English

English

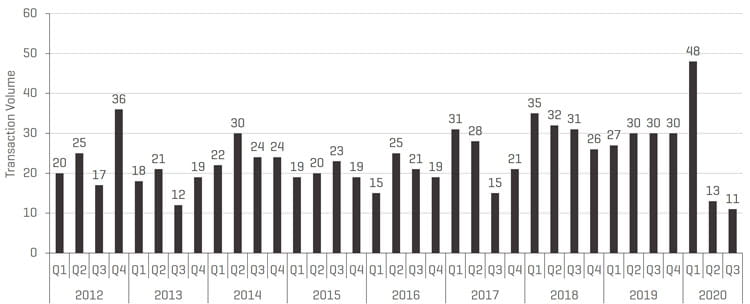

Not surprisingly, the second quarter of 2020 saw a substantial decrease in the number of announced North American metal forming transactions. Quarterly transaction volume decreased 73% from a record first quarter of 2020 and 57% from the same quarter last year. The significant slowdown in activity illustrates the ramifications and impacts of the COVID-19 pandemic and the associated shut down and travel restrictions. However, the beginning of the third quarter has shown a slight increase in volume as sellers slowly return to the market and delayed second-quarter transactions close: 11 transactions were announced in July and August thus far. While buyers and lenders continue to approach new deals with caution, healthy deals entering the market are generating significant interest.

Key Takeaways:

- After a record start to the year, metal forming transaction volume saw a significant decline in the second quarter

- Financial buyers continue to dominate metal forming transaction volume

- Abundant capital available from private equity and strategic buyers, but fewer new deals coming to market

- New transactions are currently attracting significant interest given the supply-demand imbalance between sellers and buyers

- Uncertainty around debt financing is easing with non-bank lenders aggressively pursuing deals

- Special situations M&A activity has not yet taken off, but is expected to increase

- Public company share prices and valuations suffered in the first quarter due to historic declines in the stock market but have since bounced back in the historic market rally that began towards the beginning of the second quarter

QUARTERLY NORTH AMERICAN METAL FORMING M&A VOLUME (THROUGH AUGUST 25, 2020)

Source: Stout Research

Stout Proprietary Metal Forming M&A Database Highlights

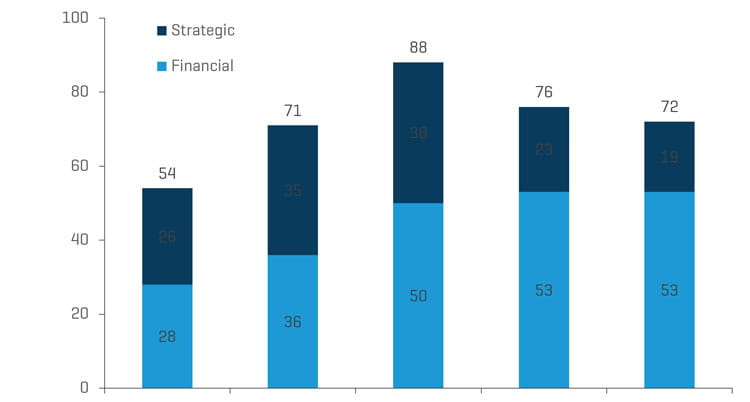

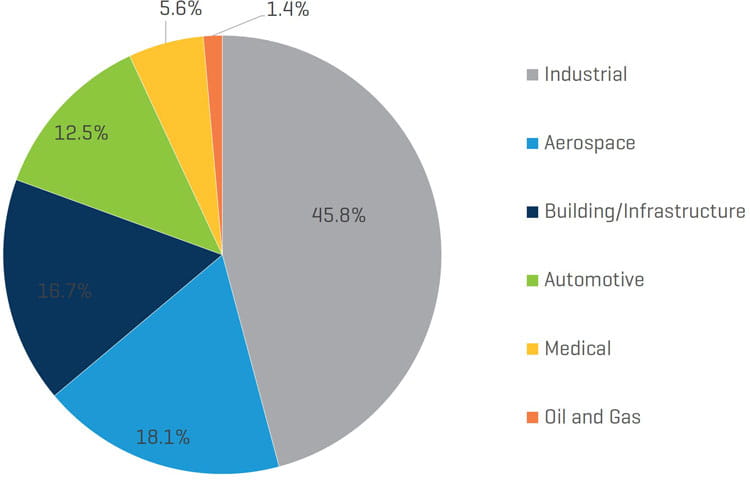

Financial buyers accounted for approximately three-fourths of North American metal forming transaction volume, roughly in line with the same period last year. Industrials continue to comprise the bulk of transaction activity, accounting for 46% of total deals announced year-to-date. Volumes across all metal forming sectors were relatively flat versus the prior year-to-date period, with 2020 transactions heavily skewed toward the first quarter.

SHARE OF TRANSACTIONS BY BUYER TYPE (YTD THROUGH AUGUST 25, 2020)

Source: Stout Research

YEAR-TO DATE TRANSACTION VOLUME BY SECTOR

Source: Stout Research

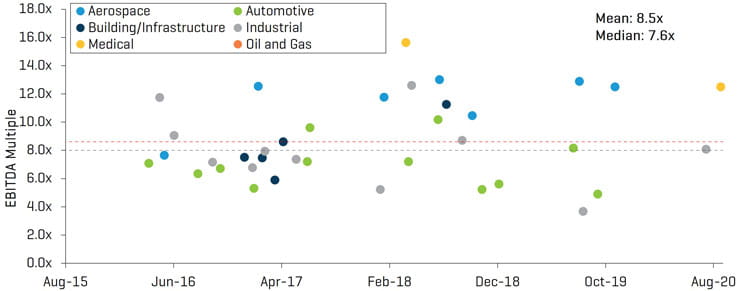

Notable transactions announced year-to-date through August 2020 include:

- NN Inc.’s (Nasdaq:NNBR) announced divestiture of the company’s Life Sciences business to MW Industries, Inc., a portfolio company of American Securities, LLC for a total consideration of $825 million (about 12.5x 2020E adjusted EBITDA)

- Stanley Black & Decker Inc.’s (NYSE:SWK) acquisition of Consolidated Aerospace Manufacturing, LLC from Tinicum L.P. for approximately $1.5 billion, or 4.0x 2019 revenue

- RTI Surgical Holdings, Inc.’s (Nasdaq: RTIX) divestiture of the Company’s OEM business to Montagu Private Equity LLP for a total consideration of $440 million.

- Kymera International’s, a portfolio company of Palladium Equity Partners, LLC, acquisition of Reading Alloys from AMETEK, Inc. (NYSE:AME) for approximately $250 million, or 1.6x annual revenue

- Placements CMI Inc. (Marcel Dutil family), Fonds de solidarité FTQ and Caisse de dépôt et placement du Québec’s acquisition of the Canadian operations and certain assets in the United States and Overseas of Canam Group Inc. for CAD 840 million

- Bendix Commercial Vehicle Systems LLC’s acquisition of R. H. Sheppard Co., Inc. from WABCO Holdings Inc. (NYSE:WBC) for approximately $150 million

SELECT TRANSACTION EV/EBITDA MULTIPLES

Source: Stout Research

Public Company Performance

After a major downturn in the public markets associated with the economic ramifications of COVID-19, a strong rally in the second quarter of 2020 brought the Dow up approximately 17% year-to-date, while the S&P 500 and NASDAQ were up 20% and 31%, respectively. Within the metal forming industry, EV/EBITDA multiples as of August for most sectors were above or near year-end 2019 trading multiples.

PUBLIC COMPANIES: LAST TWELVE MONTHS (LTM) EV/EBITDA MULTIPLES (DECEMBER 31, 2014 TO AUGUST 25, 2020)

Source: S&P CapIQ

PUBLIC COMPANIES: LTM EBITDA MARGINS (DECEMBER 31, 2014 TO AUGUST 25, 2020)

Source: S&P CapIQ

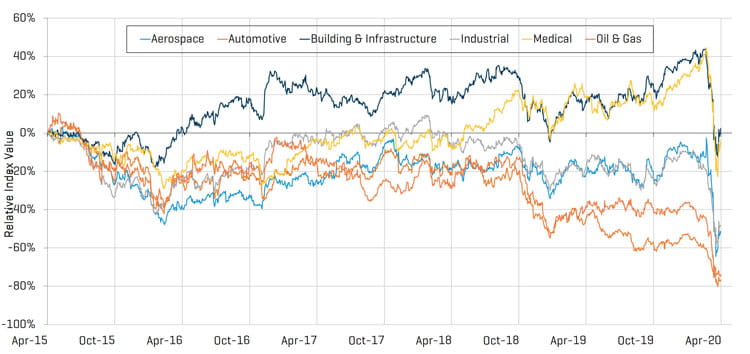

As expected, all metal forming indices saw negative impacts within the first quarter from market volatility surrounding COVID-19. Despite the initial downward pressure, the market rally in the second quarter produced significant increases across all sectors, with Building & Infrastructure and Medical trading well above August 2015 levels.

PUBLIC COMPANIES: RELATIVE SHARE PRICE PERFORMANCE (AUGUST 1, 2015 TO AUGUST 25, 2020)

Source: S&P CapIQ

Metal Pricing

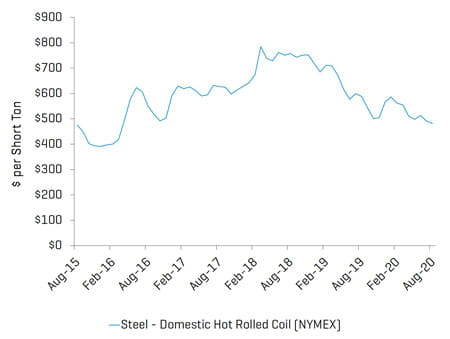

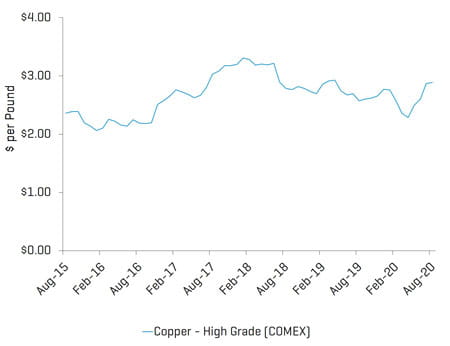

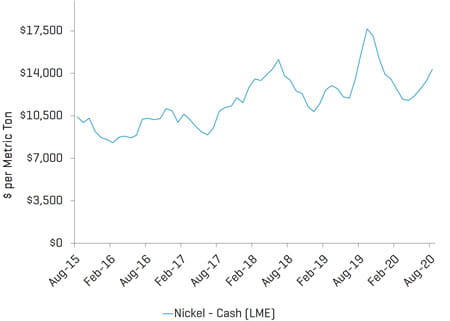

Domestic metals prices suffered in the first quarter from anticipated declines in automotive, commercial aerospace, construction and other industrial sectors. Copper, nickel, and aluminum all saw a recovery through the second quarter while steel continues to see effects of reduced demand due to halts and slowdowns in key consuming sectors.

STEEL

Source: S&P CapIQ

COPPER

Source: S&P CapIQ

NICKEL

Source: S&P CapIQ

ALUMINUM

Source: S&P CapIQ

This industry update analyzes Stout’s custom public company indices and proprietary M&A transaction database of North American metal forming transactions. Targeted companies include casting, extrusion, finishing, forging, machining, stamping, and various other processing and fabrication businesses across a wide range of end markets.