English

English

What is Unallocated Family Support and Why Should I Use It?

Unallocated family support is, in essence, a combined payment of traditional child support and spousal support. Child support is neither deductible by the payor nor taxable to the payee. By combining the payments, the entire amount will be deductible by the payor and taxable to the payee, thus taking advantage of a disparity in tax brackets.

Unallocated Support

To realize tax the benefits of using unallocated family support, the payments must qualify as taxable/deductible alimony under Internal Revenue Code (IRC) §71.

- The payments must be in cash.

- The payments must be made pursuant to a divorce or separation instrument, including a temporary support order.

- The payments must not be designated as includable in gross income under IRC §71 and not deductible under IRC §215.

- The parties may not be members of the same household.

- The payments must end on the death of the payee and there must be no liability to make a payment after the death of the payee.

- The payments cannot be fixed for child support.

Child Support

A payment is fixed as child support, and thus non-deductible by the payor, if the governing instrument designates a sum as payable for the support of a child of the payor or the payment is reduced on the happening of a contingency related to the child or at a time which can be clearly associated with such contingency (Reg. §1.71T Q-16). Events that relate to a child include the child’s attaining a certain age or income level, dying, marrying, leaving school, leaving the spouse’s household, or gaining employment.

There are two situations in which a reduction in payments will be presumed to be clearly associated with a contingency related to a child as follows:

- The payments are to be reduced within 6 months, either before or after, a child attains the age of 18, 21, or local age of majority.

- The payments are reduced on two or more occasions which occur not more than one year before or after a different child attains a certain age between the ages of 18 and 24, inclusive. The age at which the reduction occurs must be the same for each child.

These are rebuttable presumptions which can be overcome by showing that the time at which the payments are reduced was determined independently of any contingency related to the children. In general, if the reduction in payments is attributable to a complete cessation of alimony or by showing that alimony payments are to be made for a period customary for the jurisdiction, the payments will not be determined to be child support.

If it is determined that a reduction in payments is associated to a contingency related to a child, only the amount of the reduction will be considered child support. For example, assume the payee has been paying monthly family support of $4,000 for 3 years. In the fourth year, which happens to coincide with the 18th birthday of a child, the payment is reduced to $3,000 a month. The $1,000 will be considered child support, not only in the year of reduction but retroactively for all prior payments.

Advantage of Using Unallocated Family Support

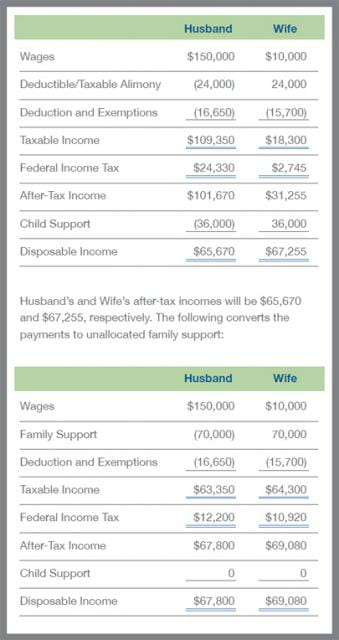

Because the payor of support is assumed to be the higher income party, the total support can be deducted at his or her higher marginal tax rate and included in taxable income at the recipient’s lower tax rate. The recipient should receive increased support to cover the tax burden on the child support portion of the payment. Assume the following facts:

- Husband’s annual income is $150,000

- Wife earns $10,000 annually

- The three children live with Wife

- Traditional child support is $3,000/month

- Traditional spousal support is $2,000/month

By converting the child and spousal support to unallocated family support, the parties have received a $3,350 tax subsidy with both parties enjoying additional disposable income.

Death of the Payee

If the decree provides that any payments in cash or property must be made after the payee spouse’s death as a substitute for otherwise qualifying payments before the death, such payments will not qualify as alimony. To the extent that the payments begin, accelerate, or increase because of the death of the payee spouse, the payments, in whole or in part, may be treated as payments that were not alimony. Whether or not such payments will be treated as not alimony depends on all the facts and circumstances.

For example:

- The divorce decree requires Husband to pay his former spouse $30,000 annually.

- The payments will stop at the end of 6 years or upon the former spouse’s death, if earlier.

- The former spouse has custody of the minor children.

- The decree provides that if any child is still a minor at the spouse’s death, Husband will pay $10,000 annually to a trust until the youngest child reaches the age of majority. The trust income and principal are to be used for the children’s benefit.

These facts indicate that the payments to be made after the former spouse’s death are a substitute for $10,000 of the $30,000 annual payments. Of each of the $30,000 annual payments, $10,000 is not alimony.

The divorce or separation instrument does not have to expressly state that the payments cease upon the death of the payee spouse if, for example, the liability for continued payments would end under state law (IRS Notice 97-9, 1987-1 C.B. 421). Thus, it is imperative to know the applicable state laws. Consider the different results in the following cases.

Schwening v. Commissioner, 2009 TC Summary Opinion 7 – Tax Court 2009

Pursuant to the parties’ 2001 divorce decree, Husband was to pay his ex-wife “the amount of $1,700 per month as and for family maintenance.” The non-modifiable payments were to be made for 6 years. Additionally, if a child was still a minor at the end of the 6-year period, the parties would agree to an amount of child support. Husband deducted the payments.

The IRS disallowed the deduction. Because there was no provision in the final judgment that the payments would end on the death of the payee, the payments did not qualify as taxable/deductible alimony. Husband argued that any portion of the payments providing support for a minor child would end on the death of his ex-wife because Husband would then become the custodial parent. However, under Colorado law, payments of maintenance and child support do not terminate upon the death of the payee. Thus, the payments were neither deductible by Husband nor taxable to Wife.

Kean v Commissioner, 407 F. 3rd 186 (3rd Cir. 2005)

From April 1992 through January 1997 when a final judgment of divorce was entered, Husband was ordered to make monthly payments to wife for the support of the wife, children, and the household. Husband deducted the amount of the monthly payments on his tax returns for the years 1992 through 1996. Wife did not report the payments as taxable income. The IRS issued deficiency notices to both parties.

Ms. Kean argued, in part, that Mr. Kean would have been required to continue making the payments even if she died. However, an order issued pendente lite in a New Jersey divorce proceeding does not survive the death of the payee. Although Mr. Kean would still have a legal obligation to support his children, he would have no obligation to make further payments to Ms. Kean or her estate. Thus, by operation of New Jersey law, the payments satisfied the requirement that they end on the death of the payee and thus, deductible by Mr. Kean and taxable to Ms. Kean.

State Specific Considerations

Because unallocated family support is partially comprised of child support, most state courts have found that it must be modifiable. In addition, some state courts are reluctant to award unallocated support, preferring the more traditional child support per state guidelines and alimony. If the parties intend the payments to be non-modifiable unallocated support, the terms should be clearly stated in the settlement agreement or divorce decree.

In summary, unallocated family support may not be appropriate in all cases, but it is a useful tool too often overlooked in settlement negotiations.