English

English

After an unprecedented first half experienced in 2020, industrial services business activity, share price performance and M&A rebounded strongly in the second half of the year. Equity values rebounded near or to their pre-COVID highs by December. With the Federal Reserve lowering rates, thus slashing the cost of debt capital, and the new administration proposing massive expenditures with a focus on infrastructure for 2021 and beyond, we are projecting a very strong run looking outward for industrial services businesses, from new construction through service/repair/maintenance and upgrade/modification projects.

Key Takeaways

- Industrial Services both outperformed during covid and rebounded strongly from the depths of the pandemic

- Strong rebound in equity values and M&A activity in the second half of 2020 a sign of confidence in the sector and certain end markets served

- Infrastructure bill, significant federal government spending, and support for state budgets will be a key driver in 2021 and coming years, spurring robust activity

Industry Statistics

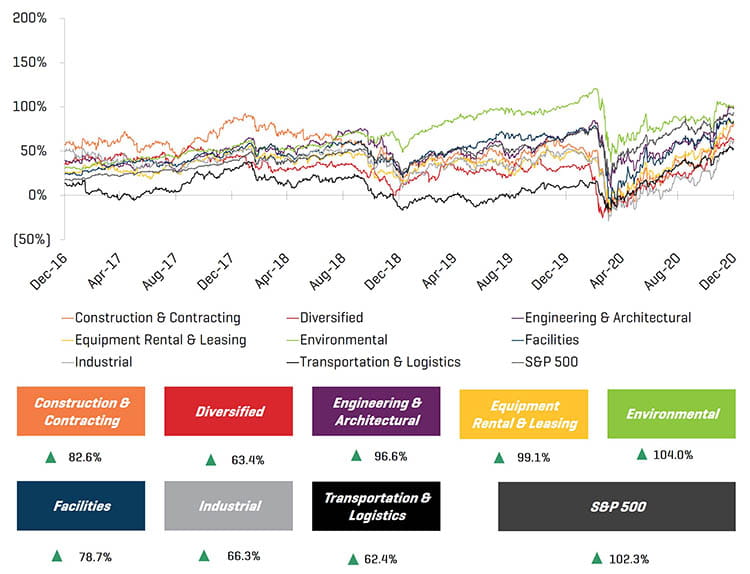

5-Year Historical Price Performance

Operating and Market Performance

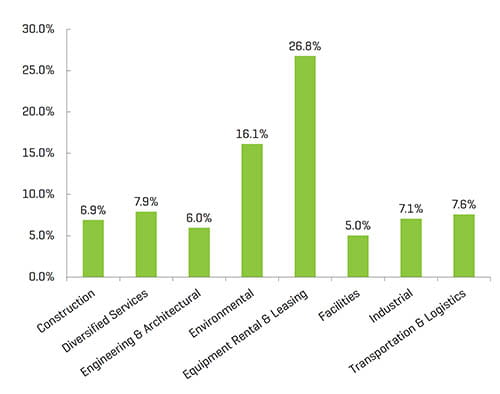

LTM EBITDA Margin

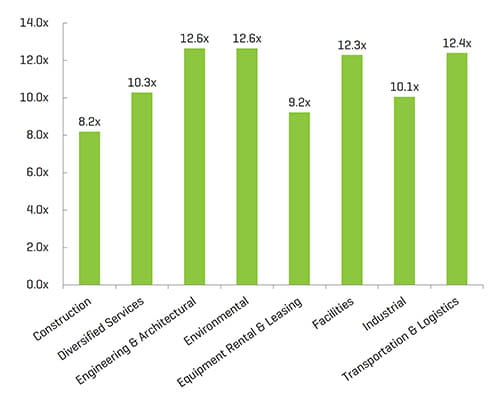

Enterprise Value / LTM EBITDA1,2

(1) Multiples above 20x are excluded from the mean/median calculation

(2) Median from public comp sets featured in report

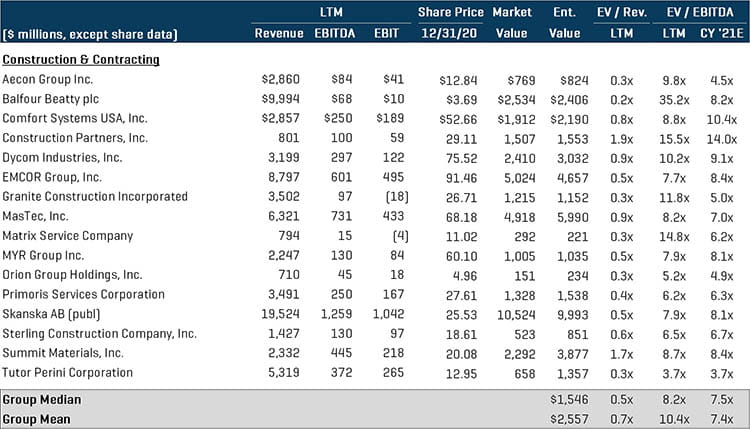

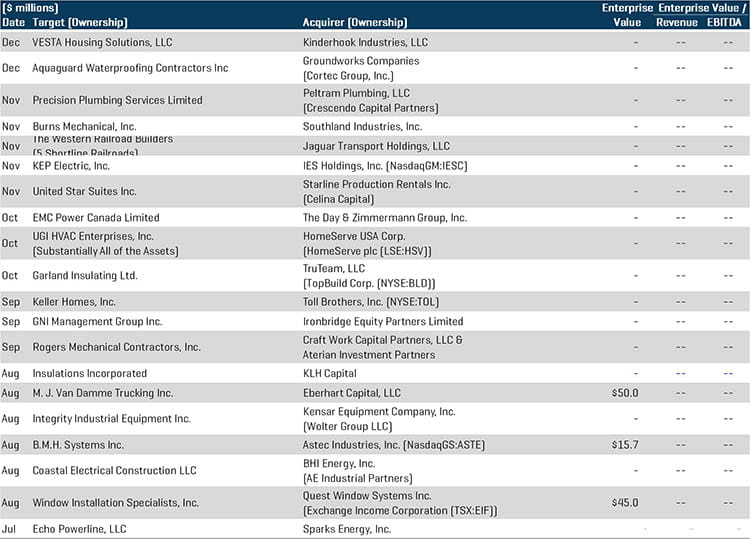

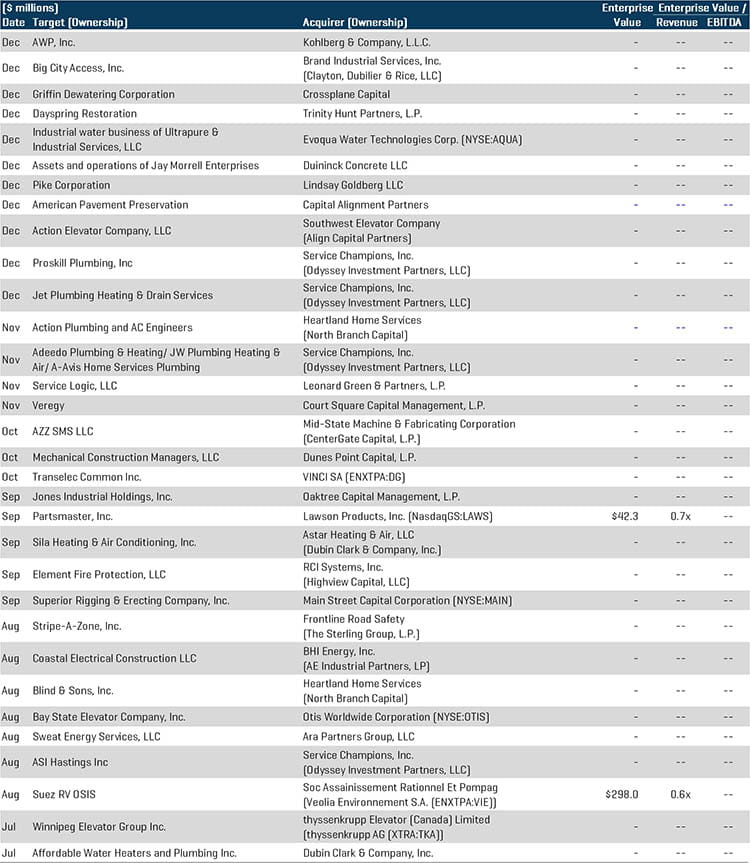

Construction and Contracting Services

The construction and contracting services segment continued to be one of the more active segments in terms of M&A activity as evidenced by continued industry consolidation by both strategic and hybrid buyers. However, industry performance during the remainder of 2020 has been mixed, given the "long tail" nature of certain projects. Companies were more exposed to COVID-19-affected segments (like retail and hospitality). Despite strong order books, companies are experiencing challenges such as project delays and cancellations, as well as difficulty obtaining permits. Many operations were given the “essential” nod from state governments to resume work as the country continued to reopen through the end of 2020. Notable transactions include:

- Craft Work Capital Partners, LLC, a joint venture between Craft Work Capital, LLC and Aterian Investment Partners, acquired Rogers Mechanical Contractors, Inc., a leading national provider of mechanical, HVAC and plumbing contracting services, specializing in mission-critical, time-sensitive and complex projects. A third-generation family-owned business, Rogers has strategically evolved into the only mechanical contractor of scale focusing on the distribution center market and will benefit from the new strategic partnership with Craft Work.

- IES Holdings, Inc., a holding company that owns operating subsidiaries that provide electrical contracting and other infrastructure services, acquired K.E.P. Electric, Inc., a Batavia, OH-based electrical contractor specializing in the design and installation of electrical systems for single-family housing and multi-family developments. The acquisition of KEP continues IES Holdings’ strategy to partner with proven management teams and expand into attractive growth markets.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

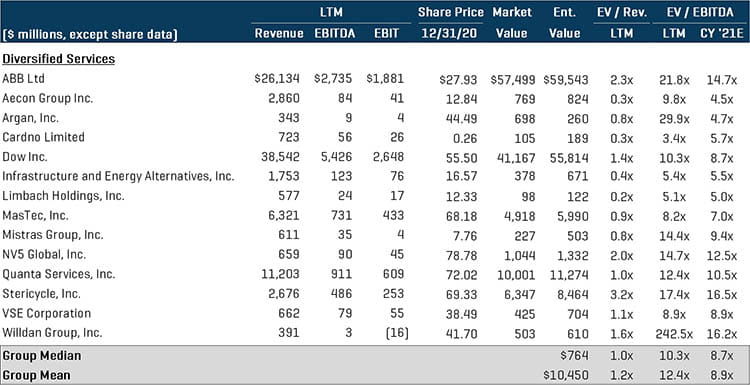

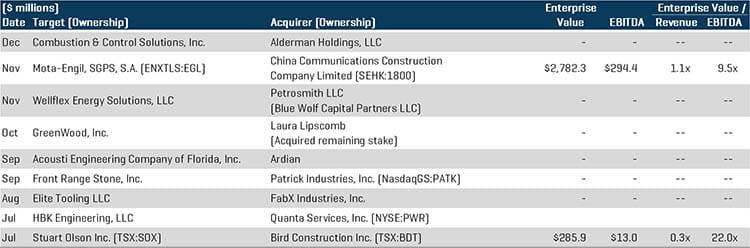

Diversified Services

The diversified services segment saw an overall increase in transaction volume in the second half, which was greatly attributed to rebound from the pandemic and the economic stabilization. The industry saw a mixture of large strategic acquisition activity as industry players continue to pursue complimentary service offerings and capabilities, as well as private equity buyers diversifying industrials-oriented portfolios. Notable transactions include:

- HBK Engineering, LLC, a fully licensed, professional engineering design firm, has been acquired by Quanta Services, Inc. (NYSE:PWR), a leading specialized contracting services company, delivering comprehensive infrastructure solutions for the utility, pipeline, energy and communications industries. This acquisition meaningfully enhances Quanta's turnkey engineering capabilities in its core utility markets and particularly strengthens its communications engineering capabilities.

- Stuart Olson Inc. (TSX:SOX), a provider of construction services including vertical infrastructure and electrical building systems, has been acquired for $286.0 million by Bird Construction Inc. (TSX:BDT), a leading Canadian construction company operating from coast-to-coast and servicing all of Canada’s major markets. The combination of both businesses will create a company with substantially increased breadth and scale, diversified across services, end-markets, and geographies. Operating synergies are expected to generate accretion in operating cash flows and Adjusted Earnings Per Share in the first full-year, further positioning the company to deliver sustainable value and continuing dividends to shareholders.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

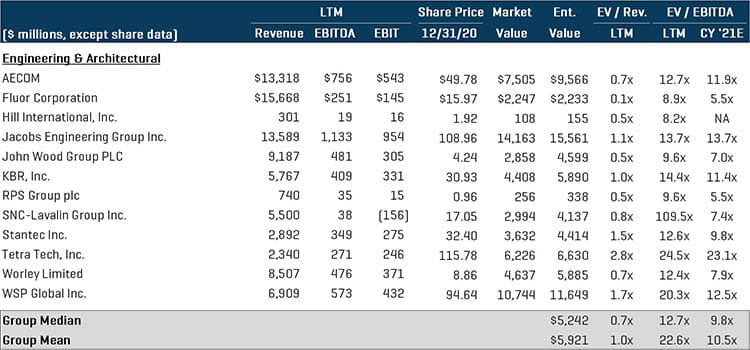

Engineering and Architectural Services

While the segment saw lower LTM EBITDA margins at year-end, average market capitalizations rebounded from March lows. Private equity buyers were active in the second half of 2020 executing platform and add-on acquisitions, in addition to exiting current investments. Notable transactions include [For more details see Stout's Engineering and Construction 2020 Year in Review Report]:

- The LiRo Group, a provider of construction management, engineering, and architectural services, has been acquired by Global Infrastructure Solutions Inc., a construction investment firm. GISI will provide LiRo with resources to fuel growth as well as industry expertise to assist in strategic planning and client relationships. LiRo represents the initial building block in GISI’s new Global Engineering and Consulting Platform, and complements their current service offering within their construction services division.

- TAM Consultants, Inc., a professional services firm for structural engineering, building enclosure consulting, and a variety of building testing services, has been acquired by Terracon Consultants, Inc. Terracon provides engineering services from more than 150 offices with services available in all 50 states. Terracon’s investment will expand the company’s position throughout Virginia and the mid-Atlantic region and further drive the Company’s focus towards extending the service life and efficiency of existing buildings in the U.S.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

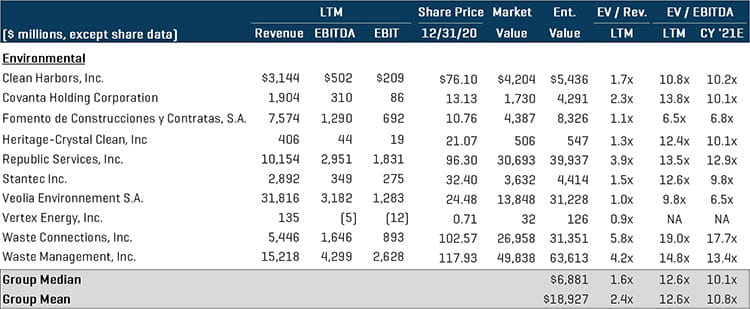

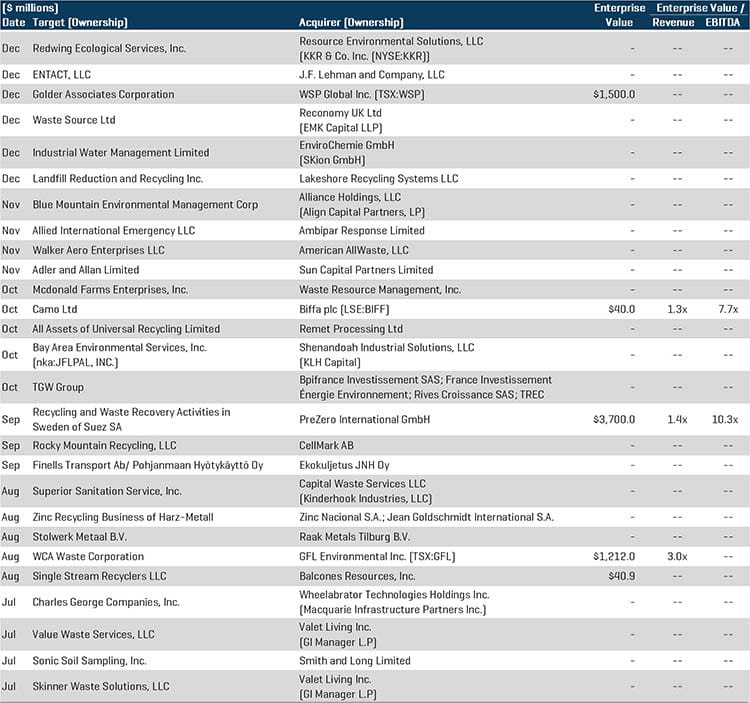

Environmental Services

The environmental services segment finished the second half trading at the highest overall multiple among its industrial services peers. The segment’s overall success during 2020 has been driven by the demand for environmental services, which remained sheltered from the negative effects of the pandemic. The segment is poised for further growth stemming from the overwhelming societal focus on highly sustainable and health-conscious environmental practices, and regulatory tailwinds focused on health, safety, and sustainability. Despite the uncertain economic period, both private equity and strategic buyers remained active in terms of M&A and executed several industry-changing transactions. Notable transactions include:

- PreZero International GmbH , the environmental division of Germany-based Schwarz Group, acquired Suez SA (ENXTPA:SEV)‘s Recycling and Recovery operations in the Netherlands, Luxembourg, Germany, and Poland. For Suez, the transaction represents another major step in the delivery of its asset rotation strategic plan, which aims at positioning the company as a global, agile, innovative, and highly technological leader in environmental services. The combination of both companies' know-how creates synergies and a foundation for further growth for PreZero. By enhancing the service portfolio and location coverage, the Company will create sustainable added value for its customers.

- GFL Environmental Inc.(TSX:GFL), a diversified environmental services company in North America, acquired WCA Waste Corporation for approximately $1.2 billion. WCA operates a vertically-integrated network of solid waste assets, including 37 collection and hauling operations, 27 transfer stations, three material recovery facilities and 22 landfills supported by over 1,000 collection vehicles, across 11 U.S. states. The acquisition provides GFL with attractive opportunities to expand their geographic footprint and further diversify their service offering throughout North America.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

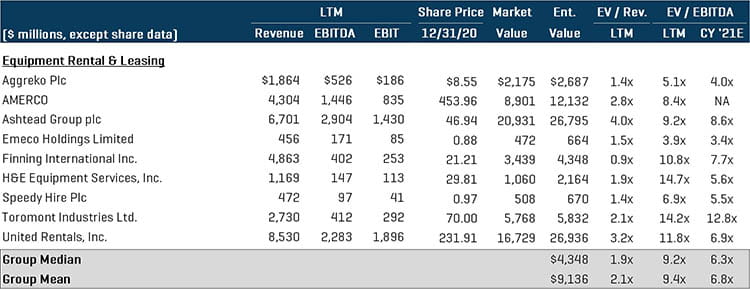

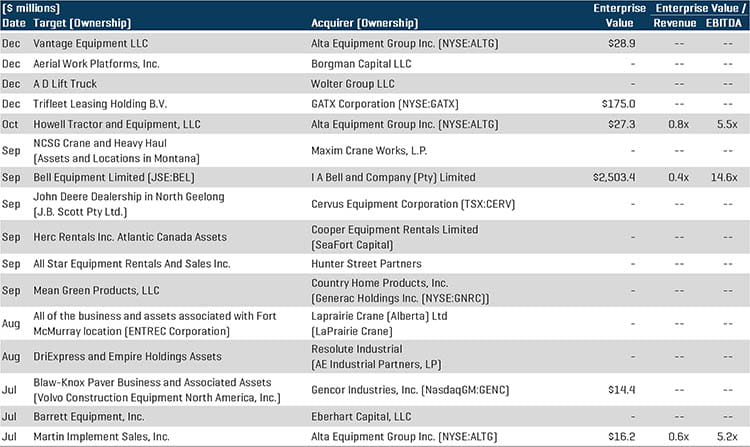

Equipment Rental and Leasing

The equipment rental and leasing segment continued to benefit from industry consolidation amongst large strategic serial acquirers pursuing roll-up acquisitions to expand geographic footprint, fleet size, and service capabilities. Private equity firms were also active in this segment. As more construction projects come back online and are developed through the pipeline, activity within the equipment rental & leasing segment is expected to increase in 2021. Notable transactions include:

- GATX Corp. (NYSE:GATX), a provider of global railcar leasing services, acquired Trifleet Leasing Holding B.V., the fourth largest global tank container lessor. The transaction, valued at about $175.0 million, complements GATX’s existing railcar leasing business and shares the company culture of striving for the highest levels of safety, quality, customer service and environmentally responsible performance.

- Bell Equipment Ltd. (JSE:BEL) has been acquired by I A Bell and Company (Pty) Ltd. for approximately $2.5 billion. Bell Equipment, founded in 1954, manufactures and distributes materials handling equipment primarily for agriculture, forestry, waste-handling, and construction industries. I A Bell’s acquisition of Bell Equipment aligns with the company’s growth strategy and further equips the company to expand its offering of general engineering services globally.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

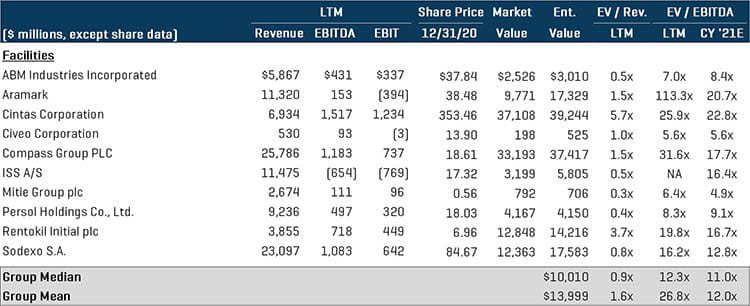

Facilities Services

Several roll-up strategies amongst interested buyers were seen in this space in the second half, as the health and safety procedures of commercial buildings remains paramount as the population slowly returns from the work-from-home environment. The industry continued to witness consolidation as buyers pursued multiple acquisition targets to further build out existing platforms. Notable transactions include:

- Serco Group Pty Limited has announced it has entered into a sale and purchase agreement to acquire Facilities First Australia Pty Ltd., a cleaning, maintenance, and facility services management company, for approximately $76.5 million. The transaction is still in process and is expected to close in the second quarter of 2021. Upon completion, the combination of Serco and Facilities First will enable Serco Australia to target a significant pipeline of new opportunities and further expand the Company’s reach in Australia.

- Pride & Service Elevator, Inc., a provider of elevator maintenance, repair, and related services, has been acquired by Arcline Investment Management, a private equity firm specializing in control investments in middle-market buyouts. The Pride & Service Elevator acquisition marks another in a string of acquisitions by Arcline in the sector in 2020. Back in May and August respectively, the firm acquired Unitec Elevator and Jersey Elevator.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

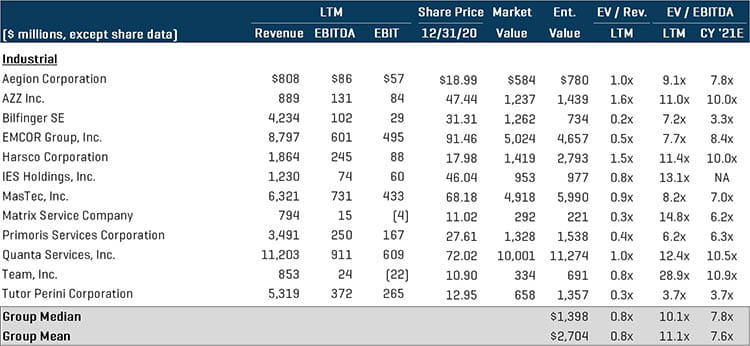

Industrial Services

While the performance for many public firms in the Industrial Services segments was negatively impacted during the first half of 2020, most firms finished the year on a positive note with increasing margins and market caps. The last two months of the year saw very strong M&A activity, with both strategics and private equity firms spending aggressively. Notable transactions include:

- BrandSafway, a provider of specialized construction services for the industrial, commercial, and infrastructure end markets, has acquired Big City Access, a portfolio company of Rock Hill Capital Group. Big City Access, established in 2002 and headquartered in Houston, is a premier provider of scaffolding and other access solutions in the Texas commercial construction market. For BrandSafway, the acquisition of Big City is the latest step in its major investment and acquisitions process which is yielding rapid growth and global expansion, with names such as Dutch steel-coating specialist Venko already part of BrandSafway’s growing portfolio of businesses.

- Pike Corp., one of the largest providers of infrastructure solutions to utilities in the United States, was acquired by Lindsay Goldberg, a leading private investment firm focused on partnering with families, founders and management teams. The acquisition provides Pike access to substantial resources to further accelerate the company’s significant growth and strategic initiatives.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

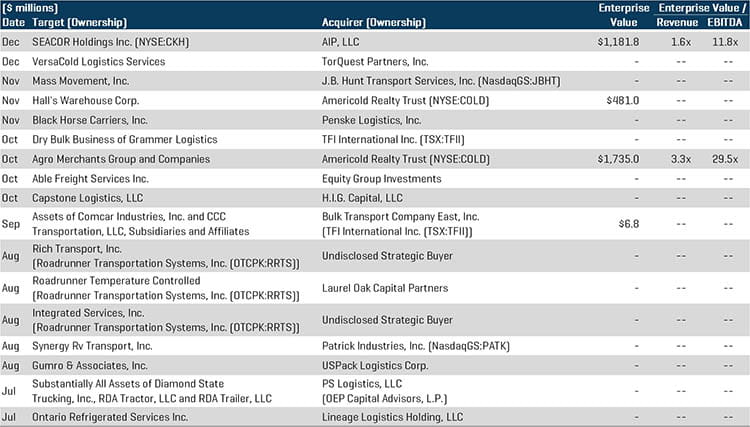

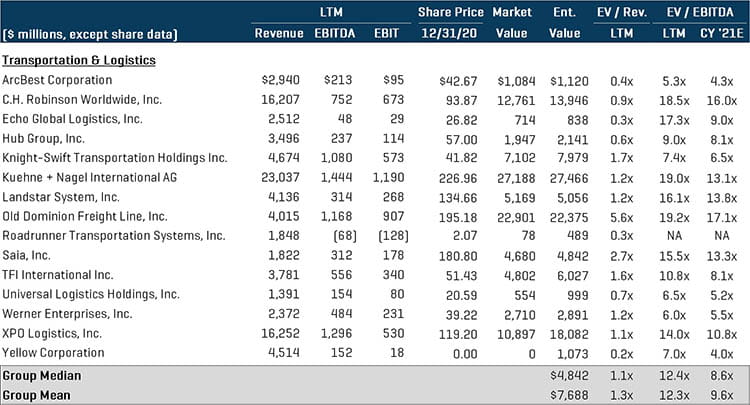

Transportation and Logistics

Both strategic and private equity buyers made several notable transactions in the second half, as targets are looking to capitalize on strong industry tailwinds and execute growth initiatives. The pandemic driven shift from traditional brick-and-mortar marketplace to online platforms contributed to the increase in activity in this space. Quality transportation and logistics assets were in demand as the pandemic fueled recession pushed the economy to heavily rely on the transportation and logistics industry to facilitate the recovery. Notable transaction include:

- SEACOR Holdings Inc., a provider of integrated logistics and barge transportation services, was acquired for approximately $1.2 billion by AIP, LLC, a New York-based private equity firm that focuses on buying, improving and growing industrial businesses. The transaction complements SEACOR’s unique, diversified platform while leveraging AIP’s investment and operational expertise in pursuing industry consolidation and other growth opportunities.

- Americold Realty Trust (NYSE:COLD), a cold storage warehouse owner and operator, acquired the world’s fourth-largest temperature-controlled operator, Agro Merchants Group, for $1.7 billion. The transaction follows several others over the last two years as the Atlanta-based real estate investment trust continues to expand its network through acquisition. The merger represents a unique opportunity for Americold to acquire an institutional-quality global portfolio, facilitates strategic entry into Europe, and adds complementary locations in the U.S., South America, and Australia.

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transaction