English

English

When Bluetooth technology was conceived two decades ago, no one could have predicted that automotive original equipment manufacturers (“OEMs”) would use it to provide consumers a seamless connection with their vehicles. What started as hands-free voice control has evolved into technology that enables other semi-autonomous capabilities, such as collision avoidance, self-parking and adaptive cruise control. But automotive and technology companies are not content to stop there. The terminus in the automotive technology evolution is the development of fully autonomous (i.e., self-driving) vehicles.

Self-driving cars might seem like something out of The Jetsons, but revolutionary technological advances unimaginable just a short time ago are now very real and occurring with increasing frequency. Competition challenges OEMs and their suppliers to be first to market, and the need to accelerate engineering and research and development (“R&D”) efforts rapidly has led to a spike in merger and acquisition (“M&A”) activity, whereby established automotive industry participants acquire innovative technology-focused entities.

This article describes the unique challenges automotive companies face as they integrate and account for these transactions, and addresses certain complexities inherent in measuring the fair value of nascent technologies that do not yield immediate economic benefits.

The Past: Manufacturing efficiencies and globalization

Over the past decade, OEMs have undertaken significant investment and restructuring initiatives to improve their manufacturing efficiencies and capture new sales in emerging markets (e.g., Mexico, South America, Asia). Global automotive demand has risen significantly, spurring OEMs to compete to capture market share. In order to streamline manufacturing and distribution costs, OEMs have relocated their production facilities closer to the expanding customer base in emerging markets. Additionally, to make their manufacturing and distribution more efficient, OEMs have initiated plans to reduce the number of global platforms. For example, Ford Motor Company (“Ford”) plans to reduce its 27 global platforms as of 2007 to a future target of eight,1 and General Motors Corporation (“GM”) plans to reduce its current offering of 26 to four by 2025.2

Automotive part and system suppliers that understood and were ready to contribute to OEMs’ globalization pursuits were best-positioned to win contracts for new platforms from OEMs. Many suppliers carved out an advantage by moving their manufacturing facilities to emerging markets, just like OEMs have done. M&A transactions between traditional automotive supply businesses enabled these moves.

The Present: The development of technologically advanced vehicles

Technology has usurped globalization as the most significant trend in the automotive space. A decade ago, suppliers took their cues from OEMs; today, OEMs and suppliers must respond to consumers. OEMs and suppliers’ edge now comes from developing technologically advanced products likely to meet consumer demands over the coming years.

Automotive companies understand that today’s consumers are more connected than ever to smartphones and tablets. At this year’s Consumer Electronic Showcase (“CES”), automotive companies took center stage, relegating the perennial technology stars — Microsoft, Google and Apple – to side acts. This year’s hottest technology was autonomous driving, though connectivity was also popular. At CES, Bayerische Motoren Werke AG (“BMW”) proved just how technologically advanced its i Vision Future Interaction connectivity concept is.3 The concept allows drivers to communicate with their vehicles and devices without physical interaction; they need only make simple hand movements.

CES also demonstrated how OEMs are partnering with technology companies, including Apple, Google and Amazon, to ensure that their vehicles contain information systems whose features are compatible with consumer devices. For example, Ford demonstrated how consumers can use Amazon Echo and Wink to communicate with their vehicles.4

Consumer connectivity comes with a significant downside: distracted driving. In response, the automotive industry is developing safety technologies to combat distracted driving, including 360-degree-view cameras, blind-side warnings and audio text reading. Vehicles equipped with these safety technologies warn drivers of unexpected road conditions and help drivers avoid collisions. For example, Delphi Automotive PLC’s Adaptive Cruise Control system contains sensors that read road conditions and adjust the vehicle’s speed accordingly, thereby maintaining a safe radius around the vehicle.5 Such semi-autonomous options and their related sensor technologies put the automotive industry one step closer to creating fully autonomous vehicles.

The Future: The fully autonomous self-driving vehicle

Drivers use increasing amounts and types of technology to control their vehicles, and OEMs, suppliers and technology companies are rapidly developing software and applications to enable driverless vehicles. Concerns about safety, however, could cause the public to hesitate in the acceptance of these vehicles, especially given the recent occurrence of the first fatality in a vehicle crash involving autonomous technologies.6

In pursuit of autonomous technologies and vehicles, automotive and technology companies are collaborating on development and production. For example, in July, BMW, Intel and Mobileye announced their partnership to develop a fully autonomous vehicle by 2021.7 Regardless of public perception and the current lack of clarity regarding a regulatory framework for these vehicles, automotive companies are confident that fully autonomous vehicles, which are projected to be a $42 billion industry by 2025,8 are the future of the industry, so they are adopting strategies accordingly to meet changing consumer demands and lifestyles.

Planning for the Future: In-house development vs. M&A

”With engineering, I view this year’s failure as next year’s opportunity to try it again. Failures are not something to be avoided. You want to have them happen as quickly as you can so you can make progress rapidly.”

Gordon E. Moore, Co-founder and Former Chairman, Emeritus of Intel Corporation, May 2000

This quote from Mr. Moore (who famously predicted in 1965 that computer processing power would double every other year) may be 16 years old, but it applies to current automotive technology trends. As new technologies continue to enter the automotive industry, companies must embrace the failures of today’s technologies and research new technologies to shape future developments in connectivity, safety and autonomous driving.

Automotive companies historically were not strategically positioned to develop technological innovations as quickly as consumer product companies like Apple and Samsung. Consequently, developing autonomous technologies in-house proved costly for automotive companies not only in terms of actual expense but also — and more important — in terms of time to market. With this recognition, automotive companies have engaged in M&A transactions to accelerate their R&D capabilities. The target companies are already developing innovative technologies with automotive applications, so automotive companies’ acquisition of in-process research and development (“IPR&D”) is a primary — and sometimes singular — rationale for these transactions.

Changing Asset Compositions: From customer-related assets to IPR&D

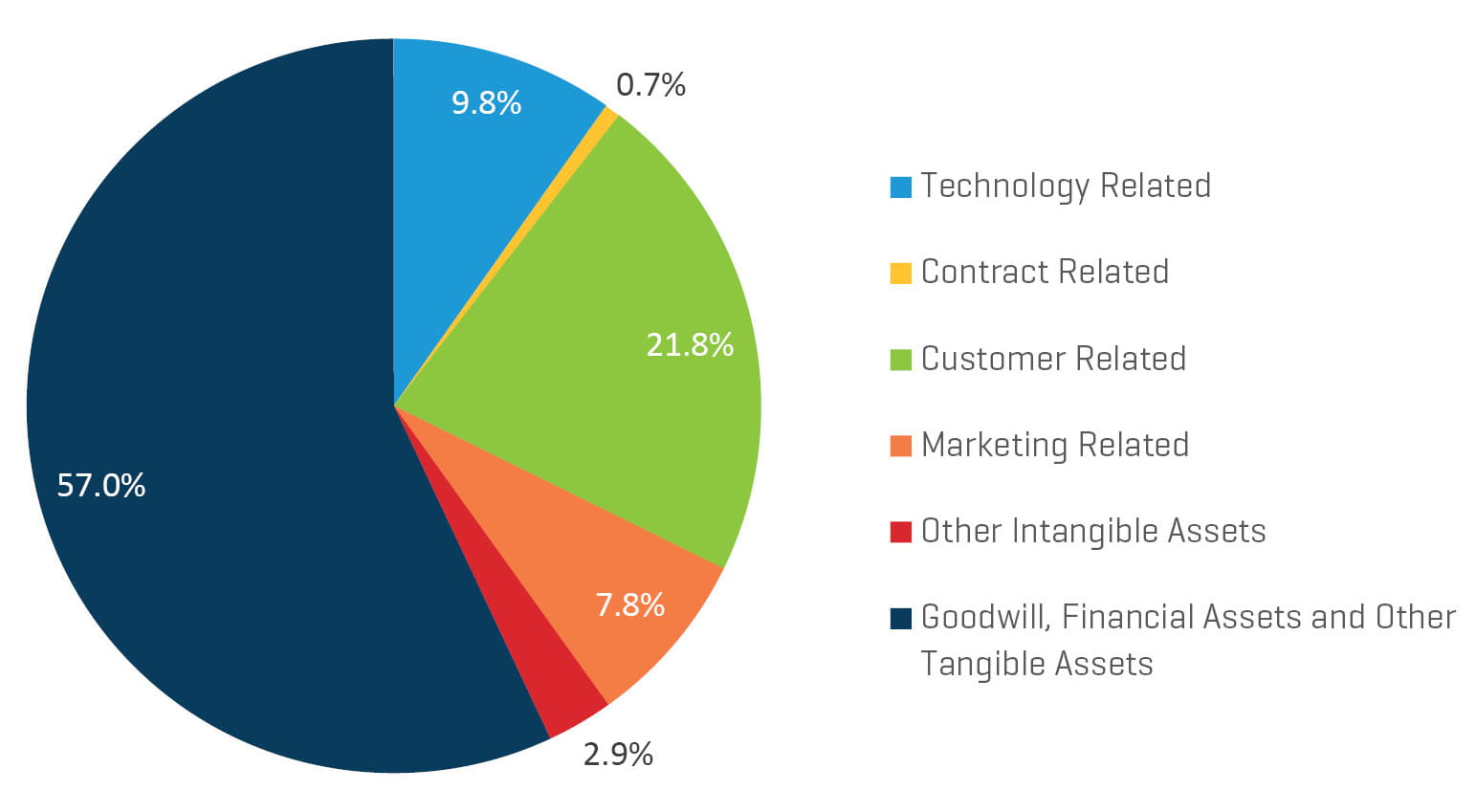

As the automotive industry continues to focus on the development of innovative technologies, there is likely to be an increase in technology-related intangible assets ascribed value in purchase accounting (also referred to as purchase price allocations [“PPAs”]). A 2010 study by KPMG indicated that customer-related intangible assets were the primary asset acquired in automotive PPAs, as indicated in Figure 1.9

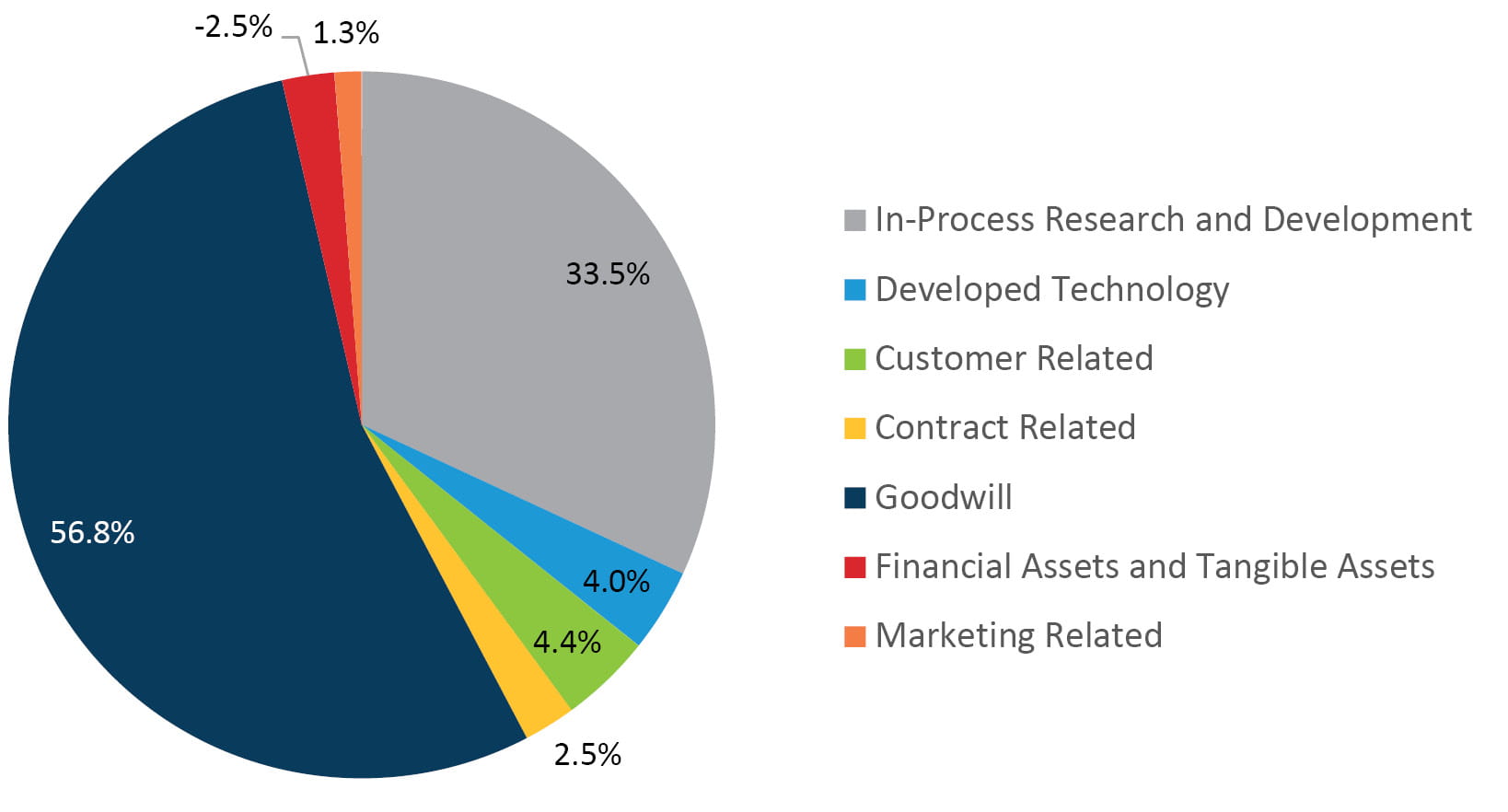

Customer-related intangible assets will continue to be a primary asset in transactions of established automotive companies with traditional manufacturing capabilities, but an increase in technology-related intangible assets is likely. In transactions involving only R&D activities, technology-related intangible assets will likely account for all identified assets. Figure 2 highlights this trend, providing data from six recent technology-driven transactions in which Stout was involved.

Figure 1: Allocation of Total Net Assets in Automotive PPAs

Source: Intangible Assets and Goodwill in the Context of Business Combinations: An Industry Study, KPMG International; 2010

Figure 2: Allocation of Total Net Assets in Automotive PPAs Related to Technology

Source: Stout internal work papers

Stout’ data shows that technology-related intangible assets (i.e., IPR&D and developed technology) accounted for more than a third of the intangible assets ascribed value in the six deals, indicating the acquiring companies’ drive to accelerate R&D.

This transition in value attribution introduces more complexity, thereby requiring more specific valuation expertise. For example, forecasting the timing of commercialization and revenue generation related to IPR&D is tenuous and can be difficult. Furthermore, transactions with significant IPR&D tend to include more complex transaction structures with contingent consideration, such as milestone payments predicated on future technological achievements.

Unraveling the Uncertainties: Selecting the valuation methodology for IPR&D

Financial Accounting Standards Board Accounting Standards Codification (“ASC”) Topic 820, Fair Value Measurement (“ASC 820”), outlines generally accepted accounting principles (“GAAP”) in the United States for determining the fair value of assets, including those acquired in a business combination. ASC 820 terms fair value as “the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.”10 Further, ASC 820 outlines three fundamental methods to valuing intangible assets — the cost approach, the market approach and the income approach — that companies can contemplate based on the relative merits of each considering the nature of the subject asset and the facts and circumstances surrounding it.

Cost approach

Under the cost approach, the replacement cost method is used for valuing IPR&D. An analysis of the various costs that a company would expect to incur is performed in order to re-create an asset of equivalent functional utility. Traditionally, this approach is appropriate for established, developed technologies. Given the significant anticipated benefits of autonomous IPR&D, however, this method will likely undervalue the acquired asset. As such, the cost approach is not frequently employed as a primary valuation method of IPR&D in technology-driven automotive PPAs, but it may be useful as a confirmation of reasonableness.

Market approach

The market approach uses prices and other relevant metrics generated by transactions involving identical or closely comparable assets in the marketplace. Given that technology-related assets are typically sold in connection with operating businesses, not individually, limited market data exists for use of this valuation method in this context, and the market approach is typically not employed in the valuation of IPR&D.

Income approach

Under this approach, we may consider the relief from royalty method, which is a hybrid method that reflects certain market considerations, or the multiple-period excess earnings method (“MPEEM”) to value IPR&D. The relief from royalty method measures the benefit of owning intellectual property as the “relief” from the royalty expense that would otherwise be incurred by licensing the asset from a third party. Selecting an appropriate royalty rate usually involves researching market transactions for similar proprietary technology. As previously stated, limited market data exists for autonomous automotive technologies, so it is difficult to support the inputs necessary to employ the relief from royalty method in the valuation of IPR&D.

The MPEEM identifies streams of revenue and expenses for a particular asset group. The prospective earnings associated with the subject asset are then isolated from the overall business by identifying and deducting portions of the projected economic benefits attributable to assets that contribute to the revenue-generating effort of the IPR&D. Next, the remaining earnings, or “excess earnings,” attributable solely to the subject asset are derived. In essence, the MPEEM considers the future revenue and expenses of the IPR&D once the technology has been commercialized.

In many cases, the IPR&D in and of itself does not produce standalone cash flows. As such, it might be necessary to introduce contributory asset charges for benefits (e.g., a pre-existing brand name, access to an OEM) the acquirer brings to the equation. In addition, IPR&D typically requires further application-specific design and development — and the associated costs, of course — to determine how the acquired technology can be incorporated into a larger autonomous driving system. The system itself often must be engineered to the specifications of automotive production standards, resulting in significant engineering and capital costs.

Using MPEEM to value IPR&D

The first step in IPR&D valuation is to investigate whether the acquired technology will be separable into multiple groupings or measured as one asset category. This analysis contemplates the anticipated future revenue streams associated with the IPR&D and the timing of each. Once the projected revenue stream associated with the IPR&D is isolated, expected revenues are adjusted by applying an economic depreciation rate, which reflects the expected rate of decay or loss in value over time of the subject intangible asset.

As stated previously, Moore predicted that computer processing technology would double every two years. Along these same lines, an economic depreciation rate is applied to estimate the continued evolution of innovative automotive technologies — and to reflect the reality that technology acquired on a certain transaction date will become functionally obsolete as new breakthroughs are made. The economic depreciation rate should be based on the estimated remaining useful life of the applicable technologies (once commercialized), which can be relatively short given the rapid pace of advancement.

Next, an applicable earnings margin attributable to the IPR&D is estimated. An appropriate earnings margin should consider the future R&D costs necessary to achieve commercialization, as well as ongoing required engineering costs. Additionally, contributory asset charges associated with other assets (i.e., net working capital, fixed assets, intangible assets [e.g., assembled workforce]) that support the production of cash flows associated with the IPR&D are subtracted from the projected earnings stream to derive the excess earnings associated with the subject intangible asset.

Finally, cash flows are discounted to a present-value equivalent by applying a rate of return commensurate with the risk associated with achieving the prospective cash flows. Given their innovative nature and stage of development, these technologies generally warrant discount rates that approach those required by venture capital investors, which are supported in practice by the calculated internal rate of return implied by a specific transaction and a review of relevant studies on venture capital rates of return.

Unlike other less-flexible valuation approaches, the MPEEM makes it possible to address the uncertainties and risks of IPR&D through the application of certain inputs. By factoring in startup R&D expenses and ongoing engineering expenses, the MPEEM calculates an earnings margin that reflects the uncertainties pertaining to the development cost of the innovative technology. Additionally, the application of economic depreciation and discount rates address the risks associated with the timing of commercialization and achieving the projected cash flows.

The distinction between developed technology and IPR&D relates to the stage of development. If the acquired technology is not commercialized as of a transaction date, it qualifies as IPR&D for purchase accounting purposes. For suppliers, the litmus test typically comes when the technology associated with the IPR&D is employed upon award of a contract to work on a specific platform. Subsequent to purchase accounting, IPR&D is not amortized but rather tested for impairment annually until it is commercialized. Upon commercialization, the IPR&D will be amortized over its estimated remaining useful life. If the R&D efforts were discontinued, the IPR&D would become fully impaired.

Conclusion

Stout’ data and experience in recent technology-driven acquisitions show that OEMs and automotive suppliers will encounter increasingly complex accounting and integration challenges as they engage in M&A transactions with technology companies and incorporate those companies’ new technologies in their operations. Technology-driven M&A transactions could raise issues the automotive industry has never before encountered, so OEMs and suppliers need to be proactive in the valuation exercise in order to avoid unwarranted balance sheet and income statement volatility.

Also contributing to this article:

Jacob Smyth

Analyst – Valuation Advisory

+1.248.432.1348

jsmyth@stout.com

- Product Excellence and Innovation, Mark Fields and Raj Nair, Ford Motor Company; 2015.

- GM’s 2025 Platform Plan: Simplify and Seek to Save Billions, Ben Klayman and Paul Lienert, Thomson Reuters Corporation; October 2, 2014.

- Hottest Cars and Automotive Tech from CES 2016, Consumer Reports; January 10, 2016.

- Ibid.

- Delphi Adaptive Cruise Control, Delphi Automotive PLC.

- Consumer Reports Urges Tesla to Disable Auto Steering, CNBC LLC; July 14, 2016.

- BMW to Develop Driverless Car Technology with Intel, Mobileye, Edward Taylor, Thomas Reuters Corporation; July 7, 2016.

- Driverless-Car Global Market Seen Reaching $42 Billion by 2025, Jeff Green, Bloomberg L.P.; January 8, 2016.

- Intangible Assets and Goodwill in the Context of Business Combinations: An Industry Study, KPMG International; 2010.

- Financial Accounting Standards Board Accounting Standards Codification 820-10-05.