English

English

The term “BOE” (or “barrel of oil equivalent”) provides a standardized way to compare the energy content and economic value of different hydrocarbon products, including oil, natural gas, and natural gas liquids. The formula for calculating the barrel of oil equivalent (BOE) considering oil, natural gas liquids, and natural gas is:

BOE = Oil (barrels) + Natural Gas Liquids (barrels) + (Natural Gas [cubic feet] × Conversion Factor)

The conversion factor used to convert natural gas from cubic feet to BOE varies depending on the energy content of the natural gas and the energy density of the crude oil used as a reference.

The factors affecting the conversion factor are:

- Energy Content: One barrel of crude oil contains approximately 5.8 million British Thermal Units (BTU) of energy, while one thousand cubic feet (Mcf) of natural gas contains approximately 1 million BTU of energy.

- Ratio: By dividing the energy content of one barrel of crude oil (5.8 million BTU) by the energy content of one Mcf of natural gas (1 million BTU), we get a ratio of approximately 5.8.

- Rounding: For simplicity and standardization, the ratio of 5.8 is often rounded up to 6.

Therefore, one Mcf of natural gas is considered equivalent to approximately 1/6 of a barrel of crude oil in terms of energy content. The BOE conversion factor allows companies and analysts to express the combined energy output from both oil and natural gas production in a single unit, making it easier to compare and analyze energy production across different sources.

Historical Review

As a starting point for our analyses, we considered commodity prices back to the year 2000.

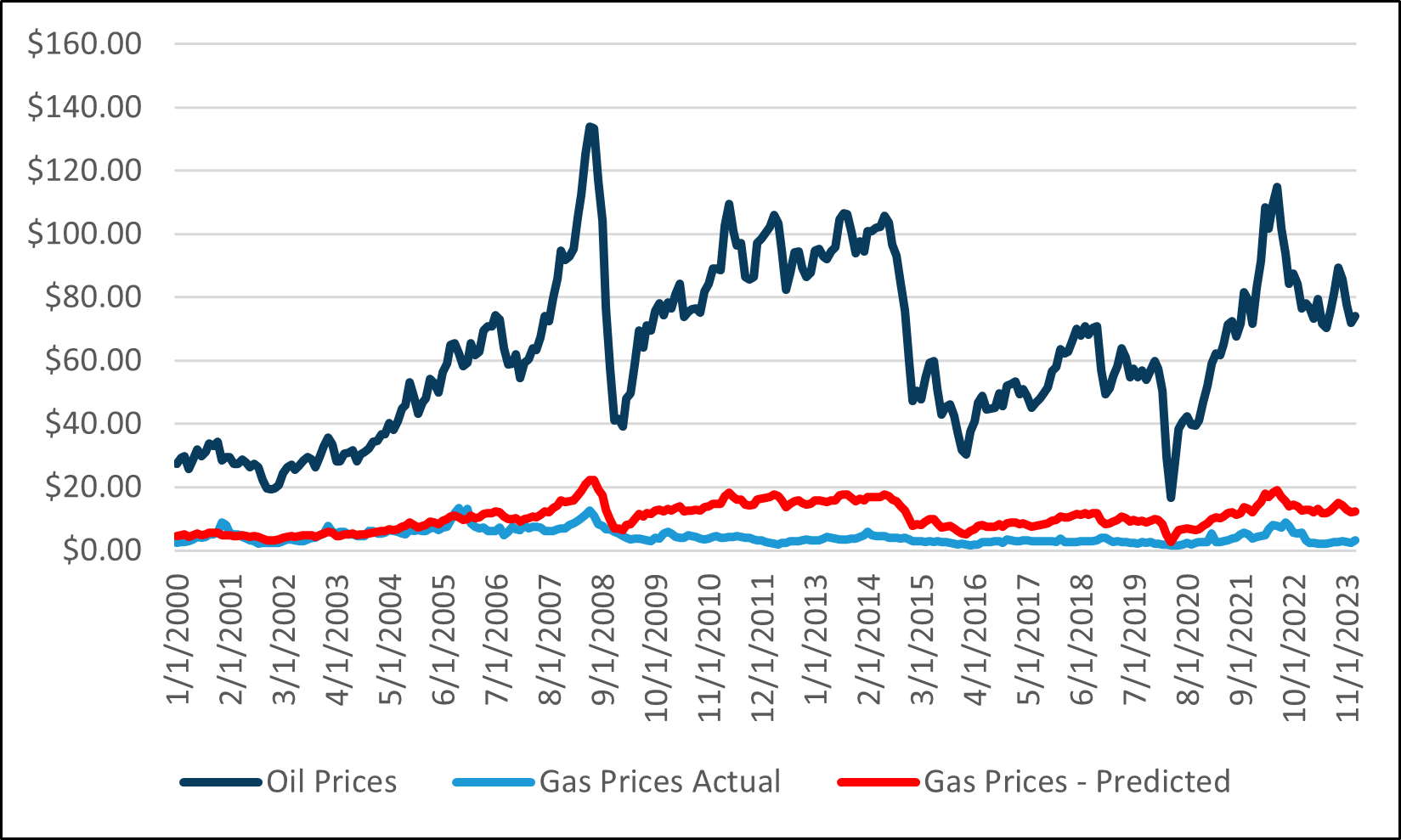

Historical Commodity Prices

Shown in the graphic above are actual spot prices of oil and gas, along with the “predicted” gas price assuming the six-times BOE conversion factor. As shown, this relationship supports the underlying market prices until late 2008, but after that date natural gas prices have failed to keep up with oil prices and the expected conversion factor.

2008 Turning Point

The divergence in the prices of natural gas relative to oil beginning in 2008 can be attributed to several key factors:

- Shale Gas Revolution: One of the most significant factors was the advent and rapid expansion of hydraulic fracturing (fracking) and horizontal drilling technologies, particularly in the United States. These innovations made it economically feasible to extract natural gas from shale formations, leading to a substantial increase in natural gas supply. The shale boom significantly increased natural gas production, contributing to lower prices due to the increased supply.

- Market Dynamics and Supply-Demand Balance: The prices of oil and natural gas are influenced by their own supply and demand dynamics. While both commodities are used for energy, they have different applications and market dynamics. The surge in natural gas supply, especially from shale gas, outpaced the growth in demand for natural gas, leading to lower prices.

- Infrastructure and Transportation Constraints: Natural gas markets are more regionally segmented compared to the global oil market due in part to transportation constraints. Natural gas requires pipelines for transportation over land and liquefaction facilities for overseas shipping, which can be costly and time consuming to develop.

- Economic Recession: The global economic recession in 2008-2009 led to a decrease in demand for both oil and natural gas. However, the impact on natural gas prices was more pronounced due to the already increasing supply from shale gas production. As the economy recovered, the demand for oil rebounded more quickly than for natural gas, partly due to the global nature of the oil market and the slower recovery of industrial demand for natural gas in certain regions.

- Environmental and Regulatory Factors: Increasing environmental concerns and regulatory policies aimed at reducing carbon emissions have also played a role. Natural gas is seen as a cleaner alternative to coal for power generation, which has increased demand for natural gas in some regions. However, the rapid increase in supply has kept prices relatively low compared to oil, which has a more diversified demand profile, including transportation, where alternatives to oil are less prevalent.

These factors combined to create a situation where natural gas prices have been lower relative to oil prices and the BOE conversion factor since 2008.

Market Analyses

To test the relevance of reserves stated in terms of BOE as a driver of current oil and gas company values, we developed a regression analysis. The starting point for our analysis was a group of publicly traded E&P companies and the value of their total market capital as of February 29, 2024:

Company |

Ticker |

Total Capital (BEV) $Billions |

|---|---|---|

|

APA Corporation |

NasdaqGS:APA |

$14.18 |

|

Callon Petroleum Company |

NYSE:CPE |

$3.99 |

|

ConocoPhillips |

NYSE:COP |

$151.33 |

|

Devon Energy Corporation |

NYSE:DVN |

$34.42 |

|

Diamondback Energy, Inc. |

NasdaqGS:FANG |

$39.37 |

|

EOG Resources, Inc. |

NYSE:EOG |

$70.19 |

|

Hess Corporation |

NYSE:HES |

$53.41 |

|

Marathon Oil Corporation |

NYSE:MRO |

$19.44 |

|

Matador Resources Company |

NYSE:MTDR |

$9.76 |

|

Murphy Oil Corporation |

NYSE:MUR |

$7.39 |

|

Occidential Petroleum Corporation |

NYSE:OXY |

$81.33 |

|

Ovintiv, Inc. |

NYSE:OVV |

$19.08 |

|

Pioneer Natural Resources Company |

NYSE:PXD |

$60.28 |

|

Range Resources Corporation |

NYSE:RRC |

$9.43 |

|

SM Energy Company |

NYSE:SM |

$6.64 |

|

Vital Energy, Inc. |

NYSE:VTLE |

$3.37 |

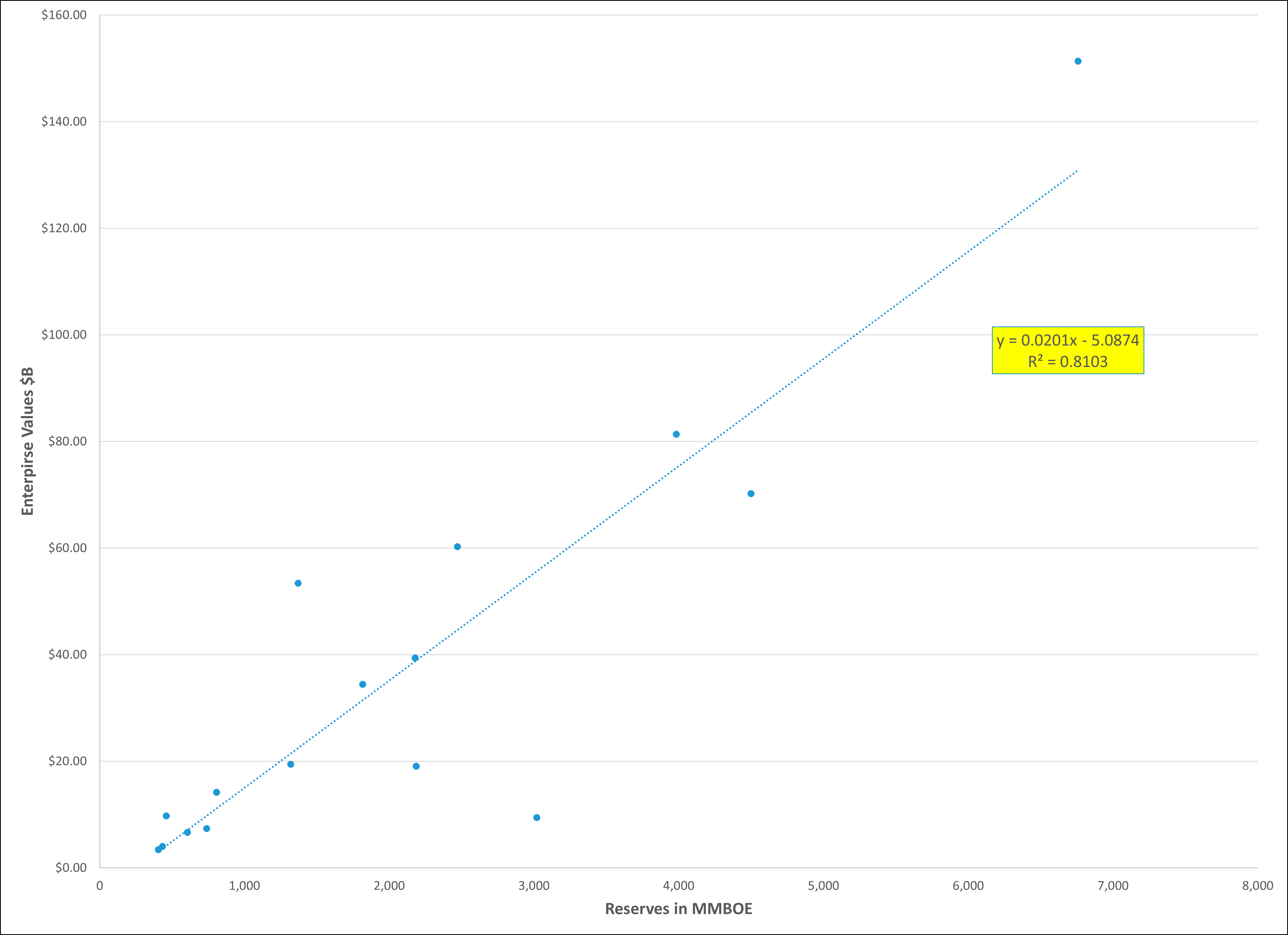

Next, we compared each of these companies’ total capital, or business enterprise value, to their reported reserves stated in terms of BOE.

Publicly Traded Oil & Gas Companies Enterprise Value versus BOE Reserves

As seen above, there is definitely a correlation, and the R-Squared metric for the regression shows a value of about 81%. This implies that statistically, based on the underlying data, the quantity of each companies’ reported reserves explains about 81% of the expected values in the sample of companies.

Current Market Pricing

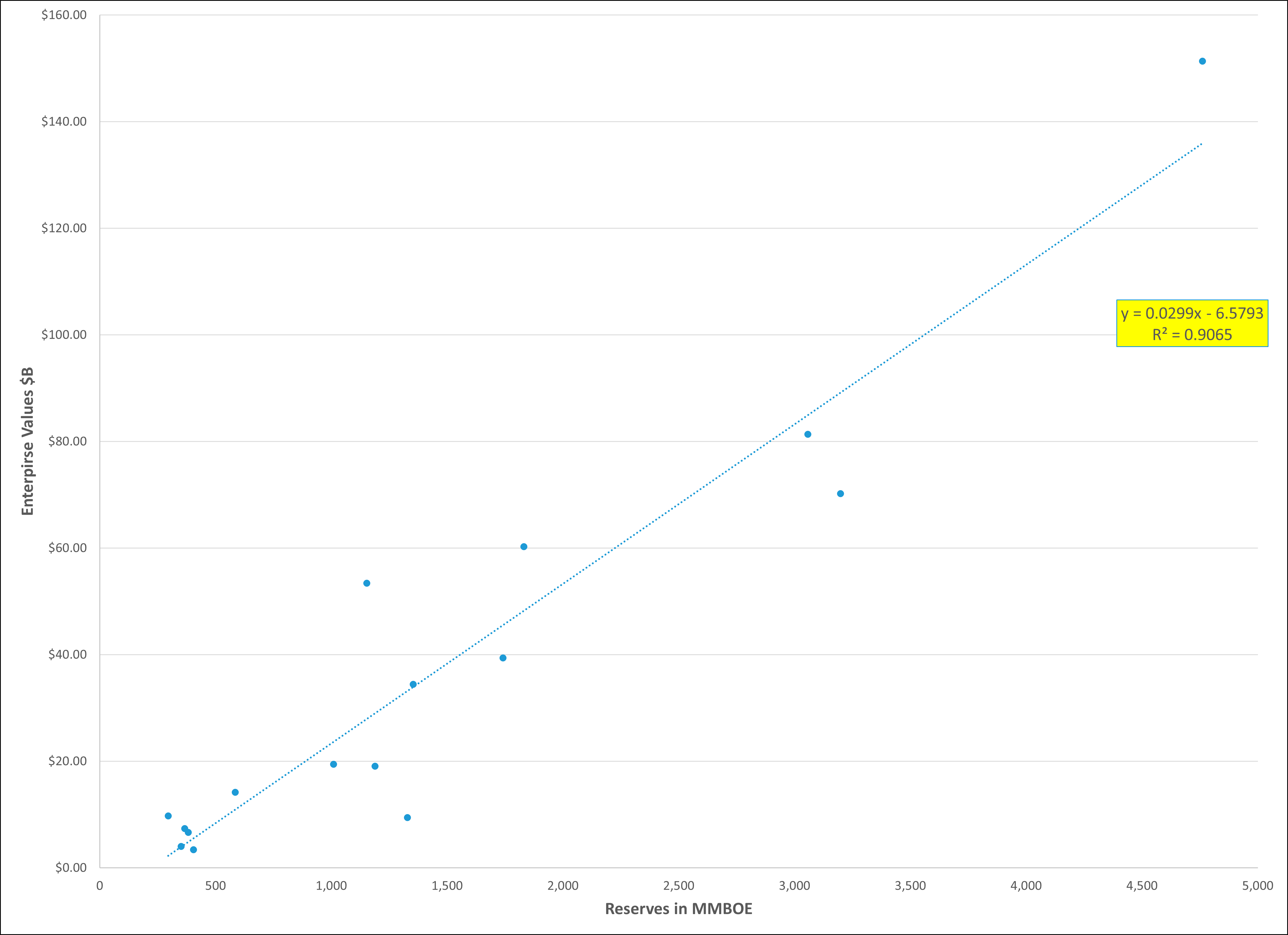

According to the EIA, as of February 29, 2024, oil and natural gas prices were $79.22 per barrel and $1.67 per MMBTU, respectively. On an economic basis, this implies a ration of more than 47 units of natural gas to equal one unit of oil, as compared to the six-times conversion factor based on the relative heating values within each commodity. This significant pricing disparity casts concern on the use of BOE, without modification, as an indicator of oil company values.

Revised Market Price-Based Analyses

To test this concept, we replicated the previous regression analysis, except we used 47.4 times “market price conversion factor,” as compared to the six-times conversion factor consistent with heating values.

Publicly Traded Oil & Gas Companies Enterprise Values versus Price-Weighted BOE Reserves

Other Factors

Reserves are just one of the factors that drive the market values of E&P companies. Other key factors include:

- Strength of the management team

- Access to capital

- Proximity to pipelines and transportation hubs

- Access to drilling rigs and completion crews

- Geographic location and perceived quality of the underlying reserves.

So one would not expect to see a perfect correlation (R-squared of 100%) between these two variables, but it does appear that current market valuations reflect the current commodity price disparity from BOE.

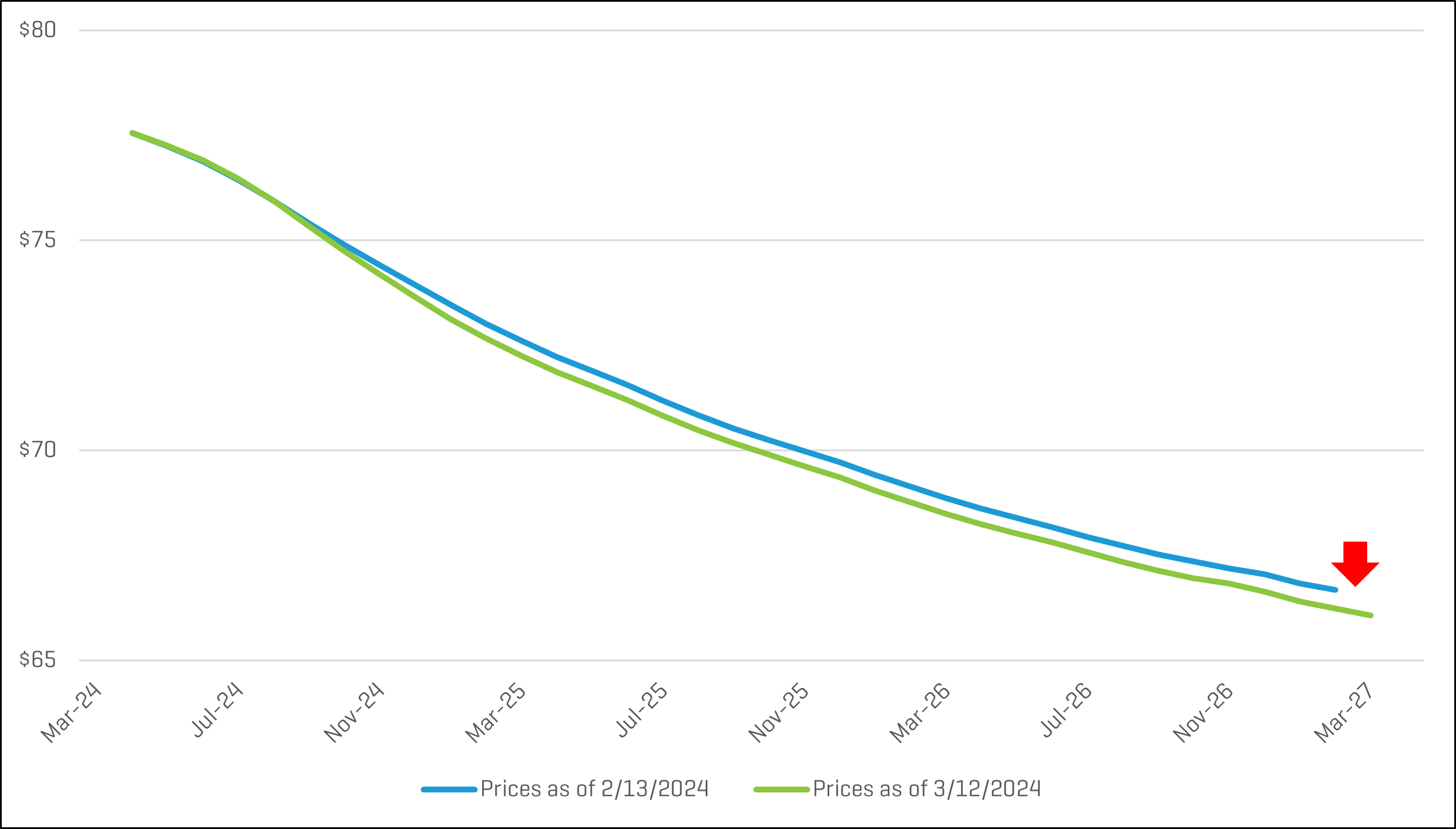

WTI Strip Prices Decrease

Spot prices and futures prices for the West Texas Intermediate (WTI) contract remained stable in the near term and decreased approximately $0.50 over the longer term.

WTI Strip Prices - One Month Change

As shown, the oil price curve remains in a state of “backwardation,” reflecting the market’s expectation of lower future spot prices.

Oil Price Outlook

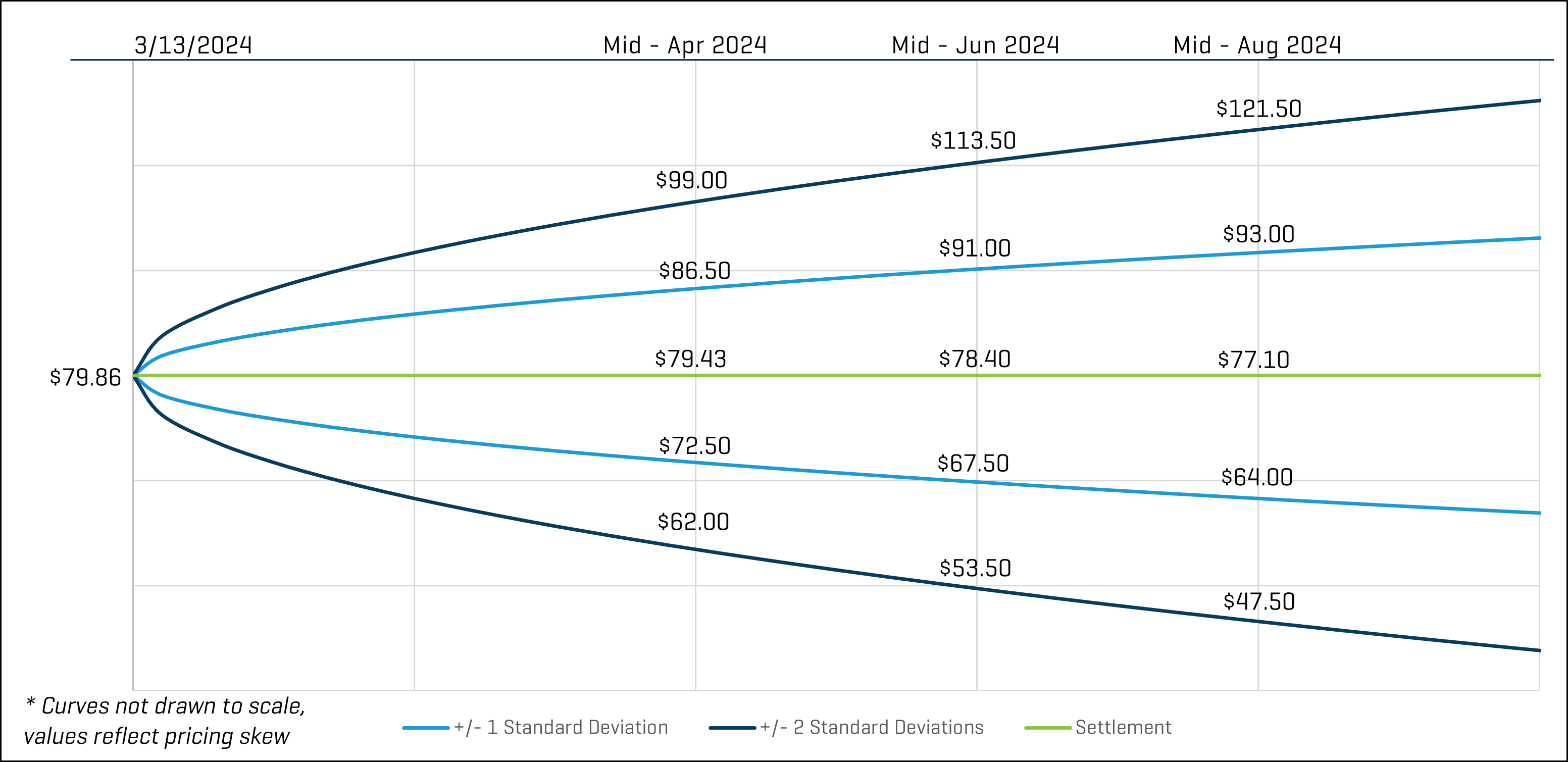

The price distribution below shows the crude oil spot price on February 13, 2024, as well as the predicted crude oil prices based on options and futures markets. Light blue lines are within one standard deviation (σ) of the mean, and dark blue lines are within two standard deviations.

WTI Crude Oil $/BBL

Based on these current prices, the markets indicate there is a 68% chance oil prices will range from $67.50 and $91.00 per barrel in mid-June 2024. Likewise, there is roughly a 95% chance that prices will be between $53.50 and $113.50. By mid-August 2024, the one-standard deviation (1σ) price range is $64.00 to $93.00 per barrel, and the two-standard deviation (2σ) range is $47.50 to $121.50 per barrel.

Key Takeaways

Remember that option prices and models reflect expected probabilities, not certain outcomes, but that does not make them any less useful. Through the early half of 2023, crude oil spot prices primarily fluctuated within the range of $70 to $80 per barrel. Thereafter, from August 2023 through October 2023, we observed spot prices primarily above that range. During that time, we observed an increase in futures price volatilities.

As spot prices have settled back down to the $70 to $80 per barrel range, futures price volatilities have begun to decrease, as evidenced by the futures price ranges observed. For mid-August 2024 pricing as of March 13, 2024, the 1σ range had a spread of $29.00 per barrel, and the 2σ range has a spread of $74.00 per barrel. For comparison, in 2022 we observed 1σ and 2σ price ranges in excess of $65.00 and $150.00, respectively.