Français

Français

You’ve probably heard the stories—your neighbor or a friend of a friend believes they have the next great idea, perhaps the next Facebook. Ideas can come from anywhere: a part-time hobby in someone’s garage, heated planning sessions over the kitchen table, or at the local university’s funded incubator. However, ask any venture capitalist and he or she will tell you: Ideas and people willing to work hard are easy to come by. However, the process of maturing an idea, no matter how brilliant, into a successful business is exceedingly complex, challenging, fraught with risk, and expensive.

A study by Harvard researcher Shikar Ghosh suggests that 75% of startups fail.1 This statistic raises the question of what attributes separate the 25% of successful startups2 from their less successful counterparts? Very often, the difference between expansion and extinction for a startup is its ability to raise additional capital. It is not uncommon for technology startups to have little or no revenue, large research and development expenses, and few tangible assets. For high-tech companies especially, the companies’ primary and most valuable assets are their ideas and the IP that protects their ideas—patents, trade secrets, trademarks, or copyrights.

The big question for many IP-centric startups is, “How does a new business venture attract money to meaningfully commercialize or monetize its ideas?”

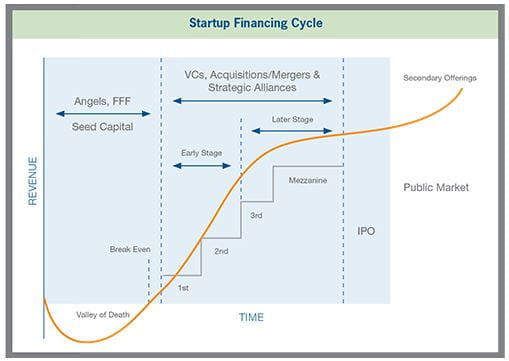

Startup Financing Cycle

As discussed in more detail within this article, quality IP assets act as a signal to potential investors that a company is more likely than its less IP-rich competing startups to have a sustainable competitive advantage that will allow it to succeed in the marketplace.

Investment funding can be categorized by stages based on certain business and operational characteristics. In general, the higher the perceived risk of a company, the more it will have to pay to attract capital. Consistent with this principle, the cost of financing for a startup business is reduced as it expands and successfully matures over time. A classic startup life cycle is represented in the following figure showing various sources of financing in relation to a hypothetical startup’s revenues.3

In the initial startup period, the Seed Capital Stage, the startup company begins with an idea and tries to establish its proof-of-concept. This stage is also referred to as the “valley of death” because the business is characterized by negative cash flows as significant monies are spent on research and development, building prototypes, and assessing the technology’s economic and commercial viability in the absence of significant revenues. Finding financing during this phase is difficult because there is a high risk that the enterprise might fail, and few investors are willing to take that risk. Seed capital often comes from the entrepreneur, friends, family, and professional contacts.

The next phase of the startup life cycle is the Early Stage, where the company has successfully demonstrated its proof-of-concept. In this chapter of a company’s development, its products are being commercially launched for the first time—preliminary operations have commenced, production initiated, and some sales have been generated. The Early Stage can be segmented into First-Stage and Second-Stage financing rounds. First-Stage financing involves funding for ramping up of production and sales. Revenues are positive, but the company may not yet be generating profits. As the venture experiences some initial success, Second-Stage financing provides capital for the necessary expansion of the business.

In the Later Stage, capital is required for companies that are profitable, but in need of further financial support. Growth-related activities that typically require funding include operations expansion, marketing, new technology development, a product line expansion, and geographic market expansion.

One source for expansion in the Later Stage is mezzanine financing, which has the characteristics of both debt and equity. Mezzanine financing is generally the layer of debt that sits between senior debt and equity and may also incorporate equity instruments such as warrants. It can increase the capital base of a company without significantly diluting shareholders’ control.

Growth capital for the expansion of Early and Late Stage companies may be obtained through organic growth resulting from financially successful operations or growth through acquisition or strategic alliance. Venture capitalists can also provide financing for organic growth and acquisition/takeover bids.

Importance of IP Assets in Securing Financing

A strong IP portfolio often plays a key role in business formation and financing.

The importance of IP to venture financing is supported by a World Intellectual Property Organization (“WIPO”) white paper, which suggests that IP is the basis for a significant portion of venture capital investments.4 For technology-based companies, IP is the essential element in obtaining venture funding. Venture capitalists look to maximize returns and look to determine whether the company, through its proprietary inventions and innovations, offers an advantage over competitors and, of equal importance, whether that advantage over competitors is sustainable. The WIPO white paper states that, “[w]ithout the strength of the intellectual property and its protection, little if any investments would be made into new or growing enterprises.”

A paper by Professors David Hsu and Rosemarie Ziedonis examines the degree to which patents enable entrepreneurs to acquire financial capital across the new venture life cycle.5 The authors conclude that having larger portfolios of patent applications increases the likelihood that entrepreneurs will attract initial financing from a venture capitalist. Specifically, they found that a doubling in the patent application portfolio of a new venture is associated with a 24% increase in valuation, representing an upward funding-round adjustment of approximately $12 million for the average startup in their sample.

Since the quality of early-stage enterprises often cannot be observed directly, determining the commercial promise and value of nascent technologies can be difficult, particularly for those outside the company like potential lenders, investors, or customers. It is the belief of Professors Hsu and Ziedonis that patents act as signals of business quality that positively affect investors’ perceptions.

This concept is echoed in a paper by Mark Lemley, which suggests that companies, especially startups, obtain patents as a financing tool. The paper goes on to state that venture capitalists use patents as “evidence that the company is well managed, is at a certain stage in development, and has defined and carved out a market niche.”6

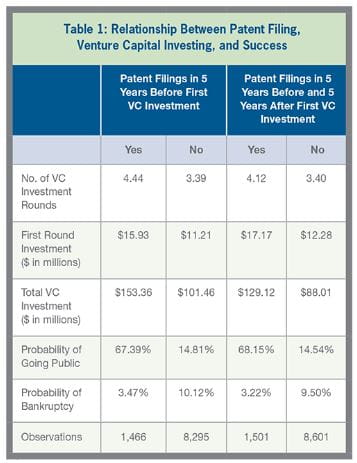

The positive effects of IP assets in generating financing are not limited solely to the beginning of an enterprise’s life cycle. There is evidence, as summarized in the table below, that companies with strong IP assets have increased likelihood of success by way of:7

- Higher number of venture capital financing rounds

- Greater investment funding

- Lower probability of bankruptcy

- Higher probability of successful exit through initial public offering

Types of Financing

Startup businesses seeking capital essentially have two options: debt or equity financing.

Equity financing is the capital source generally employed by a business that has high growth prospects with high investment risk. This may be a good option for Early Stage companies with limited revenues and prospects for negative operating income in the near term.

Startups seeking debt financing typically will be required to pledge their most valuable assets, namely their IP, as collateral. Lenders that focus on startups and emerging companies likely will insist on obtaining a security interest in the IP assets to secure the loan.

Unfortunately, IP-backed securitization is simply not available to most startups. Securitization involves the pooling of financial assets and issuance of new securities backed by those assets. Assets that can be monetized in this way are those that have reasonably predictable cash flows, such as future royalty payments from patent or trademark licensing. One of the most famous IP securitizations was the “Bowie bond” launched in 1997, which was backed by David Bowie’s song catalog and raised $55 million.

Securitization differs from debt because it is not financing, since the entity securitizing its assets is not borrowing money, but selling a stream of fairly predictable future cash flows. Securitization is generally not a viable option for startup firms, as their IP assets are “untested” and do not yet have a predictable stream of future cash flows.

Valuation Methodologies and Why Valuation Is Important

For most high tech startup businesses, the value of the entire business or enterprise is easy to determine once the value of the IP is determined. This is typically true because the IP constitutes the vast majority of the business value and because the IP is generally the most challenging asset class to value. Consequently, the following sections concentrate on valuing a company’s relevant IP rather than the entire business.

Private investors, whether equity or debt investors, are driven by the goal of maximizing returns while keeping risks as low as possible. Risks associated with a startup’s technology —including its technical viability, uncertainty regarding the size of the achievable markets, the legal viability of the IP protections, and a lack of history for the company or data from comparable companies/technologies to provide a precedent— make the valuation of IP for Early Stage technology firms a very challenging task.

Moving through the startup financing cycle as described earlier, the riskiness of the IP assets typically decreases as each subsequent hurdle is overcome (successful proof-of-concept, manufacturing scale-up, positive revenue, profitability, etc.). This decrease in risk will have a positive impact on valuation of the IP assets and, in turn, have an influence on the ability of enterprise to attract funding.

Not all IP assets are created equal. Uncertainty surrounding IP asset valuation can be seen as a key obstacle to access financing. There is an imperfect market for IP assets and often a disparity between what they can be sold for and what an owner thinks they are worth. The value of IP assets depends on a combination of legal, economic, and technical factors. For this reason, it is critical to obtain an objective valuation of these assets from an appraiser who understands the complex nature of IP assets.

Three approaches are typically considered in measuring IP value. The results derived from these various approaches are evaluated based on their respective merits, on a case-by-case basis, to arrive at a conclusion regarding value. The three primary approaches are defined as follows:

- Market Approach: determines the value of an IP asset by comparing the subject asset to assets that have been transacted in the marketplace between unrelated parties. The degree of reliance on this approach depends, in large part, on an assessment of whether the transactions of potentially comparable assets to those being valued are sufficiently similar to provide an indication of the value of the assets in question. Factors to consider include the nature of the assets transferred, the industry and products involved, the agreement terms, the circumstances of the parties to the agreements, and other elements that may affect the agreed-upon compensation.

IP by its very nature is novel and unique; consequently, market transactions occurring under comparable circumstances rarely exist. Moreover, even if reasonably comparable transacted assets can be identified, the details surrounding the deal may not be publicly available. Identifying transacted comparable IP at a similar stage of development may be challenging for startup firms. This approach may be used if appropriate adjustments are made for differences such as: stage of development, other included IP assets, timing, market applications, and many other potential factors.

- Income Approach: values assets based on the present value of the future income streams expected from the asset under consideration. This approach considers the amount and timing of the expected cash flows that can be attributed to the subject asset and the risk of realization of those cash flows. The risk associated with the realization of the stream of future cash flows may be captured through the use of an appropriate discount rate, probabilities of success within the inputs used to project the cash flows, or a combination of these factors.

For IP owned by startup firms, the use of the Income Approach may be particularly problematic given sensitivity of the model to inputs such as cash flows derived from the IP, which have not yet materialized. However, projected cash flows based on a detailed build-up of revenues with sound assumptions regarding technical viability, customer acceptance, ramp-up, growth rates, and estimated useful life could form a reliable basis for employing the Income Approach.

- Cost Approach: values IP relying on historical development cost or the cost of replacing an asset by purchasing or developing an asset similar in utility. The concept behind this method is that potential buyers would not pay any more for the IP than it would cost them to create or design around an asset of comparable usefulness. The Cost Approach takes into account direct expenditures such as research and development expenditures, prototype costs, engineering labor, and indirect costs, such as legal and consulting fees.

A disadvantage of the Cost Approach is that it fails to reflect the IP’s earnings potential. Economic benefits from IP are not always commensurate with the cost of replacing the asset. If the IP has significant income upside in a growing market, the Cost Approach will likely understate its value. However, in situations where there is limited market and income data available (making the Market and Income Approaches less viable), this method can be useful for valuing a startup’s IP where the costs incurred to develop and create the IP are reasonably available.

When performing the IP valuation, the weight given to each of the approaches varies with the facts and circumstances of each valuation effort and the availability of appropriate data; however, the attempted application of multiple approaches is generally preferred over the reliance on a single methodology.

A well-reasoned and documented credible valuation, performed by an independent party who understands the complexities of intangible assets and is able to employ established valuation techniques, provides an effective vehicle for communicating the value of early stage IP and benefits both the entrepreneur and investors.

Benefits to Entrepreneurs of a High Quality Valuation

- Entrepreneurs, often “idea people,” visionaries, and/or scientists typically lack the requisite financial skills, training, resources, and experience to employ proper valuation techniques to appraise their IP assets. Thus, the entrepreneurs benefit from relying on a valuation report they could not create themselves.

- Entrepreneurs lack the objectivity that a third-party valuation provides. Appraisals performed by experienced, independent professionals provide credibility to the analysis and offer an impartial determination of value. Such credibility and impartiality will likely be quite important to potential financing sources.

- The appraisal process itself involves due diligence around the legal status of the IP, the technical advantages/disadvantages of the invention(s) in comparison to prior art, and the business potential of the assets, among others. Thus, the appraisal process itself often provides valuable insights to entrepreneurs regarding ways to strengthen their IP positions and protections as well as to generally improve their technologies and business. A well-performed appraisal will help articulate to readers of the appraisal report the potential benefits of the technology as well as the strengths and weaknesses of the underlying business plan. The appraisal can be an important supplement to a business plan.

- If IP assets are to be used as collateral to obtain financing, the assets stand a greater chance of being accepted as collateral if a startup is able to demonstrate its expected liquidity, for instance, by being readily transferable between businesses. Less commonly, the appraisal may identify other licensing opportunities outside the core business, which increases the cash flows and liquidity of the IP.

Benefits to Investors of a High Quality Valuation

- A well-written appraisal report can serve to identify new and valuable investment opportunities that might have gone unnoticed without the valuation.

- Provides a third-party perspective of the value of the investment and, equally important, on the likely value drivers associated with the investment.

- Provides a “head start” to legal, technical, and business due diligence. Valuation firms with specialized IP valuation practices have access to data sources not generally available to any but the largest and most sophisticated venture capital firms. Therefore, the valuation may provide relevant information of which the potential investor otherwise might not have been aware.

- IP value continually changes with the passage of time and with evolving perceptions of likely risks and projected benefits. Valuations at different points in time in a startup’s life cycle allow investors to make informed decisions regarding whether and when to invest. For example, a valuation conducted after the achievement of a key milestone would communicate the reduction in uncertainty and the new value of the investment.

- The valuation may identify non-core uses of the IP, which could represent additional revenue streams outside of the owning company’s core business. If the IP is being infringed, the net value associated with potential infringement actions can also be estimated.

- Allows investors to quantify the contribution that IP assets make to company value. This enables an informed view to be taken on the return on investment offered by these assets.

Conclusion

Credible IP assets strengthen a startup’s likelihood of obtaining financing from investors and lenders because of the sustainable competitive advantage; i.e., higher expected returns, strong IP assets confer.

Further, IP valuations performed by a competent valuation analyst, knowledgeable in the unique characteristics of IP assets, provide numerous advantages to both entrepreneurs and investors, including reduction of information asymmetries in markets for entrepreneurial financing.