English

English

The rapidly evolving landscape of environmental, social, and governance (ESG) factors presents new challenges and opportunities for public companies. As ESG continues to make headlines, leaders of these institutions need to understand how the Securities and Exchange Commission’s (SEC) proposed climate-related disclosure requirements will affect them. These requirements, part of a wider regulatory trend, underscore the growing importance of ESG considerations in financial markets.

The disclosures primarily concern “The Enhancement and Standardization of Climate-Related Disclosures for Investors” proposal. A draft was released in early 2022 for comments, those comments have been reviewed, and the proposals are in the process of being finalized.

Navigating the SEC’s Proposed Disclosure Requirements

The SEC’s proposed rule will directly impact registrants, including recently acquired companies or those filing a registration statement for the first time.1 While these are required, companies have a vested interest in compliance, as sustainable businesses practices allow those companies to stay competitive in a landscape where consumer preferences are increasingly tilted toward sustainability and meet expectations of institutional investors who are increasingly sensitive to ESG factors. This will also allow the companies to understand how ESG risks could impact their products and services, and it could aid in attracting and retaining top talent in an industry where ESG credentials are increasingly important.

The relevant disclosures should be included in a separate section named “Climate-Related Disclosures” in registration statements and annual reports. Additionally, disaggregated climate-related financial statement metrics, derived primarily from existing financial statement line items, should be presented in the notes.

Six Key Climate-Related Disclosures

Qualitative Disclosures

1. Climate-Related Risks

Climate-related risks refer to the actual or potential negative impacts of climate-related conditions and events on a registrant’s consolidated financial statements, business operations, or value chains. The proposal requires disclosure of material risks over different time horizons, namely short, medium, and long term.

According to the proposal, registrants will first need to identify climate-related risks and then specify whether they are a physical or a transition risk. Physical risks refer to risks related to the physical impact of climate change, and they can be acute (like hurricanes or floods) or chronic (such as sustained higher temperatures or sea level rise. In contrast, transition risks refer to the risks related to a potential transition to a lower-carbon economy (such as regulatory, technological, market, liability, or reputational changes).

Following the identification and categorization of the climate-related risk, registrants will need to discuss an assessment of the materiality of risks over the time horizon.

2. Climate-Related Opportunities

Climate-related opportunities refer to the actual or potential positive impacts of climate-related conditions and events on a registrant’s consolidated financial statements, business operations, or value chains. These can include increased resource efficiency, cost savings from renewable energy use, development of new products, and increased resilience along supply or distribution networks.

The SEC proposes treating climate-related opportunities disclosure as optional due to anti-competitive concerns, though those disclosures can provide valuable insights for investors.

3. Governance

Under the SEC’s proposed disclosure requirements, governance forms a crucial aspect of climate-related disclosures. The rule would require entities to disclose the specific roles, responsibilities, and expertise of their board and management in overseeing climate-related risks and opportunities.

The proposal establishes two main pillars of governance: board oversight and management oversight.

Board Oversight: The first tier of governance, the board of directors, has a crucial role in overseeing climate-related risks and the management’s response to these risks. The rule requires that companies identify responsible board members or committees for oversight of risks, explain their expertise in those risks, discuss the processes and frequency of climate-related risk review, and discuss whether/how the board integrates climate-related risks into the overall business strategy, risk management, and financial oversight.

Management Oversight: The day-to-day management of climate-related risks and opportunities falls to the management team. As such, the proposal would require companies to identify responsible positions or committees for oversight of risks, disclose relevant expertise in risks, describe processes and frequency of risk oversight, and discuss whether responsible parties report to the board or board committee on those risks and the frequency it occurs.

4. Risk Management

The SEC’s proposed rule would require that companies describe how risk management processes are used to identify and assess risks, including how the risks’ significance, regulatory requirements, shifts in the market, and materiality are all considered. Companies will also need to describe how they are managing those risks, such as how risks are prioritized and how decisions are made to mitigate high-priority risks and mitigate/accept/adapt other risks.

If a registrant adopts a transition plan (a strategy and implementation plan to reduce climate-related risks, such as a plan to reduce its greenhouse gas emissions), the proposed rule requires a description of the plan, the relevant metrics and targets used, and how to mitigate or adapt to the physical or transition risks identified.

Quantitative Disclosures

5. Financial Statement Metrics

The financial statement metrics are a key aspect of the SEC’s proposed disclosure requirements and can provide investors with detailed insight into how an organization’s financial performance is affected by climate change.

The proposed rule requires a registrant to include disaggregated information about the material impact of climate-related events and transition activities on the consolidated financial statements. (Generally, those events and activities are linked to negative impacts. However, there could be situations where they result in positive impacts.) The proposed rule requires disclosure of the impacts from both climate-related events associated with physical risks and transition activities associated with transition risks on any of the financial statement metrics as well as the expenditure metrics.

Climate-related events include severe weather events and other natural conditions related to physical risk (flooding, drought, wildfires, extreme temperatures, sea-level rise, etc.). In contrast, transition activities consist of the transition risks and efforts to reduce greenhouse gas (GHG) emissions or mitigate exposure to transition risks. Examples include increased costs due to changes in law or policy, the devaluation or abandonment of assets, or reduced market demand for carbon-intensive products leading to decreased sales/profits.

A registrant may also disclose the impact of any opportunities arising from those events and activities on any of the financial statement metrics.

Financial Impact Metrics

These metrics demonstrate the ways in which climate-related events, transition activities, and opportunities can have a direct impact on a company’s financial health. Examples include:

- Changes to revenue or cost resulting from the loss of sales contracts due to new emissions pricing or regulations

- Adjustments to cash flows arising from changes in upstream costs

- Variations in the carrying amount of assets due to a reduction in useful life or salvage value as these assets become exposed to transition activities

- Changes to interest expense driven by financing instruments with climate-linked terms and conditions

The proposed rule provides a bright-line 1% threshold when determining what to include in the notes. In the example below, the cost of revenue balance is $1,000, and it is negatively impacted by Events A and B for $30, but it is positively impacted by Event C and Transition Activity D by $7 and $9, respectively. Therefore, the absolute value of all these impacts is $46, which translates into 4.6% of the total line item for the fiscal year.

As the 4.6% is greater than the 1% threshold, it will need to be included in the note disclosure despite some of the impacts being below the 1% threshold individually.

Financial impact metrics — bright-line 1% threshold

Example:

- Note X. Climate-related financial metrics:

*Example illustrates situation where registrant elected to include impacts from transition opportunities.

In the note, the table disaggregates the negative and positive impacts from climate-related events and from transition activities. In this example, the registrant chose to include the impacts from the opportunities as well.

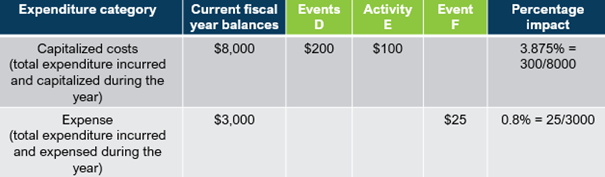

Expenditure Metrics

Expenditure metrics are broken down into expensed and capitalized expenses and are related to both climate-related events and transition activities. Examples include:

- Changes to interests related to financing for projects that are part of transition activities

- Changes in research and development activities to meet the increased demand for more environmentally friendly products

Like the financial impact matrices, the bright line 1% threshold also applies to expenditures.

In the example below, the capitalized costs represent 3.875% of the total capitalized cost for the fiscal year, over the 1% threshold, so it’s included in the note disclosure. However, the expenditure expensed representing 0.8% of the total for the fiscal year is below 1%, so no disclosure would be needed.

The example note shows the $200 impact from the events and $100 from transition activities.

Expenditure metrics — bright-line 1% threshold

Example:

- Note X. Climate-related financial metrics:

Financial Estimates and Assumptions Disclosures

Registrants will be required to disclose estimates and assumptions used in their financial reports. These should include qualitative descriptions of how these estimates and assumptions were impacted by exposures to risks and uncertainties related to the following:

- Climate-Related Events: Whether and how the estimates and assumptions used were affected by exposures to risks and uncertainties tied to climate-related events.

- Transition Activities: Whether and how the estimates and assumptions were developed and were impacted by potential transition or disclosed climate-related targets.

- Opportunity: If chosen, the company should disclose the impact of an opportunity on its financial estimates and assumptions. This allows potential investors to understand how a company might benefit from opportunities presented by climate change.

The financial statement metrics required by the SEC’s proposed rule can provide a comprehensive view of a company’s exposure to climate-related risks and opportunities. Registrants should comply with these requirements and use them as tools for strategic planning and risk management.

6. Greenhouse Gas Emissions

In the proposed rule, registrants are required to disclose their greenhouse gas emissions in accordance with three defined scopes:

- Scope 1 pertains to direct emissions resulting from the registrant’s owned or controlled operations

- Scope 2 encompasses indirect emissions arising from the generation of purchased or acquired electricity, steam, heat, or cooling consumed by the registrant’s operations

- Scope 3 covers all other indirect emissions outside of Scope 2, including those occurring in the upstream and downstream activities of the registrant’s value chain

Scope 1 and Scope 2 Disclosures

When making disclosures related to greenhouse gas emissions, registrants should provide comprehensive information. For Scope 1 and Scope 2 emissions, it is necessary to disaggregate the data by each constituent greenhouse gas and present both the individual and aggregated figures. These emissions should be disclosed in absolute terms as well as intensity terms, using carbon dioxide equivalent (CO2e) as the standard unit of measurement. Moreover, registrants should report gross emissions data without factoring in purchased or generated offsets. The intensity of greenhouse gas emissions can be expressed as a ratio, such as the number of tons of CO2e per unit of total revenue or per unit of production for the fiscal year.

Scope 3 Disclosures

Regarding Scope 3 emissions, registrants must disclose them if they are deemed material. The disclosure requirement extends to cases where the registrant has established a reduction target or goal that incorporates Scope 3 emissions.

SEC Accommodations

To facilitate compliance with these disclosure requirements, the SEC has introduced certain accommodations. Registrants can benefit from a safe harbor provision, which offers protection against certain forms of liability under federal securities laws. Smaller reporting companies (SRCs) are exempt from the disclosure provision, and a delayed compliance date is provided to allow for sufficient implementation time.2 These measures aim to support companies in meeting their GHG emissions disclosure obligations effectively.

SEC Proposed Rule Sentiment and Status

Comments received on the proposed rule have been reviewed. According to a study, most non-governmental organizations, investors, academics, and companies support the proposal, while most politicians and trade associations oppose it.3 Potential political and legal challenges arise in both the content of the rule and the SEC’s authority to pursue the rule. The most significant pushback revolves around the requirement for companies to disclosure GHG emissions that are generated, purchased, or indirectly generated from the company’s supply chain. Other resistance has formed against the proposal’s rule regarding shareholder proposals and proxy advisory firms.4

Regarding the timeline of the rule, former SEC Commissioner Robert Jackson said, “It looks like the rule is going to be pushed back a little further than many had thought …. Looks more like the fall of this year [2023].”5

The SEC’s proposed climate-related disclosure rule present a new set of requirements for public companies to navigate. As registrants step up to this challenge, there are regulatory obligations while demonstrating a commitment to sustainable business practices. By proactively engaging with these guidelines, companies can play a crucial role in building a more resilient financial system while simultaneously establishing a sustainable framework for the future.

- The proposed disclosure requirements would apply to companies filing SEC Forms S-1, F-1, S-3, F-3, S-4, F-4, S-11, 6-K, 10, 10-Q, 10-K, and 20-F, which include companies conducting initial public offerings or being acquisition targets of public companies.

- See “Amendments to the Smaller Reporting Company Definition” and “Smaller Reporting Companies” for the SEC's definition of an SRC.

- “Review of Comments on SEC Climate Rulemaking,” Cynthia A. Williams, Robert G. Eccles, Harvard Law School Forum on Corporate Governance, November 23, 2022.

- “Republicans press SEC division head on climate disclosure proposal, proxy rules,” Brian Croce, Pensions & Investments, July 18, 2023.

- “SEC's climate disclosure rules probably pushed back until fall,” Cydney S. Posner, Cooley LLP, Lexology, May 18, 2023.