English

English

The Merger & Acquisition Environment

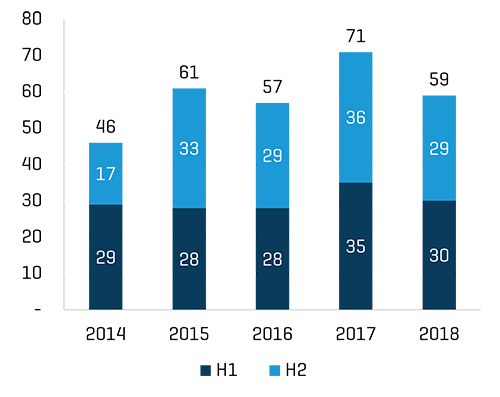

The fourth quarter produced notable transactions across each segment, bringing total transaction volume in line with 2015 – 2016 levels. While aggregate M&A dipped modestly versus 2017, various mega deals (both from larger strategic players and financial sponsors), coupled with ground-shifting trends industrywide (particularly within the wholesale segment, which saw a number of strategic alliances formed and industry leaders experiencing severe disruption as a result), made for a whirlwind year. As consolidation trends move deeper into “disruption” territory (e-commerce integration across the traditional brick and mortar retail and wholesale segments, joint ventures among the majors touching all segments, and new partnerships within the wholesale distribution segment), we expect steady acquisition activity in 2019, as strategic players and sponsors alike look to capitalize on the industry’s recent (and continued) reshaping.

For privately held businesses, valuations remain healthy, making a sale in the current environment a way to achieve full value. For family and entrepreneur business owners, reinvestment opportunities from sale proceeds continue to be a challenge (stocks seem expensive, bank deposits still pay very little, and bond yields remain relatively low). But this must be viewed holistically in line with higher valuations, which will typically more than compensate a seller for income lost in a low-interest-rate/high-asset-price environment – compensating a seller upfront as opposed to over time.

We hope you find our annual review informative, and we welcome the chance to engage with you in 2019.

Key Takeaways:

- Wholesale distribution landscape experienced significant disruption throughout 2018. The segment will continue to evolve in 2019 as the large, newly formed companies/joint venture entities integrate and jostle for position.

- Softer retail transaction activity was driven by retail consolidators, manufacturers, and new market entrants.

- Manufacturing segment sees further consolidation as large manufacturers acquire niche/specialty tire and wheel companies.

Historical M&A Trends by Period / Sector

Total Transaction Count

Note: Double-count of transactions which are included in multiple industry subsectors/categories, have been removed.

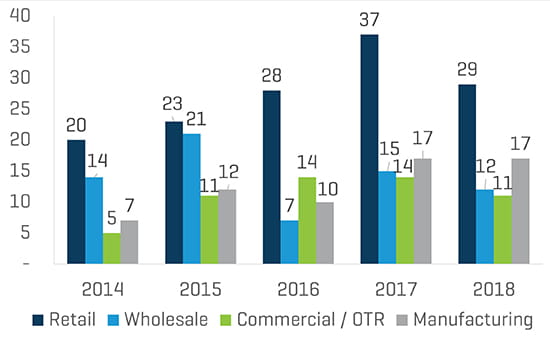

Transactions per Sector

Note: Double-count of transactions which are included in multiple industry sub-ectors/categories, have been removed.

Retail

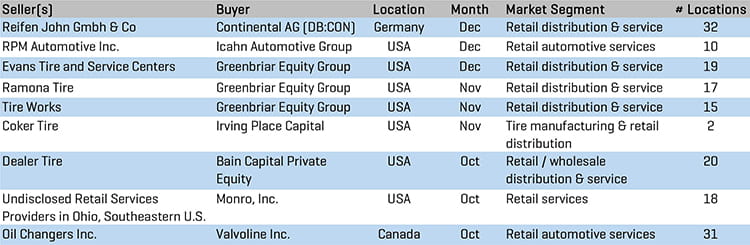

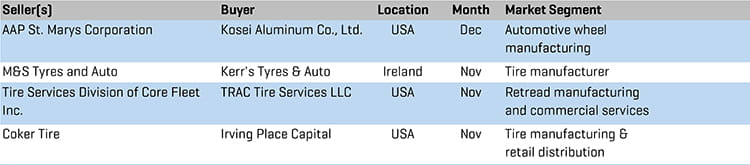

Retail M&A Transactions - Q4 2018

Greenbriar Equity Group

In the fourth quarter, Greenbriar Equity Group announced that it had made three recent acquisitions in the retail tire space: California-based Ramona Tire Inc., Evans Tire and Service Centers, and Nevada-based Tire Works Total Car Care. Greenbriar, a transportation-focused private equity firm, has added these most recently acquired businesses to its growing GB Auto platform, which now boasts more than 65 retail locations across the Southwestern U.S.

Icahn Automotive

Icahn Automotive Group announced its acquisition of Florida-based RPM Automotive in December. Operating with 10 locations across Florida, RPM complements Icahn’s existing footprint in the region and provides a platform for accelerated growth over the near term. Throughout 2018, Icahn has made a number of acquisitions, which have already been integrated under the Pep Boys, AAMCO, and Precision Tune Brands. The Icahn portfolio now includes over 2,000 owned and franchised service locations throughout North America.

Wholesale

Wholesale M&A Transactions - Q4 2018

Groupe Touchette, Inc.

In a move that further shifts the North American wholesale tire landscape, Groupe Touchette announced its acquisition of Ontario-based Atlas Tire Wholesale, Inc. in November. The acquisition extends the footprint of Canada’s largest tire distributor into the Ontario market, where Atlas currently operates three distribution centers with a fourth under construction. Post-acquisition, Groupe Touchette will operate with a workforce of about 750 employees across 35 distribution centers in Canada. The acquisition will increase storage capacity nearly 25%, and will augment the growth of the wholesaler within the Canadian distribution market.

Glide Buy Out Partners

European private equity firm Glide Buy Out Partners announced its acquisition of Gundlach Automotive Corporation (“GAC”) in November. Based in Germany, GAC is a leading distributor of tires, rims, wheels, and related services to car dealerships and wholesalers in the German market, as well as wheel assembly services provider to a number of blue-chip OEMs throughout Europe. Glide’s investment team seeks to position GAC as the “number 1 integrated player in the European tire and wheel distribution business.”

Bain Capital Private Equity

In October, Bain Capital Private Equity announced its acquisition of Dealer Tire, LLC., a national leader in replacement tire and parts distribution, based out of Cleveland. A family business founded in 1999, Dealer Tire manages replacement tire and parts programs for more than 20 automotive OEMs in the U.S and China, and serves more than 10,000 automotive dealerships from nearly 40 distribution centers across the U.S. Dealer Tire has made a number of strategic moves in 2018 to expand its platform, including investments in Tyrata, Inc., a tire sensor and data management company, and SimpleTire, LLC, an online marketplace facilitating web-based tire sales. Through its investment, Bain will look to further expand Dealer’s platform to support dealers, OEMs, tire manufacturers, and web-based customers.

Commercial/OTR

Commercial/OTR M&A Transations - Q4 2018

Border Tire

In October, Border Tire, a Texas-based commercial tire dealership and retreader, announced its plans to acquire five TCi Tire Centers plus one retreading plant from Michelin. The deal covers the last remaining TCi assets in California. Border furthers its expansion westward through the acquisition, and hopes to provide residents, agricultural industry players, and truck drivers access to premium products and services throughout the Southwestern U.S. Michelin has now divested or closed 51 TCi commercial sales locations and eight retread plants since the beginning of 2017.

TRAC Tire Services LLC

TRAC Intermodal announced in November 2018 that it had acquired assets relating to the tire services division of Core Fleet, Inc., a Kentucky-based commercial tire and automotive services provider. TRAC Intermodal, through its newly formed subsidiary, TRAC Tire Services LLC, will operate out of a brand new 102,000-square-foot facility that will accommodate both a production facility, warehousing and storage space, and various other administrative functions. The acquisition will allow TRAC to provide wholesale, parts distribution, retreading, and related services to the intermodal and commercial trucking industries.

Manufacturing

Manufacturing M&A Transactions - Q4 2018

Irving Place Capital

In November, Irving Place Capital announced its acquisition of Tennessee-based Coker Tire. A leading manufacturer of collector car and motorcycle wheels and tires, Coker has experienced significant growth and profitability in recent years under the direction of its current leadership team, who tapped Irving Place Capital for support during the buyout. Irving Place Capital is an active investor in the automotive aftermarket.

Kerr’s Tyres & Auto

Kerr’s Tyres & Auto, a Northern Ireland-based tire services provider, announced its acquisition of tire manufacturer M&S Tyres, in November. Kerr’s believes the acquisition will strengthen its regional coverage throughout Northern Ireland and broaden its service offering. Management also noted that there are substantial opportunities for consolidation within the industry, and will be looking for avenues to continue to grow the business.

2018 M&A Transactions by Segment & 2019 Forecasts

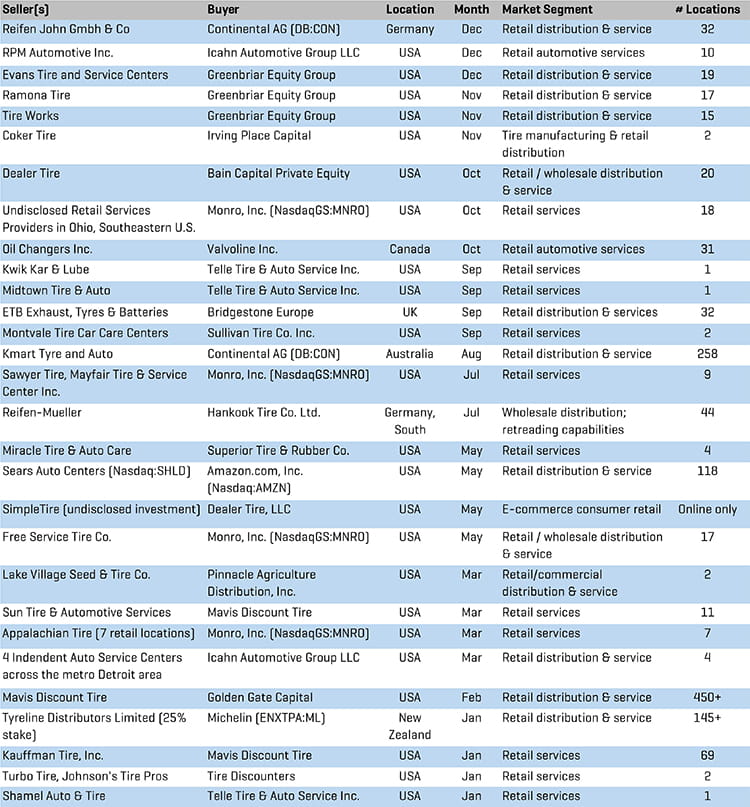

Retail: Though still a strong year for retail M&A, the 2018 transaction count fell back into line after experiencing heavier than usual activity in 2017. The drivers for continued consolidation in the space remain largely unchanged – soft organic growth being offset by accretive acquisitions of contiguous retail networks, significant private equity and institutional investor involvement in the retail sector, and attainable synergies when combining retail networks.

The U.S. was by far the busiest market for retail M&A globally, with honorable mentions for activity in the U.K., Australia, and Germany.

Retail Forecast 2019

- Look for consolidation activity to continue at a steady pace in 2019, as the strong rate of annual transaction volume moderates.

- We expect continued integration of e-commerce into both the physical retail and wholesale segments, as total market access further integrates with the regional install base.

- There remains potential for large, transformative deals as the big retailers look to expand and consolidate footprints, and regional, privately held companies take advantage of the current M&A environment. This may be driven further by the lack of succession planning in many family- and entrepreneur-owned retailers combined with a favorable deal environment.

Retail M&A Transactions - 2018

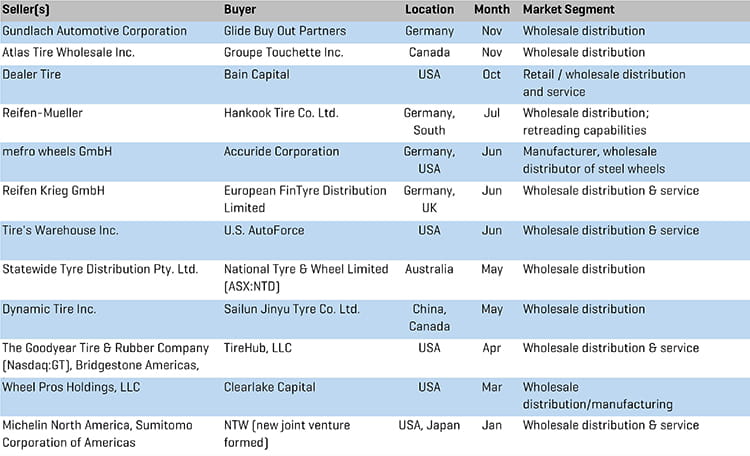

Wholesale: Wholesale transaction volume dipped modestly compared with 2017 activity. Transaction drivers for the year included enhanced regional presence from strategic players (with joint venture activity changing the landscape significantly), as well as financial sponsors seeking to capitalize on macro shifts in the broader wholesale landscape.

Transaction activity was global in its scope, with notable names in the U.S., Europe, and Asia changing hands.

Wholesale Forecast 2019

- Look for regional consolidation activity to continue in North America as wholesalers with $150 million in revenue or less continue to be absorbed, while there remains potential for one or more large/transformative transactions (more than $200 million in revenue) as the upper end of the market seeks opportunities to offset flat to slow organic growth with M&A, and attain the benefits of added scale.

- As forecast in our 2017 report, we expect manufacturers will continue to stick with their core business and create alliances, joint ventures, and other arrangements to increase product availability and achieve greater scale and control over the wholesale channel.

Wholesale M&A Transactions - 2018

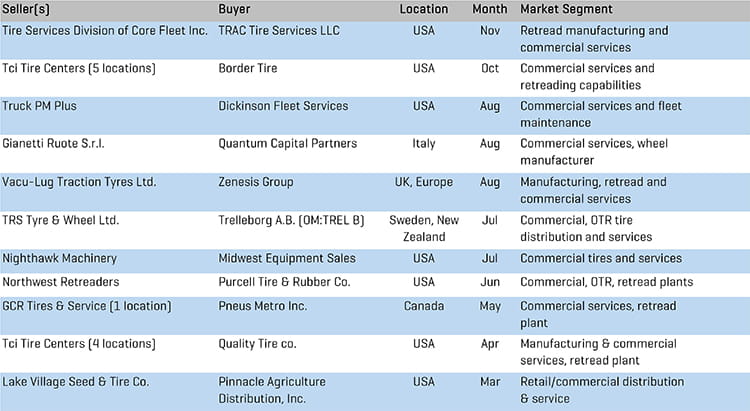

Commercial/OTR: In a modest year for M&A, the commercial/OTR segment saw the continued wind-down of Michelin’s TCi Tire Centers to qualified regional players in the U.S., as well as activity both domestically and abroad from strategic players, with limited private equity involvement.

Commercial/OTR Forecast 2019

- Look for travel center operators to continue to actively expand retread and commercial distribution/service offerings organically and via acquisition

- Regional consolidation by the strong midsize players

Commercial/OTR M&A Transactions - 2018

Manufacturing: Transaction activity in 2018 remained consistent with prior-year levels, with notable transactions in the segment coming from Michelin in its acquisition of Camso, and from Kumho, which sold a significant equity stake in its business earlier this year in order to avoid bankruptcy.

Manufacturing Forecast 2019

- Look for manufacturers sticking to targeting core manufacturing operations, targeting specialty manufacturers for acquisition, and initiating/expanding partnerships with distribution networks of scale

- We expect continued pursuit of specialty manufacturers and brands by the top 10 global companies

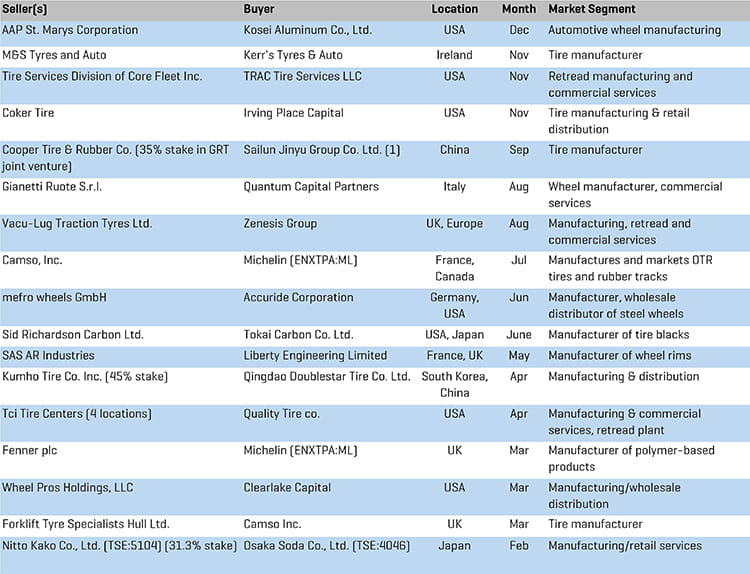

Manufacturing M&A Transactions - 2018

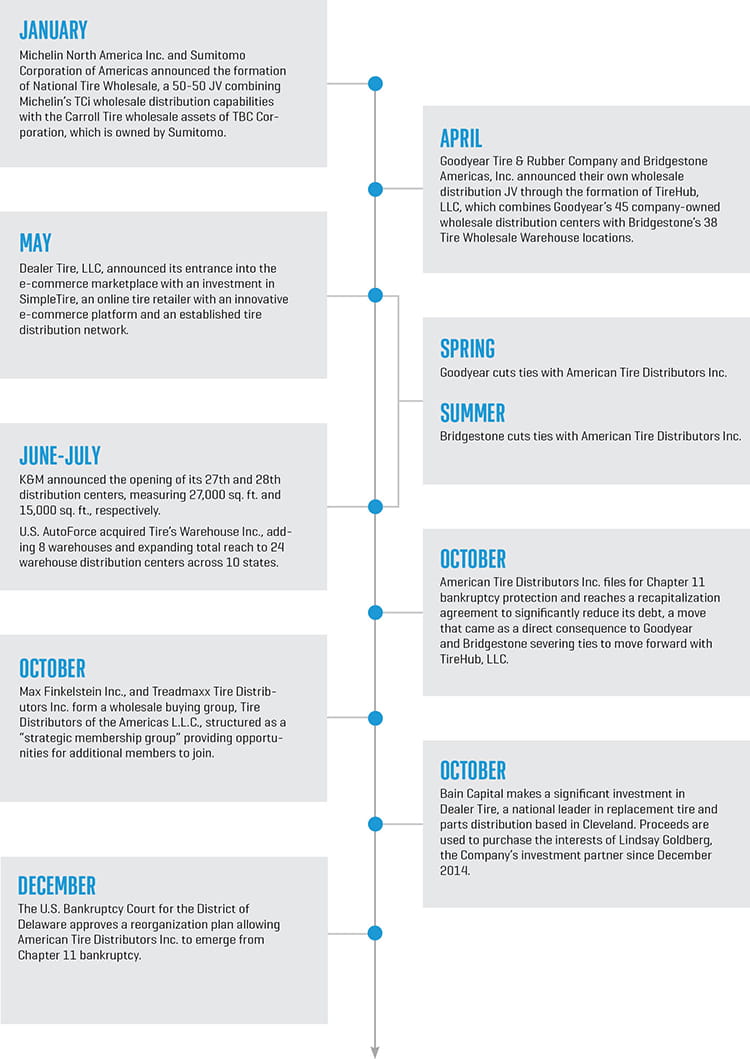

2018 Featured Theme: Wholesale Disruption

2018 produced tectonic shifts, several of which have materially changed the wholesale tire landscape, both in the U.S. and internationally. In addition to robust M&A activity (highlighted throughout this report, as well as in our Q1, Q2, and Q3 2018 reports), the wholesale segment experienced significant, fundamental changes, such as:

- large manufacturers, traditional competitors, and regional distributors alike established partnerships that seemed unlikely in prior years

- traditional, long-term supply partnerships were canceled, driving the industry leader into restructuring mode and presenting opportunity to regional wholesale partners of Goodyear and Bridgestone

- in response, retailers changed and/or added suppliers

- in seeking ways to stay ahead of the technology curve, enhance margin, and enhance control of the channel and pricing, moved into the retail e-commerce marketplace via strategic acquisitions.

The timeline below highlights select major events within the wholesale tire segment in 2018: