English

English

Despite robust transaction volume domestically and internationally in the first quarter of 2020, the industrial services industry experienced unavoidable disruptions across the board in the second quarter of 2020 as a result of the COVID-19 pandemic. Many “non-essential” businesses were forced to shut down their operations for much of the second quarter, causing tremendous volatility in public markets, which has since subsided as the nation has collectively begun to ease its health guidelines. In conjunction with the public markets, trading multiples trended negatively in the second quarter, with overall LTM EBITDA margins slightly contracting due to the lack of revenue generation from the forced shutdowns.

As businesses continue to refine their operations and procedures to combat the impact of the global pandemic, strategic buyers and private equity firms remain keen on investing in attractive, services-based commercial and industrial firms with competitive advantages such as “essential” status, a service suite necessary to keep large segments of the economy operating, and technological capabilities to boost overall revenue generation. The continued technological advancement and development of various industrial equipment and practices remain paramount and has propelled the industrial services industry to reach higher growth avenues as it pertains to complex predictive maintenance and the Industrial Internet of Things (IIoT). Although transaction volume drastically declined in the second quarter due to market volatility and an inability for buyers and sellers to forecast near and longer-term business conditions, private equity continues to look at deploying its massive capital overhang, as firms continue to bolster existing platform investments with diverse service offerings and geographic expansion.

The looming presidential election, domestic political campaign activity, and the federal government’s continued response to the COVID-19 pandemic will be headlines to watch in the second half of 2020 with respect to expected performance in industrial services.

Key Takeaways

- Industrial Services, in general, outperformed many sectors of the economy during COVID-19

- Sharp drop-off in transaction volume in the second quarter as a result of the COVID-19 pandemic

- Public equity performance nearing pre-COVID levels despite volatile first and second quarters

- Public company valuation multiples are slightly down year-over-year

- Uncertain macroeconomic trends to continue with evolution of global pandemic and looming Presidential Election

- “Essential” businesses which performed well during COVID-19 period will be even more sought after as clarity returns to the forecast period

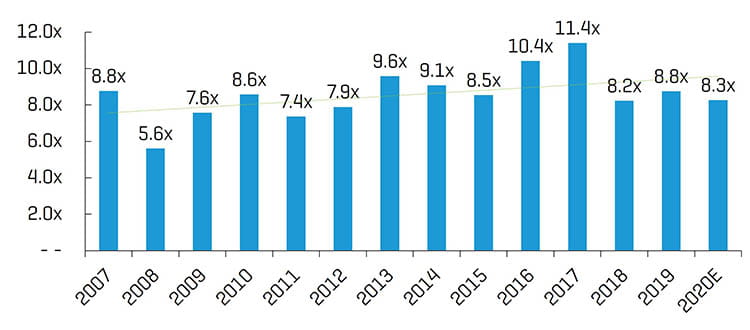

Historical Enterprise Value / EBITDA Multiples1

(1) Multiples above 20x are excluded from the mean/median calculation; data represents the overall median of all nine sub-segment benchmarks presented in this report

Industry Statistics

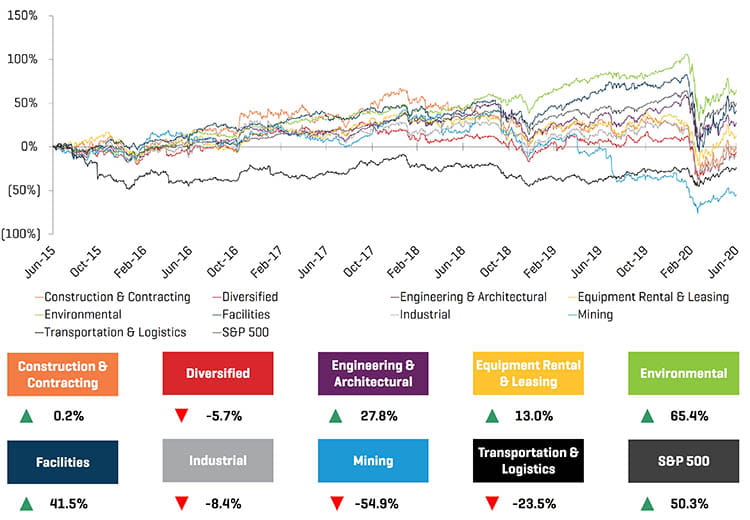

5-Year Historical Price Performance

Operating and Market Performance

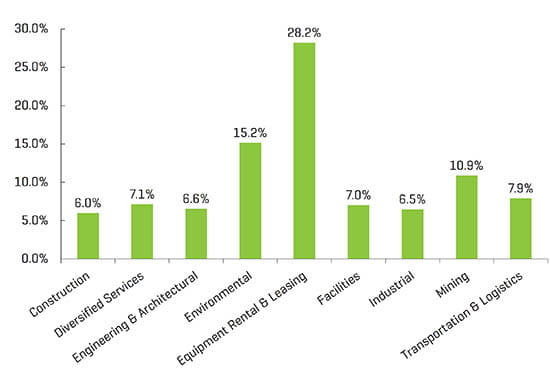

LTM EBITDA Margin

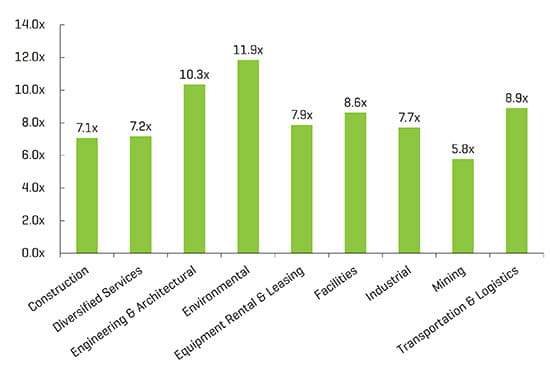

Enterprise Value / LTM EBITDA1,2

(1) Multiples above 20x are excluded from the mean/median calculation

(2) Median from public comp sets featured in report

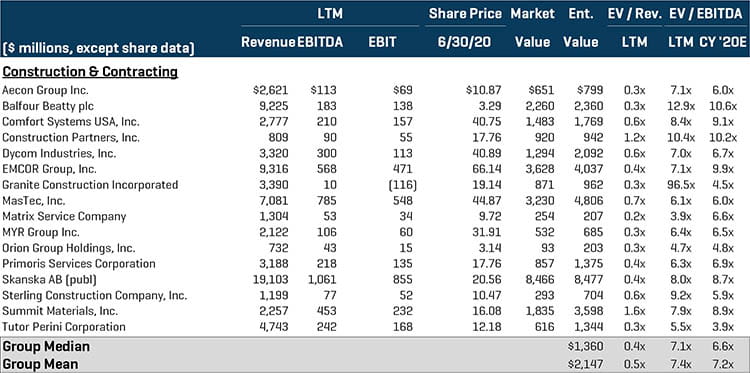

Construction & Contracting Services

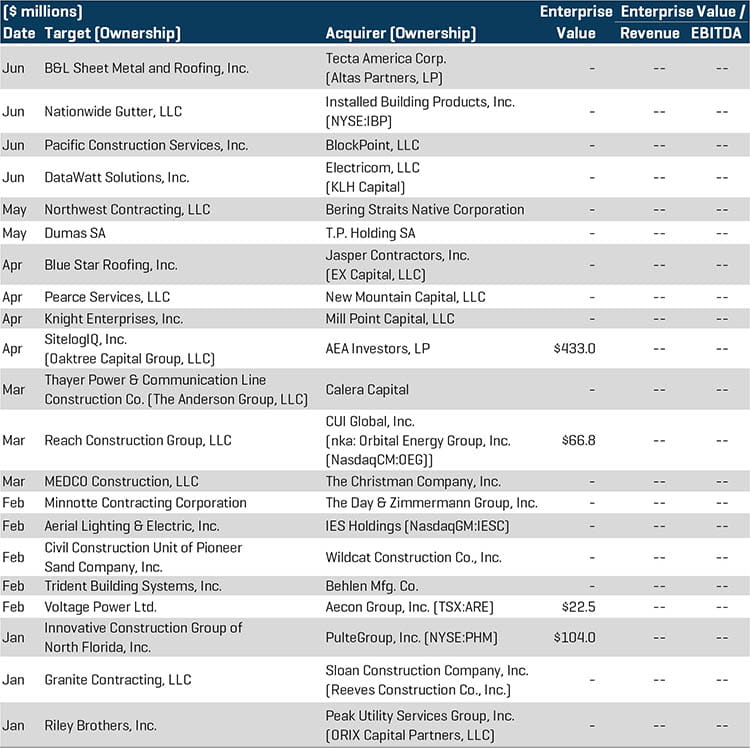

The construction and contracting services segment continued to be one of the more active segments in terms of M&A activity as evidenced by continued industry consolidation by both strategic and hybrid buyers. Despite many infrastructure projects that were underway pre-pandemic and a majority of new construction projects being put on hold during much of the second quarter, many operations were given the “essential” nod from state governments to resume work toward the end of the first half with tightened health procedures in place. Notable transactions include:

- SitelogIQ, Inc. was acquired by AEA Investors, LP for approximately $433.0 million in April. SitelogIQ provides facility planning, design, and management services to commercial buildings in the United States. This acquisition partners the private equity firm with SitelogIQ’s strong senior management team and enables the company to be a major player in the highly attractive energy services and contracting services industry which is benefiting from underlying growth trends such as aging infrastructure and continued focus on green initiatives.

- PulteGroup, Inc. (NYSE:PHM), an Atlanta-based homebuilder, has acquired Innovative Construction Group of North Florida, Inc. for approximately $104.0 million. Innovative Construction Group provides off-site solutions focused on single family and multifamily wood framed construction. This acquisition for PulteGroup progresses the homebuilder’s long-term strategy of attaining greater production efficiency and overall build quality with the ability to deliver high quality framing components with less waste; a persistent problem for the construction industry.

- Knight Enterprises, Inc., a provider of integrated communication infrastructure services, was acquired by Mill Point Capital, LLC. Mill Point Capital, a private equity firm based in New York, has extensive experience investing in the business services industry and will look to execute on multiple growth opportunities and other strategic initiatives to further bolster Knight’s strong track record and reliable customer service.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

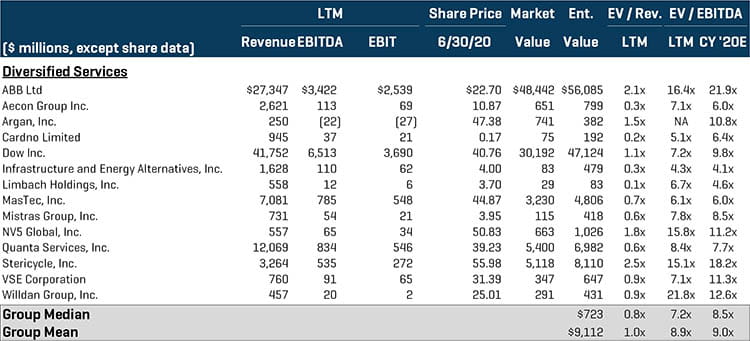

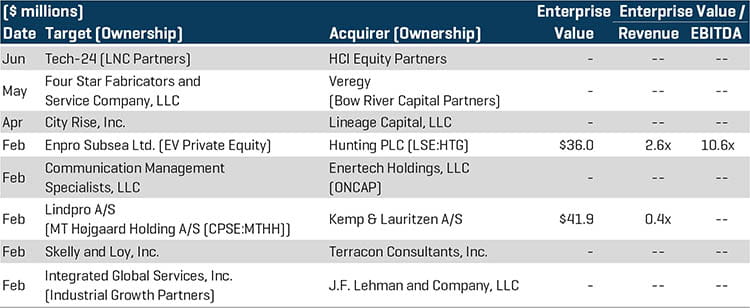

Diversified Services

The diversified services segment saw an overall decrease in transaction volume in the first half, which was greatly attributed to the global pandemic and the economic uncertainties that ensued. Hybrid and pure-play private equity buyers were particularly active in this segment, as they continue to pursue complementary service offerings and capabilities in order to diversify their existing portfolio holdings. Notable transactions include:

- Hunting PLC (LSE:HTG), an international energy services group, has acquired Enpro Subsea Ltd. for approximately $36.0 million. Enpro provides flow intervention, field decommissioning, and project management services for the recovery of subsea wells. With Hunting’s investment, Enpro will embark on a new chapter to globalize the business and enhance the delivery of the company’s production enhancing subsea technologies.

- Four Star Fabricators and Service Company, LLC, a mechanical contracting services provider based in Texas, has been acquired by Veregy, a portfolio company of Bow River Capital Partners. This transaction marks the eighth acquisition under the unified Veregy platform, as the partnership with Four Star enables the energy services company to address growing energy efficiency and power generation needs, as well as progress the company's overall long-term master planning goal of offering customized, high-value solutions to its customers across Texas.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

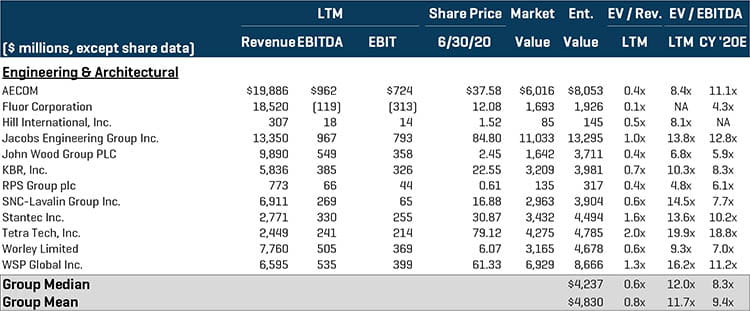

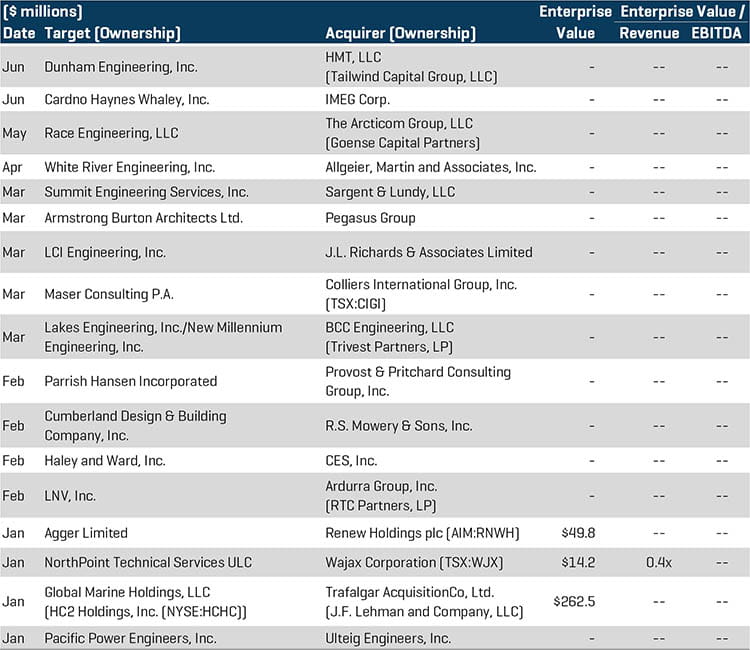

Engineering & Architectural Services

The engineering and architectural services segment continued to trade at a double-digit multiple – the second highest out of all the industrial services segments. Strategic buyers were the most active in the first half, executing several industry-consolidating transactions. Optimism around infrastructure spending post-COVID as part of one or more stimulus packages continues to drive interest in engineering firms given their position at the front of the construction pipeline. Notable transactions include [insert link to C/E Report]:

- Global Marine Holdings, LLC, a provider of offshore engineering services, has been acquired by Trafalgar AcquisitionCo, Ltd., an investment affiliate of J.F. Lehman and Company, LLC, for approximately $262.5 million. J.F. Lehman has extensive experience in the maritime industry and offers a unique combination of expertise, relationships, and capital that should enable Global Marine to pursue the numerous growth opportunities identified by the company’s management team.

- Renew Holdings plc (AIM:RNWH), an engineering services contractor in the United Kingdom, has acquired Agger Ltd. for approximately $49.8 million. Agger provides engineering services to the United Kingdom’s strategic highway network and was incorporated in 2016. Renew’s investment will expand the company’s position in the United Kingdom’s regulated highways sector and further drive the company’s interest in an attractive, new growth sector with long-term framework contracts and high barriers to entry.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

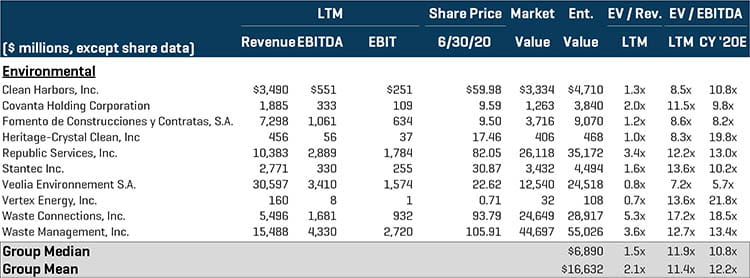

Environmental Services

The environmental services segment finished the first half trading at the highest overall multiple among its industrial services peers. The segment’s overall success in the first half has been driven by the “essential” nature of the services provided by industrial participants. As a result, while many other industrial service segments partially or completely ceased operations for much of the second quarter, the demand for environmental services remained relatively unchanged and is poised for further growth stemming from the outcomes of the pandemic. Additionally, a renewed light has been shed on the topic of highly sustainable and health-conscious environmental practices, thus driving future growth initiatives as a result of COVID-19. Despite the uncertain economic period, both private equity and strategic buyers remained active in terms of M&A and executed several industry-changing transactions. Notable transactions include:

- KKR & Co., Inc. (NYSE:KKR) made two noteworthy environmental services acquisitions in the first half. The private equity firm acquired Viridor Ltd., a waste management services company in the United Kingdom, for nearly $4.9 billion and ESG Group, a medical waste disposal services provider, for approximately $755.5 million, respectively. These two acquisitions significantly bolster the private equity firm’s position in the overall global environmental services segment, as the firm will look to continue to build critical infrastructure and help the United Kingdom meet long-term sustainability and environmental goals.

- Harsco Corporation (NYSE:HSC), a diversified environmental solutions provider for industrial and specialty waste streams, acquired the Domestic Environmental Solutions Business of Stericycle Environmental Solutions, Inc. for approximately $462.5 million. The business segment of Stericycle comprises various hazardous waste services, and this acquisition for Harsco further accelerates the company’s long-term plan of transforming into a global, market-leading, single-thesis environmental solutions platform.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

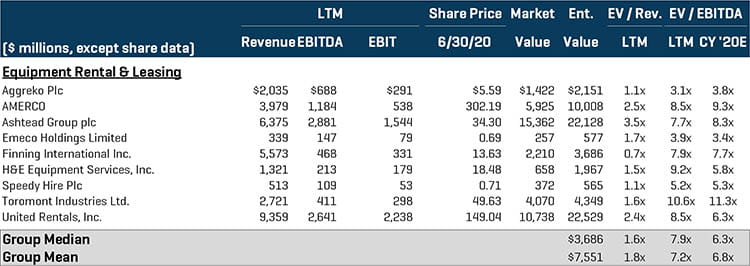

Equipment Rental & Leasing

Private equity and hybrid buyers remained active throughout the first half in terms of M&A activity, as acquirers were focused on expanding the scale, product offerings, and geographic reach of current platform investments. As more construction projects come back online and are developed through the pipeline, activity within the equipment rental & leasing segment is expected to increase in the second half of 2020. Notable transactions include:

- Strad, Inc., a provider of rental equipment and matting solutions to the oil & gas industry, has been bought out by select employees of the company and their affiliates for approximately $112.7 million. Following completion of the transaction, Strad’s shares were delisted from the TSX and the private entity will continue to be run by the current management team.

- HILO Equipment & Services, LLC has been acquired by Alta Equipment Group, Inc. (NYSE:ALTG) for approximately $17.3 million. HILO, founded in 1977, operates as a dealer of material handling equipment. Alta’s acquisition of HILO is aligned with the company’s growth strategy by expanding its distribution footprint with stable OEMs and strengthens the company’s presence in the robust New York equipment rental market.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

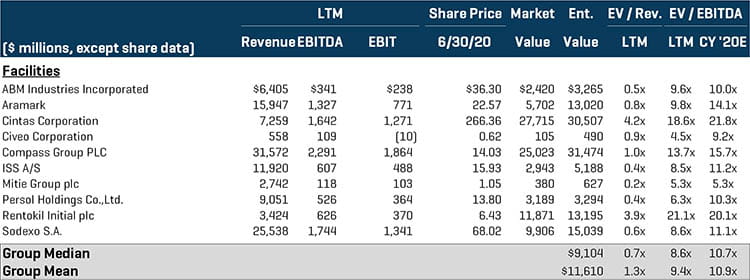

Facilities Services

The facilities services segment saw a mix of hybrid buyers diversifying their current holdings and private equity buyers investing in the space for the first time. Several roll-up strategies among interested buyers were seen in this space in the first half, as the health and safety procedures of commercial buildings remains paramount as the population slowly returns from the work-from-home environment. Moving forward, emphasis on health safety and regulatory compliance will continue to develop as the pandemic ensues, thus pushing the importance of facilities services into the industrial services spotlight. Notable transactions include:

- Mitie Group plc (LSE:MTO) announced it has entered into a sale and purchase agreement to acquire Interserve Facilities Management Ltd., a facilities management solutions provider, for approximately $504.4 million. The transaction is still in process and is expected to close in the fourth quarter this year. Upon completion, the combined entity will be one of the United Kingdom’s largest facilities management providers with coverage throughout the country.

- Har-Bro, Inc., a California-based provider of emergency restoration and reconstruction services to commercial and residential buildings, has been acquired by BlueSky Restoration Contractors, LLC, a portfolio company of Dominus Capital, LP. The Har-Bro acquisition marks the fourth such acquisition Dominus Capital has made to support BlueSky’s growth and brings Har-Bro’s strong, well-established reputation along the West Coast into the platform’s mix.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

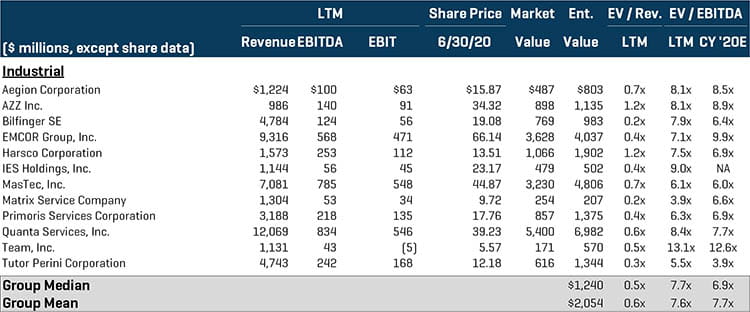

Industrial Services

The industrial services segment continued to be an attractive segment for private equity buyers given its inherently “essential” nature, despite the many economic uncertainties plaguing the first half. Several notable private equity firms continued to diversify their portfolios through roll-up and add-on strategies. Although overall deal volume was down for the industrial services segment in the first half, quality assets with strong product and service offerings remain available. Notable transactions include:

- KAEFER Isoliertechnik GmbH & Co. KG, a German integrated services and solutions provider to the construction industry, has acquired Wood Group Industrial Services Ltd. for approximately $118.0 million. KAEFER and Wood Group’s industrial services businesses will combine into one company operating as KAEFER throughout the United Kingdom and Ireland. The entity will realize joint expertise in capabilities and provide additional capacities and project management abilities.

- StandardAero Business Aviation Services, LLC, a subsidiary of Dubai Aerospace Enterprise (DAE) Ltd., has acquired TRS Ireland for approximately $51.4 million. TRS, headquartered in Ireland, provides component repair services and process solutions for industrial, aero derivative, and aircraft gas turbines. The acquisition of TRS gives StandardAero nearly 70,000 additional square feet of MRO operations and an installed base of highly recurring blue-chip customers.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

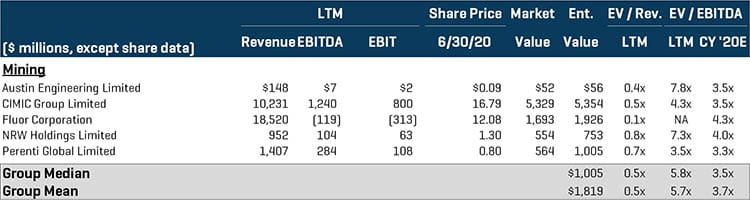

Mining Services

The mining services segment’s M&A activity continued to be dominated by international acquirers in the first half, as the industry saw strategic buyers being the most acquisitive. As more consolidating transactions occur, access to attractive geographic locations remains paramount in order to sustain profit margins. Notable transactions include:

- TerraCom Limited (ASX:TER), an Austrailian coal miner and producer, has acquired Universal Coal plc (ASX:UNV) for approximately $105.8 million. TerraCom was already the largest shareholder in Universal, a coal miner and producer in the United Kingdom, and upon completion of the transaction, the stock was delisted from the ASX on July 3rd, 2020.

- Deere & Ault Consultants, Inc., a provider of mine reclamation and geotechnical services in Colorado, has been acquired by Schnabel Engineering, Inc. Schnabel’s acquisition of Deere & Ault meaningfully expands the company’s national presence, increasing the capabilities provided to its established customer base.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

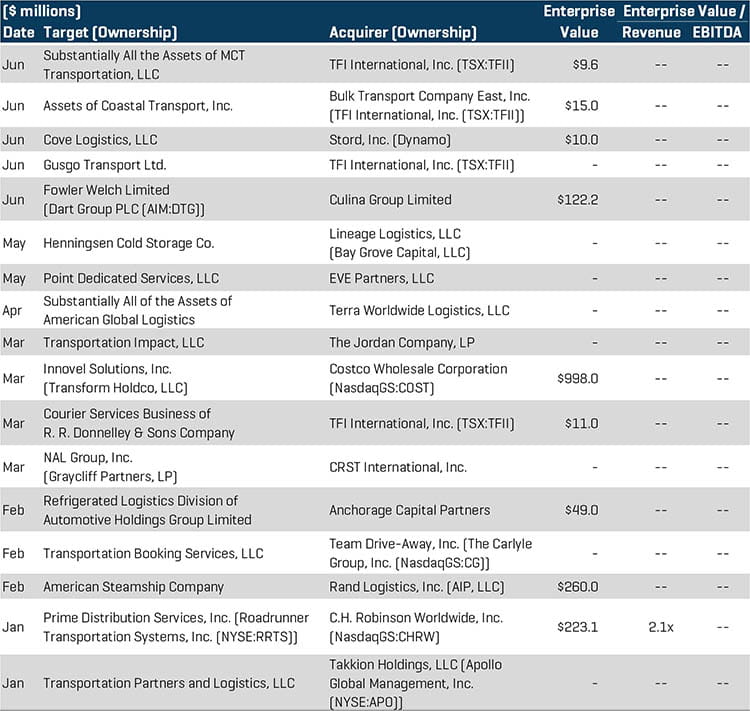

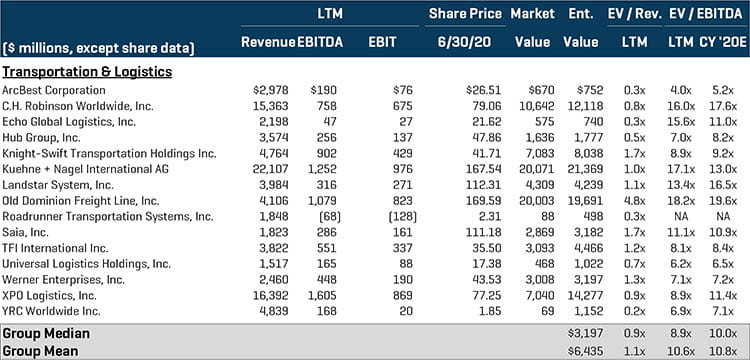

Transportation & Logistics

The transportation & logistics segment continued to be one of the more active segments as it pertains to M&A activity. Both strategic and private equity buyers made several notable transactions in the first half, as targets are looking to capitalize on strong industry tailwinds and execute growth initiatives. As more retail shifts from a traditional brick-and-mortar marketplace to an online platform, which has been accelerated by the various stay-at-home orders enforced during the nationwide quarantine, quality transportation & logistics assets will see their valuations increase as the pandemic further drives the highly essential nature of the transportation & logistics industry. Notable transaction include:

- Costco Wholesale Corp. (NasdaqGS:COST) has acquired Innovel Solutions, Inc. for approximately $998.0 million. Innovel, headquartered in Hoffman Estates, IL, provides supply chain solutions to the retail, manufacturing, commercial, and military markets throughout the United States. Costco, a customer of Innovel since 2015, gains access to Innovel’s “final mile” delivery and logistics platform with a network that covers approximately 90% of the United States and Puerto Rico.

- Rand Logistics, Inc., a portfolio company of AIP, LLC, has acquired American Steamship Company, a provider of waterborne dry-bulk transportation services, for approximately $260.0 million. Rand’s acquisition gives the company the capability to meet almost every type of dry bulk transportation need on the Great Lakes and the combined business will move almost 50 million tons of dry bulk commodities annually.

- Roadrunner Transportation Systems, Inc. (NYSE:RRTS) has sold its subsidiary, Prime Distribution Services, Inc., to C.H. Robinson Worldwide, Inc. for approximately $223.1 million. Prime provides warehousing, cross-docking, packaging, and multi-vendor freight consolidation services. The acquisition is expected to be slightly accretive in 2020, as C.H. Robinson looks to bring scale and value-added warehouse capabilities to the company’s consolidated platform of global services.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions