English

English

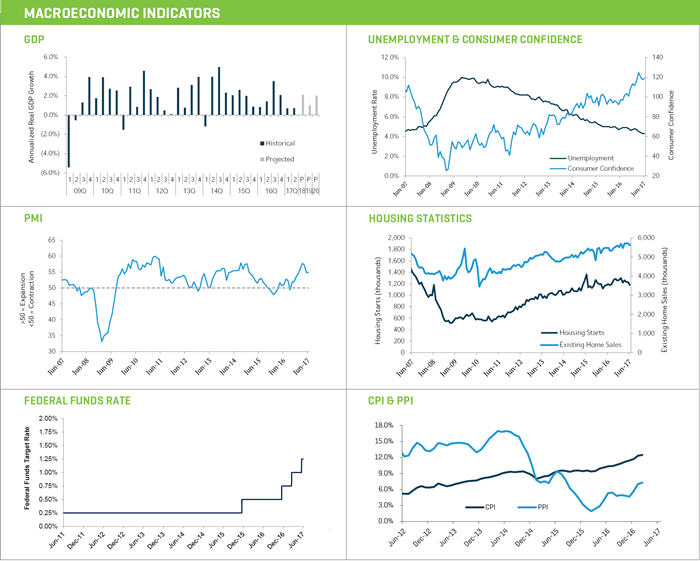

Senate Republicans are having difficulty garnering enough votes to pass The Better Care Reconciliation Act (BCRA) of 2017, which is likely a result of the Congressional Budget Office (CBO) forecasting that the bill would: 1) leave 22 million Americans without health insurance, and 2) curtail Medicaid expansion. The House version of healthcare reform, the American Health Care Act (AHCA), had passed the House May 4, 2017.

As of this writing, it looks like Senate Republicans may be giving up on replacing Obamacare for now and will attempt to repeal the Affordable Care Act with a two year transition period to avoid disrupting the insurance markets. This approach will provide time to replace Obamacare with a better bill that is thoughtfully debated in consideration of all facts and constituents. A new healthcare bill and its repeal of elements of the Affordable Care Act (ACA) can be passed with a simple majority of the Senate as long as it complies with the budget reconciliation rule.

A repeal of the ACA would still curtail Federal Medicaid funding and expansion and eliminate the mandate that individuals purchase insurance or that employers provide insurance. It would also repeal tax increases that the ACA had established for the federal government to subsidize state Medicaid programs and their expansion. The move to repeal may put pressure on democrats to come to the table to negotiate a replacement as repeal could lead to loss of coverage or premium levels for persons with pre-existing conditions for example.

Repeal could also mean that states could waive mandated coverage of essential health benefits defined by the Affordable Care Act, such as behavioral health benefits, and could remove a ban on insurance companies placing lifetime caps on benefits. In general, the legislative direction seems to be to push more of the responsibility for who and what is covered back onto the states and their respective insurance agencies.

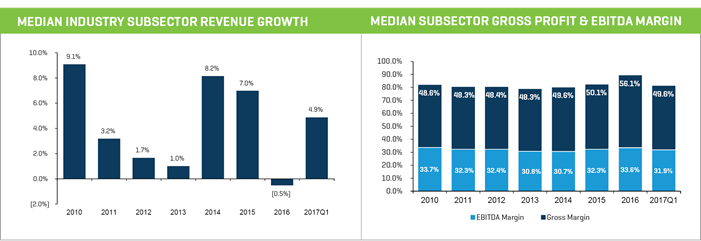

Recent Healthcare & Life Sciences Trends

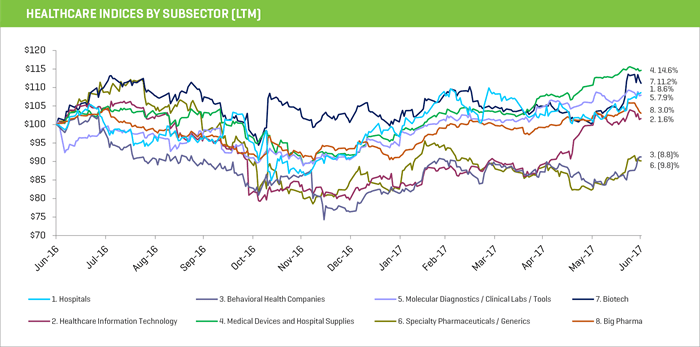

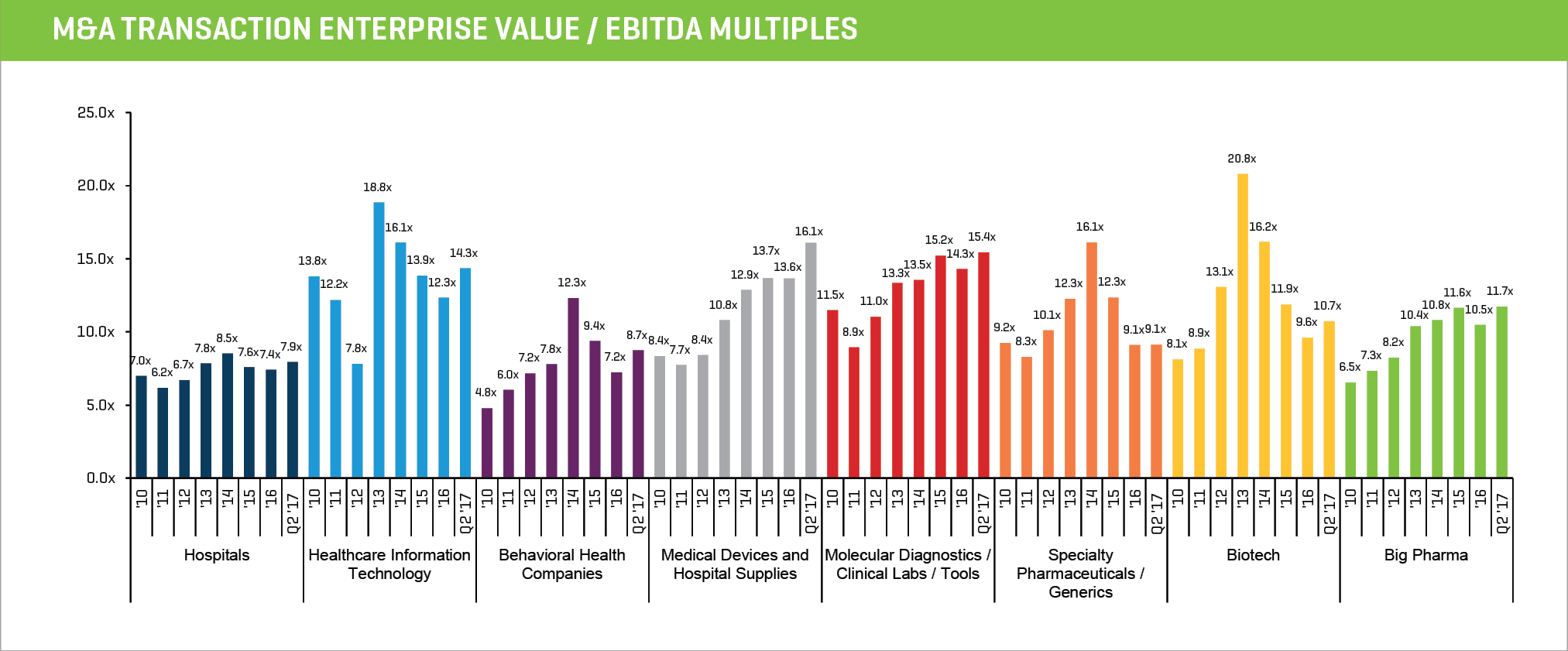

BIOTECH – CONTINUED STRONG PERFORMANCE

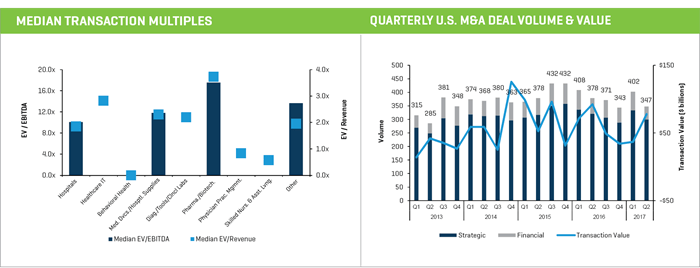

Big Biotech has been a market performer over the last year, up 11.2% in our index, and has rallied with the market since April and May. Big Pharma continues to selectively buy up oncology therapeutics, in some cases in Phase 1 or Phase 2, which is encouraging. The average premium has been 50% to the prior day’s close with respect to a broad list of M&A transactions in biotech. Funding continues to be a challenge for smaller biotechs as investors have derisked with the market at higher valuation levels and the IPO market window remains tight.

Smaller biotechs continue to focus on oncology as the large, expensive trials for cardiovascular, CNS (major depressive disorders), and diabetes drugs have relegated them to the domain of Big Pharma.

Investor interest has been focused on immuno-oncology drugs such as PD-1 inhibitors, PD-L1 inhibitors, CTLA-4 inhibitors, and Car T-Cells, where there have been some promising clinical and commercial results. This has largely been the domain of big pharma (Merck, Pfizer, BMS, Astrazeneca, Roche/Genentech, etc.), but smaller biotechs like Kite and Juno are also benefiting from investor enthusiasm for immuno-oncology. Therapeutics for NASH (nonalcoholic steatohepatitis) and anti-infectives/antibiotics continue to be other areas of interest.

HOSPITALS – SHIFTING TO VALUE-BASED REIMBURSEMENT

Hospitals and other healthcare service providers will continue to face reimbursement pressures. They will need to deliver better risk-adjusted health outcomes while operating more cost efficiently to maintain profitability under the value-based payment model put into place by the Affordable Care Act and Medicare Access and CHIP Reauthorization Act of 2015 (MACRA).

These laws will provide incentive payments for providers that achieve better health outcomes at a lower cost. The MACRA law only impacts Medicare payments, but commercial payors are following this lead with risk-sharing contracts with providers.

This shift to value-based reimbursement from traditional fee for service (volume-based) will require integrated healthcare systems to better coordinate with physicians and post-acute facilities to manage outcomes and costs. It may also lead to further industry consolidation.

Integrated healthcare service providers are pursuing alternative payment models with commercial payors, such as bundled payment systems (shared savings and shared risk), to improve health outcomes and optimize reimbursement and revenue, while reducing costs associated with readmissions or lengths of stay. This is also likely to lead to further industry consolidation among hospitals, physician groups and other service providers. Managing payor mix, services offered, system providers, and delivery settings will all be important. Having technology and analytics that can evaluate important revenue and cost variables will be critical, hence the high level of strategic and private equity interest in digital health.

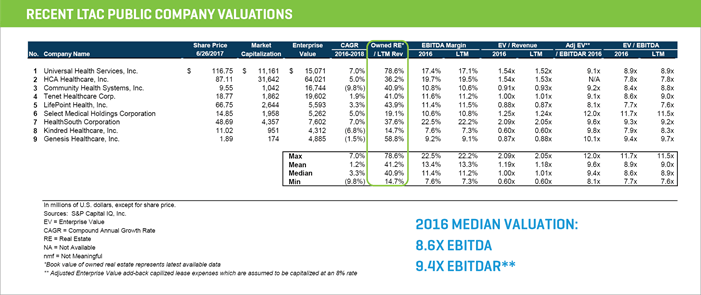

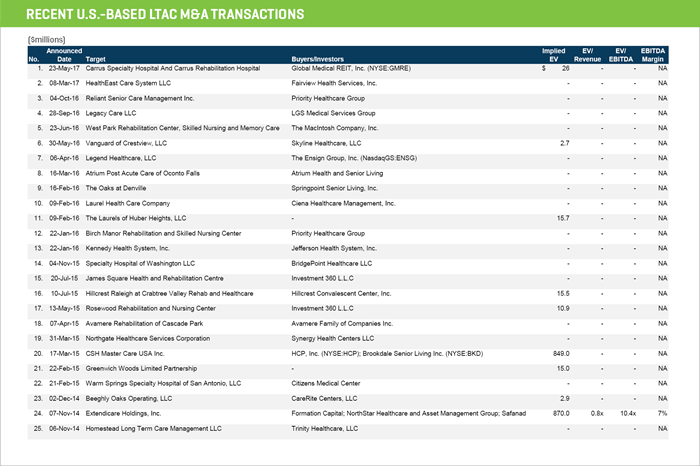

LONG-TERM ACUTE CARE HOSPITALS

Hospital stocks were up 8.6% versus a year ago in our index. This is likely a function of stock market performance and moderating concerns about overly disruptive healthcare reform changes.

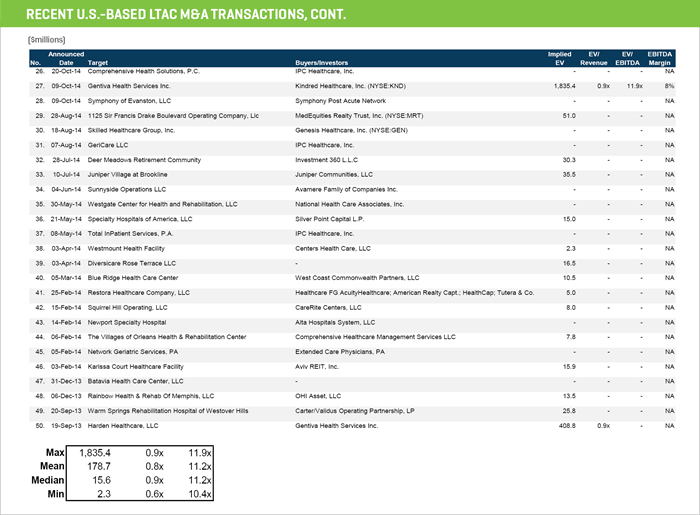

Long-term acute care hospitals (LTACs), a subsegment in which companies like Kindred Healthcare compete, have been confronted by reimbursement changes that lower reimbursement for patients who were referred from an acute care hospital but were not in an ICU, cardiovascular ward, or on a ventilator for 96 hours. This has forced some LTACs to restructure their business models, operations, and debt to survive. In fact, recent bankruptcy filings blame the Medicare rule changes.

Investors have been concerned that many LTACs lease their properties from REITs and could be adversely impacted by escalating rents when revenue per patient is declining. M&A activity in this segment remains active, but it is predominantly strategic acquirers involved and not private equity, which is consistent with what we hear from private equity firms. They are and have been concerned about the reimbursement outlook for LTACs and regular acute care hospitals as well.

HEALTHCARE INFORMATION TECHNOLOGY – A DYNAMIC AND EMERGING LANDSCAPE

With the healthcare payment system transitioning from volume-based fee for service to value-based reimbursement, healthcare providers will need greater and different healthcare information tools and analytics to truly understand how to get superior outcomes at the lowest cost.

This will be critical if they want to secure greater revenue-sharing rewards from payors and boost their own revenue and profitability. A better understanding of which procedures and physicians have the best cost-based outcomes will be vital. Value-based reimbursement is designed to rein in spiraling healthcare costs for the nation, and reimbursement pressures on providers will continue for the foreseeable future. Thus, they will need to learn to operate their Medicare business efficiently and be strategic in managing their commercial mix of services, as well.

Healthcare Information Technology encompasses an eclectic group of companies or subsegments and represents an exciting segment that is destined to grow rapidly and also see a lot of consolidation activity. New coding requirements imposed by the Affordable Care Act and MACRA will mean changes to billing systems and will impact revenue cycle management. Telemedicine is an exciting opportunity where reimbursement is expanding, new business models are emerging, and companies like TelaDoc and Plushcare compete. Precision medicine, where a patient’s treatment is tailored to their personal genetic profile, will grow, along with bioinformatics as sharing of data-intensive records among providers will be necessary. Electronic medical records and their security are an element of the equation, as well.

Some other segments of interest include online health insurance providers and companies that help pharmaceutical companies target prescriptions to physicians and their patients.

BEHAVIORAL HEALTH - A LARGE, GROWING, AND UNDERSERVED MARKET

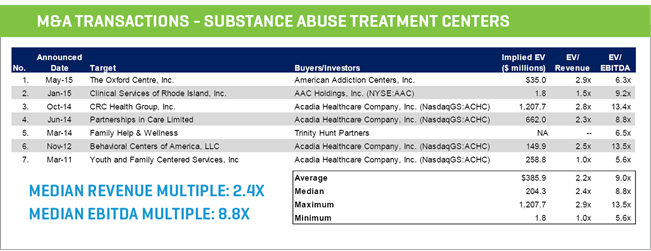

Behavioral health broadly, and substance abuse treatment centers specifically, remains one of our favorite segments for investment. We see this profitable and fragmented industry growing as the opioid epidemic and regulatory changes and public policy drive growth in covered lives and treatment service options.

M&A activity in the substance abuse treatment center industry is bouncing back in 2017 after a lull in 2016. We are getting a lot of private equity and strategic interest in geographic rollup strategies. An increase in reimbursement and eligibility for state Medicaid programs began its rollout in the second quarter of 2017, but it will be interesting to see what happens if the ACA is repealed. This could potentially be very disruptive for the industry, as could the elimination of essential healthcare benefits. However, our view is that this is an underserved market and that periodic weakness in the sector may just be an opportunity to invest in what looks to be a growing industry for many years to come.

Interested in learning more about the latest behavioral health trends? We recently published a special report filled with timely, data-rich insights relating specifically to substance abuse treatment.

MEDICAL DEVICES AND HOSPITAL SUPPLIES – SLOWED GROWTH BUT PROMISING NEW ENTRANTS

Medical device stocks have been the top performer in healthcare, up 14.6% from a year ago on strong financial performance and some large acquisitions at premium prices, such as the Becton Dickinson purchase of C.R. Bard. The medical device segment has seen growth and innovation slow somewhat from the early adoption of minimally invasive surgery, interventional cardiology, neuroradiology, Botox and Restylane, breast implants, and cervical and lumbar discs. But there continues to be exciting areas of growth and/or promise in diabetes (insulin pumps and continuous glucose monitoring), robotic surgery, structural heart disease (transcatheter valves), exoskeletons, aesthetic medicine (body contouring), presbyopia (Acu-focus, Glaukos, Presbyia and Revision Optics) and sensors/remote monitoring.

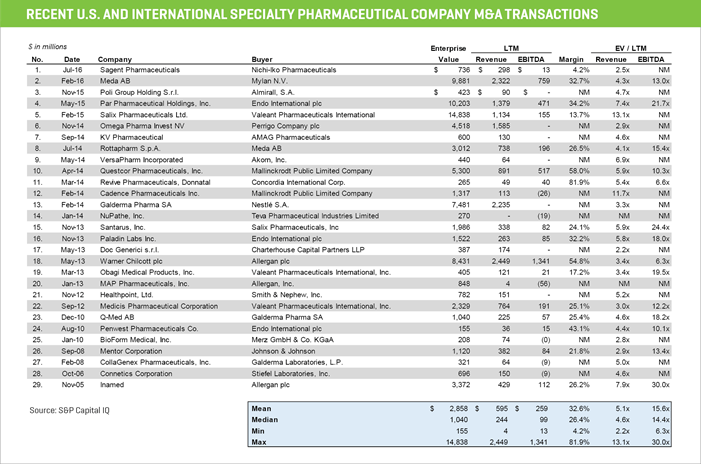

SPECIALTY PHARMACEUTICALS/GENERICS – CONTINUED FOCUS ON PRICING

Valeant/Philidor and the Turing Pharmaceuticals fiascos have done this group no favor, as it has put pricey reformulated drugs in the crosshairs of regulators, patient advocacy groups, and payors alike. Well-publicized attacks on Mylan over the EpiPen pricing and Mallinckrodt have also put pressure on the group, and actually led to discounting. Endopharmaceutical’s withdrawal of pain medication Opana from the market at the request of the FDA has also been a negative for the stocks. Specialty pharma has been the worst performer among our indices, down 9.8% from a year ago.

MOLECULAR DIAGNOSTICS/CLINICAL LABS/TOOLS – LARGE LABS ARE EXPECTED TO DOMINATE

It’s going to be tough for smaller molecular diagnostic labs to compete going forward. Only those with proprietary specialized tests for a subspecialty (for example, central nervous system disorders) are likely to survive on their own. As a result, we have seen consolidation that will likely continue. It will be a daunting task to compete with large, well-heeled CLIA labs and/or instrument manufacturers, such as Roche/Foundation Medicine or NantHealth, that have now developed much more sophisticated biomarker tests that look at a broad range of oncogenes designed for precision or personalized diagnostics.

Reimbursement cuts have hit areas like pharmaco-genomics hard, but those are areas that seem quite promising for the future. Personalized diagnostics (matching the right drug or drug combination to the right patient based on genetic profile) are the future, so this is an emerging area of interest. Manufacturers like GenMark are moving respiratory diagnoses to the point of care, and this model seems to be working.

BIG PHARMA – GLOBAL MIX OF BUSINESS AND PATIENT DEMAND SHOULD DRIVE CONTINUED GROWTH

The Trump Administration threats to put drugs out for bid for Medicare, concerns about many having domiciled outside the U.S., and patent expirations continue to dog this group. But they continue to chug along in the stock market (up 3% from a year ago) given their volume growth, stability, global market position, and proprietary drugs and development pipelines.