English

English

The IRS is pushing back against the size of acceptable undivided interest discounts in real estate, particularly with respect to situations involving disparate ownership positions. The Service argues that the discount is constrained by the potential premium an owner of a majority undivided interest would pay to purchase the minority undivided interest.

Undivided interests in real estate suffer from a variety of relatively unattractive economic ownership characteristics. These characteristics contribute to the reduced desirability of these ownership interests when compared to fee-simple interests and leave the undivided interest owner with few options with respect to achieving liquidity, which include locating another willing investor, or conducting a potentially protracted and expensive partition lawsuit.

An Offer You Can’t Refuse?

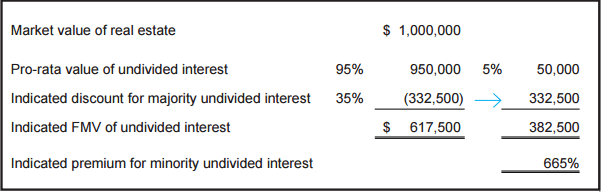

The Service claims they frequently review cases involving unsupportable discounts (e.g., 35% - see table below) applied to large majority undivided interests in real estate. As a result, the IRS has developed a model highlighting a third option for a majority interest owner to achieve liquidity. Consider an example whereby two co-tenants own 95% and 5% undivided interests, respectively. As an alternative to accepting a 35% discount, the Service argues that the 95% owner could simply offer the 5% owner a significant premium (relative to his pro-rata value) to incentivize him to sell. The 95% owner would then own the entire property and would be able to sell it outright and maximize value.

Knowing that if he rejects the offer, the 5% owner may face a significant deterioration of value to the extent a judicial partition process is pursued. This is particularly detrimental for small minority undivided interest owners in states (such as Michigan) where default law specifies costs are not split equitably based on ownership percentage, but are borne individually.

The following tables illustrate the Service’s minority premium argument. To the extent the 95% owner is indifferent between pursuing a partition process (resulting in a 35% discount) or offering this reduction to buy out the 5% owner, a 665% premium to the pro-rata value of the 5% owner would result.

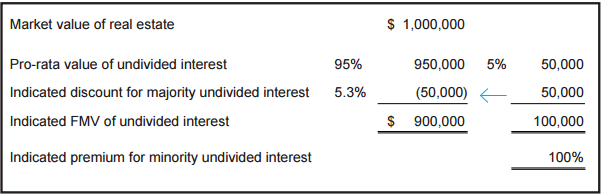

The Service uses this example to test the validity of the estimated discount. Citing traditional acquisition premium studies, the Service proffers that a 100% premium may be necessary to incentivize a very small percentage owner to induce a transaction and that a larger minority owner may require a lesser premium, say 30% to 50%, for example. Assuming a 100% premium would be sufficient to compel the 5% owner to sell, the implied discount to the pro-rata value of the 95% interest would be 5.3%, as illustrated in the following table, using the IRS’ purported logic.

Some of the assumptions made by the Service in its arguments on this issue are flawed. For one, the IRS’ argument relies on assumptions regarding a host of economic motivations by each of the co-tenants that would purportedly lead to a series of hypothetical transactions in the future, a stance that previous Court decisions have rejected1. In addition, the facts and circumstances of a particular case may dictate that a buyout of the small minority interest is unlikely under any circumstances, or that a significant premium (i.e., even at levels in the prior example of over 500%) would be negotiated given the relative bargaining strength of the buyer and seller.

Regardless, the framework presented by this model certainly warrants consideration. Discounts perceived to strain credibility will be drawing greater attention by the Service and the minority premium argument, to the extent not addressed properly, may be viewed favorably by the Court resulting in lower discounts.

In order to make the entire IRS argument moot, estate planners may want to advise clients to establish ownership positions in equal size blocks (e.g., two 50% owners, three 33.3% owners, four 25% owners, etc.) when possible in structuring a transaction for estate planning purposes. This type of ownership structure limits the ability of the Service to employ a control premium model given that the IRS’ presumed incentive of a buyout would not necessarily be advantageous to any of the owners.

1 For example, in Simplot, the Appeals Court reversed a fully reviewed Tax Court decision which had determined that a large premium existed for a 24% minority interest in voting common stock. In its opinion, the Appeals Court ruled that the Tax Court departed from the hypothetical willing buyer standard apparently because it believed that “the hypothetical sale should not be constructed in a vacuum isolated from the actual facts that affect value.” Obviously, the facts that determine value must be considered. The facts supplied by the Tax Court were imaginary scenarios as to who a purchaser might be, how long the purchaser would be willing to wait without any return on his investment, and what combinations the purchaser might be able to effect… In violation of the law, the Tax Court constructed particular possible purchasers. As a result, the Appeals Court overturned the decision in favor of the estate. (See Estate of Simplot v. Commissioner, Ninth Circuit, No. 00-70013, May 14, 2001).