Food & Beverage Industry Update - Q3 2019

Subscribe to Industry UpdatesFood & Beverage Industry Update - Q3 2019

Subscribe to Industry UpdatesValuations Remain at Elevated Levels

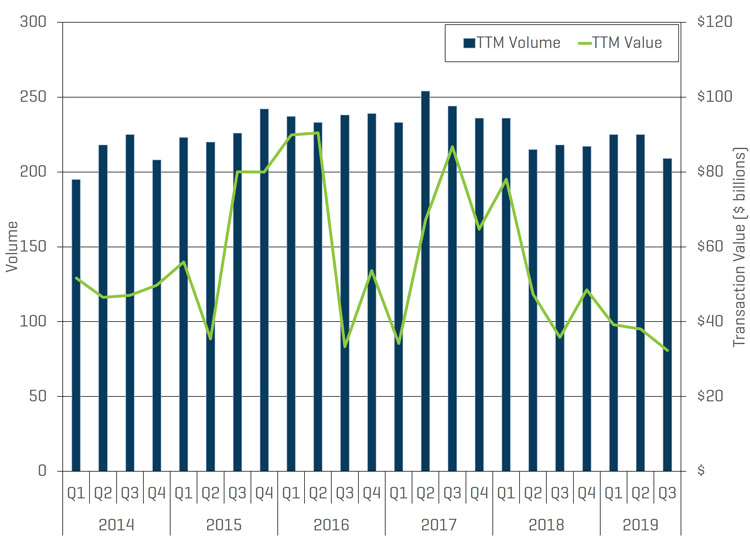

Strong Food & Beverage (F&B) industry M&A activity continued through the third quarter of 2019 with 39 completed transactions during the quarter; although this represents a 29% decrease year over year (YoY), the headline number masks a resurgence in financial buyer / private equity activity. Trailing 12-month (TTM) volume is down a modest 4% with 209 transactions completed while reported TTM value declined approximately 9% to $32.4 billion (a rash of large deals completed in late 2017 / early 2018 skews the comparison).

Barring an extraneous geopolitical event (e.g. severely escalating trade war with China, war with Iran) we expect the remainder of 2019 to be robust given 1) valuations remain at peak levels, 2) credit markets are still highly accommodative, 3) private equity’s capital overhang is at historical highs, and 4) strategic buyers continue to seek accretive growth at all costs (though they are increasingly finding themselves outbid by financial buyers).

Key Q3 Takeaways

- Continued strong overall F&B industry M&A activity

- Overall volume down 4% YoY

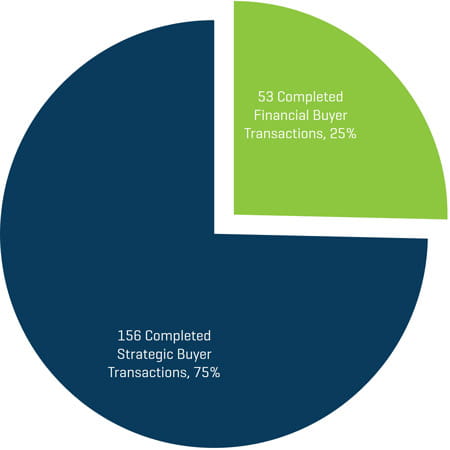

- Financial buyer activity has surged in the trailing 12 months – up 47% YoY

- Cross-border M&A activity has been tempered by trade tensions (particularly with respect to China, which has severely curtailed its U.S.-based buying spree)

- Private market valuations remain strong despite recent volatility in public market stock prices

- Debt and equity financing remain in ample supply and at attractive rates

- Key macroeconomic indicators remain solid

HISTORICAL M&A VOLUME AND VALUE

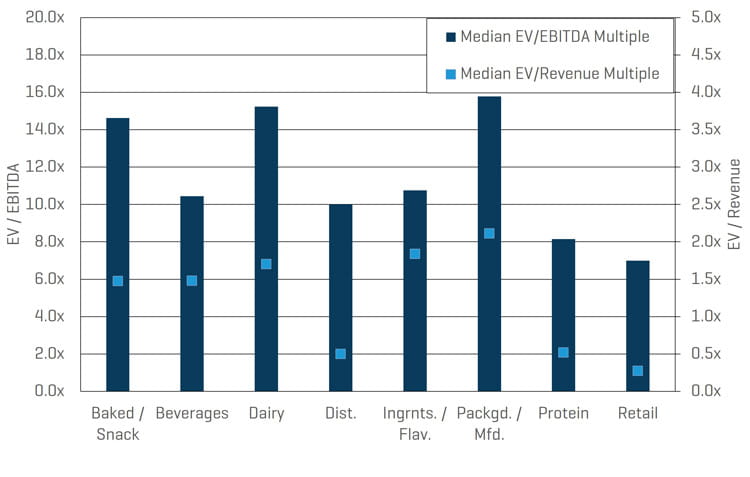

VALUATION BY CATEGORY

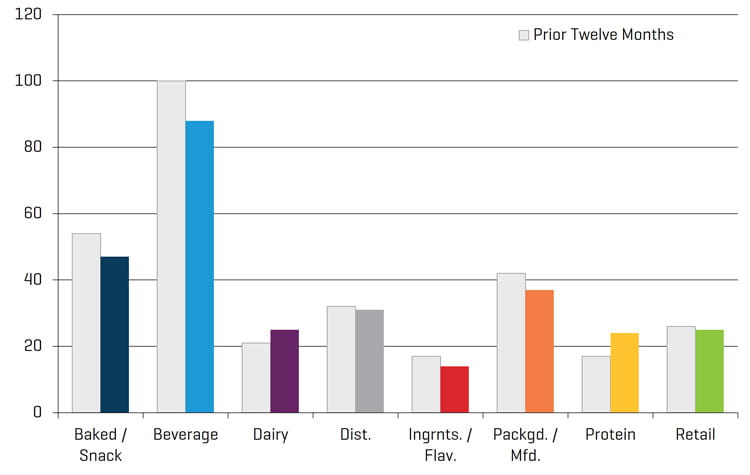

TTM VOLUME BY CATEGORY

TRANSACTIONS COMPLETED OVER PAST 12 MONTHS, BY BUYER TYPE

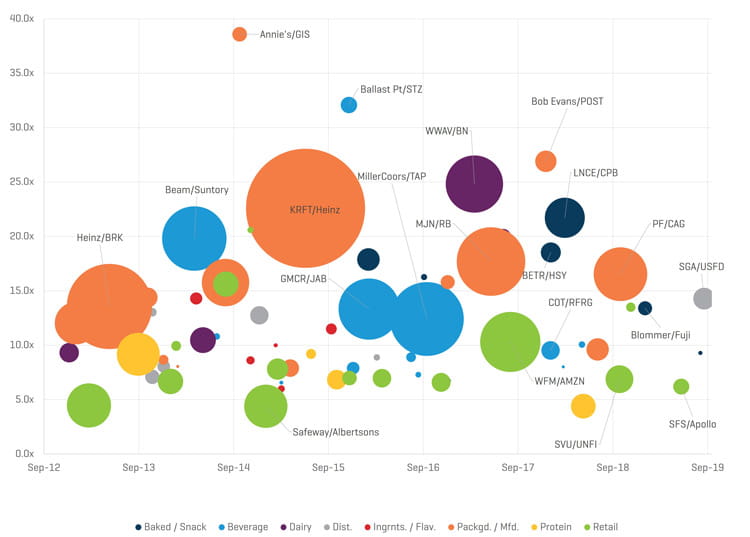

Overview of Recent Transactions; Valuation by Size

Across all sectors of the economy, we estimate that transaction valuations are materially higher than just a few years ago and F&B is no exception. A linear regression of our proprietary data set indicates that multiples for F&B is between two to four multiples of EBITDA higher than the long run average. Valuations at these levels are unprecedented – and as many industry veterans would say, unsustainable.

Recent deals of note include:- Distribution: SGA’s Food Group of Companies acquired by US Foods (USFD) for $1.8 billion or 14.3x EBITDA in September 2019

- Retail: Smart & Final Stores (SFS) acquired by Apollo Management (CPB) for $1.0 billion or 6.2x EBITDA in June 2019

- Baked / Snack: Blommer Chocolate Company acquired by Japanese ingredient company Fuji Oil Holding for $750 million or 13.4x EBITDA in January 2019

- Packaged / Manufactured: Pinnacle Foods (PF) acquired by Conagra (CAG) for $10.9 billion or 15.8x EBITDA in October 2018

Overall, larger deals still command size premiums, though even at the lower end of the market (i.e. transactions below $250 million) multiples have recently averaged 9.3x EBITDA.

SELECT TRANSACTION EBITDA MULTIPLES

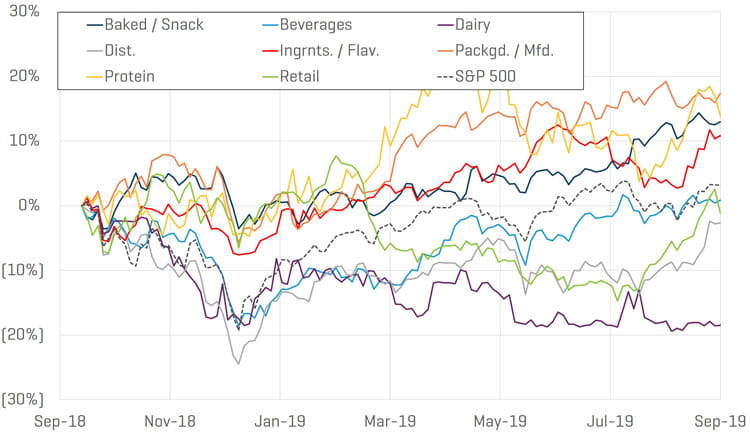

Public Traded Comparables: Packaged / Manufactured & Protein Up, Dairy Down

The past twelve months have been a mixed bag for large, publicly traded F&B company stock prices. Protein – coming off a few tumultuous quarters – outperformed all but one other category while the Dairy sector continued its woes. Other winners included Packaged / Manufactured (the best performing category), Ingredients / Flavorings, and Baked / Snack. Retail and Distribution largely erased the losses seen in the second quarter of 2019. Only Dairy severely underperformed the F&B universe as well as the broader stock market.

RELATIVE SHARE PRICE PERFORMANCE

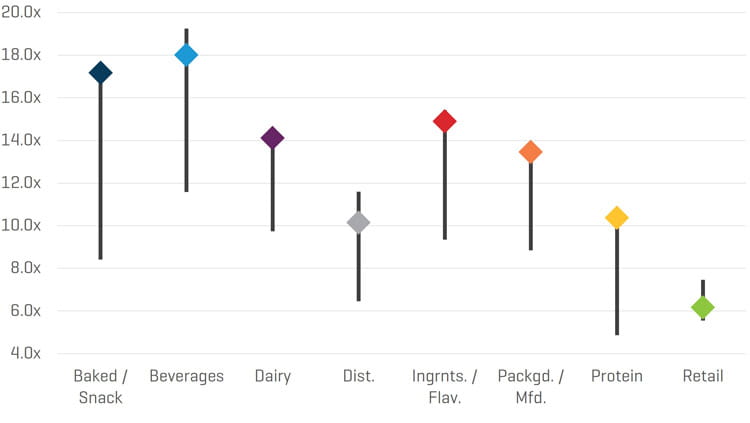

Every sub-sector except Retail is currently trading at or near recent highs; furthermore all sub-sectors except Retail are currently trading above 10x TEV / forward EBITDA, with Beverages and Baked / Snack commanding the highest valuations in the public markets.

CURRENT FORWARD EBITDA MULTIPLES VS. 10-YEAR HISTORICAL RANGE

Source for charts: S&P Capital IQ and Stout research.