English

English

Introduction

Enterprise value (“EV”) represents the sum of debt plus equity. Given this relationship, equity is equal to EV minus debt, right? Unfortunately, it’s not always that simple.

A company’s stage of development and the makeup of its capital structure can pose oft overlooked valuation challenges, particularly when measuring equity value of a private company for purposes of financial or income tax reporting. For example, measuring the equity value of a private company may be required when marking a private equity investment to market or complying with Internal Revenue Code (“IRC”) Section 409A when issuing stock options as compensation to employees. If the subject company’s capital structure is highly leveraged or consists of security classes more complex than plain-vanilla debt and equity (e.g., convertible preferred stock), the valuation professional must apportion EV to each security class based on the rights and preferences thereof. This article outlines three prevailing approaches to allocating a company’s value, including two forward-looking approaches that have gained acceptance in recent years.

Overview of Value Allocation Techniques

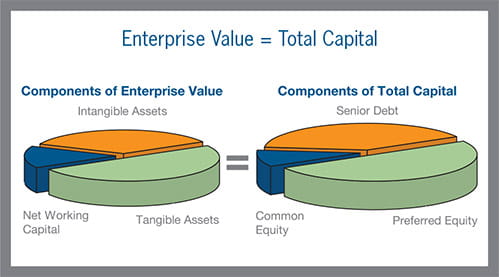

Common equity reflects a residual interest in a company’s value after considering senior securities such as debt. Typically, valuation analysts determine common equity value by first valuing the business as a whole, and then subtracting the values of securities senior to common equity in the capital structure. For example, debt and straight preferred stock are usually subtracted from EV to derive common equity value. This method of allocating EV is referred to as the Current Value Method. A chart illustrating typical components of EV and total capital is presented below.

By its very nature, the Current Value Method assumes that the company is sold at the valuation date and the proceeds are distributed in accordance with investors’ liquidation rights. This approach may be the most applicable scenario in certain circumstances, but most companies operate as going concerns without an imminent liquidity event (e.g., a sale of the company, an initial public offering (“IPO”), or liquidation).

There are two other generally accepted methods of allocating a company’s value to the various components of its capital structure.These methods, which are described in the American Institute of Certified Public Accounts (“AICPA”) practice aid, Valuation of Privately-Held-Company Securities as Compensation (the “Practice Aid”), are based on two key premises. First, the value of each class of securities should result from the security holders’ expectations about future economic events and the amounts, timing, and uncertainty of future cash flows. Second, at least some nominal value must be assigned to the common shares unless the enterprise is being liquidated and no cash is being distributed to the common shareholders (i.e., there exists option value). These value allocation methods are:

- Probability-Weighted Expected Return Method (“PWERM”): The PWERM estimates common equity value based upon an analysis of various future outcomes,such as an IPO, merger or sale, dissolution, or continuedoperation as a private, viable ongoing enterprise. The allocated value is based upon the probability-weighted present values of expected future investment returns, considering each of the possible outcomes available to the enterprise, as well as the rights of each security class.

- Option Pricing Method: The Option Pricing Method treats equity as a call option on the enterprise’s value. The value of equity is based on the optionality overand- above the value of securities senior in the capital structure (e.g., senior debt).

PWERM Example – Early-Stage Company with Convertible Preferred Stock

Capital structures involving multiple classes of securities (generally with conversion features) are often found in start-up enterprises funded by venture capital. Typically, investors receive preferred stock for cash investments in the enterprise, whereas initial issuances of common stock are primarily granted to founders for nominal (or no) cash consideration. In addition, employees are often granted options to purchase the enterprise’s common stock.

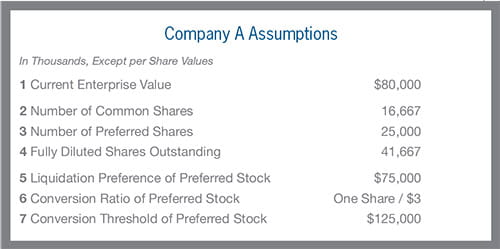

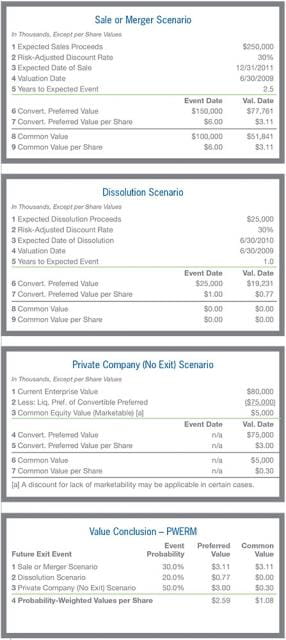

In this example, Company A is a technology company that is working on a revolutionary Internet-based advertising platform. Company A’s investors have no imminent expectation of a liquidity event, although management is targeting a sale or merger with a larger competitor in two to three years. Currently valued at $80million, Company A has raised $75 million in preferred stock convertible into 25 million common shares at a conversion price of $3.00 per share. It also has 16.7 million com shares and penny warrants outstanding. Based on these assumptions, the Current Value Method suggests a marketable value per common share of $0.30 (calculated as EV less the liquidation preference of preferred stock divided by the number of common shares outstanding).

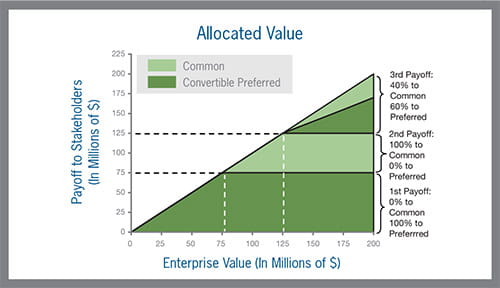

An analysis of Company A’s business plan, as well as comparable merger and acquisition (“M&A”) transactions, suggests that if the company successfully executes its business plan it could be sold in two to three years at an EV of $250 million. However, Company A’s industry is highly competitive and there exists significant risk that its business plan might fail. In that event, it is estimated that the company could be liquidated for $25 million. Further, as illustrated in the following chart, it is economically advantageous for the company’s preferred shareholders to convert to common shares above the $125 million value threshold (calculated as the number of fully diluted shares outstanding multiplied by the preferred stock conversion price) as the sales proceeds on a converted, fully diluted basis would be greater than the liquidation preference of the preferred stock.

The PWERM is employed in a multi-step process, with the first step requiring an estimation of future possible outcomes available to the enterprise. As described above, this example considers three possible business outcomes: (i) merger or sale, (ii) dissolution / failed business plan, and (iii) status quo as a private company. For each scenario, we estimate the value of the enterprise and then calculate the estimated proceeds to each security class. Theoutcome of each scenario is then discounted to the valuation date at a discount rate commensurate with the risk associated with each outcome. Finally, a probability factor is applied to the present value of each outcome based on the likelihood of each event occurring.

The following tables outline the calculated values for both the preferred and common stock under each event, both at the expected event date and at the valuation date (present value).

As this example illustrates, the values per common share indicated by the PWERM differ materially from the results of the Current Value Method (i.e., $1.08 vs. $0.30, respectively). The PWERM-derived common share value of $1.08 reflects the forward-looking nature of an investment in an early-stage company such as Company A. In other words, an investor in Company A has significant upside potential associated with the future outcomes above-and-beyond the current liquidation value of the common shares. (It should be noted that this is a zero sum exercise as the value accrued to the common equity must come from some other security holder. In this example, it is the preferred shareholder.)

Option Pricing Method Example –Highly Leveraged Company

In addition to early-stage companies (e.g., companies funded with complex capital structures comprising convertible securities), the value allocation techniques outlined in the Practice Aid can be applied to any situation where one part of the capital structure stands to achieve significant upside due to the effects of leverage if EV increases in the future.

Many equity holders of established businesses are now facing an “equity squeeze” due to the compounding effects of (a) the wide availability and generous terms of debt financing during the period from 2003 to 2007 and (b) declining business values in the current economy. Not unlike being “upside down” on a mortgage, an equity squeeze occurs when the residual equity of a company becomes an increasingly small portion of a company’s overall capitalization. This is due to the fact that debt holders have liquidation preference over the common equity, and common shareholders will receive distributions only to the extent that distributable funds at the time of a liquidity event are in excess of the amounts owed to debt holders.

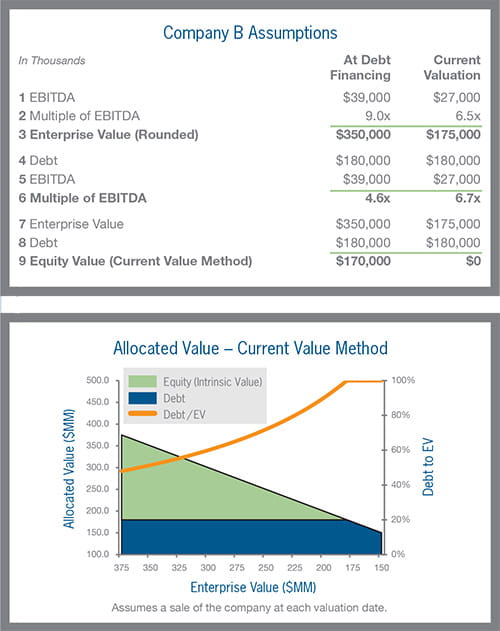

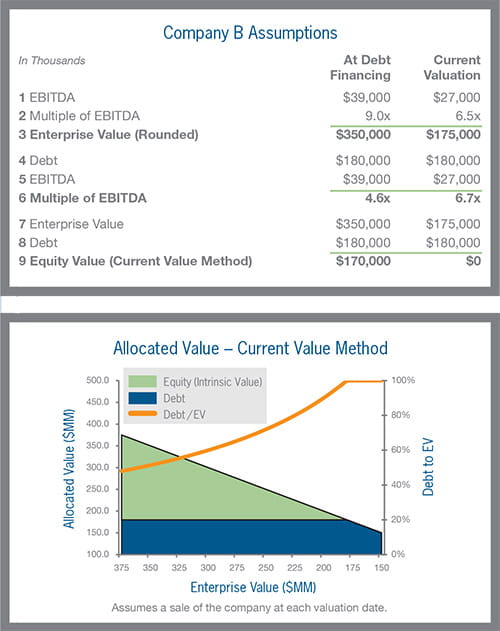

For example, let’s assume that Company B raised $180 million in debt a few years prior to the date of valuation. The debt financing was completed at 4.6x earnings before interest, taxes, depreciation, and amortization (“EBITDA”). Since that time, Company B’s EBITDA has decreased 31%, while EV pricing multiples in Company B’s industry have declined from 9.0x EBITDA to 6.5x EBITDA. As a result, the implied residual value available to common shareholders is significantly depressed. In fact, application of the Current Value Method would suggest common equity value of $0 based on these assumptions, as illustrated in the following charts.

Assuming that Company B expects to generate sufficient cash flow to service its debt obligations and there is no imminent expectation of a liquidity event (or bankruptcy), the Current Value Method does not reflect the going-concern status of the enterprise from the standpoint of the common shareholders. Specifically, the Current Value Method ignores the fact that Company B’s shareholders have claim on the company’s future potential upside above a certain level of EV (in this case, an EV greater than the face amount of interestbearing debt plus any accrued interest).

In order to account for the optionality associated with a highly leveraged company’s equity over an anticipated holding period, theOption Pricing Method may be employed. The Option Pricing Method values common equity as a call option above-andbeyondits fixed obligations to debt holders, including future principal and interest payments; that is, the common shares effectively represent call options on Company B’s EV. Further, the Option Pricing Method incorporates an assumption of EV volatility over an anticipated holding period.

One of two approaches may be employed when applying the Option Pricing Method: the Black-Scholes Option Pricing Model (the “Black-Scholes Model”) or a lattice or binomial model (the “Binomial Model”). In the case of “plain-vanilla” options (such as the option value associated with common equity in our example), the Black-Scholes Model and the Binomial Model generate similar answers. This is because the Black-Scholes Model is simply a mathematical formula for a standard lattice model.

The Black-Scholes Model relies on six key variables: (i) asset value; (ii) exercise price; (iii) term; (iv) the risk-free rate; (v) the underlying asset’s price volatility (or level of risk); and (vi) dividend yield of the underlying asset. The Black-Scholes Model’s formula for call options is as follows:

C = S*e^(-dT)N(d1)-X*e^(-rT)N(d2)

- Asset Price (S) – Common equity effectively represents a call option on Company B’s EV. As such, the asset price is set equal to current EV.

- Exercise Price (X) – Exercise price is the sum of all securities senior to the common stock. In this case, Company B’s shareholders only receive value in a liquidation event to the extent that distributable funds exceed the company’s fixed obligations to debt holders, including future principal and interest payments. As such, the exercise price utilized in this example is set equal to (a) the face value of all interest-bearing debt instruments, (b) accrued interest, and (c) future after-tax interest payments on the debt over the anticipated holding period.

- Term (T) – Since there is no contractual term associated with a company’s EV or common equity, the value of common equity is based on the likely holding period for the common shareholders’ investment in Company B. Term may be correlated with the maturity date(s) of its existing debt obligations due to the fact that a highly leveraged company may be unable to refinance at similar terms, which could force a sale of the company.

- Risk-Free Rate (r) – The risk-free rate of return is generally represented by the U.S. Treasury Bond over the estimated holding period.

- Volatility (the Variable Component of N(d1) and N(d2)) – Volatility represents an estimate of the annualized standard deviation of differences in the natural logarithms of the possible future stock prices. Volatilities of comparable public company stock prices are typically used as a proxy for a private company’s volatility. In doing so, it should be noted that the public company volatilities represent equity volatilities and not EV volatilities (unless the public companies do not employ debt). Thus, all else being equal, the EV volatility factor used in the Option Pricing Method should be lower than the public company volatilities due to the fact that EV is comprised of debt and equity and that the volatility associated with debt is generally lower thanthe volatility associated with equity.

- Dividend Yield (d) – The dividend yield should reflect the anticipated normalized dividend level for common equity divided by EV. Typically, a highly leveraged company will not pay common dividends since itsoperating cash flow will be used for principal and interest payments on debt or reinvestment purposes.

Assuming a three-year time horizon to a liquidity event and EV volatility of 25%, the following table illustrates the application of the Option Pricing Method. As shown, the indicated value of equity is approximately $26 million versus $0 via the Current Value Method. Moreover, the following graph illustrates the optionality component of the company’s equity value which, in this example, becomes more pronounced as the debt to EV ratio exceeds approximately 60%.

It is important to point out that the more significant the equity squeeze, the higher the possibility that the subject company could be forced into bankruptcy or other sale by its creditors. If there is a high probability of such an event, it may be appropriate to apply a hybrid of the Option Pricing Method, Current Value Method, and PWERM. First, one would use the Option Pricing Method to estimate the current intrinsic and option value of the common stock assuming a sale of the company in the future. Second, one would use the Current Value Method to estimate the residual value to common shareholders in the event the company is subject to a forced sale or bankruptcy (which may be zero), discounted to the valuation date. These two scenarios would then be weighted with consideration of all pertinent factors known or knowable as of the valuation date.

Other Considerations

No single allocation method is superior in all respects and all circumstances. Each method has merits and challenges, and there are tradeoffs in selecting one method over the others. That being said, when applying one (or more) of the value allocation techniques described herein, it is important to note that the Securities and Exchange Commission (“SEC”) has openly questioned the appropriateness of averaging allocation techniques that yield materially different results. In a statement, the SEC noted:

In some cases the underlying conceptual differences between certain allocation methods would appear to render the results of averaging somewhat meaningless. For example, the probability-weighted allocation method is forward-looking and the current value method is not. Averaging a forward-looking allocation method that considers the value inherent in a going concern with an allocation method that does not is like trying to average apples and oranges. The result isn’t meaningful.

Additionally, while the examples presented herein do not include consideration of discounts for lack of control or marketability, these adjustments may be appropriate depending on the facts and circumstances of the valuation assignment. In estimating an applicable valuation discount, one must be careful to consider that the allocation technique employed likely includes assumptions related to a prospective liquidity event in the future. The timing of this event should be considered in the determination of appropriate discounts.

Conclusion

The current economic and regulatory environment poses significant challenges when valuing the equity of companies with complex capital structures or in highly leveraged situations. In these situations, equity value is not necessarily equal to EV less debt. Rather, the overlapping rights and preferences of stakeholders in a business must be considered in the context of future potential outcomes – rather than simply assuming that the business was sold on a particular valuation date. These issues continue to garner attention in the financial and tax reporting communities, and as such, sound judgment and reasonable assumptions must be adequately supported and documented when employing these methodologies.

1 Todd E. Hardiman, “Speech by SEC Staff: 2004 Thirty-Second AICPA National Conference on Current SEC and PCAOB Developments,” U.S. Securities and Exchange Commission, 6 December 2005