English

English

With all the changes in recent years as a result of tax reform and anticipated changes on the horizon as a result of the upcoming election or as stipulated in recent tax law, the trend of companies converting to an S corporation may see a shift. Historically, the avoidance of “double taxation” and high corporate tax rates have driven many companies to convert to S corporations to take advantage of certain tax attributes impacting their shareholders. We are in a unique period where the advantages of being an S corporation relative to a C corporation may not be so clear anymore.

Overview of S Corporations

Valuations that involve a subject company classified as an S corporation (or S subchapter) often bring unique considerations that are different than valuations of businesses classified as C corporations. An S corporation refers to a type of corporation that meets certain thresholds or requirements as provided by the Internal Revenue Code (IRC § 1361). Historically, one of the primary benefits in electing to be an S corporation is being categorized as a “pass-through” entity where the company elects to pass its tax obligations directly to its shareholders for federal tax purposes.

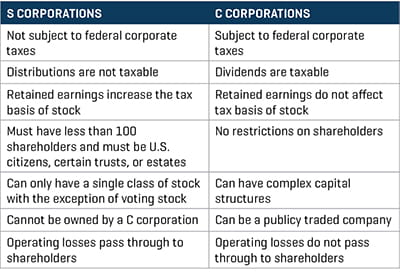

Shareholders of an S corporation are taxed individually on the company’s income by reporting their pro-rata portion of the company’s taxable income on their own personal tax returns; therefore, they pay taxes using their individual income tax rate. Any distributions that are made by the S corporation to its shareholders, however, are not subject to income taxes. This differs from a C corporation, where the company itself pays taxes on its taxable income at the entity level, and any dividends paid to shareholders are also subject to dividend income taxes at the shareholder level. This avoidance of a double taxation on corporate earnings is one of the key economic benefits to being an S corporation. Further, any net income that is not distributed to shareholders and is classified as retained earnings does not affect the shareholder’s tax basis of the stock in a C corporation; conversely, undistributed net income that is passed through to the shareholder does increase the tax basis of the shareholder’s stock in an S corporation. Additional key differences are presented in Figure 1.

Figure 1. S Corporations vs. C Corporations

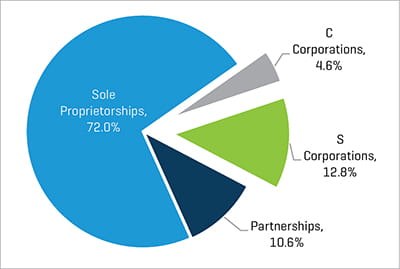

Figure 2. Number of Returns by Business Form

Tax Year 2015

The Internal Revenue Service (IRS) provides statistical information relating to the number and different types of tax forms they receive. Specifically, the latest information available as of February 2020 provides information by business form for the 2015 tax year, which is summarized in Figure 2. The IRS received a total of approximately 35 million business returns for 2015. The majority of returns (72.0%) were for sole proprietorship businesses. While the total amount of net income reported by C corporations far exceeds the total for S corporations (approximately $1.6 trillion versus approximately $560 billion, respectively), the approximately 4.5 million S corporation returns is greater than the number of C corporation returns of only 1.6 million. A large driver behind this disparity is likely the qualitative differences discussed above, resulting in the larger, publicly traded corporations being classified as C corporations. However, with that in mind, the sheer number of S corporations that report in the United States suggests that the economic benefit of being formed as, or later converted into, an S corporation (as discussed in more detail later) has historically been considered advantageous to shareholders.

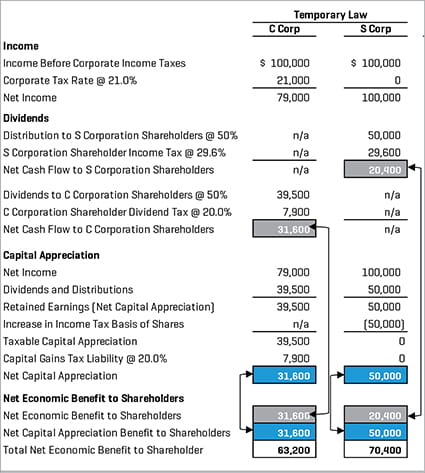

Figure 3. Net Economic Benefit Differential

There are a multitude of factors to consider in determining the economic efficacy of a C to S conversion. Management of C corporations contemplate the pros and cons associated with converting from both a qualitative and quantitative perspective. Specific factors that entice C corporations to convert include, but are not limited to:

Avoidance of Double Taxation

As described above, one of the primary benefits of converting to an S corporation is the avoidance of double taxation on corporate earnings. An example of the net economic benefit associated with C corporations versus S corporations is illustrated in Figure 3.

- C corporations are subject to corporate income taxes at the entity level. Conversely, S corporations are not subject to corporate income taxes at the entity level.[2] S corporation shareholders recognize their pro-rata share of the net income of the company on their personal income tax returns and pay taxes at individual income tax rates.

- Dividends paid by C corporations to their shareholders are subject to dividend income taxes at the shareholder level. Conversely, distributions (i.e., dividends) paid by S corporations to their shareholders are not subject to income taxes.[3]

- The undistributed net income of a C corporation does not affect the tax basis of its equity securities. Conversely, the undistributed net income of an S corporation increases the tax basis of its equity securities.

Avoidance of Built-in Gains Tax on Appreciated Assets

Pursuant to IRC § 1374(d)(7), if a company’s shareholders elect to convert to an S corporation and the company waits five years (i.e., the recognition period) to sell its appreciated assets carried over from its C corporation status, it can avoid the double taxation of corporate rates imposed on the gain and instead utilize capital rates passed through to the shareholder level.

C corporation management may engage a valuation firm (or other qualified advisor), such as Stout, to advise on the disparate characteristics of C and S corporations and the potential economic impact of conversion.

Converting from a C Corporation to an S Corporation

Congress enacted the Tax Reform Act of 1986, which instituted a corporate-level tax on certain built-in gains of S corporations pursuant to IRC § 1374. Section 1374 was enacted to prevent taxpayers from avoiding the corporate-level tax associated with appreciated assets by converting to an S corporation. As such, a C corporation must provide the fair market value of its assets[4] on its tax return, which is performed on a control basis on the last day the business existed as a C corporation, in order to establish a tax basis from which subsequent gains can be measured. To the extent that the business or its appreciated assets are sold after conversion but during the recognition period of five years, the company may be subject to a corporate-level built-in gains tax on the appreciated assets, in addition to the tax imposed on its shareholders. Built-in gains recognized during the period are taxed at the highest rate applicable to corporations.

An entity that wishes to make an S corporation election can do so by obtaining Form 2553 (IRC § 1362(a)) from the IRS website, which must be signed and consented to by all shareholders. This form must be filed within 2.5 months after the beginning of the tax year in which the S corporation election is to take effect, or the year preceding the year in which the election is to take effect.

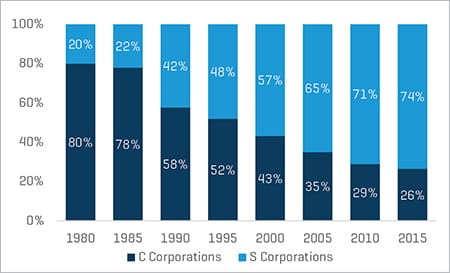

Based on empirical data from the Statistics of Income Division at the IRS, the proportion of companies filing C corporation tax returns versus S corporation tax returns has shifted dramatically since the 1980s. As illustrated in Figure 4, there were approximately four times as many businesses structured as C corporations compared to S corporations in 1980 (2,163,458 C corporations versus 545,389 S corporations). Over time, however, that relationship flipped such that there were approximately three times as many businesses structured as S corporations compared to C corporations in 2015 (4,487,336 S corporations versus 1,611,236 C corporations). This trend appears to support the notion that the economic benefits associated with electing S corporation status are enough to entice more entities to either be formed as, or later converted into, an S corporation. With the advent of the Tax Cuts and Jobs Act of 2017 (TCJA), it is yet to be seen whether this trend will continue; however, it is safe to say that businesses will reevaluate their S corporation status to determine which structure is more economically advantageous going forward.

Figure 4. Historical Tax Returns by Business Form (C and S Corp)

TCJA and Recent Trends

On December 22, 2017, the TCJA, which represented the largest reform to the tax code since the Reagan administration, was signed into law. The resulting changes were substantive to businesses and individuals, and it reflected both temporary and permanent changes. One of the significant permanent changes to the tax code was the reduction in the corporate income tax rate from 35% to 21%. While this corporate tax rate does not directly impact S corporations, it does alter the economics related to the benefits of S corporations and its corresponding shareholders relative to C corporations. The TCJA also specified certain temporary changes that are set to sunset at the end of 2025 before returning to the tax rates prior to the TCJA. Specific temporary changes were 1) a reduction in the top marginal individual income tax rate from 39.6% to 37.0%, 2) limited state and local tax deductions for federal tax purposes for S corporations only, and 3) the potential for shareholders to deduct up to 20% of their pro rata share of the company’s qualified business income (QBI) if the business qualifies. Further research is imperative in understanding whether or not a shareholder qualifies for the QBI deduction; however, at a high level, shareholders of companies that classify as a “non-service” company do qualify for the deduction, while shareholders of companies classified as “service” companies, where the primary asset of the company is its employees (e.g., professional services firms), do not qualify.

The impact of the changes above has had a material effect on valuation as it relates to both C and S corporations. Specifically, C corporations benefit from the permanent reduction in the federal corporate tax to 21%. The economics behind the benefit of being a pass-through entity for tax purposes is largely diminished as a result of this change. While the 20% QBI deduction for shareholders offers a tax break similar to that of the permanent change for C corporations, it only applies to businesses classified as “non-service” companies, and it is expected that this benefit will expire beginning in 2026. With the benefits of converting or being formed as an S corporation largely diminishing, the trend in more corporations recently being swayed towards electing S corporation status may slow down or potentially even reverse. For example, IRC § 1202 provides for capital gains from select small business common stock to be excluded from federal taxes. While there are certain restrictions in place, one requirement to qualify for this tax break is that the company must be a C corporation. The permanent reduction in corporate tax rates is receiving more attention from corporations and their shareholders and adds to the potential tax advantages to being a C corporation over an S corporation.

With 2020 being an election year, tax planning is always a very important consideration when there is uncertainty or risk of change in tax law as a result. The coming months (with the election) and years (with potential changes to the tax code reverting back starting in 2026) may add to the importance for businesses and their shareholders to consult with their tax advisors to assess the advantages and disadvantages associated with a company’s tax status. With any corporate conversion, a valuation performed by an independent valuation firm provides support to the extent that a subsequent transaction draws scrutiny from the IRS.

- Internal Revenue Service, Statistics of Income Division, February 2020.

- In certain states, S corporations are subject to income taxation at the entity level.

- To the extent that distributions are paid out of the earnings and profits of the S corporation in any given year. Corporate net income is passed through to the shareholder and taxed to the individual; however, distributions are not subject to additional individual tax.

- The assets of a business consist of tangible items such as accounts receivable, inventory, machinery and equipment, and real property; identifiable intangible assets such as trade names, trademarks, assembled workforce, or proprietary processes; and unidentifiable intangible assets, commonly referred to as goodwill. The overall value of a business is comprised of the sum of these individual assets less its current liabilities (i.e., net working capital + other tangible assets + intangible assets). This total value of a business is commonly referred to as enterprise value. In order to arrive at total asset value, any outstanding current liabilities (excluding debt) must be added to enterprise value (i.e., Enterprise Value + Current Liabilities = Current Assets + Tangible Assets + Intangible Assets).