English

English

When thinking about the energy landscape in 2025 and beyond, a clear inflection point for the oil and gas industry lies ahead in the form of the November 2024 presidential election. Two significantly different outcomes are possible depending on the election results.

2025 Democratic Administration: More of the Same?

Since taking office in 2020, the Democratic candidate Joe Biden has implemented policies to reduce fossil fuel production and increase reliance on renewable energy sources. These policies included halting new oil and gas leases on federal lands, increasing royalty and bonding rates for producers, and blocking the Keystone XL pipeline project. The results of these changes on the industry have increased oil prices and limited new exploration efforts for producers. Although a significant component of the current rate of inflation, higher prices to fuel gasoline and diesel-powered vehicles also make electric vehicles more affordable, in comparison.

Given this administration’s continued focus on climate change, it is reasonable to assume similar policies would be implemented/maintained during a second term.

2025 Republican Administration: A Return to “Drill Baby Drill”?

Republican candidate Donald Trump has revived the “drill, baby, drill slogan, using it to advocate for increased domestic oil and gas production.1 While serving as President from 2016 – 2020, Trump’s administration did the following:

- Emphasized increasing domestic fossil fuel production, including oil and gas, to achieve energy independence

- Rolled back environmental regulations seen as obstacles to oil and gas extraction and transportation

- Supported projects like the Keystone XL and Dakota Access pipelines to expand oil and gas infrastructure

- Withdrew the U.S. from the Paris Agreement, reducing focus on climate change and emissions reduction2

2023 Sources of Cash for Big Oil

In order illustrate the potential effect on oil and gas producers, I selected a group of five large domestic oil companies (“Big Oil”), all with sales in excess of $10 billion in 2023:

Company |

2023 Sales |

|---|---|

|

$ Billions |

|

|

1. Exxon Mobil Corporation |

$338.3 |

|

2. EOG Resources, Inc. |

$23.3 |

|

3. Chevron Corporation |

$194.8 |

|

4. Hess Corporation |

$10.3 |

|

5. ConocoPhillips |

$57.9 |

During 2023, oil prices averaged about $78 per barrel, as indicated by the West Texas Intermediate (WTI) spot prices. For that time period, the selected companies reported positive cash flows from operations of between approximately $27 and $41 per barrel of oil equivalent (BOE) produced.

Company |

2023 Operating Cash Flow

|

|---|---|

|

$ Billions |

|

|

1. Exxon Mobil Corporation |

$40.58 |

|

2. EOG Resources, Inc. |

$31.54 |

|

3. Chevron Corporation |

$31.26 |

|

4. Hess Corporation |

$27.42 |

|

5. ConocoPhillips |

$29.95 |

|

Average |

$32.15 |

In round numbers, this shows that during 2023, when oil prices averaged about $78 per barrel, the group of large oil companies was able to produce about $32 of cash flow, per barrel, for the same time period.

So what did these companies do with these net cash flows? The following table shows the net amount each company invested (leases acquired, wells drilled and completed) in 2023:

Company |

2023 Investment

|

|---|---|

|

$ Billions |

|

|

1. Exxon Mobil Corporation |

$14.13 |

|

2. EOG Resources, Inc. |

$17.63 |

|

3. Chevron Corporation |

$13.37 |

|

4. Hess Corporation |

$28.61 |

|

5. ConocoPhillips |

$18.00 |

|

Average |

$18.35 |

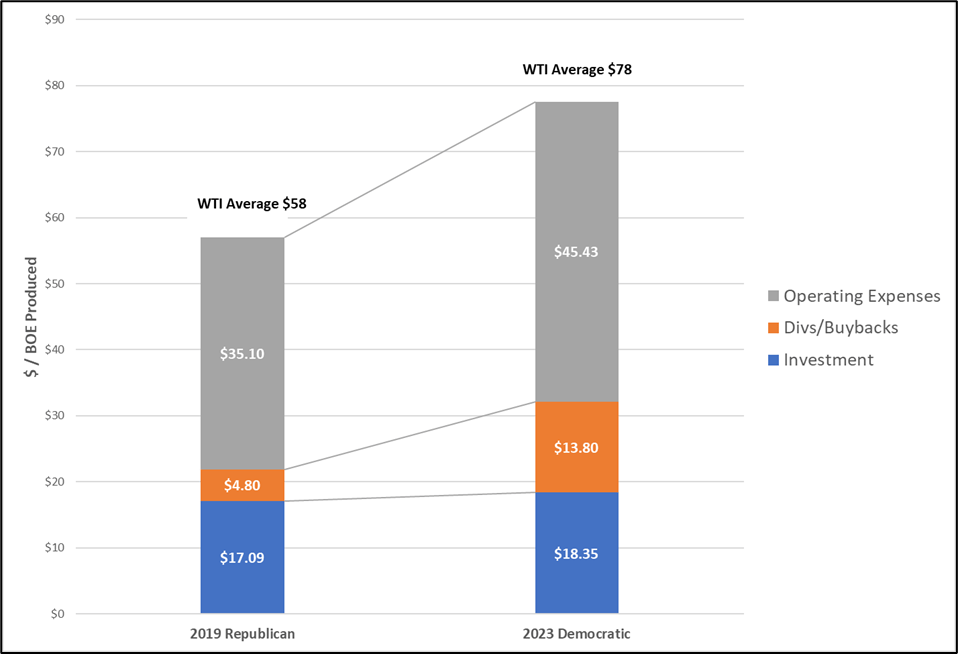

The difference between the $32 of cash flow per barrel produced and the $18 per barrel of cash flow reinvested, approximately $14 per barrel, was primarily returned to equity investors in the form of both dividend payments and stock buybacks. In percentage terms, this means that 56% of the operating cash flow was reinvested, and 44% was returned to shareholders and creditors.

Republican Administration Lookback: Fiscal Year 2019

To provide a comparison to the oil industry under the current administration, I examined the same factors for the same group of companies. During 2019, oil prices averaged about $57 per barrel, as indicated by the WTI spot prices, about $21 per barrel less. In 2019, the selected companies created positive cash flows from operations of between approximately $14 and $27 per BOE produced.

Company |

2019 Operating Cash Flow

|

|---|---|

|

$ Billions |

|

|

1. Exxon Mobil Corporation |

$20.60 |

|

2. EOG Resources, Inc. |

$27.33 |

|

3. Chevron Corporation |

$24.47 |

|

4. Hess Corporation |

$14.47 |

|

5. ConocoPhillips |

$22.58 |

|

Average |

$21.89 |

In round numbers, this shows that under the Trump administration in 2019, the group of large oil companies was able to produce about $22 of cash flow per barrel, or about $10 per barrel less than in 2023.

Given that cash amounts generated from operations were less, what about investing during the same period? The following table shows the net amount each company invested (leases acquired, wells drilled and completed) in 2019:

Company |

2019 Investment

|

|---|---|

|

$ Billions |

|

|

1. Exxon Mobil Corporation |

$16.00 |

|

2. EOG Resources, Inc. |

$20.68 |

|

3. Chevron Corporation |

$10.26 |

|

4. Hess Corporation |

$25.05 |

|

5. ConocoPhillips |

$13.46 |

|

Average |

$17.09 |

The difference between the $22 of cash flow per barrel produced and the $17 per barrel of cash flow reinvested, approximately $5 per barrel, provided much less cash with which to pay dividends and repurchase shares. Also, under the Trump administration, interest rates were lower, making debt an attractive financial source of funds. In percentage terms, this means that in 2019 over 77% of the operating cash flow created was reinvested, and only 23% was returned to shareholders and creditors.

Key Takeaways

There has been a very different macroeconomic environment for oil producers under the two administrations. Between 2019 and 2023, oil prices increased by approximately $20 per barrel. Operating costs experienced by operators increased over the same period by about $10 per barrel, reflecting the increased demand and reduced supply of equipment, materials, and oil field labor.

Even as oil prices increased by $20 per barrel and operating cash flows increased by $10 per barrel, the industry saw expenditures for new wells (drilling, completion, etc.) increase by only one dollar per barrel between 2019 and 2023. The remaining cash flows created were then paid out to shareholders in the form of higher dividends, special dividends, and share buybacks.

Republican (2019) and Democratic (2023) Comparison

Looking Ahead

As investors and company leaders look ahead to 2025 and beyond, the results of the 2024 election will impact the ultimate outcome. If President Biden is re-elected to a second term, “more of the same” is a reasonable expectation: in other words, higher prices, lower drilling, and increased focus on reducing the use of fossil fuels, again focusing on combating climate change.

However, if Republican candidate Trump is elected again, one could expect lower prices, higher volumes, and potentially lower interest rates if interest rates fall given the lower inflation impact of lower oil prices for the country.

A third consideration is that current higher payout rates (returning capital to shareholders via dividends and stock buybacks) in recent years have been driven by investors previously burned by E&P company bankruptcies and poor shareholder returns during the 2010 to 2019 drilling boom, and potentially not the result of executive policies.

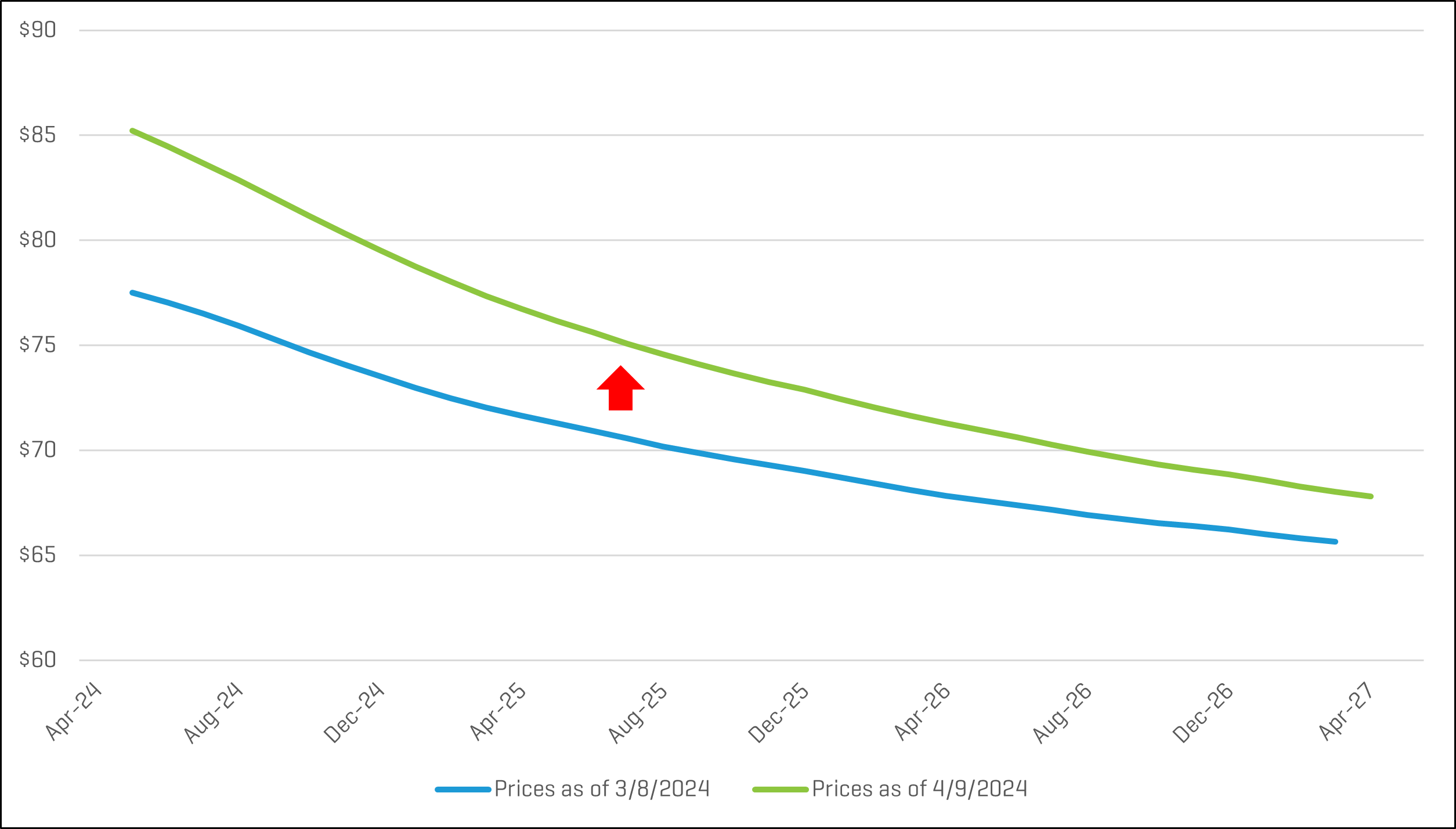

WTI Strip Prices Increase

Spot prices and futures prices for the WTI contract increased by approximately $7.75 per barrel in the near term and increased approximately $2.50 in the longer term futures prices.

WTI Strip Prices – One Month Change

As shown, the oil price curve remains in a state of “backwardation,” reflecting the market’s expectation of lower future spot prices.

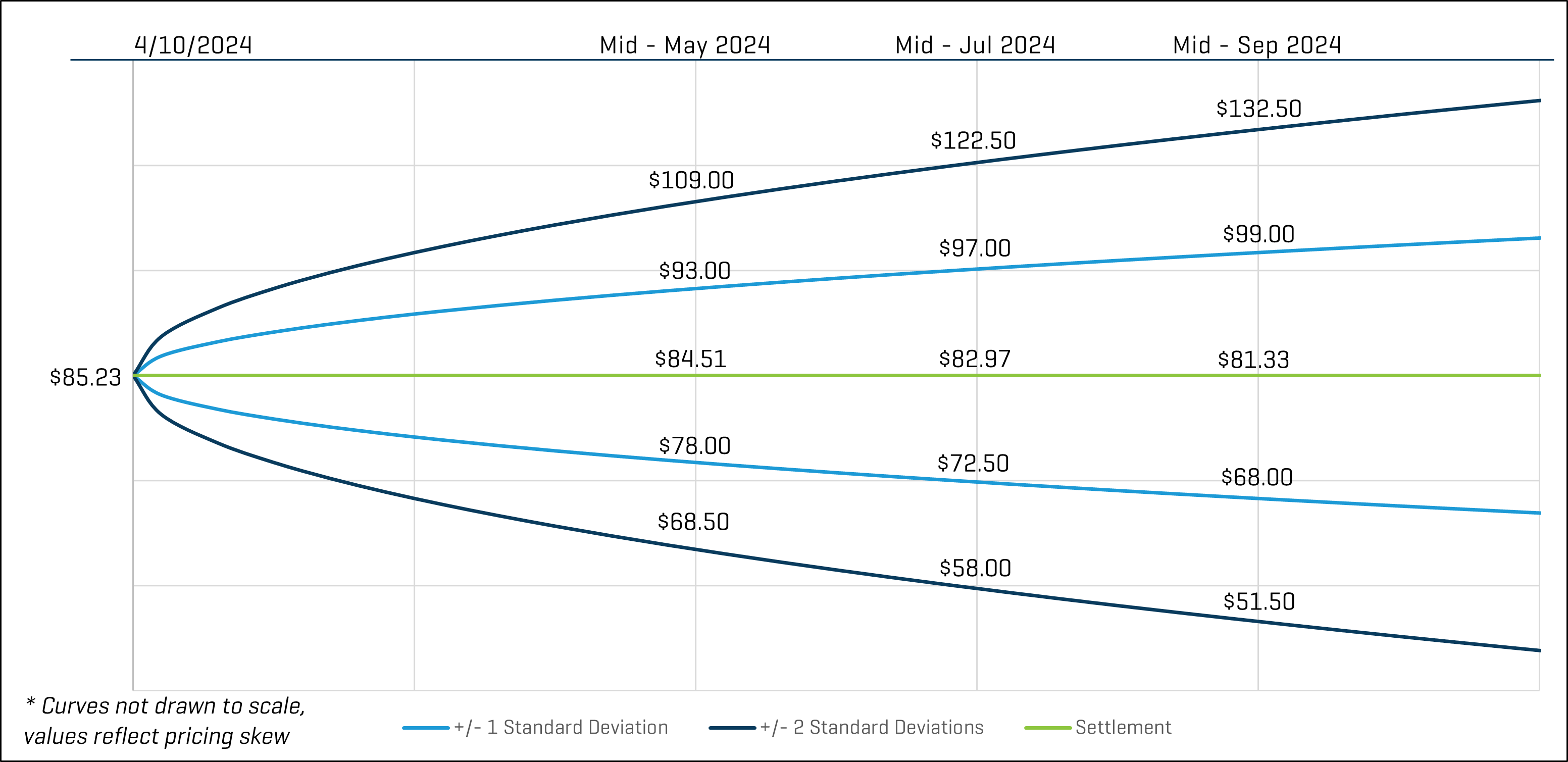

Oil Price Outlook

The price distribution below shows the crude oil spot price on April 10, 2024, as well as the predicted crude oil prices based on options and futures markets. Light blue lines are within one standard deviation (σ) of the mean, and dark blue lines are within two standard deviations.

WTI Crude Oil $/BBL

Based on these current prices, the markets indicate there is a 68% chance oil prices will range from $72.50 and $97.00 per barrel in mid-July 2024. Likewise, there is roughly a 95% chance that prices will be between $58.00 and $122.50. By mid-September 2024, the one-standard deviation (1σ) price range is $68.00 to $99.00 per barrel, and the two-standard deviation (2σ) range is $51.50 to $132.50 per barrel.

Key Takeaways

Remember that option prices and models reflect expected probabilities, not certain outcomes, but that does not make them any less useful. Throughout most of 2023 and 2024, crude oil spot prices have primarily fluctuated within the range of $70 to $90 per barrel. During that time, we observed general increases in futures price volatilities as prices neared the upper bound of that range, as evidenced by the futures price ranges observed. For mid-September 2024 pricing as of April 10, 2024, the 1σ range had a spread of $31.00 per barrel, and the 2σ range has a spread of $81.00 per barrel. For comparison, in 2022, we observed 1σ and 2σ price ranges in excess of $65.00 and $150.00, respectively.

- The “drill, baby, drill” slogan was first used by former Maryland Lieutenant Governor Michael Steele at the 2008 Republican National Convention. Steele coined the phrase to express support for increased domestic drilling for oil and gas as a way to reduce U.S. dependence on foreign energy sources. The slogan was then also prominently used by Republican vice presidential nominee Sarah Palin during the 2008 vice presidential debate.

- “A Comparison of Biden and Trump Energy Policies: Priorities and Impacts,” Gusti Ngurah Krisna Dana, Modern Diplomacy, April 27, 2023.