain relatively low, which could continue to positively impact the cost of certain resins in the short term.

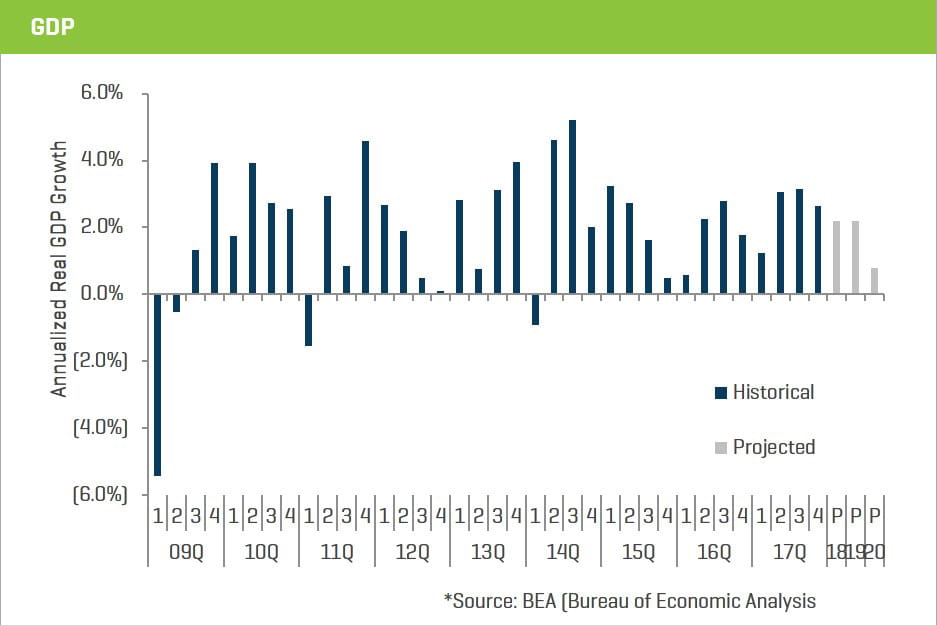

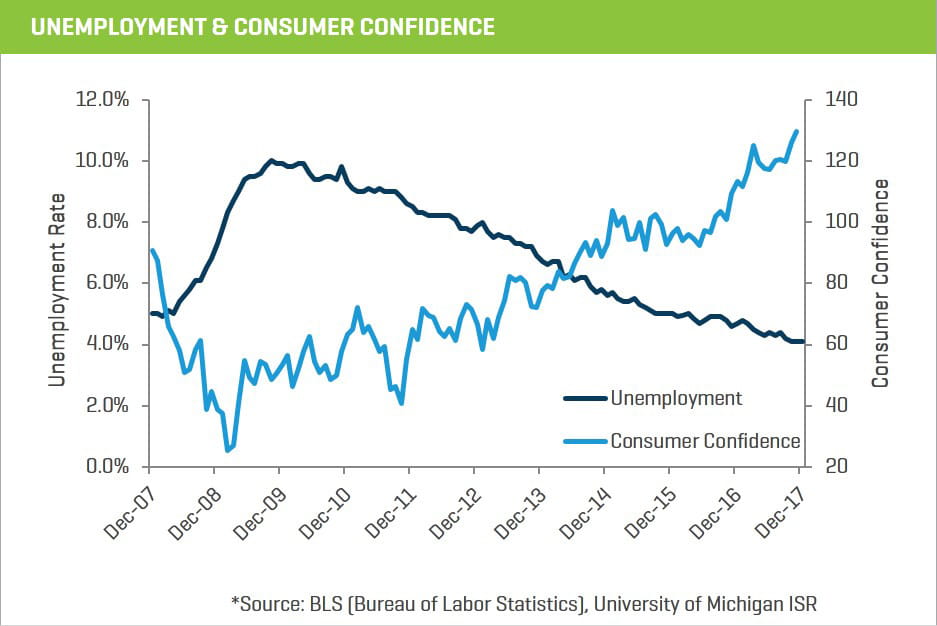

- Macroeconomic metrics such as GDP, consumer confidence, and unemployment remain strong.

- Reshoring to U.S. manufacturing, which has been on the rise during the past several years, lends additional support to an overall positive economic outlook.

A deeper dive reveals insights and data important to participants within the plastics industry.

Plastics M&A Activity

2017 saw another strong year for M&A activity within the plastics industry and there was continued overall strong demand for plastic companies across all end markets and manufacturing processes.

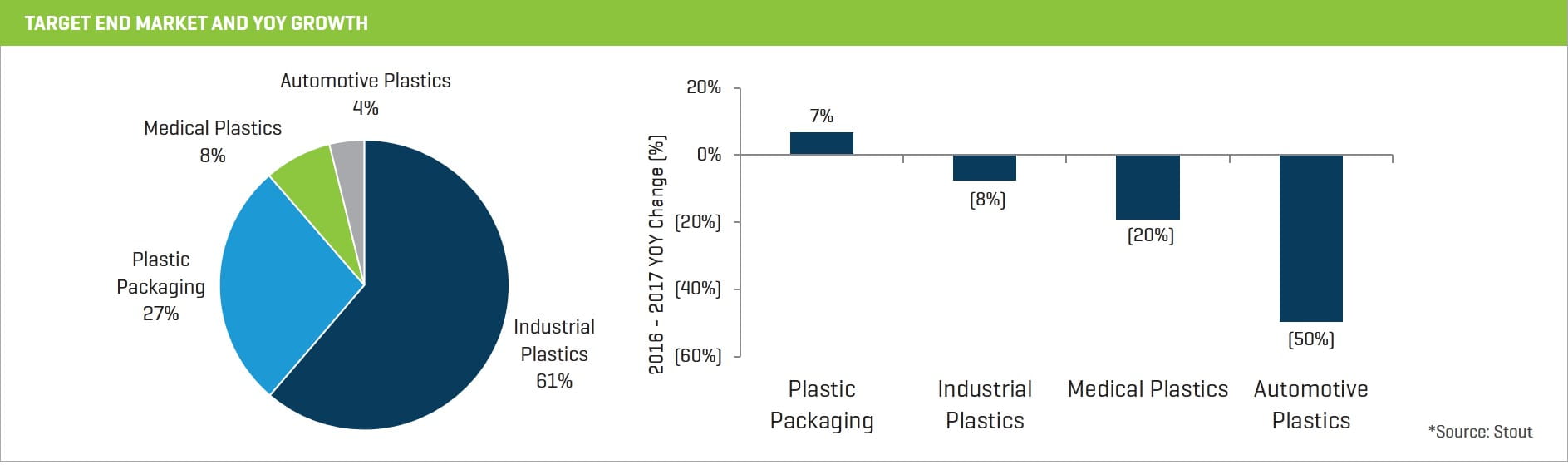

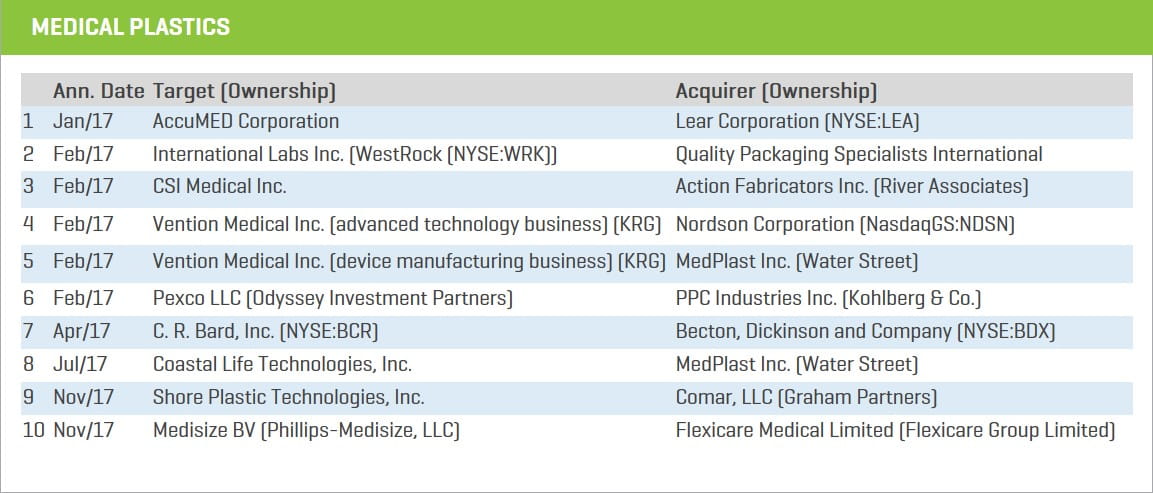

- End Market. From an end market perspective, plastic packaging performed the strongest, with a 7% increase in M&A volume, year over year (YOY). Automotive saw the biggest decline, dropping 50% YOY, followed by medical and industrial plastics, which declined 20% and 8%, respectively, YOY. Within medical, there was a significant increase in the number of extrusion transactions.

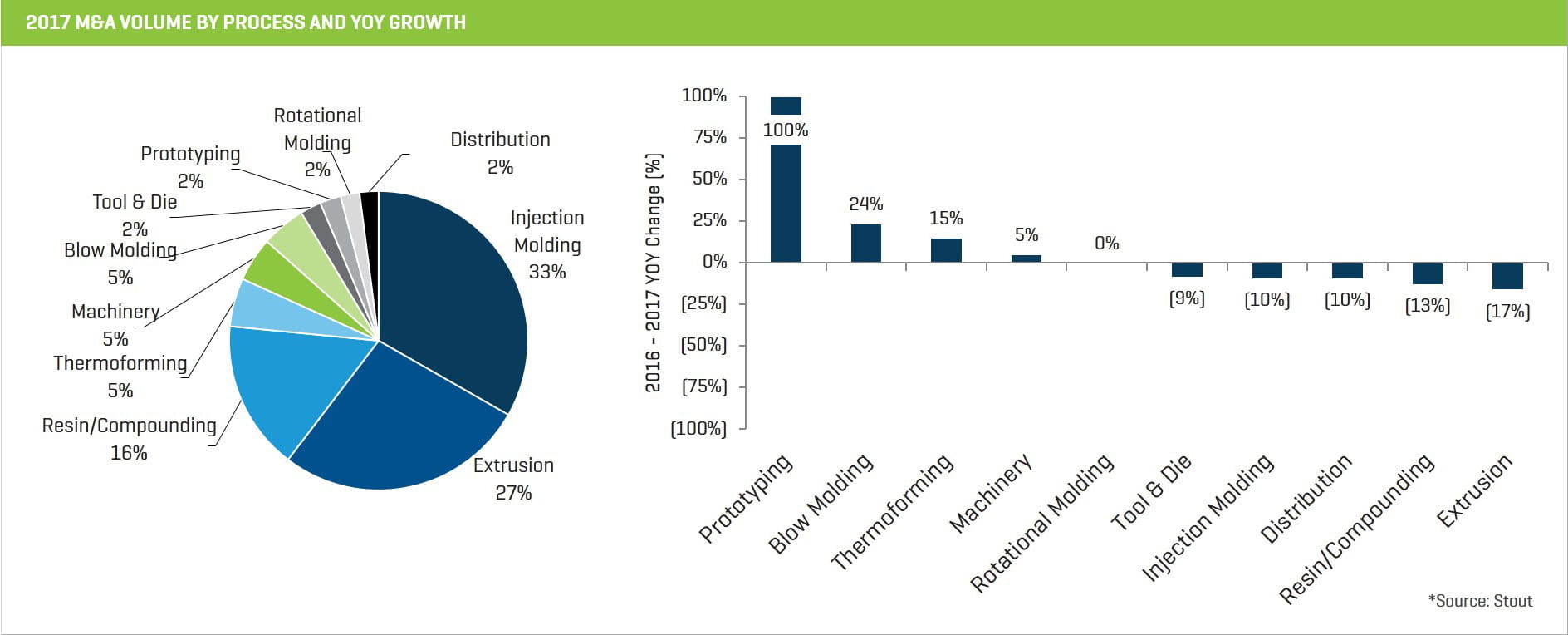

- Process Type. Transaction activity involving plastic manufacturing process types was mixed during 2017, with half of the categories flat or up and the other half down. M&A activity was up for several niche process categories, including prototyping, blow molding, and thermoforming, which increased 100%, 24% and 15%, respectively, YOY. Two of the largest segments, extrusion and injection molding, declined 17% and 10%, respectively, YOY, although injection molding saw growth in plastic packaging and industrial plastics, while extrusion saw an increase in plastic packaging transactions.

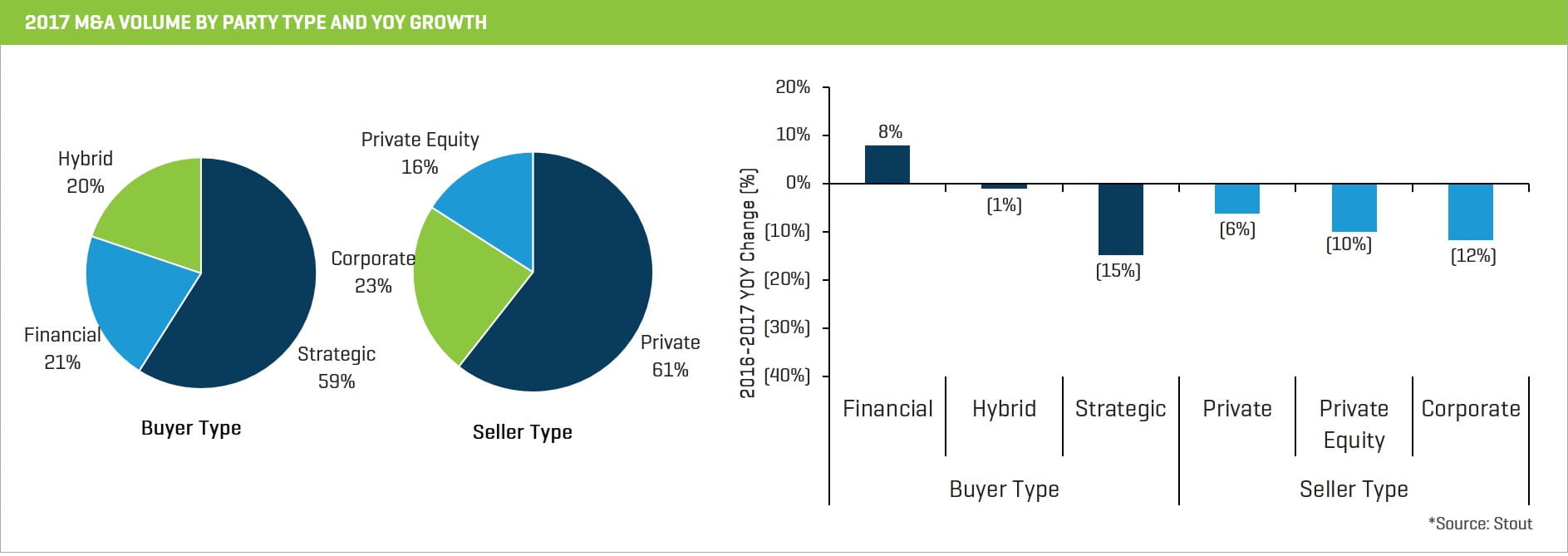

- Buyer/Seller Type. Financial and hybrid (PE-owned strategic) buyer activity was flat or up during 2017, while strategic purchases were down 15%, YOY. Within hybrids, there was an increase in the number of injection molding transactions. M&A activity involving all three seller types was down during 2017 – private equity, private owners, and corporate. In 2017, there was an increase in the number of corporate carve outs involving injection molding businesses.

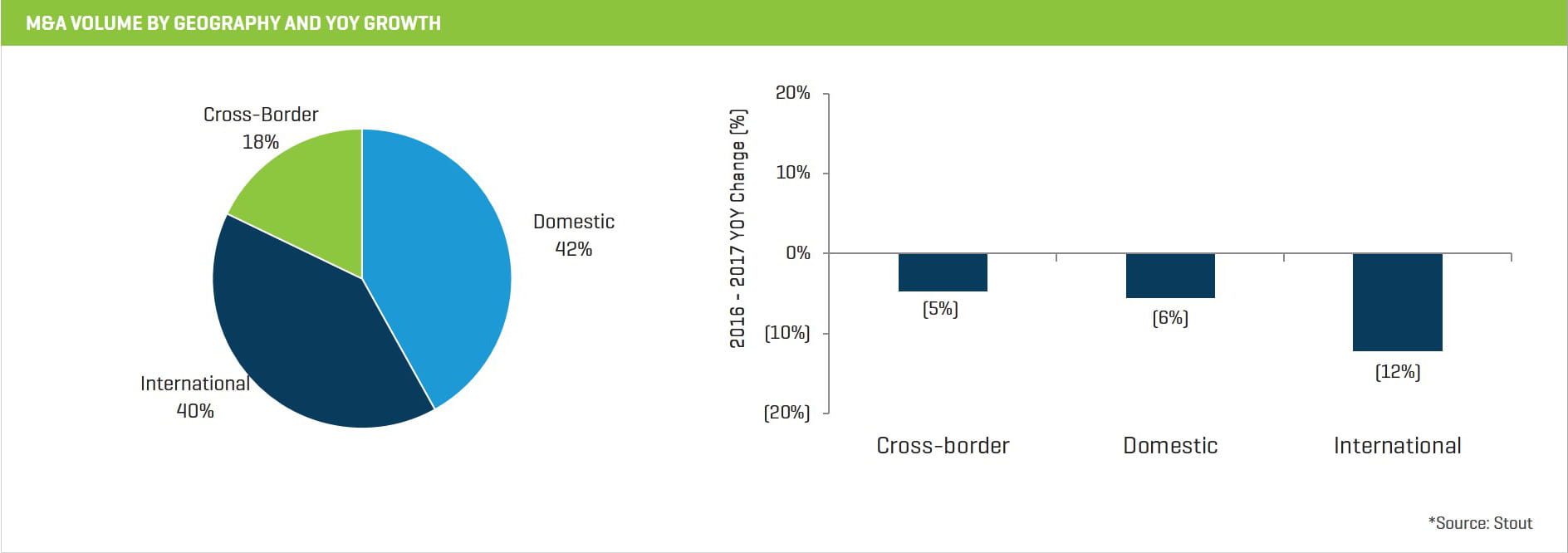

- Geography. From a geographic perspective, domestic, cross-border and international transaction activity was down during 2017, although the U.S. domestic market remains strong. Machinery and blow molding domestic and cross-border transaction activity saw notable increases during 2017.

Plastics Industry Multiples

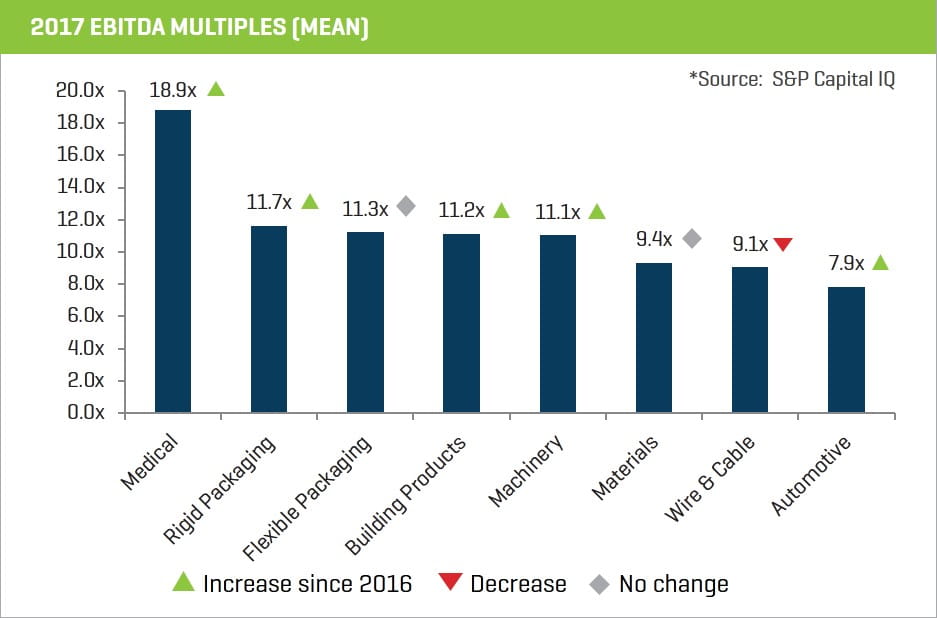

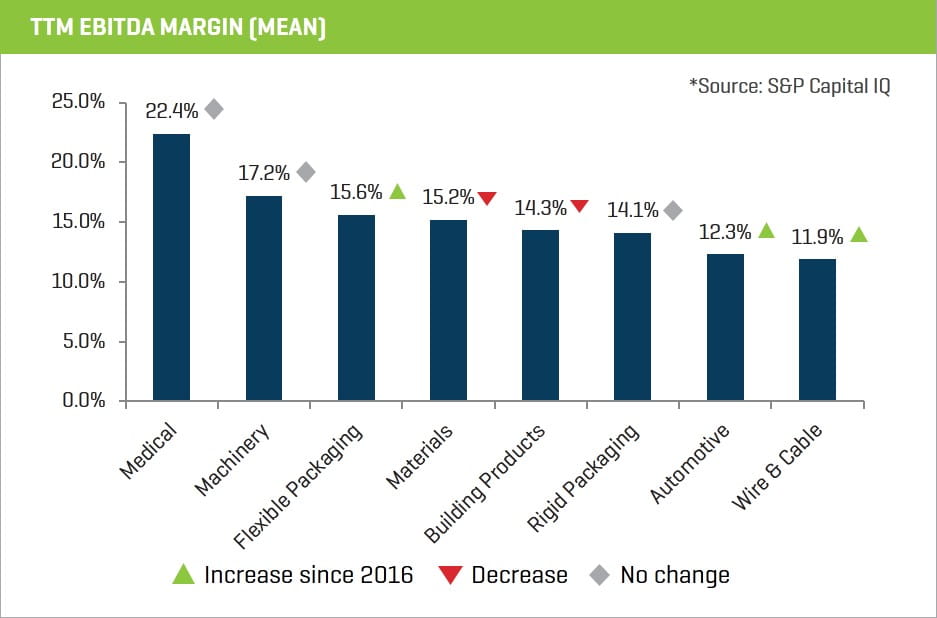

Despite recent volatility, valuation multiples continue to be near all-time highs across each of the plastic end market sectors, as well as the overall market.

- Particularly within the U.S. market, there is somewhat of a supply/demand imbalance (i.e., more interest in plastics businesses relative to the number of quality companies available for sale) contributing to the high valuation levels that continue to be prevalent in the marketplace.

- Looking at publicly traded companies within the plastics industry, medical, packaging, machinery, and automotive multiples were up during 2017, although all segments are trading at very high levels.

- Major market indices are another indicator of high valuation levels, with the Dow Jones Industrial Average, S&P 500, and Nasdaq extending their highs from 2016 with increases of 24%, 18% and 27%, respectively, in 2017.

- In addition, new lower corporate tax rates, all things equal, could lead to higher cash flows for businesses, which could help sustain or increase valuation levels for plastics companies.

Capital Markets / Macroeconomic Indicators

Transaction volume benefited from continued favorable credit markets, a low overall cost of capital, and an abundance of equity capital from strategic and financial buyers.

- Private equity firms have significant funds available for transactions and many strategic buyers have cash reserves and excess credit availability. That said, buyers are generally increasing the level of due diligence for transactions given the full valuations currently being paid for quality companies.

- There also continues to be historically low interest rates for debt financing and significant competition among lenders, which is expected to continue during 2018.

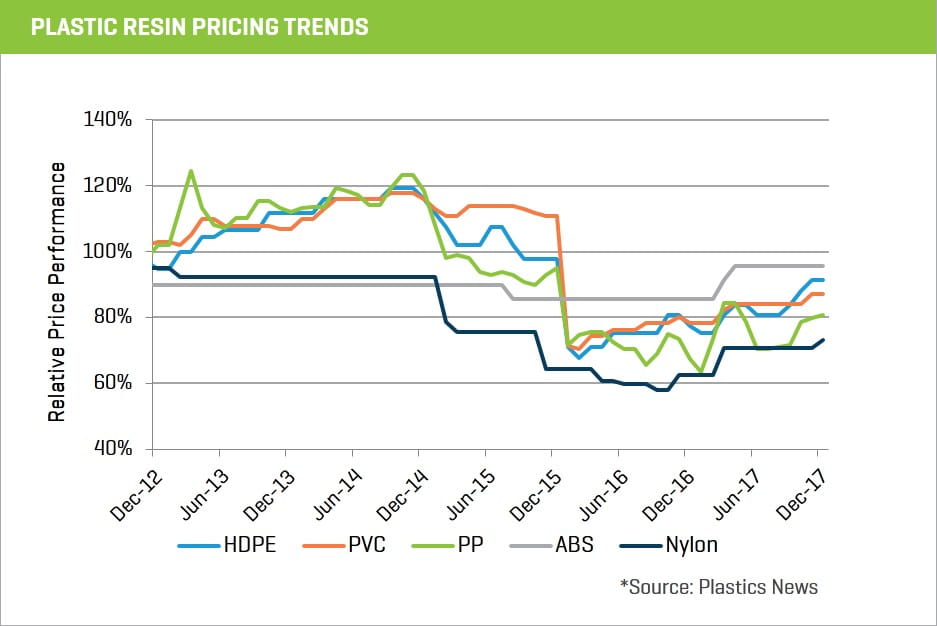

- Crude oil prices increased approximately 12% during 2017, from $54 to $60 per barrel, while natural gas prices ended the year essentially flat. Certain resin prices also experienced increases during 2017.

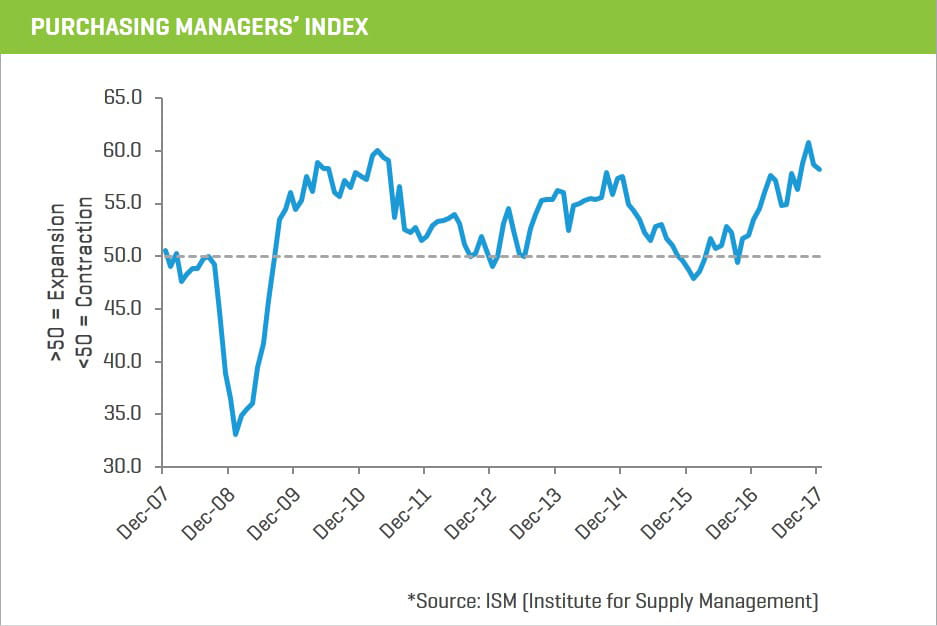

- Positive macroeconomic trends and an overall strong U.S. economy continued in 2017, which bolstered the M&A market and benefited many companies within the plastics industry. In addition, the Institute of Supply Management Purchasing Managers’ Index (PMI), an indicator of the economic health of the manufacturing sector, expanded throughout 2017.

Trend Data Highlights Opportunities and Challenges

Plastics M&A Activity Reveals Wide Range of Deal Opportunities

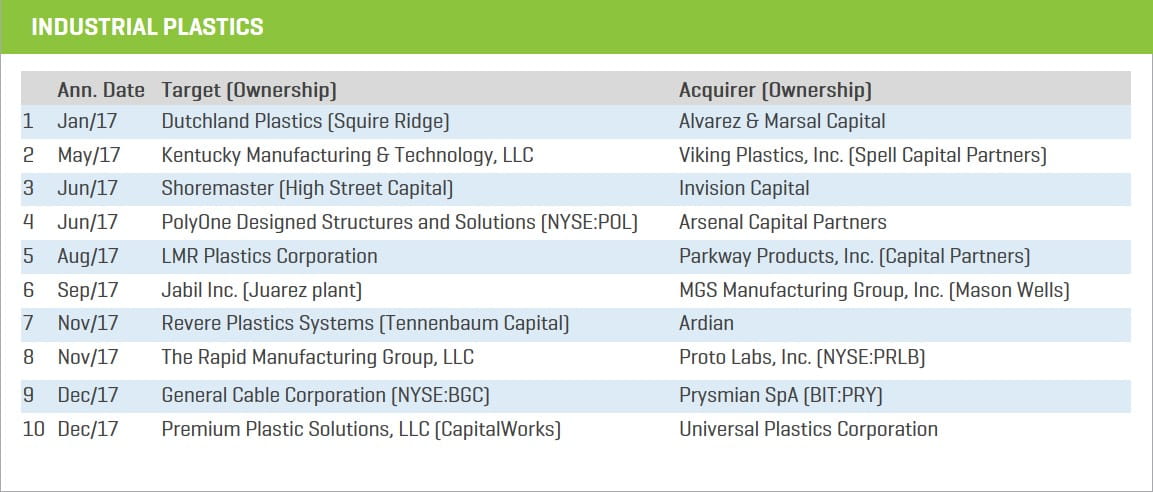

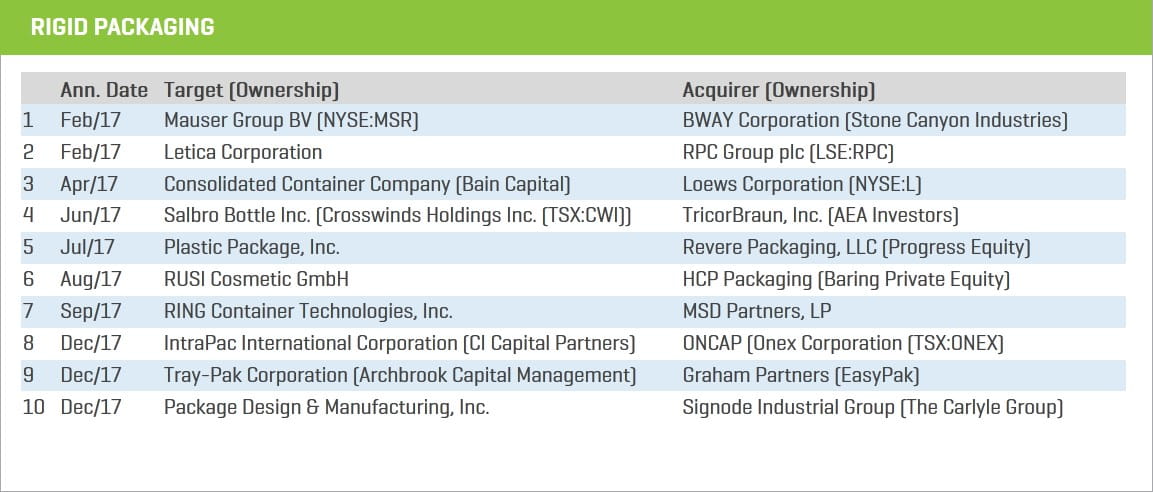

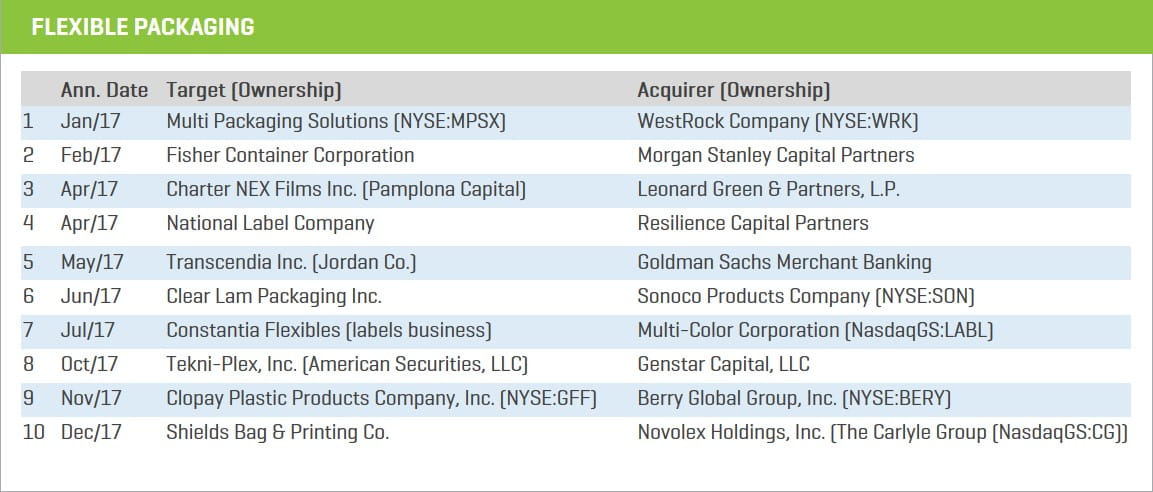

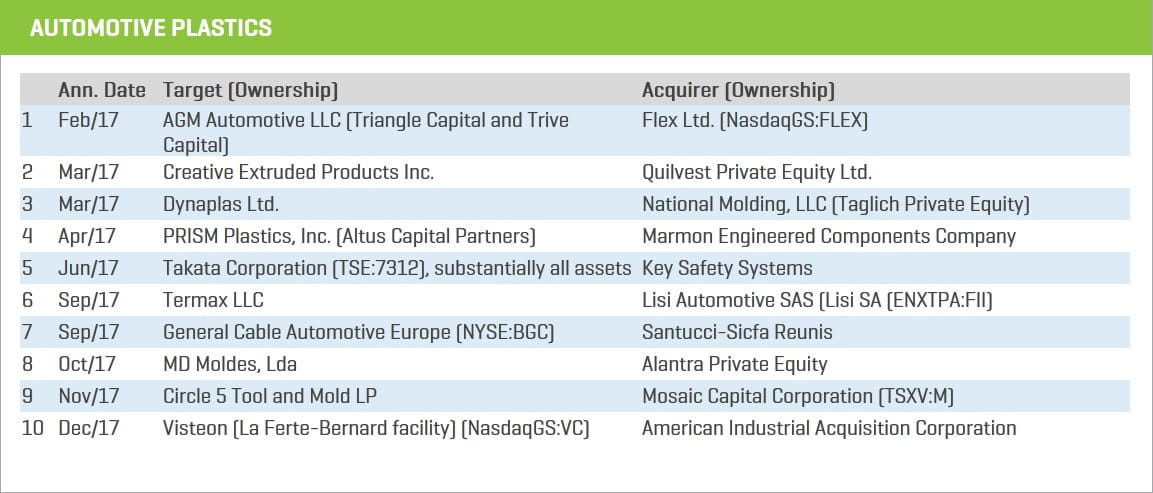

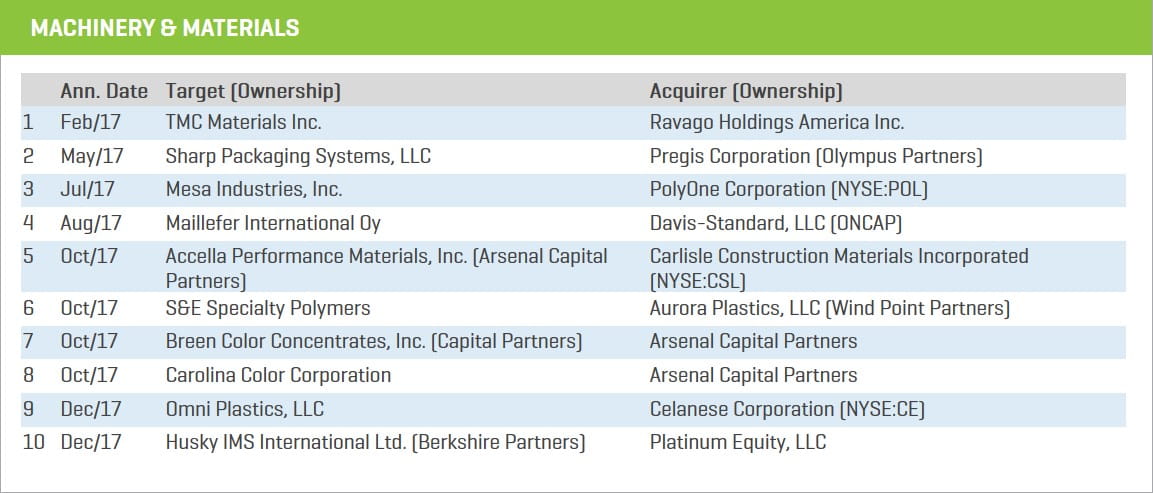

Select 2017 Plastics Industry Transactions

Public Company Valuations and Margins Remain High

Plastic Resin Prices Show Stability

Macroeconomic Indicators Remain Positive

Stout’s Proprietary Transaction Data Key to Comprehensive Plastics Industry Reporting

This Plastics Industry Update is exclusive to Stout Capital, LLC (Stout) and is the most comprehensive report available in the industry. The report is based on proprietary data collected annually by Stout on several hundred relevant deals. This data becomes part of an exclusive transaction database that facilitates in-depth analysis and reports utilizing a myriad of data subcategories. Stout has invested in this unique asset for our customers and the industry for the past several years.