English

English

Co-authored by:

Tim Osborne Valuation Advisory

Associate

+1.216.373.2999

tosborne@stout.com

Market dynamics continued to benefit the credit markets during the fourth quarter of 2017, marking a sixth-consecutive quarter of favorable momentum that has spurred both lending and borrowing activity. After declining in each of the last two years, middle market loan issuances totaled $170 billion in 2017, reflecting a 23% increase over 2016. Leading the way were large middle market loan issuances (i.e., loans up to $500 million), which were up 18% in the fourth quarter of 2017 over the same period in 2016. Overall institutional loan issuances also surged during this period, increasing 38%.

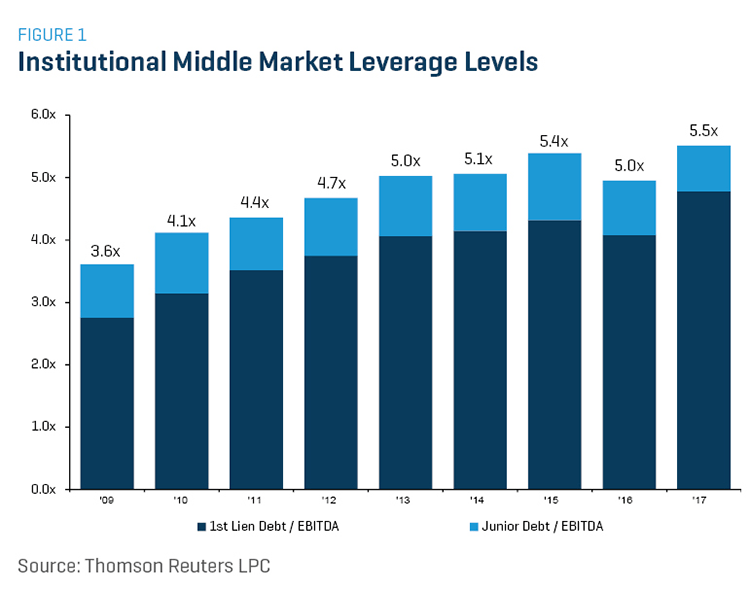

Lending became incredibly borrower-friendly over the course of 2017 as a result of heavy competition among banks and nonbank lenders. Such competition has driven yields down despite a noticeable increase in the London Interbank Offered Rate. Yields stayed tight during the year and averaged only 6.06% in the fourth quarter. Since the first quarter of 2016, middle market term loan yields have declined 1.27%. Lenders have loosened terms considerably during the last year in response to this competition, offering covenant-lite terms in favor of securing volume. Taken altogether, these factors have resulted in some of the most generous leverage on record at almost 6.0x earnings before interest, taxes, depreciation, and amortization?

Financial sponsors in particular have continued to take advantage of the strong lending environment, responding by aggressively pursuing new borrowings to capitalize their portfolio companies. The sponsored lending market has seen a major uptick in issuances, which increased 48% over 2016 and reached an all-time high of $77.7 billion, setting a new annual record by surpassing 2013’s mark of $72.5 billion.

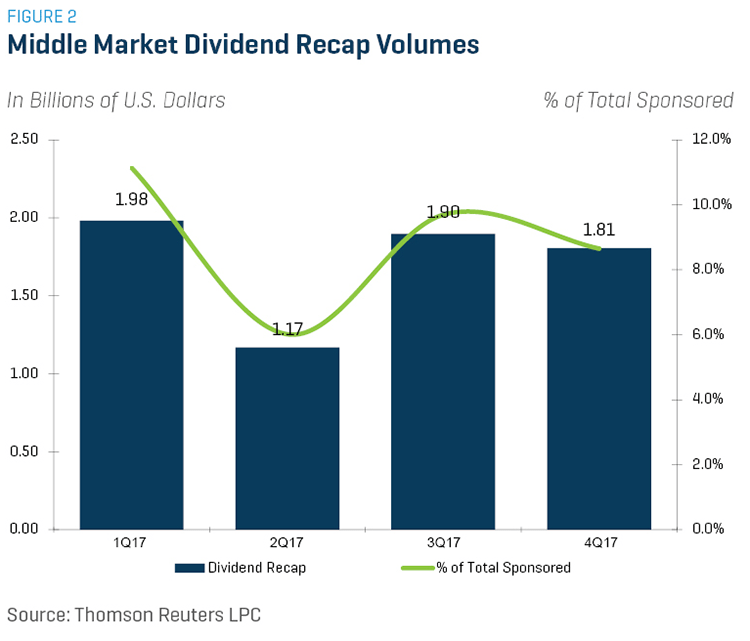

Reflecting the strong appetite from both investors and borrowers, dividend-recapitalization activity surged during 2017, with associated lending doubling 2016’s level and topping out at $6.9 billion. That said, 2017 fell well below the record of $13.8 billion seen in 2013, suggesting that there is potential in the market for dividend recapitalization activity to increase further in 2018 if favorable market conditions continue to persist.

Signs point in the direction that the current lending environment will continue through 2018, as 64% of respondents to the William Blair Leveraged Lender Survey indicated they expect pricing to remain consistent with current levels, with an additional 25% of respondents suggesting further price compression will occur. Lenders also expect a continuation of borrower-friendly terms and leverage levels during the year. While it remains to be seen how the recent market volatility will affect credit markets, fundamental market and economic conditions suggest that the recent strength of the markets will persist, at least for now.