English

English

In its December 6, 2018 newsletter, Warranty Week discussed automotive warranty claims trends. To better analyze these trends, Warranty Week segmented reported claims data, from publicly reported OEM and supplier financial statements, into those for passenger cars/small vehicle OEMs and heavy trucks/large vehicle OEMs, as well as suppliers of powertrain components and other vehicle components.

Warranty claim rates are calculated by dividing quarterly warranty claims paid in a quarter by the vehicle or component sales for that quarter. Warranty claim rates of vehicle manufacturers and suppliers can be helpful in identifying the emergence of defect trends, understanding the impact of financial reserves, identifying opportunities for risk management strategies, and considering the impact of defect rates on component pricing and margin.

For its analysis, Warranty Week divided the 50 vehicle manufacturers into 24 that manufacture small vehicles (including passenger cars and motorcycles) and 26 that manufacture large vehicles (including trucks, buses and RVs). It also divided 120 suppliers into 27 that primarily manufacture drivetrain components and 93 that manufacture other components.

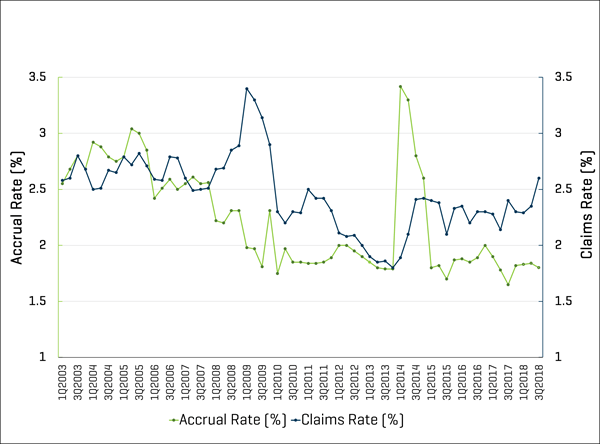

From this analysis Warranty Week identified a recent uptick in the industry warranty claims rate for passenger cars/small vehicles in the third quarter of 2018 from 2.3% to 2.6%, the highest claims rate since 2009, when the U.S. economy was in recession which is shown in Figure 1. After peaking at nearly 3.5% in 2009, the warranty claims rate for small vehicle makers steadily declined until 2014 when it was less than 2%. In the last several years the small vehicle maker claims rate had stabilized between 2.1% and 2.4%. The most recent reported increase broke a pattern and raises concerns that claims rates may again be rising, particularly if sales volumes begin to slow.

Figure 1. Passenger Car & Small Vehicle Makers Average Warranty Claims & Accrual Rate

(as a % of product sales, 2003-2018)

Over the last five years there has also been a consistent gap between the accrual and claims rates for these small vehicle makers, of about 0.5%. That is, small vehicle makers were consistently recognizing more claims as a percentage of sales than their accruals as a percentage of sales. This can result from fluctuations in sales, as well as unexpectedly higher levels of claims being paid. In the last period, when the claims rate increased, the accrual rate actually decreased, seeming to indicate the small vehicle manufacturers may not have anticipated the increase in claims.

On the other hand, Warranty Week observed a steady decline in the warranty claims rate for heavy trucks/large vehicles during 2018, decreasing from about 2.0% to 1.6% by the third quarter; this was the lowest claims rate related to heavy trucks/large vehicles since 2012. The warranty claims rate and accrual rates for large vehicle manufacturers have tracked very closely during most of the last 15 years.

Similarly, warranty claims rates for powertrain suppliers have decreased from 0.96% in 2017 to 0.84% by the third quarter of 2018. Warranty claims rates experienced by other parts suppliers also decreased, from 0.55% in 2017 to 0.51% by the third quarter of 2018. Both sets of suppliers have had warranty claims and accrual rates that have tracked closely with each other during the last 15 years.

In recent years we have seen a decline in the number of automotive recalls, a decline in the average size of recalls, a trend toward recalls of newer vehicles, and an increasing number of recalls related to software and integrated electrical components. The combination of these factors could result in a decline in overall recall costs for light vehicle manufacturers, as well as declines in cost recoveries from suppliers. This may help to explain a decreasing accrual rate as small vehicle manufacturers look forward. However, the gap between the claims and accrual rates recently, and the increase the claims rate in the most recent period give us pause that we may soon see evidence of an increase in costly recall activity or other defect reports. As vehicle sales face economic headwinds, industry participants will want to carefully watch reported claims and accrual rates for small vehicle makers as a potential leading indicator or trouble ahead.