English

English

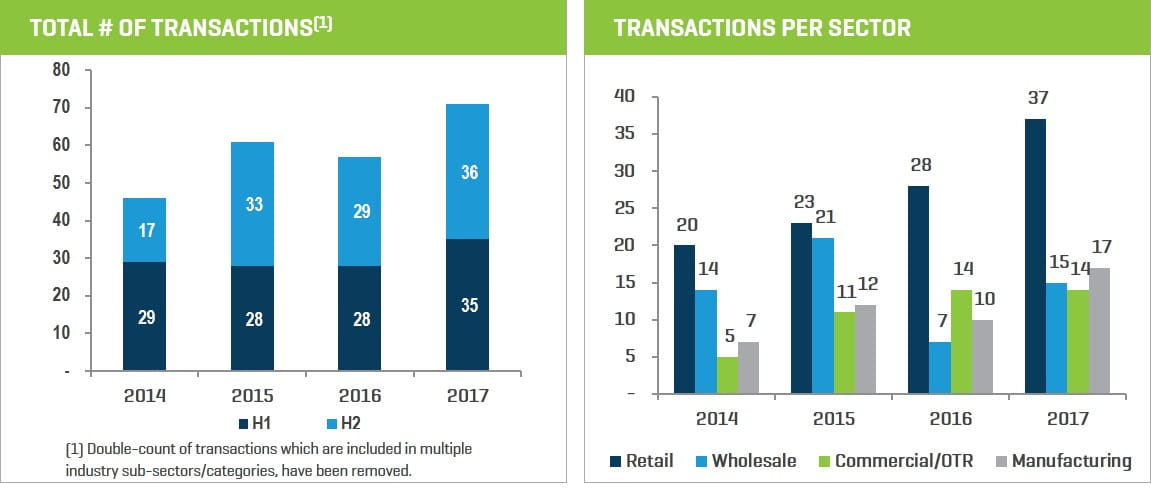

M&A activity in the fourth quarter pushed the total 2017 transaction count to its highest level since we began tracking data in 2014. Each segment saw consistent acquisition and investment activity, driven by many factors, including:

- continued retail consolidation

- increased optimism regarding infrastructure spending nationally, positively affecting the construction/industrial sectors and OTR product pricing, thus creating a tailwind for commercial and OTR businesses and transactions

- continued strength in the U.S. economy and a macro environment which seems to be improving globally

- continued asset price inflation as evidenced by stocks, real estate, and credit market performance

- favorable changes in the domestic tax environment

- an ongoing desire by investors to put capital to work while strategic acquirers look to expand beyond what is currently a flat to modest organic growth rate

Valuations remain healthy, some would say elevated, making a sale in the current environment a way to achieve full value for one’s enterprise. For private, family, and entrepreneur sellers, reinvestment opportunities continue to be a challenge, as stocks seem to be very expensive, bank accounts still pay very little, and bond yields remain low. But this must be viewed holistically with buyers paying higher EBITDA multiples, which will usually more than compensate a seller for income lost in a low-interest-rate/high-asset-price environment – and also compensate a seller upfront as opposed to over time.

We hope you find our annual review informative, and we welcome the chance to engage with you in 2018.

Historical M&A Trends – By Period / By Sector

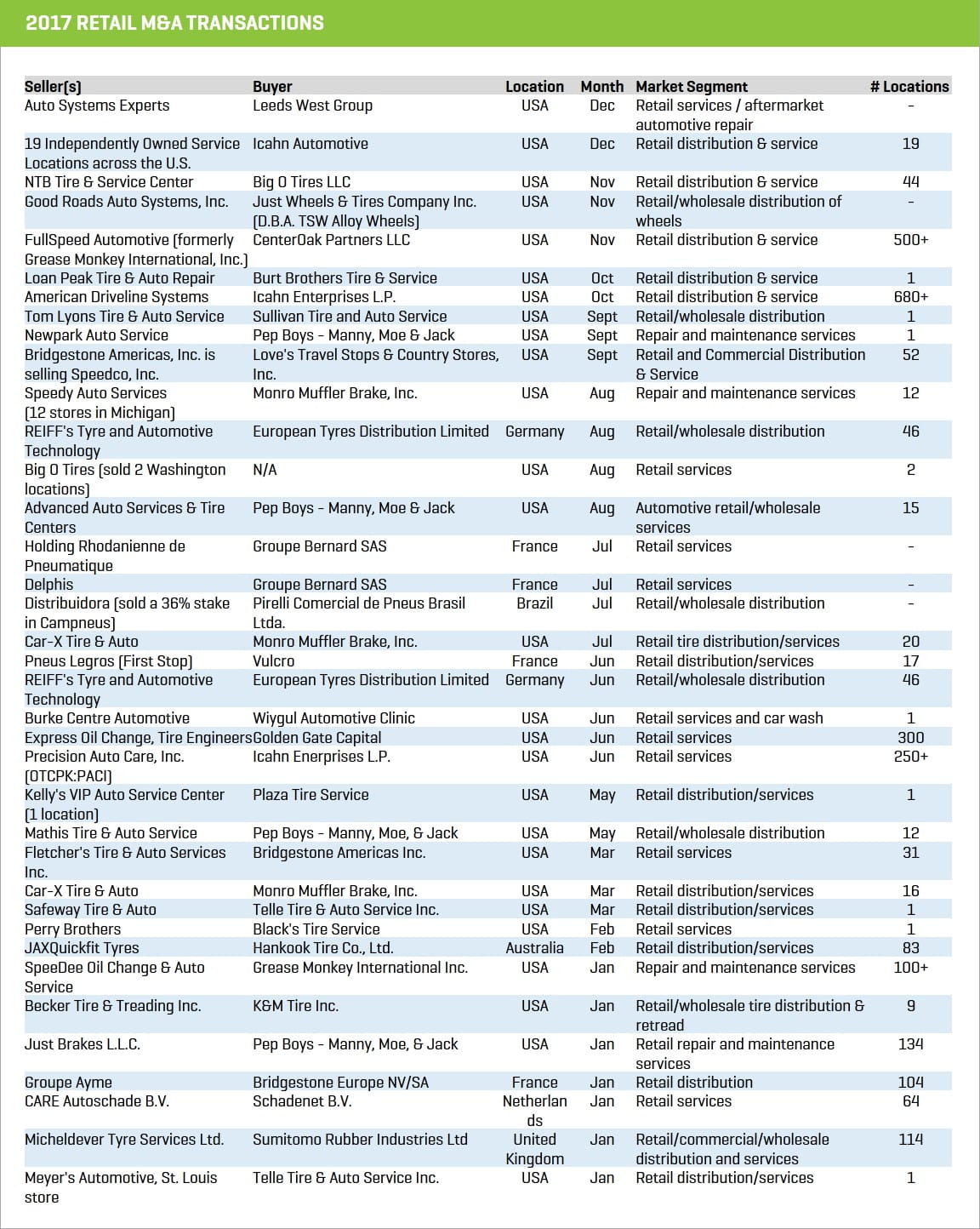

Retail

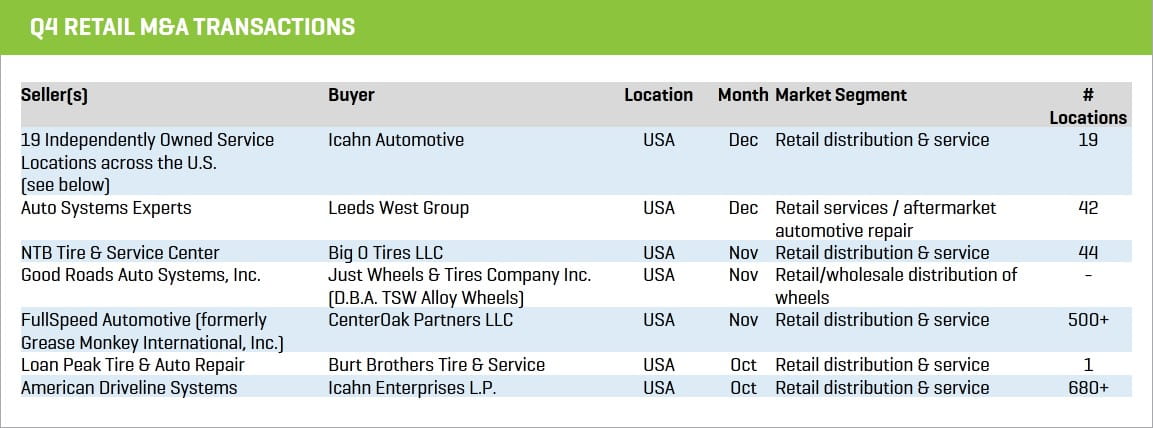

The fourth quarter was strong in the retail sector, with over 1,200 retail/service units either directly changing owners or reporting to a newly acquired franchisor.

Big O Tires LLC

TBC Corp.’s Big O Tires LLC has added 44 new stores, purchased by franchisee Mark Rhee (Rhee is currently the president of Western Automotive Ventures and already has 12 Big O Tire locations). The new locations, formerly NTB Tire & Service Centers, expand Big O’s reach into Iowa, Kansas, and Missouri. With these additions, the Big O network extends through 23 states, boasting over 400 locations throughout the western region of the U.S.

Icahn Automotive Holdings

Southfield, Michigan-based wholly owned subsidiary of Icahn Enterprises (NASDAQ: IEP), Icahn Automotive acquired American Driveline Systems (ADS) from Transom Capital Group. ADS is the franchisor of AAMCO and Cottman Transmission & Total Auto Care service centers, with approximately 680 locations in the U.S. and Canada. Icahn Automotive now operates approximately 1,900 service locations in 49 states, as well as several international locations. The ADS acquisition further solidifies Icahn’s foothold in the automotive aftermarket value chain.

In a spree of late fourth-quarter activity, Icahn Automotive acquired an additional 19 independent retail and service locations, including:

- Elliott Tire and Service (10 locations throughout Washington state)

- S&S Service in Hamburg, NY

- Jack’s Service Center in Miami, FL

- Blanchette’s Auto Center in Dracut, MA

- Quality Automotive in Napa, CA

- Honest Auto Service in Seattle, WA

- WS Haynes Tire & Services in Memphis, TN (2 locations)

- RL&F Auto Inc. in Morrisville, NC

- Plainfield Tire Center in Plainfield, IN

Icahn Automotive continues to aggressively expand its national automotive service network and strengthen its full-service capabilities, allowing the group to leverage its broad national footprint and operate with added efficiencies garnered through economies of scale.

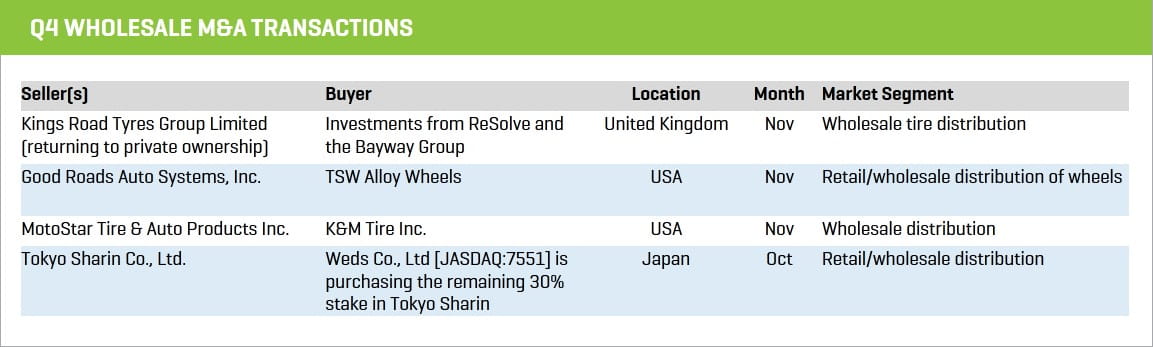

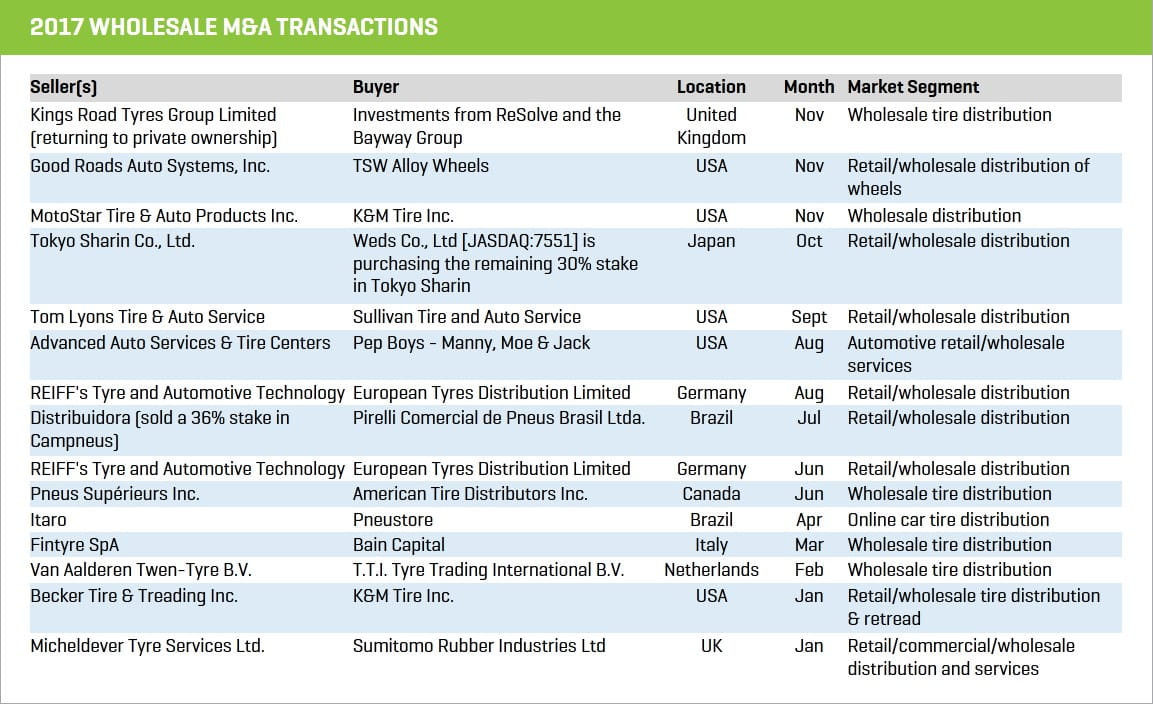

Wholesale

A total of four transactions capped off a modest year for wholesale M&A, where total transaction volume tracked at about its four-year average.

K&M Tire Inc.

- Ohio wholesaler K&M Tire Inc. acquired New England-based MotoStar Tire & Auto Products Inc. Founded in 1993, MotoStar has grown from a small storage facility to a regional distribution hub for some of the country’s top retailers. The acquisition expands K&M’s network to 26 locations, serving markets in 27 states.

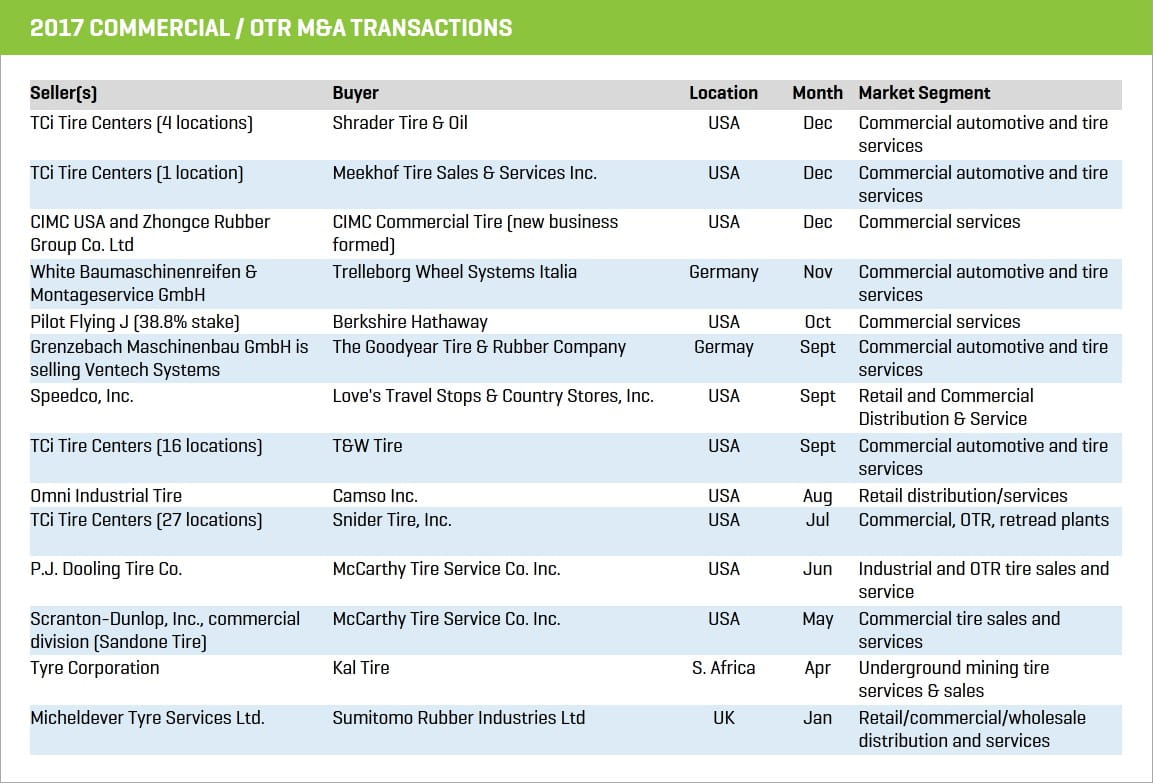

Commercial/OTR

A total of five transactions in the fourth quarter pushed M&A in the segment higher for the fourth consecutive year, as the segment continues to draw attention from a host of players

Berkshire Hathaway Inc.

- Berkshire Hathaway Inc. announced that it will acquire a 38.8% equity stake in Knoxville, TN-based Pilot Travel Centers LLC, doing business as Pilot Flying J. Under the terms of the plan, Berkshire will acquire another 41.4% of Pilot and become majority shareholder in 2023. Pilot Flying J was established in 1958 and has expanded to 750 retail locations in 44 states. It also runs 44 Goodyear Commercial Tire and Service Centers and 35 Boss Shops, operating with a total of approximately 27,000 employees across the U.S. Berkshire’s commitment to Pilot demonstrates the investment firm’s bullish outlook on U.S economic growth broadly, and its positive outlook on Pilot specifically, citing a “smart growth strategy” as a key consideration for the investment.

Shrader Tire & Oil / Meekhof Tire Sales & Service

- Shrader Tire & Oil has acquired four TCi Tire Center locations, including one retread plant, from Michelin North America. The acquisition strengthens Shrader’s presence on both the new tire and retread fronts, with the addition of the TCi retread facility nearly doubling Shrader’s retread capabilities. This deal further allows Shrader to solidify and expand its business in the greater Columbus and Cincinnati metropolitan areas.

- Meekhof Tire Sales & Services also picked up a TCI Tire Center location in Michigan, further reducing the TCi network of commercial stores to 10 locations, having divested 48 commercial sales locations in 2017 (Michelin divested 16 locations to T&W Tire and 27 locations to Snider Fleet earlier in 2017). Based in Grand Rapids, Meekhof increases its operating network to 10 commercial service locations throughout central Michigan.

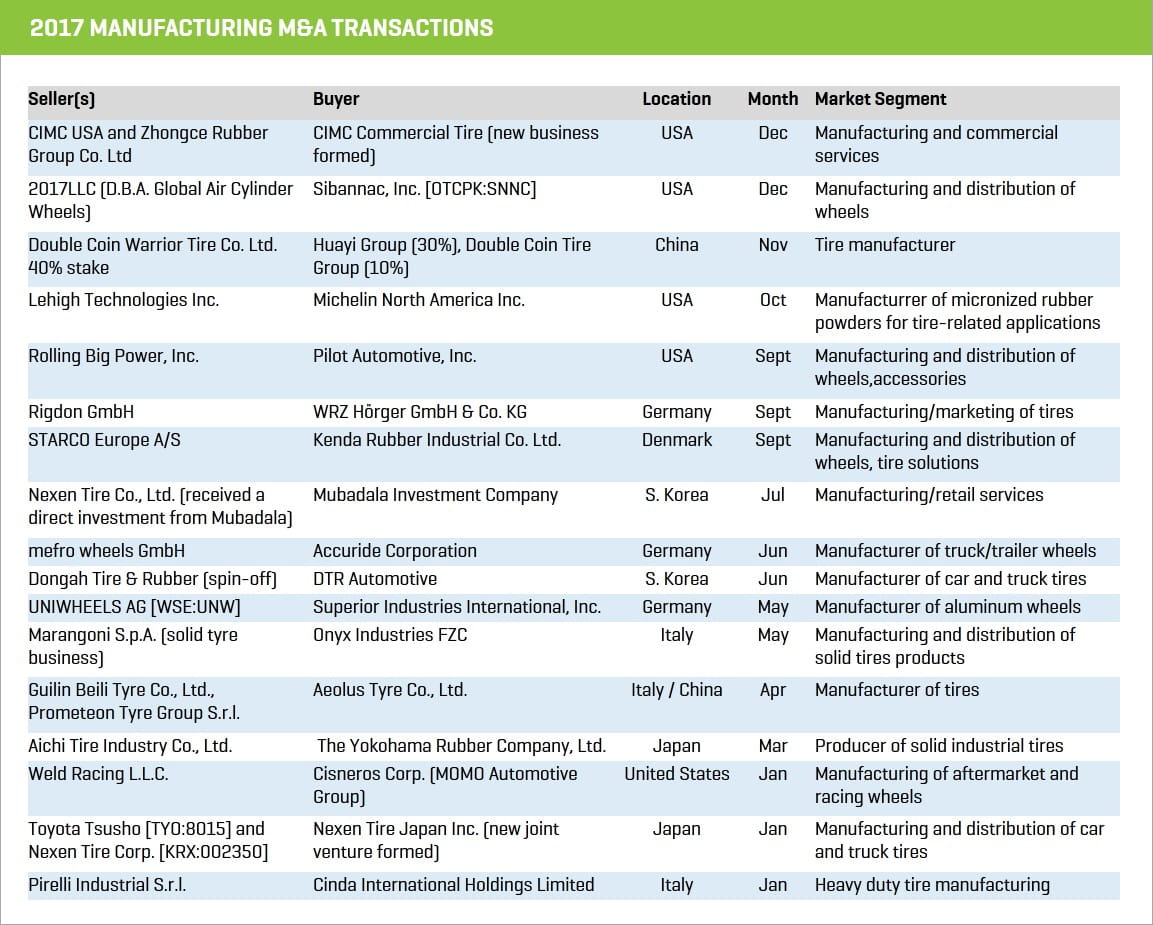

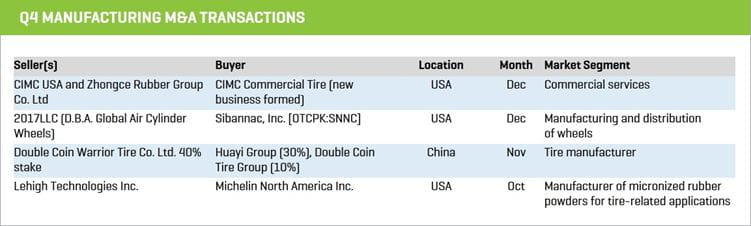

Manufacturing

The manufacturing sector had a relatively strong year, with four transactions in the fourth quarter pushing the annual total to 17.

Michelin North America Inc.

- In October of 2017, Michelin North America Inc. acquired Lehigh Technologies Inc., a scrap tire processor and recycler based out of Atlanta, GA. Lehigh is best known for scrapping tires into micronized rubber powders (MRPs) for both tire and nontire applications. Michelin’s acquisition demonstrates a certain strategic intent: bringing its materials expertise to markets that extend beyond tires, while simultaneously reducing the amount of raw materials needed in production.

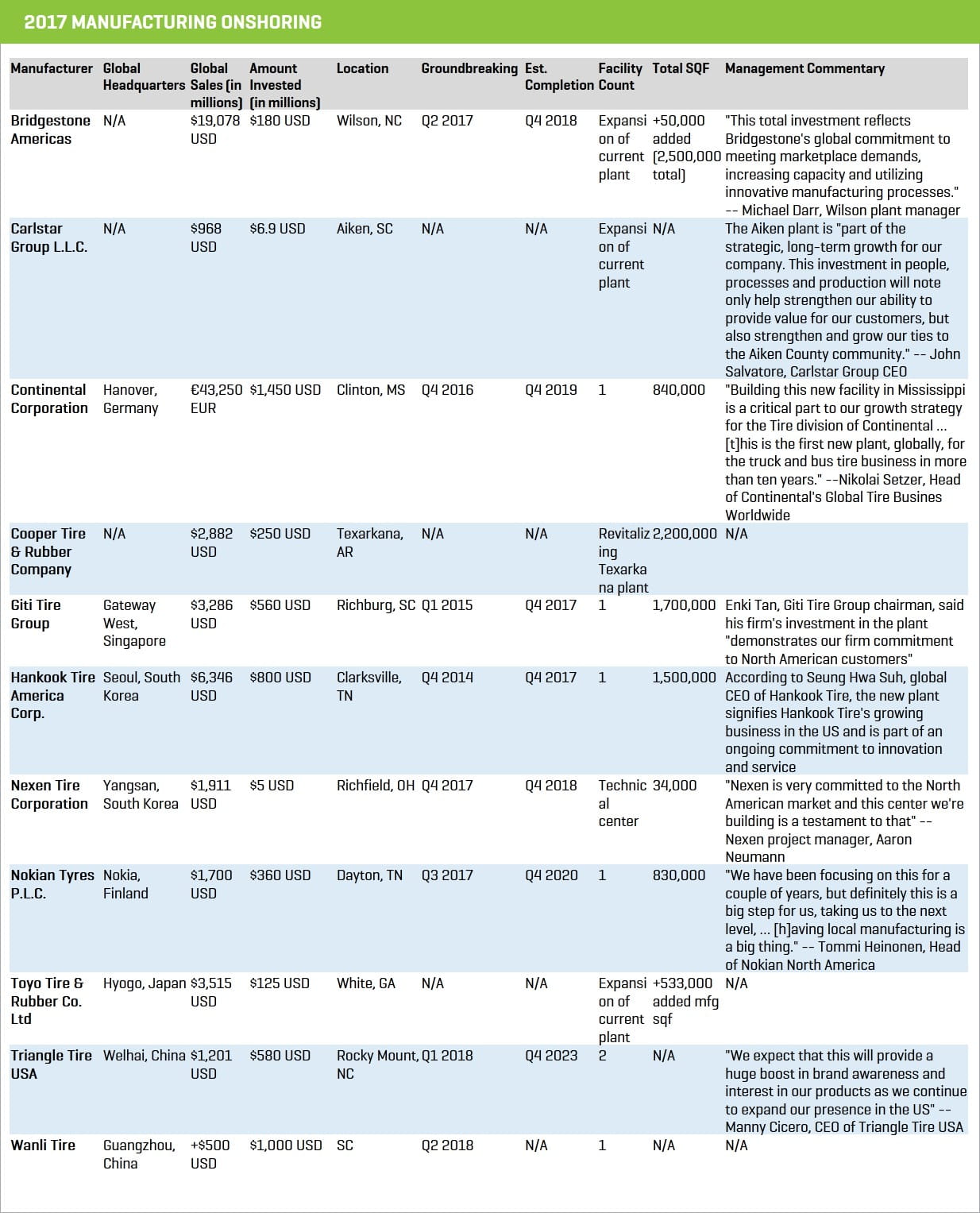

2017 Highlighted Trend: Boom in U.S. Tire Manufacturing

The southern states have been beneficiaries of global tire manufacturers making significant capital investment in new, expanded, and upgraded manufacturing facilities in the U.S. The sizable and numerous investments are creating thousands of local jobs during both the development/build phase and the operations phase of these projects.

Friendly labor conditions are influencing decision making from manufacturers and providing a significant boost to the region, particularly in Tennessee, the Carolinas, and Mississippi. Elements of these labor conditions include:

- costs and reasonable cost of land acquisition

- modest to low tax environments

- a region that, as a whole, is seeing domestic migration from higher-tax/higher-cost states

- a year-old administration with an “America first” philosophy

The vast majority of investment is in plants producing passenger and light-truck tires for the domestic U.S. market, though truck/bus tire manufacturing is also represented. This is enabling global manufacturers to avoid duties and cumbersome logistics costs, reduce lead time on deliveries, release foreign capacity, build specific products for North American consumers, and provide faster, more economical shipping to domestic customers and points of distribution.

2017 M&A Transactions by Segment & 2018 Forecasts

Retail

Transaction count increased handily in 2017 versus 2016, as did the total number of units changing hands or under newly owned franchisor stewardship (when counting franchise units covered by franchisors that changed hands, unit turnover is over 2x in 2017 versus 2016). The drivers for the most part remain the same:

- soft organic growth being offset by accretive acquisitions of retail networks

- private equity and institutional investor involvement in the retail sector

- attainable synergies when combining retail networks

- The U.S. was by far the busiest market for retail M&A globally, with honorable mentions for activity in the U.K., Australia, Germany, and France.

Retail Forecast 2018

- Look for M&A activity to continue at a steady pace in 2018, as the strong rate of annual transaction volume growth moderates

- There is ever more potential for large, transformative deals to take place as big retailers look to expand and consolidate footprints, and regional, privately held companies take advantage of a very hot M&A environment for prized retail assets. This may be driven further by the lack of succession planning in many family and entrepreneur-owned retailers combined with the favorable deal environment.

Wholesale

We anticipated a stronger year for wholesale M&A in 2017. Transaction count more than doubled versus 2016, with the drivers being strong regional distributors (K&M), private equity (Bain Capital), large consolidators (ATD), and manufacturers/distributors (Sumitomo).

Transaction activity was global in its scope with big European names, including Micheldever, Fintyre, and REIFF’s changing hands, though transaction count maintained its four-year average.

Wholesale Forecast 2018

- Look for regional consolidation activity to continue in North America as wholesalers with $150 million or less in revenue continue to be absorbed and buyers attain scale benefits. There is also the potential for one or more large/transformative transactions (companies with more than $200 million in revenue) as the upper end of the market seeks opportunities to offset flat to slow organic growth with M&A.

- We expect Bain Capital and its platform, Fintyre, to play the European equivalent role of ATD, continuing to acquire and attain scale, crossing borders where possible.

- Manufacturers will stick with their core business and create alliances, joint ventures, and other arrangements to increase product availability and achieve greater scale in wholesale delivery.[1]

Commercial/OTR

In our 2016 report we forecasted acquisition and investment of scale in the commercial/OTR segment in 2017. In what was a steady year for transaction volumes, we witnessed big moves, such as:

- Michelin North America spun off the majority of its TCi Tire Centers operations to regional dealers

- Love’s acquired Speedco from Bridgestone

- Berkshire Hathaway made a sizable investment in Pilot Flying J, which operates a significant truck care and commercial tire business.

The activity continuing to shape the commercial/OTR segment should remain intriguing.

Commercial/OTR Forecast 2018

- Look for travel center operators to expand retread and commercial distribution/service footprint organically and via acquisition

- Expect regional consolidation by the strong midsize players to continue

- It remains a matter of time before private equity acquires a sizable platform with which to consolidate the segment in a specific region (or regions), but 2018 will likely see such activity

Manufacturing

During 2016 we saw a soft year in terms of volume (10 transactions in 2016 versus 17 in 2017) in manufacturing M&A. The primary trend that year was the acquisition of specialty product/niche manufacturers by the larger global brands. Transaction activity in 2017 was driven by several factors:

- Large corporates in Asia reshuffled business units and ownership structures

- Global brands continued their specialty/niche acquisition hunt (Yokohama, Onyx)

- Manufacturers reached into end-of-lifecycle areas such as tire recycling (Michelin).

Manufacturing Forecast 2018

- Look for manufacturers sticking to core manufacturing and divesting distribution operations, or initiating/expanding partnerships with large distribution networks

- We expect continued pursuit of specialty manufacturers and brands by the top 10 global manufacturers

- Look for further reshuffling of operations and brands among the large Asian manufacturers to optimize global operations and brand portfolios

- See the special section on “Onshoring” above in this report