English

English

The Spring 2020 edition of the Stout Journal discussed a list of 10 topics to consider when valuing legal entities. Herein, we discuss an additional 10 topics that should be considered carefully when performing a valuation of multiple legal entities within a parent’s organizational structure. These valuations are most common in international tax reorganizations and acquisition accounting valuations requiring a “push-down” to individual legal entities. Such situations present management with additional circumstances and considerations throughout the valuation process.

1) Understanding Legal Entities’ Functional Purposes

Multinational enterprises frequently maintain sprawling organizational charts containing dozens or even hundreds of legal entities that are organized to perform specified functions in a particular country or region (e.g., sales and marketing, distribution, manufacturing, or intellectual property ownership). In these situations, it is important to understand the entities’ operations and how each supports the others. Further, technical valuation issues, such as utilizing appropriate valuation methodologies, public company peers, and the selection of market multiples, require additional attention.

2) Bridging Legal Entity and Consolidated Forecasts

As with other business valuations, prospective financial information (PFI) is a critical input. Frequently, however, management will not prepare forecasts for the legal entities in the standard course of business. This means that management may be preparing the legal entities’ PFI for the first time.

Critically, when doing so, the geographic location, functional purpose, and other entity-specific factors must be considered. For example, within a particular geographic region there may be a manufacturing entity, several distribution entities covering various markets, as well as a principal operating entity that functions as the regional “entrepreneur” wherein it absorbs the remaining risk and reward of the regional activities. In this instance, the manufacturing and distribution entities may be limited to a routine margin, considering their respective functional purposes, with the remaining margin attributed to the entrepreneur entity.

Once management has compiled the PFI, the valuation specialist needs to understand how the individual legal entities’ forecasts tie out to the consolidated company’s PFI and how foreign currencies and inflation levels were factored into and impacted the detailed build-up.

3) Cross-Border Economic Exposure

Operating legal entities across the globe can pose added risk in the form of country-specific risk factors due to different economic and political climates. However, the country in which legal entities are domiciled may not always correspond to the added risk inherent in the operations and cash flow generating ability. For example, a company may organize legal entities in certain countries due to geographic proximity to suppliers or a locally trained labor force. Assuming these legal entities are in a country that warrants a high country risk premium, the valuation specialist needs to take care in assessing the actual risk of the cash flow generating ability of these entities. Specifically, legal entities in a high-risk country that are supporting and generating the entirety of their cash flow in lower-risk countries may warrant a risk premium more akin to that of the country in which they are generating the cash flows rather than that in which they are domiciled.

4) Tax Nuances Between Legal Entities and Countries

Similar to how statutory tax rates vary from one country to another, the effective tax rate between legal entities also differs. Not only does the tax rate vary by country, but so does the earnings stream that can be taxed. While most countries have a set statutory tax rate for all corporations, some (e.g., the United Arab Emirates) have varying tax rates based on the legal entities’ industry. Furthermore, indirect taxes, including a value-added tax or goods and services tax, are in place in over 160 countries. When unique tax circumstances arise, the valuation specialist needs to perform thorough research regarding the specifics of the tax policies in place for each of the countries in which the legal entities operate and/or consult with the company’s internal or external tax experts. Valuation specialists should also consider historical effective tax rates. A comparison of the legal entities’ historical effective and statutory tax rates will help outline any tax differences that should be considered, such as loss carryforwards or other types of tax vs. book differences and credits. These tax items need to be separately addressed in the valuation to determine the expected benefit or detriment.

5) Forecasting Working Capital and Capital Expenditures

The nature of the legal entities will dictate how to appropriately allocate the annual forecasted investment in working capital and capital expenditures. For example, the working capital needs and investments in machinery and equipment will likely vary significantly between a manufacturing entity and one responsible solely for sales and marketing; accordingly, simplified allocations (e.g., as a percentage of sales) can be misguided. Further, the existence of intercompany transactions should prompt discussions with management to determine whether these items reflect “traditional” working capital items or whether they are akin to financing decisions made by the company.

As a “check” of reasonableness, the valuation specialist will compare historical financial statements to the forecast to discern whether the forecast reflects and assumes that the entities’ go-forward operations are in a manner consistent with how they historically operated. Inconsistencies might prompt further discussions and a comparison of projected ratios to those of guideline public companies.

6) Adjustments to Enterprise Value

From a balance sheet perspective, international tax reorganizations require similar scrutiny as a typical business enterprise valuation. Specifically, consideration should be given to non-operating assets and liabilities that do not contribute to the operations of the legal entities. For example, entities may hold assets that are unused in the operation of their business (e.g., vacant land). In that instance, the valuation specialist will need to determine and add the fair market value of the asset or liability to the enterprise value of the legal entities since the asset does not contribute to the cash flow of the business.

7) Can You Conclude on Negative Equity Value?

The Asset Approach is often relied upon to value holding companies, entities that may have negative equity balances. Unless there are substantive valuation adjustments to investments in subsidiaries or other assets and liabilities, this could result in a negative calculation of value. In these cases, the valuation specialist may need to consider whether there are offsetting liabilities on the balance sheet that management considers to be equity infusions from another legal entity in the form of a payable and thus would have a fair market value of zero since the payable would not be expected to be repaid. This most often occurs in the form of a loan guaranty from one legal entity to another, but it can also occur in less obvious situations, such as when another entity is legally required by the company’s organizational structure to act as a safeguard against any excess liabilities.

8) Adding It Up: How Each Investment in Subsidiary and Legal Entity Conclusion Flows to the Parent

It is common for global corporations to organize themselves in a manner that provides several intermediate layers of holding companies between the parent company and the operational legal entities in order to limit financial and legal liability exposure.

The challenge from a valuation perspective entails what is valued and reported separately. Under the consolidated method of accounting, the legal entities’ valuations will inherently include the value of any underlying subsidiaries (since those subsidiaries’ financials are reported in line with the subject’s). However, this does not allow for the value of the subsidiaries to be separately broken out. If the legal entities are accounted for under the equity method, the parent legal entities can be valued separately from investments in subsidiaries. Often, the valuation professional will use a “bottom-up” approach by starting with the valuation of the lowest-lying entities and working up to the ultimate parent.

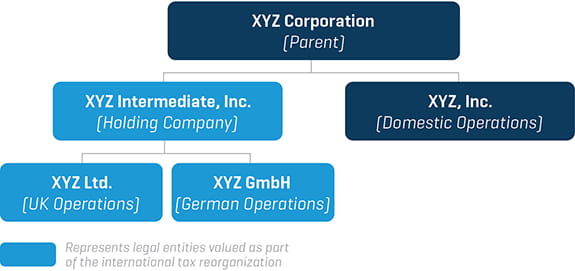

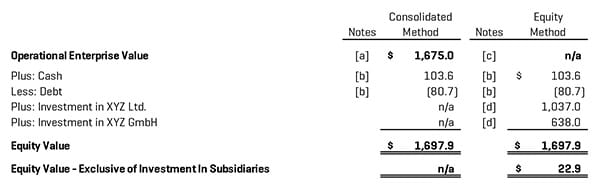

As an example, refer to Figure 1, which depicts the organizational chart of XYZ Corp. Figure 2 presents the valuation build-up conclusion of XYZ Intermediate (“Intermediate”) under both the consolidated method and the equity method. In this example, Intermediate is a holding company with a balance sheet comprised of $103.6 million in cash, investments in two foreign, legal entities (XYZ Ltd. and XYZ GmbH), a debt balance of $80.7 million, and equity. XYZ Ltd. and XYZ GmbH are the operating companies, and their values are inherently captured in Intermediate via the consolidated method. Via the equity method, the values of XYZ Ltd. and XYZ GmbH are explicitly presented based on their respective individual valuation conclusions.

Figure 1. Organizational Chart of XYZ Corporation

Figure 2. XYZ Intermediate, Inc. Value Conclusion

($ in millions USD)

n/a = not applicable

[a] Represents the value from XYZ Intermediate, Inc. wholly-owned subsidiaries, exclusive of any cash or debt.

[b] Represents the book balance of cash and debt under the consolidated method for XYZ Intermediate, Inc.

[c]] XYZ Intermediate , Inc. is a holding company and thus has no operations.

[d] Fair market value basis.

9) Reasonableness Check: Sum-of-the-Parts Value Relative to the Consolidated Company

One common reasonableness check to assess the veracity of the underlying subsidiary valuation conclusions is to compare the aggregate value conclusions included within the scope of the tax valuation to the value of the consolidated company. When presenting conclusions under the “consolidated method,” determining the aggregate value of the legal entities can be more complicated.

After concluding on and accounting for the value of the legal entities and their appropriate ownership structure, we derive the fair market value of the consolidated company. As a reasonableness check, the valuation professional can compare the consolidated value to the company’s public market capitalization (or enterprise value). However, for private companies, alternative analyses may be required and can include a comparison based on key financial metrics (revenue, EBITDA, total assets, etc.) for the legal entities to the consolidated company. This will allow the valuation specialist to compare the legal entities’ relative share of the overall financial performance and cash flow to the concluded share of the total company value, considering the relative growth, profitability, and risk of the entity subset in relation to the consolidated company.

10) What Is an Appropriate Valuation Date?

Management needs to understand the length of time that local tax authorities view as acceptable to pass before the valuation is viewed as “stale” and thus unacceptable. This may depend on multiple factors, such as whether any material changes occurred to the business environment between the valuation date and the reorganization transaction date. In instances where the tax reorganization does not take effect for some time after the valuation is performed, an updated valuation, or bring-down letter, can be utilized to help “bridge” the concluded values as of the valuation date to the tax reorganization date. Essentially, a bring-down letter addresses the primary concerns regarding the passage of time, including significant changes in the financial results and outlook of the legal entities and significant changes in market conditions (interest rates, valuation multiples, the general economic environment, etc.). In many cases, a bring-down letter helps management support the validity of the initial valuation to the relevant tax authorities.

Final Thoughts

When management understands the key components and factors involved in a valuation, including multiple legal entities and the importance of their role in coordinating the appropriate information, this should lead not only to a comprehensive and thorough process that results in a more supportable valuation, but also an easier review by the tax authorities.