M&A Market Update Navigating Uncharted Waters

M&A Market Update Navigating Uncharted Waters

With economic growth being a key priority for the Trump administration, how will new policies affect mergers and acquisitions, or business in general?

“Public sentiment is everything. With public sentiment, nothing can fail. Without it, nothing can succeed.” – Abraham Lincoln, during his first debate with Stephen Douglas on August 21, 1858, in Ottawa, Illinois

“It’s sort of like a teeter-totter; when interest rates go down, prices go up.” – Bill Gross, former manager of PIMCO’s Total Return Fund (the world’s largest bond fund) and current manager of Janus’ Global Unconstrained Bond Fund (date unknown)

It’s difficult, if not impossible, to find someone who does not have an opinion on our newly elected president and his administration. Equally difficult to find is someone who is willing to say what they think a Trump presidency will mean for the mergers and acquisitions (M&A) market, or, for that matter, business in general. Unless you are a Texasbased general contractor specializing in concrete barriers, it is difficult to predict what the next four years will bring for most businesses, though economic growth is certainly one of this administration’s top priorities.

While no one has a proverbial crystal ball, the underlying fundamentals that have driven (and continue to drive) M&A activity remain in place. That said, we find ourselves reflecting upon two of my favorite quotes, on the preceding page, that serve to remind us all that President Trump’s mandate for economic growth is clear, but that with such growth comes the potential for value-dampening hikes in interest rates.

Current State of the M&A Market

The M&A market has been on overdrive for over five years, though in 2016 we experienced somewhat of a mixed bag. Overall reported transaction value increased slightly year over year in spite of a 17% decrease in total volume. This contradiction can be explained by the resurgence of “mega- deals,” or those over $1 billion. The aggregate transaction value for such deals increased by over 8% relative to 2015.

In spite of the slowdown in overall M&A activity, valuation multiples in terms of earnings before interest, taxes, depreciation, and amortization (EBITDA) remain at or near peak levels (Figure 1). Astute readers of our market updates know that we attribute such lofty valuations to a continued imbalance between the supply of high-quality acquisition opportunities and the number of potential buyers (both strategic and private equity) willing and able to deploy capital.

Such valuation premiums – relative to more typical market environments – are difficult to quantify, though they appear to average (based on our proprietary analysis of nonpublic information of multiples paid) in the 2.0x to 3.0x range. Furthermore, just as remarkable (and even more difficult to quantify) is the widespread sentiment among dealmakers that even the most “storied” or difficult and cyclical companies are generating interest in the current environment. Even the oil and gas sector, whose recent turmoil had kept many potential buyers on the sidelines, is showing signs of a resurgence in activity.

Unemployment continues its steady downward trajectory, consumer confidence continues its upward trajectory, and U.S. gross domestic product (GDP) continues to exhibit signs of longer-term stability in spite of the past three quarters, which were soft. Such softness was attributed to increased imports combined with decreased federal spending, decreased nonresidential fixed expenditures, and decreased exports.

Our View of the Future

The view looking forward is, as always, murky at best.

The general consensus among economists is that while a Trump presidency brings with it increased risks (e.g., a trade war with China), it also carries with it greater hope for stronger growth.

Lately, corporate profits have been buoyed by deflationary raw material inputs, and many commodities, from copper to corn, are at or near recent lows, but we do not know how much longer this benefit will last.

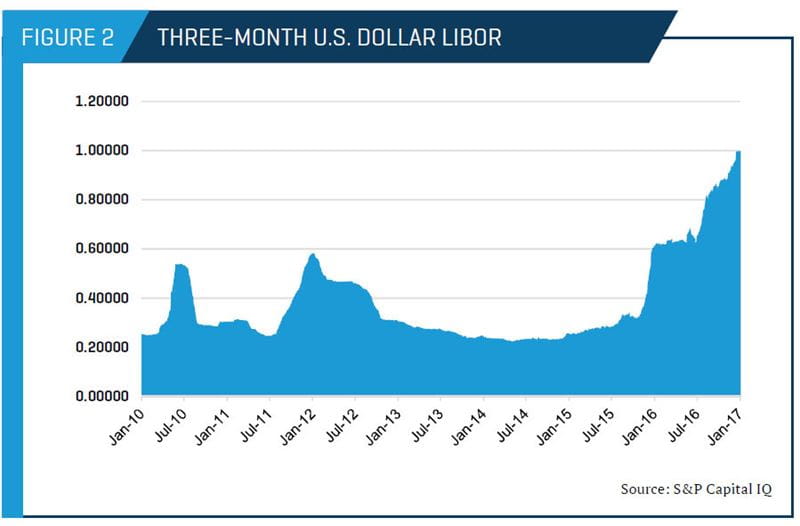

The debt markets remain open, and we cannot fathom a scenario in the next few years in which lending guidelines, capital requirements, and regulatory oversight increase under President Trump. Interest rates are a different story. If the recent run-up in LIBOR is any indication, interest rates are headed in only one direction – up (Figure 2).

Fortunately, leveraged buyout (LBO) returns are far more sensitive to decreases in debt availability than to increases in borrowing costs. As shown in Figure 3, a dramatic increase in borrowing costs – say from 4% to 18% – would only marginally impact expected returns, whereas even a moderate pullback in the debt available for buyouts – say, one multiple of EBITDA or from 3.0x to 2.0x total leverage – would decrease expected returns by over 300 basis points, ceteris paribus.

As we write this, the public equity markets continue to hit new highs seemingly every day. Yet we do not know when another correction will occur, and if such a correction will negatively influence M&A multiples.

We do not know if a major external shock to the system (e.g., a widespread coordinated terrorist attack or escalation of tensions on the Korean peninsula) is on the horizon, nor how the Trump administration and the U.S. economy would react to such an event.

Finally, we do not know how buyers will react in the face of continued pressure to top-line growth prospects. Will such buyers take a “long term” view or will they (as has typically been the case) begin to lower bid prices to better align with long-term average multiples?

In summary, as we pause to reflect upon where we are in the cycle, we see that the fundamental forces driving M&A activity and valuation multiples are no longer as perfectly aligned as they once were. This is not to say that a major pullback in prices is imminent. Rather, we no longer expect continued multiple expansion, but instead view multiple normalization as an ever-increasing possibility.

M&A Market Activity

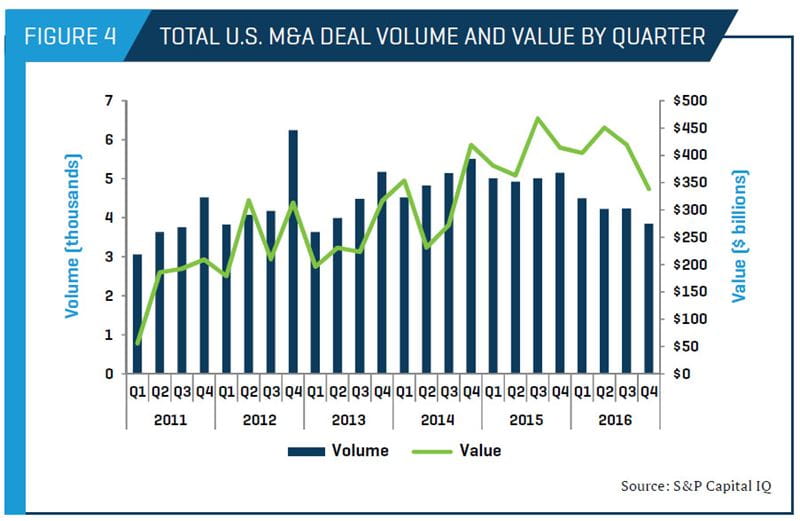

Improved availability of capital, better and sustained company performance, and narrower valuation gaps have powered U.S. M&A transaction activity since 2010. 2016 showed a steadying of overall transaction value but marked softness in M&A volumes (Figure 4).

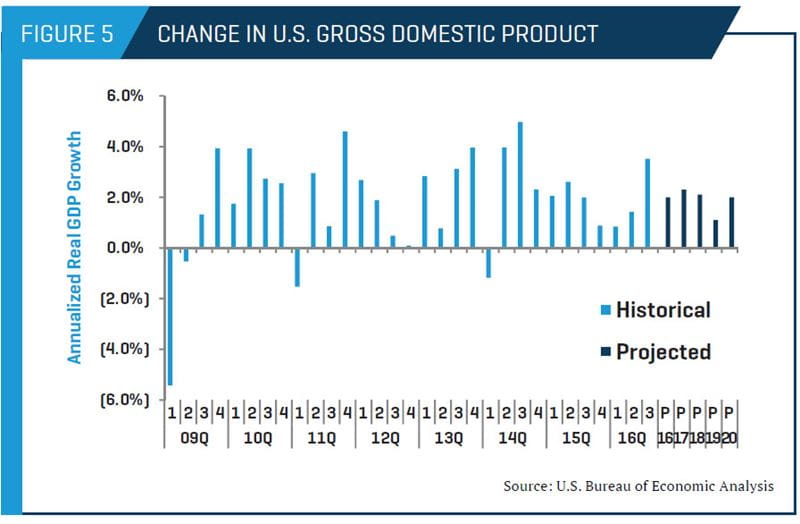

U.S. GDP, often viewed as a proxy for the overall health of the economy, has recovered from the contraction experienced during the recession in late 2008 and early 2009. While few economists are predicting another recession in the near future, neither are forecasters predicting rampant growth. Regardless, in the third quarter of 2016, U.S. GDP growth exceeded 3.0% for the first time since the third quarter of 2014 (Figure 5).

Consumer confidence generally improves as the unemployment situation improves. Fortunately, unemployment has maintained its steady march downward and sits at levels not seen since mid-2008 (Figure 6). Such favorable tailwinds are expected to continue through the first half of 2017.

As mentioned in previous articles, data on lower middle-market transactions is notoriously difficult to come by, but year-over-year comparisons can prove illustrative. Volume and the total value of deals falling within the lower middle market (in this context defined as transactions less than $250 million in total value) for all of 2016 were depressed relative to 2015; both overall volume and aggregate value were down. Only the very largest of deals showed improvement year over year (Figure 7).

Strategic buyers were active in the first half of 2016, though less so than in the recent past.

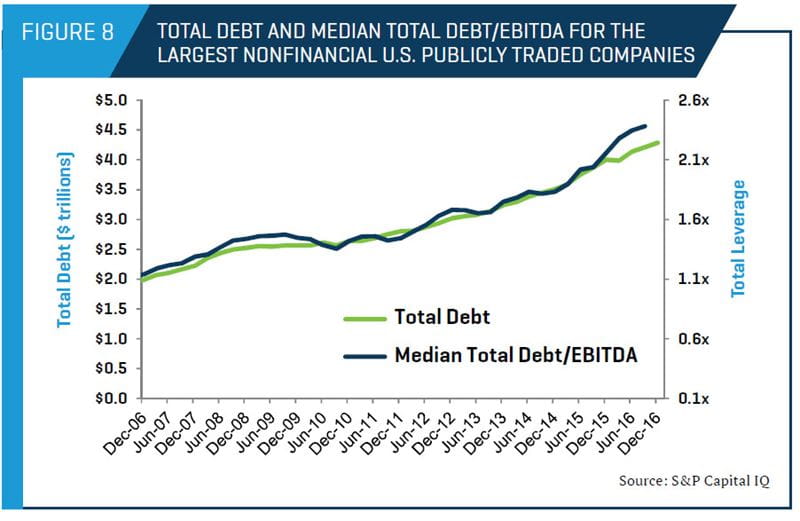

The continued (albeit, softer) stimulus for strategic-led deals is a combination of lower organic growth prospects absent acquisitions, accommodative senior debt markets (for most of the past 12 months), and a record amount of cash and other liquid assets held by nonfinancial companies. Evidence of the accommodative debt markets is clearly visible in the continued rise in total debt levels. Companies’ balance sheets are becoming more leveraged as median total debt/EBITDA ratios increased through the end of 2016 (Figure 8).

Complementing (from a seller’s perspective) strategic buyer interest is private equity, which remains a potent force in deal flow. Favorable credit markets and an estimated $749 billion capital overhang ($82 billion of which is nearing the end of its investment horizon) will continue to provide an impetus for investors to remain competitive in transactions (Figure 9). Furthermore, it should be kept in mind that the capital overhang actually translates into $1 trillion or more in purchasing power, given the leverage available in today’s marketplace.

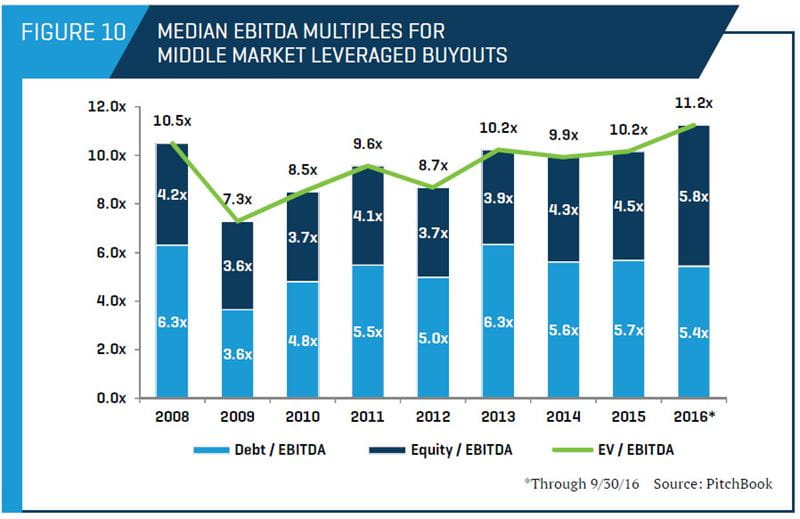

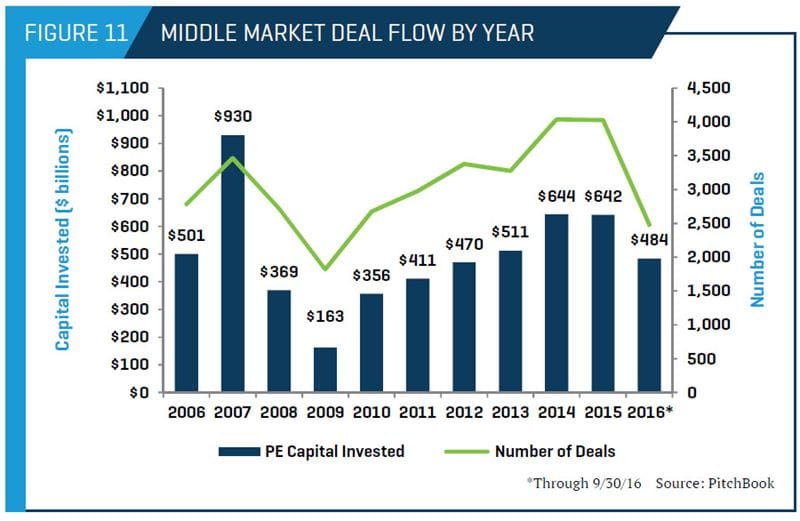

Nowhere is the increase in current valuation multiples due to the aforementioned factors more evident than in the prices paid by private equity during the past five years. Such prices are a function of debt providers’ willingness to lend and sponsors’ willingness, for the first time in history, to lower their required return thresholds. Historically, financial sponsors promised their limited partners an expected compounded annual return of 20% to 30%; however, recent feedback from many in the private equity community (all of whom wish to remain nameless) is that returns are instead being modeled in the high teens. Such a reduction in required returns has the same effect as a reduction in yields on bonds – when rates fall, the prices that buyers pay for new investments rise, as prices and rates move in opposite directions. The continued increase in the reported multiples for 2016 (the highest reported multiples in recent memory) is likely a result of a decrease in quality targets available to be acquired, as LBO volume is down relative to 2015 (Figures 10 and 11).

Outlook for 2017 and Beyond

Our view for the foreseeable future remains cautiously optimistic. Buyer appetites and resulting valuation multiples are still at or near historical levels. How long this will last is anyone’s guess; that said, for those business owners on the fence about selling their companies, it may be prudent to accelerate such decisions rather than wait to see what the road ahead has in store.

Also contributing to this article:

Christos Kyriazi