Deutsch

Deutsch

In an effort to reduce the costs and complexity of goodwill impairment tests, the Financial Accounting Standards Board (FASB or the “Board”) issued Accounting Standards Update (ASU) No. 2017-04, Intangibles – Goodwill and Other (Topic 350): Simplifying the Test for Goodwill Impairment (ASU 2017-04) on January 26, 2017. While ASU 2017-04 made significant changes to Accounting Standards Codification (ASC) Topic 350, Intangibles – Goodwill and Other (ASC 350), its main provision eliminated step two (Step II) for goodwill impairment tests under ASC Topic 350-20-35, Goodwill – Subsequent Measurement (ASC 350-20-35).

Currently, ASC 350-20-35 provides for quantifying goodwill impairment under a two-step model. An entity first identifies the potential for goodwill impairment under step one (Step I) and then quantifies the amount of impairment under Step II. Goodwill impairment exists in Step II if the carrying value of an entity’s goodwill is greater than its implied fair value. With the amendments made under ASU 2017-04, goodwill impairment tests will be performed under a one-step model, whereby the goodwill impairment amount is determined based on the carrying value of a reporting unit and its fair value.

ASU 2017-04 applies to public business entities and other entities that have goodwill reported in their financial statements and have not elected the private company alternative for the subsequent measurement of goodwill under ASU No. 2014-02, Intangibles – Goodwill and Other (Topic 350): Accounting for Goodwill (a consensus of the Private Company Council) (ASU 2014-02). The effective date for ASU 2017-04 varies based on an entity’s characteristics, as outlined below. However, FASB allows companies early adoption of ASU 2017-04 for goodwill impairment tests with measurement dates after January 1, 2017.

- Impairment tests performed after December 15, 2019: Public entities that file with the Securities and Exchange Commission (SEC)

- Impairment tests performed after December 15, 2020: Public entities that are not SEC filers

- Impairment tests performed after December 15, 2021: All other entities, including nonprofit entities

We present the key procedural differences between ASC 350-20-35 under ASU 2017-04 and the prior two-step model in our following discussion.

Taking a Step Back: How Did We Get Here?

In response to concerns expressed by private companies, FASB issued ASU 2014-02 in 2014. The main provision of ASU 2014-02 was to provide an accounting alternative to private companies that allowed for the amortization of goodwill on a straight-line basis over 10 years (or less, if another useful life is applicable), testing for goodwill impairment at the entity level or the reporting unit level, and testing for goodwill impairment only when a triggering event has occurred. Further, similar to ASU 2017-04, ASU 2014-02 permits a private company to test and measure goodwill impairment by comparing the fair value of a reporting unit with its carrying value (thereby eliminating Step II). Additionally, FASB initiated a two-phase research project in 2014 to determine whether similar amendments should be applied to public and nonprofit entities. While phase one of the project resulted in ASU 2017-04, phase two focused on additional changes to the subsequent accounting for goodwill, including amortization of goodwill and additional changes to the impairment testing methodology. However, in 2016 the Board suspended discussions on phase two and moved it to its research agenda in order to evaluate the effectiveness of ASU 2017‑04.

The Current Two-Step Model Under ASC 350-20-35

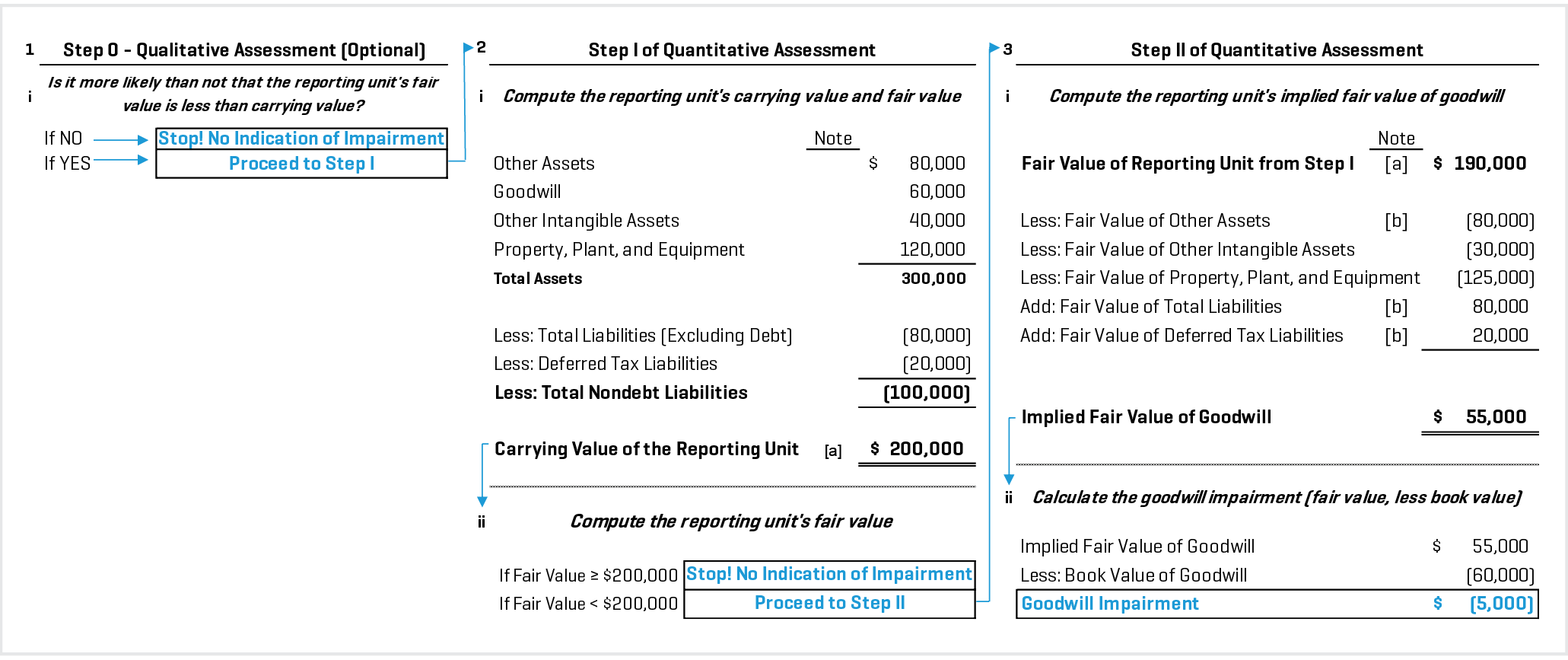

Current guidance under ASC 350-20-35 requires goodwill impairment to be tested at the reporting unit level. Before quantifying the magnitude of goodwill impairment, if any, an entity can perform a qualitative assessment (Step 0) to determine whether it is necessary to perform Step I and Step II. However, ASC 350-20-35 allows entities to bypass Step 0 and proceed directly to Step I and Step II.

Step 0 (presented in the first column of Figure 1) allows an entity to first assess qualitative factors to determine whether it is more likely than not (i.e., a likelihood of more than 50%) that the fair value of a reporting unit is less than its carrying value by assessing relevant quantitative and qualitative factors. If the assessment of the quantitative and qualitative factors indicates that it is more likely than not that the fair value of a reporting unit is less than its carrying value, then the entity must perform Step I.

Under Step I (presented in the second column of Figure 1), an entity identifies the potential impairment of goodwill by comparing the fair value of a reporting unit with its carrying value. If the carrying value of the reporting unit is greater than its fair value, an entity must proceed to Step II in order to measure the magnitude of impairment, if any. Prior to estimating a reporting unit’s fair value, an entity must determine whether the fair value estimation assumes a nontaxable or a taxable transaction. Further guidance under Step I prescribes that an entity must perform Step 0 for a reporting unit with a carrying value equal to or less than zero in order to determine the likelihood of impairment.

Finally, Step II (presented in the third column of Figure 1) compares the carrying value of goodwill with its implied fair value. ASC 350-20-35 states that the fair value of goodwill must be determined in the same manner that the amount of goodwill recognized in a business combination is determined. Specifically, the fair value of a reporting unit is allocated to all the assets and liabilities (including any unrecognized intangible assets) as if the reporting unit had been acquired in a business combination and the fair value of the reporting unit was the acquisition price. The excess of the fair value of the reporting unit over the amounts assigned to the reporting unit’s assets and liabilities is the implied fair value of goodwill. If the carrying value of goodwill exceeds its implied fair value, the entity recognizes a loss equal to the excess of carrying value over fair value. The loss recognized is limited to the carrying value of goodwill. After the entity records a loss, the adjusted carrying value of goodwill is its new accounting basis, and any subsequent reversal is prohibited.

As presented in the third column of Figure 1, Step II indicated that the fair value of Company A’s other intangible assets is $10 million less than its book value, while the fair value of Company A’s property plant and equipment is $5 million more than its book value. Accordingly, in this instance, Company A would incur an impairment loss of $5 million.

FIGURE 1. Company A’s Goodwill Impairment Test Prior to ASU 2017-04 ($ IN THOUSANDS)

[a] The carrying value and fair value are presented on an enterprise basis (i.e., inclusive of debt and equity).

[b] The fair value of the asset or liability is estimated to be equal to book value.

Eliminating Step II Under ASU 2017-04

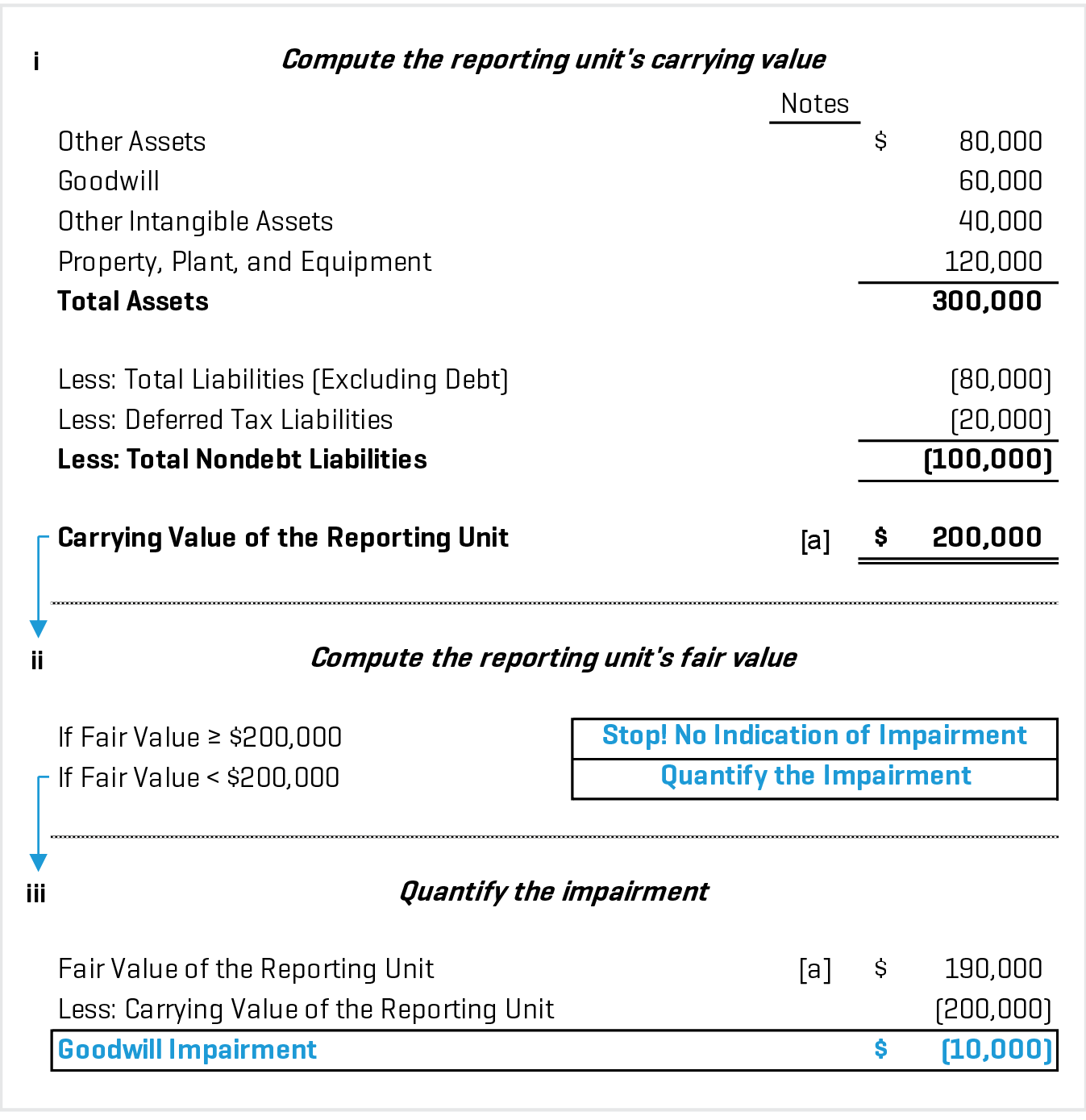

The amendments detailed in ASU 2017-04 essentially eliminate Step II. As in ASC 350-20-35, entities have the option to bypass Step 0. If Step 0 indicates impairment or the entity bypasses Step 0, ASU 2017-04 provides that the entity must perform a quantitative impairment test (the “Quantitative Test”). The Quantitative Test is used to identify both the existence and the amount of impairment. Similar to Step I before ASU 2017-04, the Quantitative Test compares the carrying value of the reporting unit with its fair value. If the carrying value of a reporting unit exceeds its fair value, an impairment loss is recognized in an amount equal to the excess of carrying value over fair value. Similar to previous guidance, the impairment of goodwill is limited to the carrying value of goodwill.

Figure 2 illustrates the Quantitative Test for goodwill impairment under ASU 2017-04, where Company A no longer needs to measure the fair value of each asset and liability to quantify the amount of impairment. Instead, goodwill impairment is simply measured by the excess of the carrying value of the reporting unit over its fair value (limited to the total amount of goodwill allocated to that reporting unit), as presented in Figure 2. Under ASU 2017-04, Company A would record a goodwill impairment of $10 million, which ignores any changes in the fair value of the entity’s assets and liabilities (which Step II considers in Figure 1). Therefore, the goodwill impairment charge under ASU 2017-04 does not consider the true economic value of Company A’s assets and liabilities.

FIGURE 2. Company A’s Goodwill Impairment Test Under ASU 2017-04 ($ IN THOUSANDS)

[a] The carrying value and fair value are presented on an enterprise basis (i.e., inclusive of debt and equity).

It should be noted that ASU 2017-04 also eliminated ASC 350-20-35-8A, which forced entities to perform Step 0 if the reporting unit’s carrying value was equal to or less than zero. Now such reporting units are assumed to pass the Quantitative Test, but the entity must disclose the amount of goodwill allocated to such reporting units.

It Cannot Be That Simple: The Circularity of Deferred Taxes Under ASU 2017-04

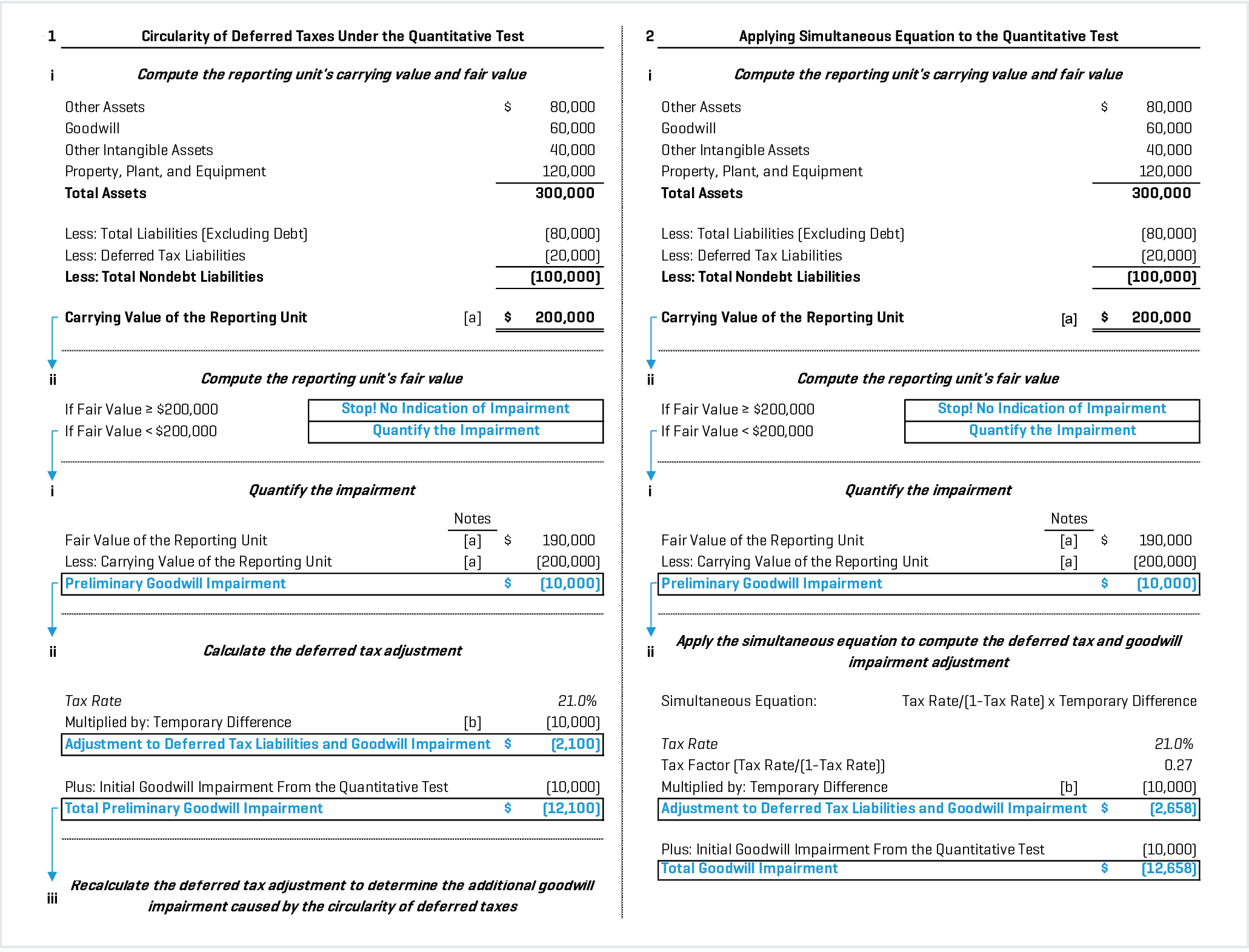

While ASU 2017-04 streamlines the goodwill impairment model, it introduces a new intricacy related to deferred taxes. The Board stresses the importance of considering the related income tax effect from any tax-deductible goodwill under ASU 2017‑04. Certain tax jurisdictions allow business entities to amortize goodwill for tax purposes, which creates deferred tax entries based on the difference between the book basis and the tax basis of goodwill. If an entity is afforded the right to amortize goodwill for tax purposes and it impairs goodwill under the Quantitative Test for book purposes, it will likely cause a change in deferred taxes that results in the carrying amount immediately exceeding fair value after accounting for such impairment. To mitigate this issue, FASB introduced ASC 350-20-35-8B and ASC 350-20-35-8C.

ASC 350-20-35-8B provides that an entity must calculate the deferred tax effect from the impairment loss in a manner similar to that used in a business combination. Consider Company A from Figure 2, where it recorded a deferred tax liability of $20 million and a goodwill impairment of $10 million. For simplicity, let us assume the goodwill is amortizable for tax purposes and the entire deferred tax liability relates to the difference between the tax basis and the book basis of goodwill. Further, let us assume that Company A’s federal tax rate is 21%. As indicated in Figure 3, Company A’s deferred tax liability is reduced by $2.1 million directly after the impairment. Given the decrease in deferred tax liabilities, Company A’s carrying value exceeds its fair value immediately after accounting for goodwill impairment. Therefore, Company A would potentially need to continuously calculate the goodwill impairment charge and its effect on deferred taxes until carrying value equals fair value. To address the circular nature of this impact, the Board introduced a simultaneous equation under ASC 350-20-55-23C to help quantify the related income tax effect from any impairment of tax-deductible goodwill, as displayed in second column of Figure 3.

FIGURE 3. Applying the Simultaneous Equation to Address Company A’s Deferred Tax Circularity Under ASU 2017-04 ($ IN THOUSANDS)

[a] The carrying value and fair value are presented on an enterprise basis (i.e., inclusive of debt and equity).

[b] The temporary difference reflects the difference between the book basis and tax basis of goodwill (i.e., the $10 million goodwill impairment).

The Advantages and Disadvantages of Early Adoption: FASB’s Split Decision

As highlighted in Figures 1 and 2, the two-step goodwill impairment model can be a burdensome process. ASU 2017-04 simplifies impairment testing by eliminating Step II and introducing the Quantitative Test. With the Quantitative Test, a reporting unit simply computes impairment of goodwill under a one-step quantitative model instead of first identifying potential impairment (Step I) and then quantifying impairment (Step II).

However, the Board voted four to three on ASU 2017-04, with the three opposing members raising concerns on the potential economic irrelevancy of the accounting outcome under the Quantitative Test. For instance, the opposing members and several financial institutions addressed a specific concern related to the decline in the fair value of reporting units of financial institutions in a rising interest rate environment. This decrease in fair value of the reporting unit may cause these institutions to record a goodwill impairment under ASU 2017-04, even though the decrease in the fair value of the reporting unit may be caused by a reduction in the fair value of financial assets carried at amortized cost.

Although the three opposing members agreed with the simplification of goodwill impairment testing, they believe that the Quantitative Test will result in entities misstating goodwill impairment. For example, consider Company A from Figures 1 and 2. Before ASU 2017-04, Company A would record a goodwill impairment charge of $5 million, while the Quantitative Test indicated an impairment of $10 million. The $5 million impairment differential is caused by the step-up of Company A’s tangible assets and step-down of intangible assets to their respective fair values under Step II. Therefore, Step II correctly estimates the fair value of Company A’s goodwill by recognizing the fair value of its assets and liabilities, while the Quantitative Test overestimates Company A’s goodwill impairment by $5 million.

Furthermore, we have observed several instances in which a company failed Step I of the impairment test, but after remeasuring the other assets and liabilities to fair value, Step II indicated no impairment of goodwill, due largely to a decline in the fair value of intangible assets. Before early adoption, we recommend that companies take a wait-and-see approach pending the results of future impairment tests under the prior framework. To this end, we have observed the following footnote disclosure in a Form 10-K filing related to ASU 2017-04:

The Company is currently evaluating the impact of this standard on its consolidated financial statements depending on the outcomes of future goodwill impairment tests.

Considering the foregoing, the opposing Board members’ comments suggested alternatives to the amendments under ASU 2017-04, which included requiring entities to perform the Quantitative Test under the enterprise premise of value and providing entities with an option to perform Step II. Nonetheless, the cost-benefit of early adoption should be weighed against the possibility of misstating goodwill impairment under the Quantitative Test.