Français

Français

A trademark is defined by the United States Patent and Trademark Office (USPTO) as “a word, phrase, symbol, and/or design that identifies and distinguishes the source of the goods of one party from those of another.”1 A properly developed trademark should quickly communicate positive or prominent characteristics of a company or product to the market. In this sense, a trademark can be an impactful, cost-effective marketing tool for companies that wish to monetize the goodwill they have built with consumers. Generally, an effective trademark should provide its owner with the ability to charge a price premium, increase sales volume, or maintain higher market share than competitors with less effective trademarks. These economic benefits generate increased profits and, as a result, underlie the value of trademarks for their owners.

For many companies, particularly those that market directly to consumers, trademarks are very serious business. Figure 1 identifies the most valuable brands in the world based on a recent study performed by Brand Finance, a brand consultancy firm. Although the trademark is only one component of a company’s brand, it typically represents the most important component that leads to brand value.

While the values of the trademarks associated with these multibillion-dollar brands may be exceptional, the basic methods for determining their values are no different than those for the trademarks of any other business.

Reasons for Valuing Trademarks

Trademarks are regularly valued for a variety of reasons, including:

- To develop pricing or deal terms for transactions such as a purchase or sale, a license, or a contribution to a collaboration like a joint venture or co-branding initiative

- To aid in the development and execution of certain corporate or individual tax strategies, or to comply with tax regulations, associated with intercompany transfers (i.e., transfer pricing), corporate reorganizations, and trust and estate issues3

- To enable the raising of capital by using the trademark as collateral for debt financing or to attract equity investment

- To assist with various aspects of bankruptcy proceedings, including issues associated with avoidable preferences, fraudulent transfers/conveyances, determining solvency/insolvency, addressing adequate protection, and the potential use of trademarks as collateral for debtor-in-possession financing, among others

- To calculate damages related to certain types of commercial disputes in which the value of a trademark has been diminished or lost, or where the value is contested by the parties

- To report values on corporate balance sheets, particularly in the context of a purchase price allocation associated with the merger or acquisition of a business

Approaches to Valuing Trademarks

Three approaches are typically considered in determining the value of trademarks:

Cost Approach: a general way of determining a value indication of an individual asset by quantifying the amount of money required to reproduce or replace the future service capability of that asset

Market Approach: a general way of determining a value indication of a business, business ownership interest, security, or intangible asset by using one or more methods that compare the subject to similar businesses, business ownership interests, securities, or intangible assets that have been sold

Income Approach: a general way of determining a value indication of a business, business ownership interest, security, or intangible asset using one or more methods that convert anticipated economic benefits into a present single amount4

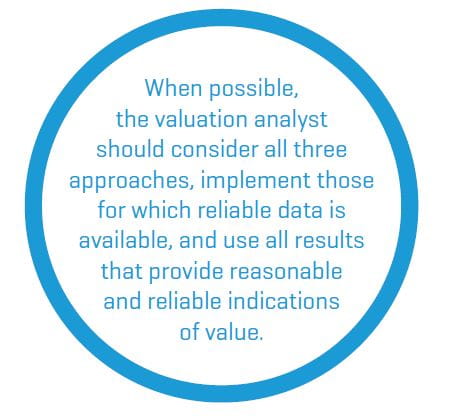

The results derived from the implementation of each these approaches are considered to be “indications of value,” and they are typically evaluated based on their respective merits, on a case-by-case basis, to arrive at a final conclusion of value. To the extent more than one indication of value is available in a particular valuation analysis, the weight given to each can vary based on the specific facts and circumstances of the valuation. In most circumstances, and when possible, the valuation analyst should consider all three approaches, implement those for which reliable data is available, and use all results that provide reasonable and reliable indications of value.

When trademarks are valued using the three traditional approaches, certain issues are particularly relevant.

Cost Approach

When considering the cost to replace the future service capability of a trademark, in many cases valuation analysts focus on the advertising/marketing expenses that would be necessary to develop the same or a similar trademark. The underlying theory behind the focus on advertising/marketing expenses is that the value of a trademark is contingent, at least in part, on the trademark’s popularity among consumers in the markets in which it is used. Advertising/marketing costs are often central to building the trademark’s positive reputation, which, in turn, can drive price premiums and/or market share gains. Of course, other expense items such as government registrations and legal fees, among others, may also be applicable to the analysis.

In many instances, the historical costs incurred to promote the trademarked products provide a reasonable proxy for the costs that would need to be incurred at and after the valuation date to replace the asset. However, when relying on historical costs, the valuation analyst must consider whether material differences exist between the historical environment and the environment likely to prevail in the future, and whether these differences require an adjustment to the historical costs. For example, historical costs may need to be adjusted to account for inflation between the dates the costs were incurred and the valuation date. As another example, the valuation may need to address the fact that, in many industries, today’s advertising/ marketing environment places a stronger focus on digital marketing strategies, which may have a different cost structure than more traditional print, radio, and television advertising methods that were most common in the past.

Another important issue to consider is any obsolescence associated with the trademark as of the valuation date. For example, if one is valuing a trademark that was more popular in the past than it is as of the valuation date, the valuation analyst may wish to rely only on historical costs incurred to obtain the same level of popularity the trademark enjoys as of the valuation date, excluding costs associated with helping the trademark reach a peak level of prominence that is no longer applicable.

Market Approach

The use of the Market Approach to value a trademark is challenging for at least two primary reasons:

- There are very few publicly available trademark sales for use in identifying transactions and prices paid for comparable assets (comps)

- Trademarks are by definition unique and, given that, it can be relatively difficult to assess comparability between a trademark being valued and other similar trademarks. For example, if a valuation analyst is trying to value the Coca-Cola® trademark based on prices paid for other soft drink trademarks, how can he or she account for the differences between Coca-Cola and the comps to determine an indication of value?

One method of addressing differences between the trademark being valued and the comps is to perform an assessment of various characteristics of the relevant trademarks, including, but not necessarily limited to:

- Popularity (as measured by recognition surveys, website visits, product sales/market share, or other means)

- Level of profitability realized on products for which the trademark is used

- The extent of any price premium realized on the products for which the trademark is used

- The extent of historical and potential future uses of the trademark across multiple product categories

Analysis of these characteristics may allow the valuation analyst to make an informed judgment regarding how to use and/or adjust the comps to account for key differences, yet still rely on the Market Approach to conclude on an indication of value.

Income Approach

Implementation of the Income Approach requires the valuation analyst to determine the present value of future incremental cash flows attributable to the trademark being valued. This objective requires the determination of four primary variables:

- The strategic use of the trademark, such as in product sales, licensing, enforcement, and/or for defensive purposes

- The amount of the cash flows

- The timing of the cash flows, including when they start and when they end (i.e., remaining useful life)

- The risks of the cash flows

The nature of the cash flows associated with a trademark typically includes the use of the trademark in the sale of one or more products with which the trademark is associated. For this business model, there are multiple methods for determining the amount of the incremental cash flows attributable to the trademark.

One such commonly relied-upon method is the “relief from royalty method,” which has been defined as “a valuation method used to value certain intangible assets (for example, trademarks or trade names) based on the premise that the only value that a purchaser of the assets receives is the exemption from paying a royalty for its use. Application of this method usually involves estimating the fair market value of an intangible asset by quantifying the present value of the stream of market-derived royalty payments that the owner of the intangible asset is exempted from or relieved from paying.”5 In the implementation of this methodology, a valuation analyst identifies the future sales of the products that use the trademark, multiplies those sales by an appropriate royalty rate that the owner would otherwise have to pay to license the trademark if it did not own it, and then discounts the after-tax theoretical royalty savings to the valuation date. This methodology is sometimes considered to be a hybrid of the Income and Market Approaches, as the royalty rate used in the analysis is typically based on market-based royalty rates from licenses or other transactions for similar trademarks.

A second commonly relied-upon method to estimate the amount of the incremental cash flows attributable to the trademark is what is sometimes referred to as the analytical approach or, informally, the “with-and-without” method. In one implementation of this method, the valuation analyst quantifies the price premium associated with the product(s) for which the trademark is used, compared with similar products that use lesser known trademark(s). For the purposes of this analysis, the price premium paid for a product that is very similar or identical to another product (other than the use of the trademark) is properly attributable to the trademark. A classic example of this phenomenon is evident in the market for many over-the-counter drugs. For example, the price of Tylenol® will typically be higher at a local pharmacy than that of the generic store brand acetaminophen. However, both the branded version and the generic version have exactly or almost the same ingredients and provide the same outcomes to users. The with-and-without method relies on the generally accepted theory that consumers are willing to spend more money on the Tylenol-branded version despite the similarities of the two products because they have a positive association with the trademark, which they likely believe communicates something about the quality and/or trustworthiness of the product that bears it.

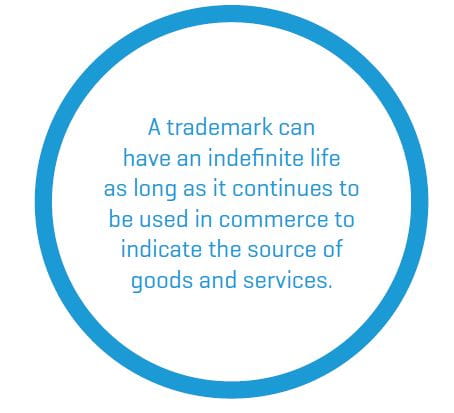

When considering the timing of the cash flows for the implementation of the Income Approach, the valuation analyst must carefully consider how long into the future the cash flows should be modeled. A trademark can have an indefinite life as long as it continues to be used in commerce to indicate the source of goods and services.6 Although a trademark can legally have an indefinite life, in some cases, trademarks have limited expected lives, and the discounted cash flow model should reflect this expectation, as appropriate. The valuation analyst should gather information related to the trademark owner’s historical and future expected use of the asset to determine the remaining useful life of the trademark.

- “Trademark, Patent, or Copyright?” United States Patent and Trademark Office

- “Global 500 2017: The Annual Report on the World’s Most Valuable Brands,” Brand Finance, February 2017.

- The authors are not tax experts and, as such, are not providing any tax advice on which readers should act. We take no responsibility for actions taken by readers based on our description of trademark-based tax strategies that we understand, from our experience as valuation analysts, are used in certain circumstances.

- “International Glossary of Business Valuation Terms,” Statement on Standards for Valuation Services No. 1, Valuation of a Business, Business Ownership Interest, Security, or Intangible Asset, American Institute of Certified Public Accountants, 2007.

- “International Glossary of Business Valuation Terms,” Statement on Standards for Valuation Services No. 1, Valuation of a Business, Business Ownership Interest, Security, or Intangible Asset, American Institute of Certified Public Accountants, 2007.

- “Trademark, Patent, or Copyright?” United States Patent and Trademark Office