English

English

The U.S. youth sports industry has quietly become a multi-billion-dollar ecosystem and continues to grow at 8–10% per year. Beneath this expansion lies a rare convergence of fragmentation, predictable recurring spend, and accelerating digital transformation that together make youth sports a highly investable category. The sector is evolving from a cottage industry into a scalable, tech-powered platform economy. For investors, this represents a rare opportunity to capture growth in an emotionally durable, economically resilient, and still largely untapped market.

Since 2020, the youth sports industry has gone through a dramatic, two-stage transformation: an initial, painful contraction driven by pandemic lockdowns followed by a rapid rebound and structural acceleration that has attracted significant institutional capital.

The Last Five Years

The early shock of 2020 forced cancellations of leagues, camps, and tournaments, shuttered training facilities, and sent participation plunging. That shock was acute but short lived in many segments.

By 2022–2023, consumer demand returned and in several sub-segments — travel tournaments, specialized elite training, tech platforms that enable registration/communications/streaming, and event operators — the business model grew larger and more monetizable than before COVID.

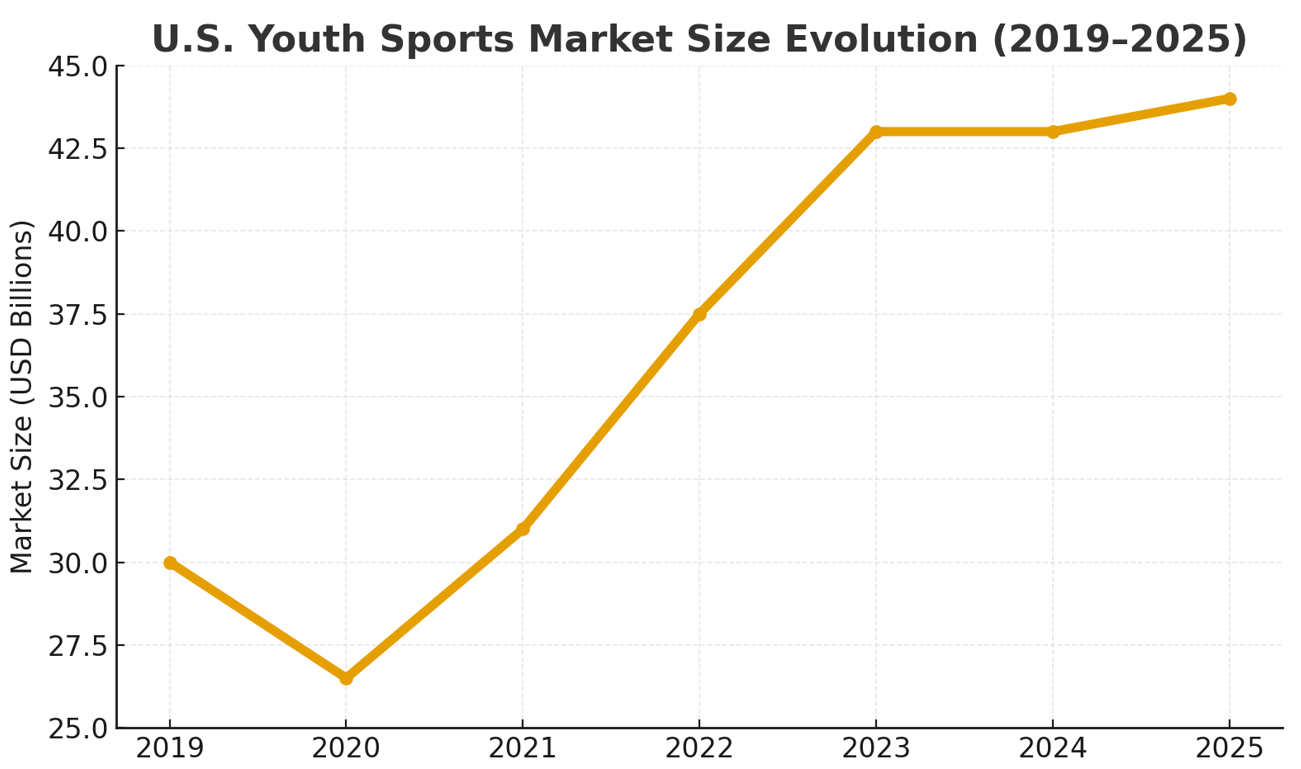

Global spending on youth sports, which fell sharply in 2020, reached record levels by 2023 with the U.S. accounting for most of the rebound; one data point summarizing this trajectory shows global spending reaching roughly $64 billion in 2023 with the U.S. portion topping $43 billion.

Why the Resurgence?

Household economics explain much of this resurgence. Parents have demonstrated a greater willingness to pay for organized youth sports, and per-family spend increased noticeably in the post-COVID years.

The Aspen Institute’s Project Play family survey found that the average U.S. sports family spent about $1,016 on their child’s primary sport in 2024, an increase of roughly 46% compared with 2019, while total annual outlays per child (counting multiple sports and ancillary costs) commonly reach significantly higher levels.

This change in parental spending behavior has translated directly into more stable revenue streams for clubs, tournament operators, camps, and specialty service providers such as private coaches and skills academies.

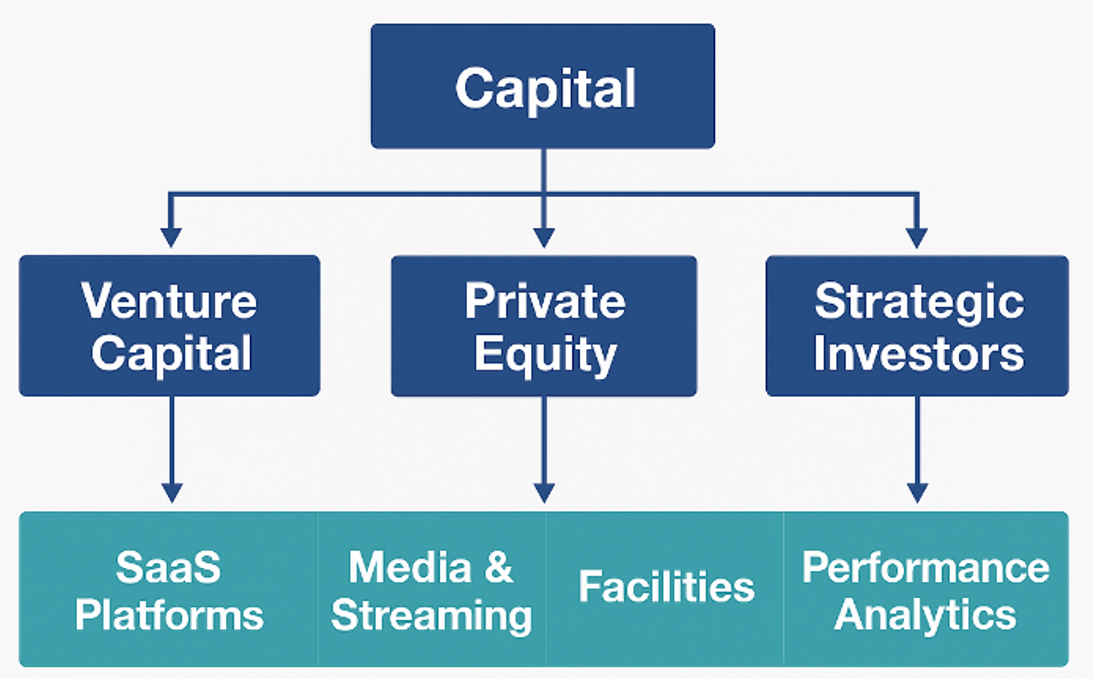

Institutional and Private Equity Interest

Institutional and private equity interest has followed the money. Large, well-publicized transactions make the trend obvious. For example:

- The acquisition of IMG Academy by BPEA EQT in partnership with Nord Anglia in 2023 at approximately $1.25 billion signaled an appetite for premium training and campus-based sports education assets that combine real estate, seasonal programming, and recurring tuition revenue

- KKR’s agreement to acquire Varsity Brands from Bain Capital for about $4.75 billion in 2024 underlined private equity attraction to vertically integrated apparel, uniform, competition, and event businesses that generate steady order flows and have strong product line margins

Growth equity and PE have been equally active in the tech stack, for example:

- TeamSnap took a majority growth partner (Waud Capital) in 2021 to accelerate product development and M&A

- In 2025, Genstar Capital backed the combination of PlayMetrics and Stack Sports to create a consolidated leader in sports-management software — an explicit roll-up of registration, league management, and club services

These deals reflect two simultaneous investment theses: buy premium consumer experiences (camps, academies, large event brands) and consolidate high-margin technology platforms that can scale and provide operating leverage across local businesses.

Revenue Dynamics

Revenue dynamics within the sector vary by sub-segment.

Tech/SaaS

Technology platforms and SaaS products that enable registration, scheduling, communications, and live/video services can show high revenue growth and attractive gross margins. Platform play and streaming investments are a good example, like the growth of Dick’s Sporting Goods’ GameChanger, which by some accounts was projected to produce meaningful revenue and engage millions of users annually.

Events/Tournaments

Event and tournament operators capture registration fees, sponsorships, and travel-driven ancillary revenue that scale quickly when national or regional circuits are built.

Franchises/Programs

Franchise and program businesses (multi-location academies, camps, and enrichment brands) generate relatively predictable tuition and membership revenue. When those companies consolidate, they unlock procurement benefits, centralized marketing, and cross-sell of higher-margin services.

Apparel/Equipment

Meanwhile, apparel and equipment companies such as Varsity/BSN retain steady product revenue with the added upsell of uniforms and competition merchandise throughout the season.

Competition in the Sector

Competition is fragmented and multi-layered. At the local level, there are thousands of clubs, recreational leagues, small academies, and independent coaches competing primarily on price, convenience, and perceived coaching quality.

At the regional and national level, event organizers and tournament circuits compete for prestige, ideal dates/venues, and travel teams. National incumbents include tech platform companies (TeamSnap, Stack Sports/PlayMetrics, SportsEngine/NBC Sports Next) that provide the plumbing for many smaller operators and therefore benefit from network effects and stickiness.

Apparel and equipment providers (BSN/Varsity and large retailers) compete on wholesale distribution and brand relationships with schools and clubs. Newer entrants, such as start-up platforms focused on livestreaming, automated highlights, analytics, and sponsorship marketplaces, are attacking adjacent revenue pools and creating new monetization pathways for clubs and parents.

This landscape means that scale matters: larger platforms can bundle services (registration, payments, streaming, sponsorship sales) and present a one-stop experience that is harder for a single local club to replicate.

Looking Ahead

Looking ahead three to ten years, the market is likely to follow several intertwined trajectories.

The Near Term

In the near term (three years), consolidation of service providers and platforms will accelerate. Private equity and strategic buyers will continue to pursue roll-ups of regional club networks, tournament operators, and tech platforms to extract cost synergies and centralize functions such as payments, procurement, and marketing.

Platform consolidation will create a smaller set of robust SaaS providers that serve as the operating systems for youth sports. Investors will prize companies that demonstrate recurring revenue, low churn, disciplined customer acquisition (CAC), and strong unit economics.

Evidence for this near-term consolidation thesis is already visible in recent transactions where private equity firms have combined or invested in platform plays and event portfolios.

The Future of Capital Flow in the Youth Sports Industry

The Next 5-10 Years

Over a slightly longer horizon (5–10 years), the sector will bifurcate between commoditized participation offerings and premium, differentiated experiences. Commoditized activities (basic recreational leagues and local clubs) will face price pressure and margin compression because of competition and lower barriers to market entry. Premium camps, elite academies, and branded national tournament circuits will consolidate higher spending families and sponsors and will be valued more highly by investors.

Technology will be a force multiplier: analytics, athlete development platforms, automated highlights, and content monetization will enable companies to extract additional lifetime value from athletes and their families, and to create new sponsorship and media revenue.

Digital products that drive engagement (streaming, highlights, coaching content) will play a growing role in monetization and fan development.

Risks Shaping Outcome

Two risks will shape outcomes. First, affordability and access remain politically and socially sensitive; continued increases in per-child cost risk participation substitution or attrition among lower-income families, which could limit top-line growth if left unaddressed.

Second, regulatory, safety, and liability issues (coach background checks, concussion protocols, and facility standards) will require sustained investment and can slow roll-up velocity if integration cannot quickly meet compliance thresholds. Companies that can demonstrate both inclusive pathways (scholarships, lower-cost offerings) and robust compliance frameworks will be advantaged in M&A processes.

Outlook

Youth sports is evolving from a local, fragmented pastime into a digitally monetized, media-rich ecosystem. The convergence of NIL rights, streaming technology, AI analytics, and platform consolidation is expanding the market’s economic ceiling and accelerating professionalization.

Investors positioned at this inflection point can capture value from an industry moving beyond participation fees into content, data, and technology-driven monetization — a structural evolution that mirrors the early-stage digitization of traditional sports, fitness, and entertainment sectors.

This article was originally published in Youth Sports Business Report.