Français

Français

While private asset valuations do not tend to move in lockstep with public markets, they are built on the same foundation (cash flows, discount rates, credit spreads, comparable-company multiples, and transaction evidence) captured through models, appraisals, and market data. Q1 2026 delivered a multitude of macroeconomic and geopolitical shocks large enough to force valuation reassessments across private equity and private credit portfolios.

As of March 31, 2026, the key story is not simply “valuations are down.” It is how risk is being (or should be) repriced: higher discount rates, wider credit spreads, more conservative growth assumptions, and greater scrutiny of liquidity terms and valuation governance.

This article highlights considerations for evaluating fair value as of March 31, 2026, under ASC 820 and/or IFRS 13. It is not a market forecast but a practical discussion of what has changed, what evidence market participants may be using, what questions should be asked of portfolio companies, and what valuation committees should be prepared to support with documentation.

Recent Market Activity: 2025 Backdrop

At year-end, investors were positioned for a continuation of the 2025 playbook. Public equity indexes including the S&P 500, Dow, and Nasdaq were close to (but not at) historic peaks. Risk appetites remained constructive, and many private marks still reflected 2024–2025 entry multiples and “normalized” exit assumptions. At the end of 2025:

- Ukraine war grinding on, but “known risk”: Russia’s invasion of Ukraine was approaching its fourth anniversary with no victory in sight. Markets had largely incorporated the conflict as background risk that was tragic and destabilizing but not newly inflationary.

- Escalating rhetoric toward Venezuela: President Trump signaled a tougher stance and moved quickly after inauguration, but the base case still assumed contained volatility.

- Iran negotiations still on the table: The U.S. negotiating posture on Iran’s nuclear capabilities implied a possible military path but not an imminent one, and many investors treated this as tail risk.

- Private markets focused on product expansion and fundraising: Alternative managers were pushing interval funds and other semi-liquid vehicles to reach high-net-worth and retail channels. That growth trend mattered to managers and investors because it assumed steady inflows and stable liquidity management.

- Private credit — Questions emerging, but contained: Increased defaults and restructurings had started to challenge the “private credit is defensive” narrative. The default rate among U.S. corporate borrowers of private credit rose to a record 9.2% in 2025, as reported in the March 2026 report by credit rating agency Fitch Ratings.

For valuation professionals (either within a fund or external), these issues matter less as headlines and more as inputs:

- Energy price sensitivity embedded in forecasts

- Customer demand shocks for exposed regions/industries

- Risk premia (equity and credit) demanded by market participants for uncertainty

- Market data related to transactions, including in the secondary markets

Fast Forward to Mid-March 2026: Geopolitical Shock and Risk-Off Conditions

By mid-March, several events changed the market’s immediate pricing of risk. Major equity indices were flat-to-down versus December 31, 2025, and public markets were no longer signaling easy multiple expansion. Meaningful events included:

- Maduro extradition/escort to the U.S.: The removal of President Maduro to face U.S. federal charges injected sudden uncertainty into oil geopolitics and regional stability, with second-order effects on energy prices, sanctions regimes, and supply expectations.

- Partial Government Shutdown: On February 14, when Congress failed to agree and approve funding for certain agencies, particularly the Department of Homeland Security (DHS), large portions of the federal government — including the DHS, the Pentagon, the Department of Health and Human Services, and the Department of Transportation, among others — were impacted.

- Stress in the Private Credit Market: Several widely known asset managers limited or suspended redemptions on retail-focused funds. This has not been well received by the market, with immediate ripple effects across private credit asset class: tender offers for locked up shares as interval funds face redemption pressure and JP Morgan questioning leverage on leveraged loan portfolios.

- AI Concerns: Citrini Research published a report with a grim scenario in which AI upends the U.S. economy, driving unemployment to over 10%, rattling investors. Software-as-a-service (SaaS) companies were specifically identified in the report as big losers due to AI advancements, sending SaaS heavy indexes lower. The S&P Software & Services Select Industry Index was down as much as 15 percent in February 2026, finishing the month down 10 percent from January.

- Ukraine passes four years with no resolution: The lack of an end reinforced the idea that Europe’s energy and security regime is structurally different for longer. This is relevant for industrials, manufacturing, and any private portfolio companies exposed to European demand, logistics, or energy-intensive inputs.

- U.S. and Israel bomb Iran: The strike pushed equity markets lower and energy prices higher, reintroducing a classic macro problem: inflationary impulse plus risk-off sentiment. Iran bet that retaliating against neighbors would increase criticism on the U.S./Israel action, but the opposite has happened. A new supreme leader who is the son of the deceased leader took power, with his wife and child reportedly killed in the attack as well, making quick de-escalation less likely in the market’s view. Supply chain for oil in the region was disrupted, pushing prices to $100+ / barrel.

Impacts on Private Valuations

For private valuations, while the index level is important, the shift in required return and financing conditions that typically accompany risk-off periods needs to be considered as well. Recent events have shifted multiple inputs used in valuation models, which can have meaningful impacts:

- Discount rates have gone up: Higher risk-free expectations, higher equity risk premium, and higher idiosyncratic risk factors.

- Cash flow forecasts have gone down in some sectors: Margin pressure from energy and other cost increases, combined with lower demand.

- Exit multiples may have compressed: Public comps re-rate as buyers demand higher returns.

- Financing assumptions have worsened: Higher spreads, tighter covenants, and less leverage at closing impact the capital mix and weighted cost of capital on deals.

Private marks don’t usually “gap down” in real time like public markets, but Q1’s magnitude increases the pressure on valuation committees, auditors, LPs, and lenders to reflect reality faster.

In March of 2020, when the COVID outbreak began, markets were also disrupted with some uncertainty as to how to approach private asset valuations. As that economic downturn created tumultuous markets for financial instruments, Stout offered guidance for the application of fair value accounting. That high-level guidance still applies and can be seen here.

Below, we’ll take a closer look at some of the value drivers and implications.

Private Equity: The Valuation Squeeze Returns (Even if EBITDA Is Stable)

Multiple Compression: The Math Becomes Unforgiving

Even though private, valuations for private equity-backed companies are heavily influenced by multiples for public market comparables and transaction multiples. When public comps flatten or decline, especially for growth sectors, sponsors face two simultaneous headwinds:

- Lower comparable multiples lead to lower indicated enterprise values

- Higher discount rates lead to lower present values in discounted cash flow (DCF) frameworks

Even modest changes matter since a one-turn decline in EV/EBITDA on a business levered at typical buyout levels can meaningfully reduce equity value. Loan covenants can also be triggered, sending an otherwise performing company into technical default.

Energy Price Shocks: Inflation Comes Back Through the Side Door

The Iran strike and subsequent energy price increases affect private portfolio companies unevenly:

- Winners (likely): Energy services, certain industrials tied to defense and infrastructure, and logistics segments that can pass through surcharges quickly.

- Losers (often): Consumer discretionary, transportation-heavy models without pricing power, energy-intensive manufacturing, and companies with fixed-price contracts.

In valuations, this shows up as lower forward margins where input costs can’t be passed through, higher working capital needs, and greater uncertainty around “normalized” earnings.

Exit Environment: Slower Realizations, Higher Required IRRs

Even if portfolio company fundamentals are holding up, a risk-off market tends to reduce IPO viability (there are exceptions such as SpaceX or Anthropic), widen the bid-ask spread in M&A, and push buyers to underwrite to lower exit multiples.

Reduced exit options, in turn, can lead to longer hold periods (decreasing IRRs even if MOIC [Multiple on Invested Capital] holds), as well as more continuation vehicles. For SaaS companies with contractual annual recurring revenue (ARR), operating performance now may be consistent, but increased spreads suggests refinancing risk, as AI may negatively impact new contracts or contract renewals down the road.

Private Credit: The Quarter Where “Liquidity And Marks” Became the Story

Private credit is valued using a mix of yield-based discounting, comparable spread analysis, and, in many cases, manager judgment due to limited observable trading levels. Q1 2026 sharpened the debate on three fronts: credit risk, duration/growth risk, and liquidity/valuation governance.

The AI Shock to SaaS

A key theme emerging in Q1 is the market’s reassessment of SaaS durability in a world where AI changes customer switching costs, pricing power (automation and commoditization), and required R&D spend.

Private credit is exposed since many direct lending portfolios are populated with sponsor-backed, recurring-revenue software businesses, which were historically seen as “safe” because of contracted revenue and high gross margins.

As SaaS multiples fall, enterprise values decline eroding equity cushion under the debt. As earnings forecasts reset (growth deceleration, higher churn, pricing pressure), interest coverage weakens further, increasing refinancing risk as lenders demand wider spreads or tighter structures. This doesn’t mean “software is unbankable,” but it does mean that credit underwriting needs to treat some SaaS subsegments less like utilities and more like competitive, fast-changing markets. As noted above, refinancing may become challenging where contract renewals show evidence of slowing.

Prominent Fund Headlines: Suspensions, Secondary Sales, and the Governance Spotlight

There were several incidents in Q1 2026 illustrating how current events translate into valuation and confidence effects:

As has been widely reported, limited or suspended redemptions by funds have gotten headline attention in the press. The suspensions have led investors to question if asset-level liquidity was overestimated, redemption features were mismatched to underlying loans, and/or if valuations were slow to reflect real clearing levels. In one instance, a secondary transaction was effected near par value.

The secondary sale near par has been interpreted in differently in the market:

- Positive: Assets are fundamentally money-good; NAV discipline is validated.

- Negative: If redemptions were suspended yet assets could be sold at par, investors may ask why liquidity gates were necessary and whether all investors were treated consistently, or whether the sale involved selection effects (selling the best assets first leaving remaining investors with less good assets).

Either way, the event raises the bar for disclosure/transparency: portfolio stratification, watchlists, non-accrual trends, and how marks are derived.

With the private credit industry facing these challenges, JP Morgan reportedly sought to reduce its exposure by marking down the value of loans held by the bank as collateral. By marking down the collateral, borrowing firms had reduced availability to leverage their portfolios.

With respect to valuation, these recent events highlight diverging approaches to smoothing versus responsiveness of marks, liquidity risk management, and communications with investors.

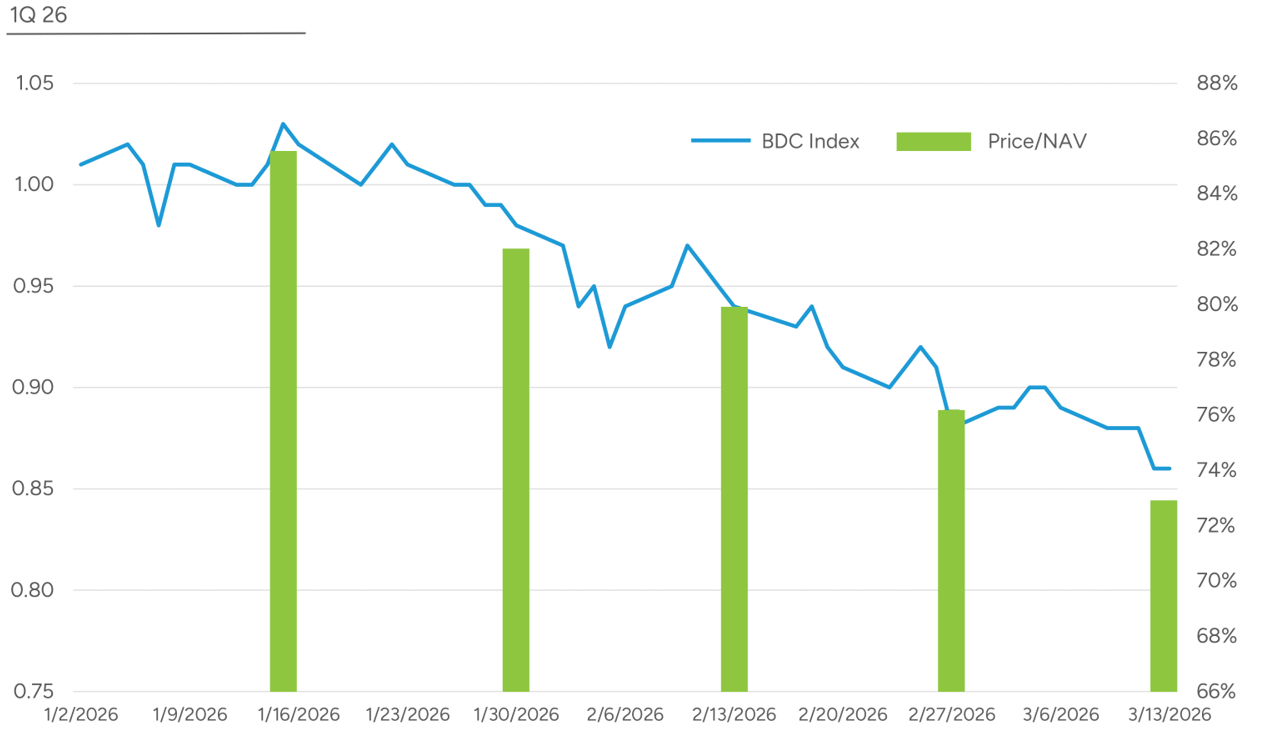

Public Pricing Derived From Private Assets

Sentiment towards private assets can be seen, in part, in the pricing of publicly traded business development corporations (BDCs). The S&P BDC Index tracks the pricing of 44 publicly traded BDCs with market caps ranging from $100 million to $12.8 billion with a median of $757 million as of March 15, 2026. Through mid-March, the BDC index was down 14% year to date, compared to the broader market, as measured by the S&P 500, which was down only 3% over the same period.

BDC shares are typically traded based on the net asset value (NAV) of the shares, and usually at a discount. NAV for public BDCs is typically reported on a quarterly basis, so for traded prices as of year-end 2025, the most recent NAV for most of the BDCs in the S&P BDC Index would be as of September 30, 2025, while in mid-March the most recent NAV would be as of December 31, 2025.

Looking at changes in valuations between the two most recent quarters, most of the BDCs in the S&P BDC Index reported a decrease in NAV per share; however, the median decrease among the group was below 1%. Share price decreases in Q1 2026, therefore, reflect an increasing discount to NAV. Over the first quarter, the median price to NAV decreased from 84% at year-end 2025 to 73% or a median discount of 27% to NAV as of March 15, 2026.1 The increasing discount to NAV suggests investors are expecting decreases in NAV per share going forward, a lack of confidence in the last reported value of the assets, or both.

Public BDC Prices

Themes to Watch

Sectors Most Likely to Take the Biggest Hits to Private Credit Marks

Based on the Q1 2026 backdrop (geopolitical risk, energy inflation, growth uncertainty, and AI disruption concerns), the areas drawing the most scrutiny tend to be:

- Software/SaaS with weak differentiation (AI-driven disruption, pricing pressure)

- Consumer discretionary (demand elasticity and inflation sensitivity)

- Transportation/logistics with fixed-price exposure (energy cost volatility)

- Healthcare services with reimbursement or labor pressure (if wage inflation persists)

- Highly levered sponsor-backed cyclicals (lower tolerance for earnings volatility)

Conversely, relative “resilience” narratives in private credit may include:

- Asset-backed lending with strong collateral controls

- Mission-critical B2B services with pricing power

- Energy-adjacent credits (though commodity volatility raises its own risks)

- Defensive infrastructure-like cash flows with contractual escalation

Higher Scrutiny on Key Inputs

Valuation committees and auditors will likely press harder on discount rates and risk premia assumptions, comparable company selection (and whether comps have structurally changed), terminal values, and “normalized” margins. The line between “temporary shock” and “permanent impairment” (especially in software) will be tested.

More Emphasis on Scenario Analysis

Expect to see more explicit downside cases tied to sustained high energy prices, recession or stagflation scenarios, delayed refinancing windows, and accelerated disruption curves in software and tech-enabled services.

Liquidity Terms

For semi-liquid products (interval funds, tender offer funds), valuation is no longer only about credit quality; it’s also about redemption queues, gating mechanics, cash buffers, and the manager’s ability to raise liquidity without disadvantaging remaining investors. When investors don’t trust liquidity management, they will discount the vehicle even if underlying assets are fine.

Practical Implications for Investors and Managers

Limited partners (LPs) and private wealth allocators should be prepared to compare marks to public comp moves and spread indices over the same period and ask why differences exist. Ask for detail on SaaS exposure breakdown (subsector, churn, retention, net revenue retention trends), non-accruals and internal risk ratings, use of third-party pricing/valuation agents, redemption management policies, and historical flow behavior.

General partners (GPs) should be prepared for more pushback on “model-based” marks without observable evidence, aggressive add-backs in EBITDA, and assumptions that refinancing will be easy. Managers should communicate early if changing valuation methodology, watchlist definitions, or liquidity management practices. GPs should be asking (as always) pertinent questions to portfolio companies on backlog and pipeline, especially in sectors that may be impacted by AI (e.g., SaaS). GPs should also understand how portfolio companies are using AI, such as whether it is being used just to lower costs and/or to create new strategic opportunities.

Bottom Line: Q1 2026 Reintroduced Correlation and Challenged the “Private” Premium

As of March 31, 2026, the biggest valuation takeaway is that private assets should be marked closer to the tempo of public markets. The Iran strike and energy shock raised macro uncertainty, Venezuela and Ukraine reinforced geopolitical instability, and the AI-driven reassessment of SaaS introduced a new fundamental risk for a sector that sits at the center of many private portfolios.

In that environment, the winners are the ones with:

- Transparent valuation governance

- Conservative underwriting assumptions

- Credible liquidity management

- Portfolio construction built for regime change, not just for benign markets

If you have questions about how market conditions should be reflected in your valuations, reach out to the professionals at Stout.

- Based on analysis performed by Stout with data obtained from CapitalIQ.