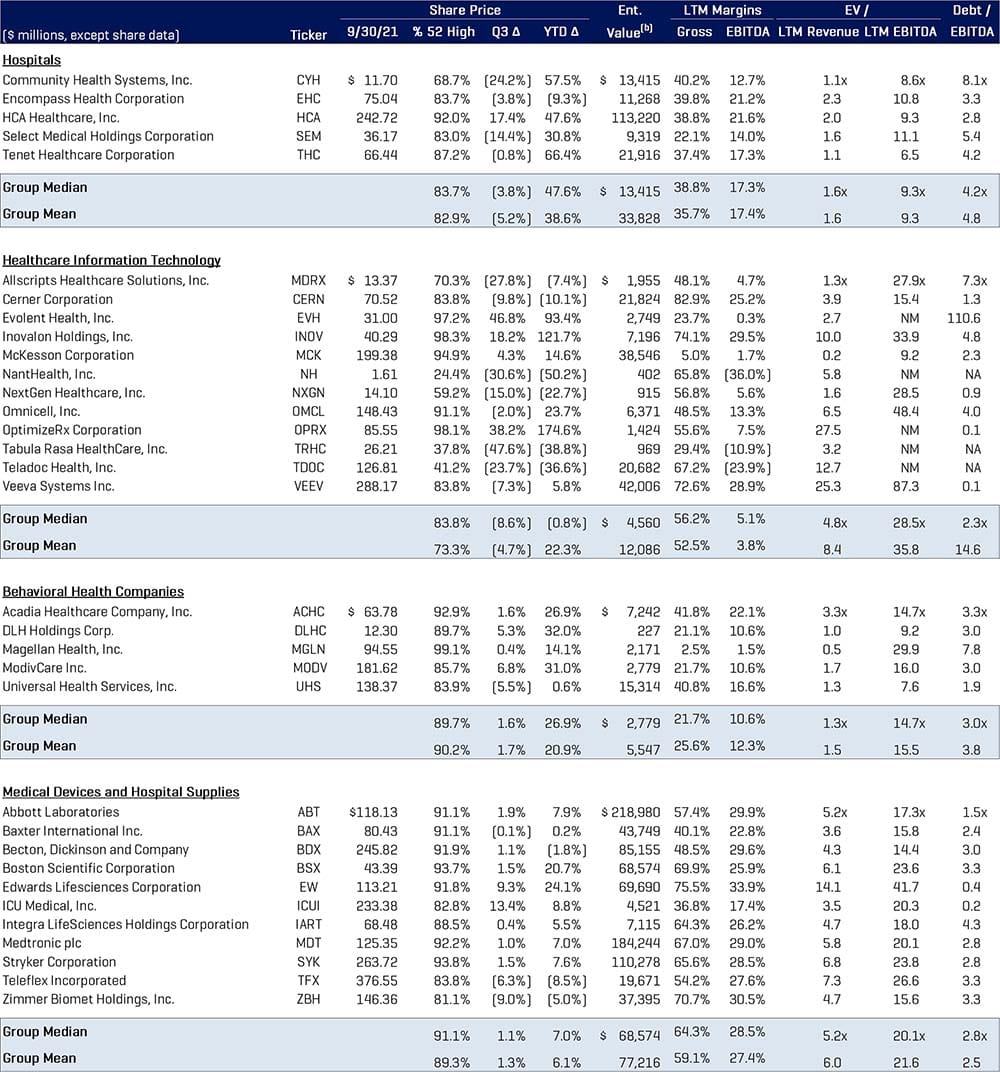

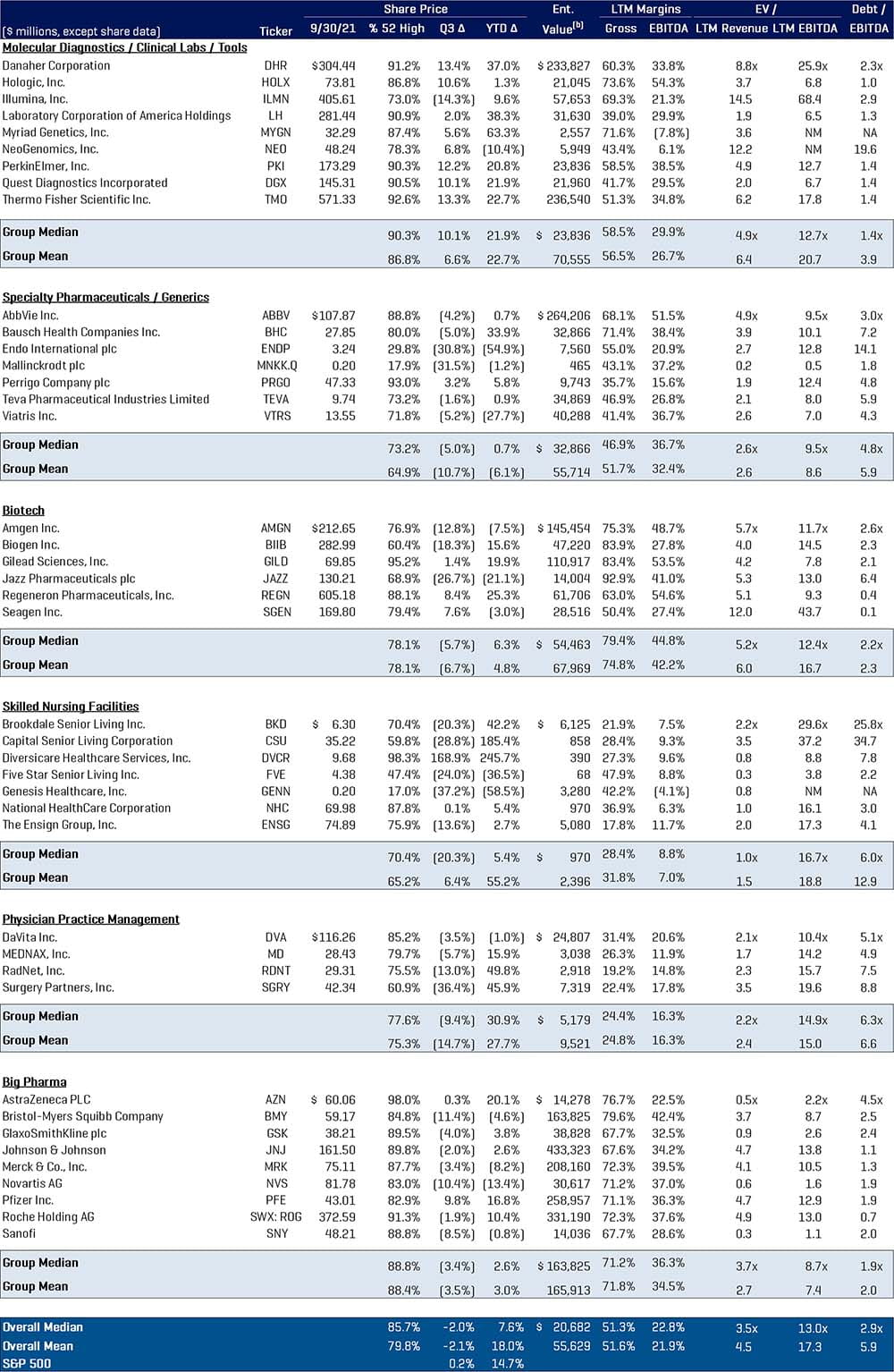

English

English

The S&P 500 was up just 0.2% in the third quarter of 2021 on concerns about rising inflation and supply chain bottlenecks amidst reductions in estimates for GDP for the year. Concern about slowing growth and a regulatory crackdown in China also weighed on markets in September.

The Healthcare Services and Life Sciences equities that we track in this report were off 2% overall and slightly underperformed the S&P 500.

Every sub-sector tracked by Stout posted minimal gains or was negative for the quarter with the exception of Diagnostics/Clinical Labs/Tools, where the average stock price increased 6.6%.

The two other healthcare sub-sectors that were positive for the quarter include Behavioral Health (+1.6%) and Medical Devices and Hospital Supplies (+1.1%), likely on the heels of the return of patients for live visits, new technologies, strong demographic trends and a recovery in elective procedures.

Healthcare Services

Healthcare outperformed year to date 2021 up 18% versus 14.7% for the market, largely due to a recovery in elective procedures impacting the hospital (median stock price up 47.6%) and physician practice management (+30.9%) sectors, which also negatively impacted performance of areas like telemedicine within the healthcare information technology sector. Hospital and Physician Practice Management performance leveled off in the third quarter of 2021, retracing some of their gains after big recovery related runs over the three preceding quarters. Long-term demographic trends remain quite positive.

We would note that unemployment in certain states has resulted in a negative payor mix shift recently for some physician practices, for example, in favor of Medicaid as opposed to commercial as one is obviously much less inexpensive to the patient who qualifies. This has likely impacted some hospitals as well.

Alternatively, we have seen strength in private pay practices in the U.S. $10 billion Med Spa segment, where data from the American Med Spa Association 2019 shows market growth of over 20% and notes that single location facilities represent 83% of total Med Spas, indicating a very fragmented industry.

Skilled Nursing performed poorly in the quarter with the median of stocks in the sector being off 20% on ongoing census issues tied to the pandemic and bad publicity. Patients are moving into the home setting for now, but longer-term, the surviving companies will likely fare okay given the aging demographic trends.

Behavioral health stocks were up marginally at 1.6% in third quarter, building on first quarter's rally of 9.8%, attributed to strong performances from ModivCare (+6.8%), which completed two notable acquisitions during the quarter of VRI Intermediate Holdings and Care Finders Total Care, and DLH Holdings (+5.3%). In addition, on-line mental health care provider Lifestance Health Group completed its IPO in mid-June, going public at $18 per share.

Healthcare Information Technology stocks were in the red for third quarter at -8.6%, although select players, including Evolent Health (+46.8%) and OptimizeRx Corporation (38.2%) posted strong gains in the period. The return of patients to the office and incredible prior performance of stocks like Teladoc impacted performance of telemedicine, but digital health funding has hit record levels in the last three quarters as interest in areas like on-line pharmacy remain strong. Telehealth unicorns such as Alto Pharmacy and Bright Health are looking to change the paradigm in their sectors.

Stout is also actively working on assignments with Home Durable Medical Equipment and medical supply companies, where the market is growing and moving toward capitation from traditional fee for service models.

Medical Devices and Life Sciences

Medical Device and Hospital Supply stocks were up 1.1% in the third quarter as the group continues to be a relatively strong and consistent performer. New technologies, including robotics for surgery, remote monitoring, transcatheter heart valves, neurostimulation devices and other categories, will all drive growth in the future.

Diagnostics, Tools, and Clinical Labs were up 10.1% (Median) for the quarter as the group continues to thrive from testing volumes required as a result of the pandemic. Many employers and/or occupations require regular testing for employees. Many patients likely waited to visit their physicians during the pandemic for routine blood and urine testing as well, and that activity is now returning to normal.

Specialty Pharma was down 5% (Median) in the quarter and continues to be hurt by litigation, price erosion, competition, and negative publicity.

Stout has also been active in working with medical device and pharma contract manufacturers, where we see a lot of opportunity for growth. Stout was proud to announce the closing of Life Science Outsourcing earlier this year, a contract manufacturer of medical devices, and Rev1 Engineering on its partnership (majority sale) to Asahi Intecc in the third quarter.

The traditional biotech names that we track here were off 6% in the quarter, but biotech remains a hot sector for M&A activity with multiple blockbuster deals announced in the quarter, most notably Merck’s $11.5 billion announced acquisition of Acceleron.

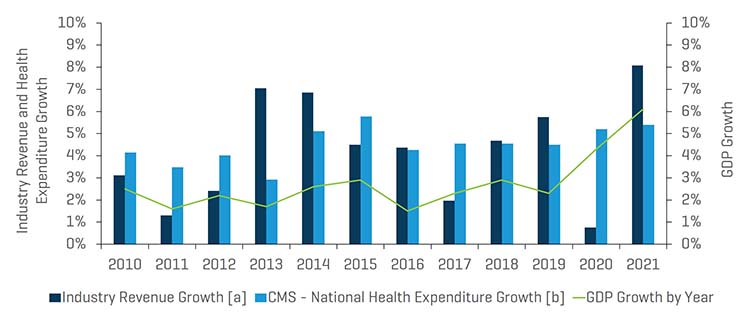

In the table below, you can see that Stout’s Healthcare Universe of companies saw revenue grow 7.8% so far in 2021, whereas real GDP for the U.S. economy is expected to grow approximately 6.1% in 2021.

Historical Revenue Growth of Segments Monitored by Stout Vs. Annual Health Expenditures and GDP Growth

Notes:

[a] For each period, total revenue figures are derived from the sum of all comparable companies listed in the appendix (Healthcare Public Company Analysis).

[b] CMS tracks National Health Expenditure Accounts (NHEA), which are the official estimates of total health care spending in the United States annually.

Source: www.cms.gov, Historical and Projected NHEA tables.

Healthcare M&A Market Update and Outlook

M&A Market Key Takeaways:

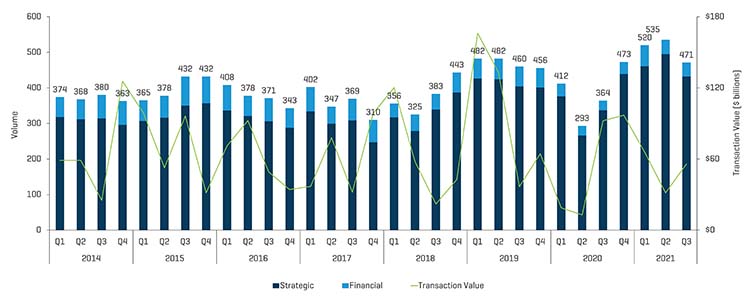

- M&A activity continued its strong run in the third quarter of 2021 with 471 deals announced and/or closed, a 23% increase from last year’s third quarter of 364 transactions. Volume did slip slightly from the record-high level of 535 in the second quarter of 2021, but activity remains incredibly robust.

- In addition to the prevailing economic strength, low cost of capital and dry powder available to private equity and strategic acquirors, the market strength stems from transactions that had been previously postponed due to Covid and the desire of founders to sell before year end 2021 and ahead of proposed Federal tax increases.

- Overall transaction value of deals announced and/or closed in third quarter 2021 came in at more than $57 billion, down from $92 billion in third quarter of 2020. As we have said in the past, the overall transaction value in a given quarter is typically impacted by the activity in Medical Devices, Life Sciences/Tools/Diagnostic, Biotech and Pharma companies, where the traditional avenue to liquidity is going public versus healthcare service providers that more often stay private and where deal values are not reported. For this reason, deal volume may be a more reliable barometer.

- The Medical Device and Life Science tools sectors had many of the largest transactions in the quarter, including Baxter International’s acquisition of Hillrom Holdings ($12.2 billion), ICU Medical acquiring Smiths Group ($2.35 billion), Medtronic buying Intersect ENT ($1 billion), Perkin Elmer buying BioLegend ($5.25 billion), GE Healthcare acquiring BK Medical ($1.45 billion), and Bioventus buying Misonix ($574 million). Other Medical device deals were Bruder Healthcare (pain management supplies), Walk Vascular (thrombectomy device), RPB Safety (powered air purifying respirators – Stout advised), PartsSource (CDMO), Zavation Medical Products (Spinal Implants), Fusion Robotics (Spine), and Devon Orthopedic Implants, among others.

- As mentioned previously, Merck’s $11.5 billion acquisition of Acceleron Pharma was another big contributor to transaction value in the quarter.

Q3 2021 M&A Transactions: Volume and Value

Source: Source: S&P Capital IQ and Stout Industry Research

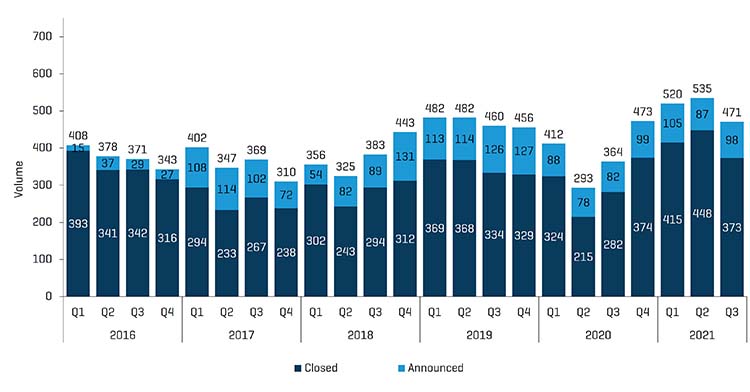

Historical M&A Transactions: Announced vs. Closed

Source: S&P Capital IQ and Stout Industry Research

Analysis of Healthcare Sub-Sector M&A Activity

M&A activity continues to flourish in many healthcare sub-sectors.

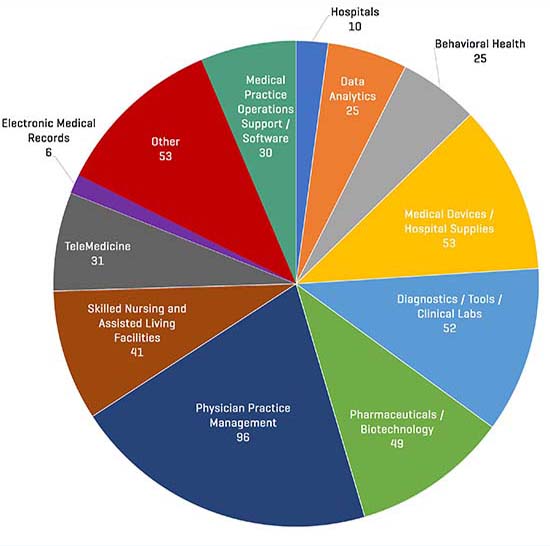

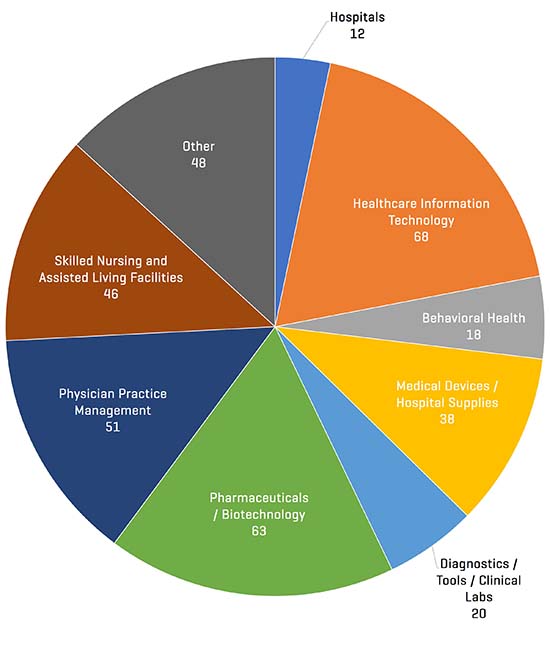

- Healthcare Information Technology (HCIT) and Physician Practice Management were the most active sectors in the quarter with 92 and 96 transactions, respectively, versus 68 and 51 a year ago.

- HCIT saw activity across many different sub-segments, led by 31 transactions in the TeleMedicine space. In addition, there were 30 transactions across the Medical Practice Operations Support / Software sub-sector, 25 transactions across the Data Analytics sub-sector, and 6 transactions across the Electronic Medical Records sub-sector.

- Physician Practice management continues to see activity across specialties, especially in Ophthalmology (10+ deals), dermatology (5+ deals), dental, radiology, primary care and urgent care, gastro enterology, urology, women’s health, fertility, ambulatory surgical centers and imaging centers, among others. Private equity has expressed a growing interest in new sub-sectors, particularly those segments that are fragmented with a host of ancillary services that can be added to scale the business. We have also seen recent activity in ENT and Allergy and Infectious Disease practices

- There were 53 medical device deals in the quarter versus 38 a year ago, whereas there were 52 deals in Diagnostics/Clinical Labs and Tools versus 20 a year ago.

- Activity levels in hospitals, skilled nursing and behavioral health are lower and stable versus a year ago.

Q3 2021 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

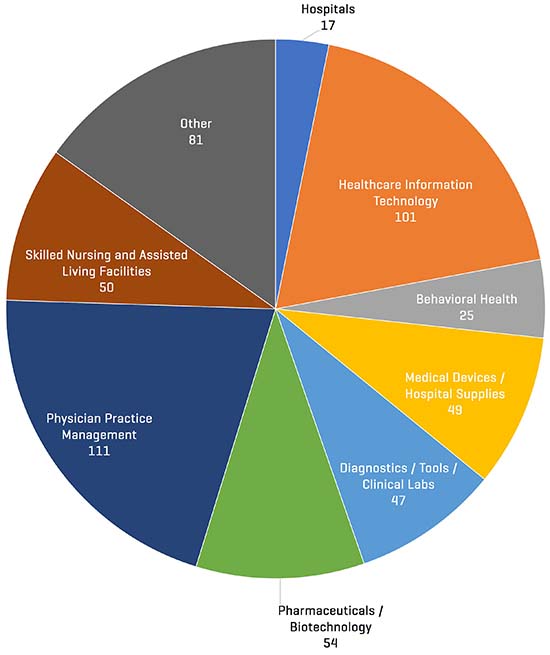

Q2 2021 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

Q3 2020 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

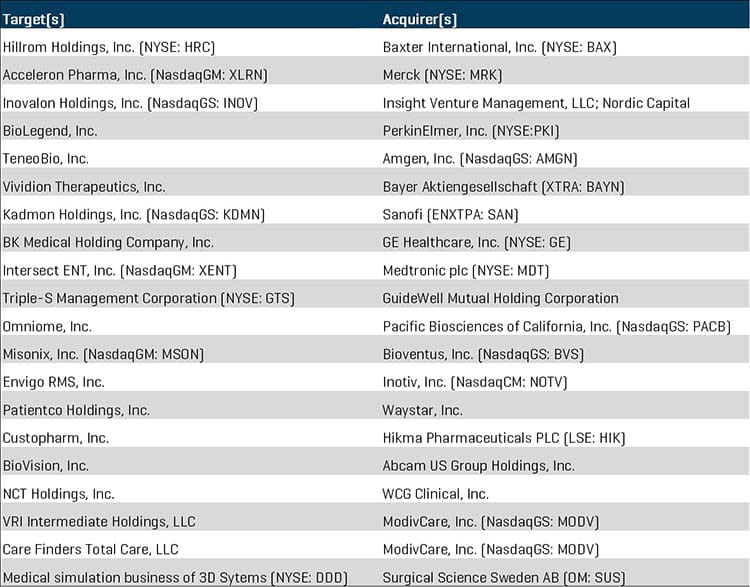

Notable Q3 2021 M&A Transactions

Baxter International, Inc. (NYSE: BAX) has announced a definitive agreement to acquire Hillrom Holdings (NYSE: HRC), a global medical technology provider, for approximately $12.4 billion, pending regulatory approval. Hillrom brings a highly complementary product portfolio and innovative pipeline of med-tech services to reach patients and clinicians across the care continuum.

Merck (NYSE: MRK) has announced its intention to acquire Acceleron Pharma, Inc. (NasdaqGM: XLRN) for approximately $11.5 billion. Acceleron is focused on developing leading therapeutics for the regulation of cell growth, differentiation and repair. The acquisition further bolsters Merck’s growing cardiovascular portfolio and pipeline of drugs.

Insight Venture Management and Nordic Capital have entered into a definitive agreement to acquire Inovalon Holdings, Inc. (NasdaqGS: INOV), a provider of cloud-based platforms driving data-driven healthcare, for an enterprise value of approximately $7.3 billion. The equity consortium will partner with Inovalon to continue developing technologies that enable the connectivity, aggregation and analysis of healthcare data to provide for better clinical outcomes across the healthcare ecosystem.

PerkinElmer, Inc. (NYSE: PKI) announced it will acquire BioLegend, Inc. for approximately $5.25 billion. BioLegend’s innovative portfolio in emerging, high-growth areas of biologics, cell and gene therapy, proteogenomics and recombinant proteins will enable PerkinElmer to accelerate discoveries in precision medicine.

Amgen (NasdaqGS: AMGN) announced a definitive agreement to acquire TeneoBio, Inc., a clinical-stage biotechnology company, for up to $2.5 billion. Tenebio’s portfolio of oncology assets and its new class of biologics, coined Human Heavy-Chain Antibodies, complements Amgen’s antibody research capabilities across therapeutic areas.

Bayer AG (XTRA: BAYN) has acquired Vividion Therapuetics, Inc. for approximately $1.5 billion, with an additional $500 million in earnout potential. Vividion’s platform is able to produce a variety of small molecule therapies across indications, with lead programs focused on targets relevant to oncology and immunology.

French-based Sanofi (ENXTPA: SAN) announced a definitive agreement to acquire Kadmon Holdings, Inc. (NasdaqGS: KDMN), a biopharmaceutical company, for approximately $1.9 billion. The acquisition will support Sanofi’s strategy to grow its General Medicines core assets with transformative therapies for disease areas of significant unmet medical needs, including Kadmon’s recently FDA-approved, first-in-class drug, Rezurock, for treatment of chronic graft-versus-host disease.

GE Healthcare (NYSE: GE) announced a definitive agreement to acquire BK Medical Holding Company, Inc., an innovator in global intraoperative imaging and surgical navigation, for a purchase price of $1.45 billion. GE Healthcare’s global presence and existing Ultrasound capabilities combined with BK Medical’s real-time surgical visualization will create an end-to-end offering through the full continuum of care.

Medtronic Plc (NYSE: MDT) announced a definitive agreement to acquire Intersect ENT, Inc. (NasdaqGM: XENT), a global provider of ear, nose, and throat medical technology, for approximately $1.1 billion. Intersect ENT’s portfolio of products, including its established line of sinus implants, complements Medtronic’s navigation, powered instruments, and existing tissue health products to provide a broader suite of solutions to ear, nose, and throat surgeons and care providers.

GuideWell Mutual Holding Corporation, a parent of Blue Cross and Blue Shield of Florida, has announced a definitive agreement to acquire Puerto Rican-based Triple-S Management Corporation (NYSE: GTS) for approximately $900 million. Triple-S Management is a leading health care services company with footprints in Puerto Rico and Florida with expertise in providing affordable health care.

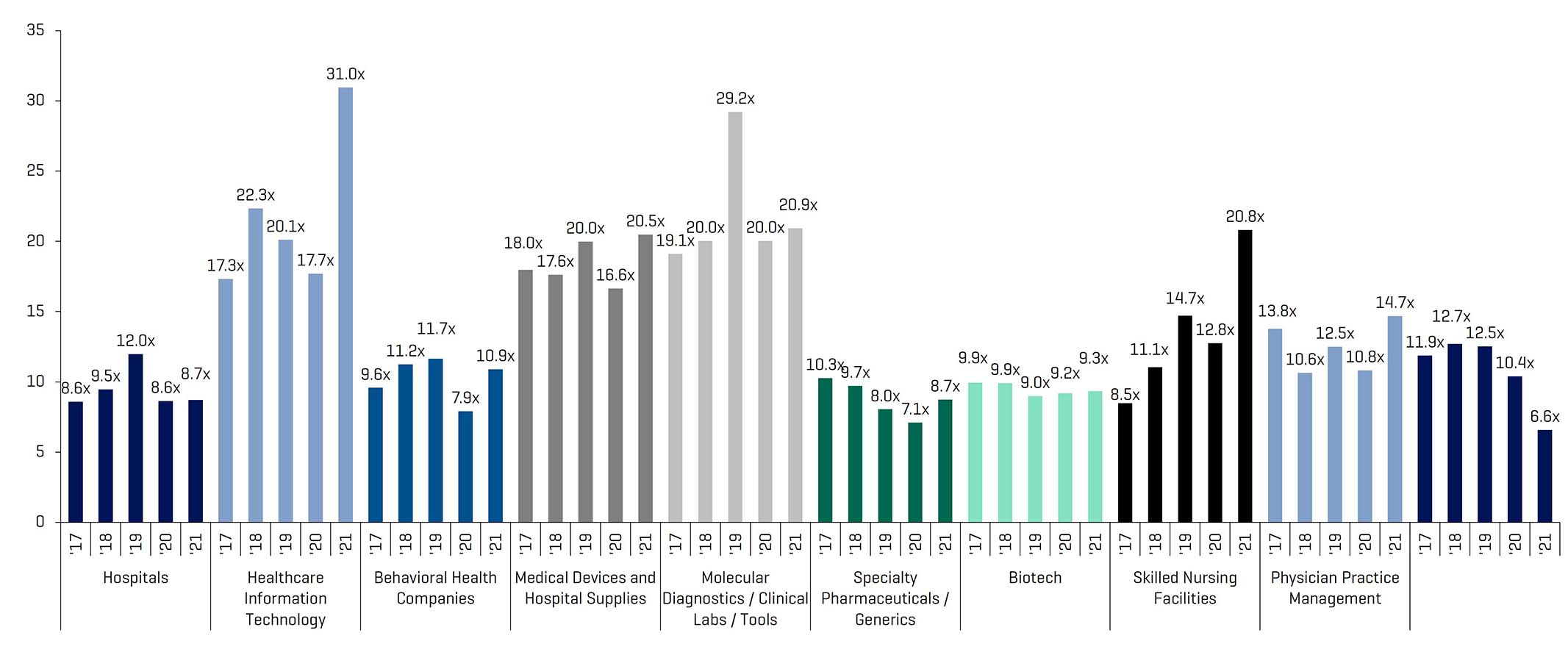

Public Comparable Companies: Historical and Forward EBITDA Multiples

Source: S&P Capital IQ; Multiples calculated from comparable companies universe that Stout tracks

Q3 2021 Largest M&A Transactions

Source: S&P Capital IQ

Healthcare Public Company Analysis