English

English

The oilfield services and equipment (“OFS”) industry is a large, highly-competitive industry that provides services and goods to oil and gas exploration and production (“E&P”) companies. The industry and transaction market for its participants are noted for significant cyclicality. Over the last decade, the OFS industry has undergone substantial changes, growth, and shocks, resulting from oil and natural gas commodity price growth, the development and expansion of U.S. unconventional drilling and production, and the fallout from the Great Recession and the Macondo tragedy. Over the last couple of years, the transaction activity transitioned to focusing on internal operational improvements and clarifying performance for investors. Consequently, we have observed muted merger and acquisition (“M&A”) activity and an interesting uptick in spin-off transactions. In addition, we have also seen increased utilization of master limited partnership (“MLP”) structures in the OFS industry, a trend that is noteworthy for its expansion of qualifying income and investor acceptance.

OFS Industry Conditions

In general, OFS companies provide products and services to E&P companies but are typically not producers of oil or natural gas themselves. In 2013, more than 10,000 companies operated in the U.S. OFS industry and ranged in size from Fortune 500 companies to small local retailers.1 The largest OFS participants, in terms of market capitalization, include the Big Four diversified service providers, Schlumberger Ltd., Halliburton Co., Baker Hughes Inc., and Weatherford International and large equipment manufacturers, National Oilwell Varco, Inc. (“NOV”) and Cameron International Corporation.

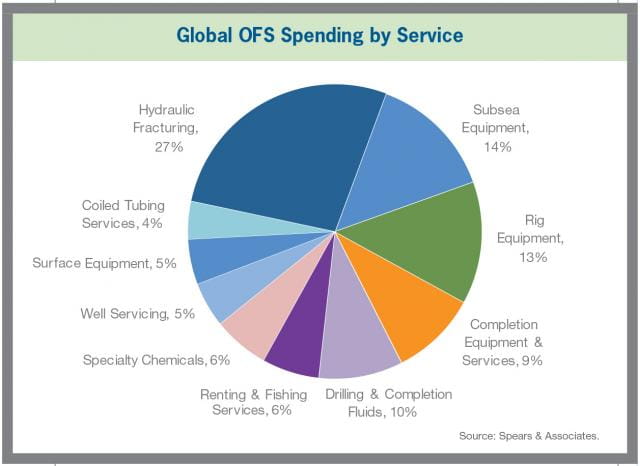

OFS companies offer a wide variety of services. As seen in the chart on the previous page, the service and equipment subsectors are comprised of a number of segments with hydraulic fracturing (“fracking”), subsea equipment, and drilling & completion fluids representing the largest segments. Fracking has grown to become the largest service segment. Although not without its own challenges due to excess equipment capacity in recent years, demand for fracking services has grown with increased reliance on horizontal drilling and fracking of denser rock formations in the unconventional plays. In addition to the segments presented in the chart, contract drilling (the provision of drilling rigs and related personnel) is another very significant service offered by OFS industry participants.

OFS industry performance is highly correlated to the capital spending budgets of E&P companies as demand is driven by the availability of capital for E&P companies as well as long-term expectations regarding the prices of oil and natural gas. Over the past five years, capital spending by E&P companies has increased significantly, as many companies have retooled their property holdings and operations in pursuit of and development of unconventional oil plays. According to IHS Herold, Inc. (“IHS”), an energy research and consulting firm, global upstream capital spending has increased from $493.5 billion in 2008 to $627 billion in 2012.2 However, increased investor pressures on E&P companies to become more operationally efficient and reduce spending caused capital spending by U.S. companies to decline by approximately 16% in 2013, with development spending being the only category to increase as companies drilled out acreage acquired in recent years. In 2013, acquisitions of proved and unproved properties also declined by approximately 50% and 60%, respectively. According to IHS, gas-weighted E&P companies decreased capital spending for the third consecutive year, while oil-weighted E&P companies reduced capital spending for the first time in several years. IHS further projects that capital expenditures by E&P companies are expected to increase by approximately 2.5% in 2014.3

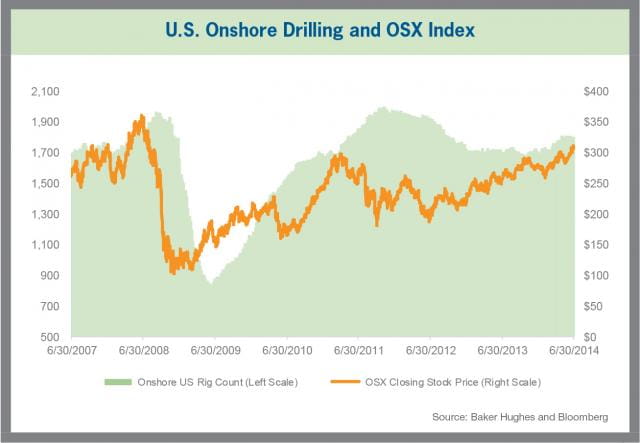

The drilling rig count increased from 2007 to 2008 (as evidenced by the increasing number of onshore U.S. rigs) primarily due to increasing oil and gas prices and favorable economic and industry conditions. In 2009, oil and gas prices dramatically decreased as a result of the Great Recession. At that time, E&P companies reduced capital and operating budgets and reduced drilling activity, which reduced the demand for the OFS industry. As oil prices began to rebound in the second half of 2009 and the broader application of unconventional drilling techniques to oil plays that have followed, drilling activity and demand for OFS has increased. As shown in the chart below, the PHLX Oil Service Sector Index (“OSX”), an index of the leading OFS service companies, has nearly recovered to the all-time highs seen in 2008 as a result of improving industry and economic conditions. However, the OSX has trailed the performance of the S&P 500 in 2012, 2013, and year-to-date through July 2014 due to general margin pressures in many segments of the U.S. market as well as slower growth in overseas markets.

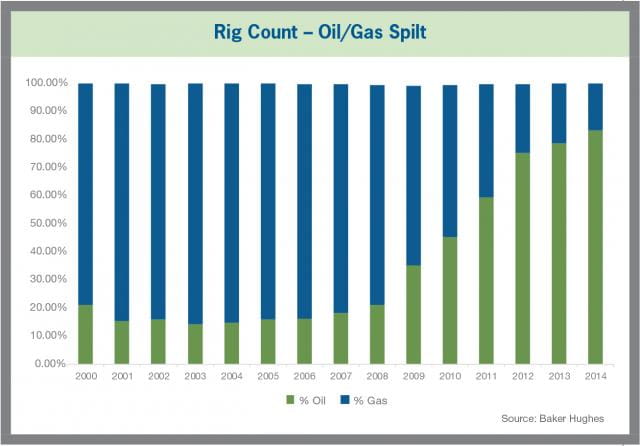

The major overriding trend in the U.S. market is the development of unconventional oil plays. The rig count for oil-directed wells has increased from approximately 20% in the early 2000s through 2007 to over 80% in 2014. This has been the result of both an acceleration in activity for oil-directed rigs and a collapse of activity for natural gas-directed rigs. The natural gas-directed rig count increased through mid-2008 following the discovery and development of unconventional gas plays in the early and mid-2000s and peak natural gas prices. In addition, following the recovery from the recession, many E&P companies needed to drill in order to maintain their leaseholds. However, in an environment of sustained low natural gas prices, the opportunity cost of giving up drill-to-hold leasehold acreage from inactivity has declined. The large increase in oil-directed rigs can clearly be seen in the Permian Basin, Mississippian, Bakken, and Eagle Ford plays which have seen rig counts increase from 771 in 2011 to 1,008 as of June 30, 2014 (on an aggregate basis).4

The development of unconventional resource plays requires more drilling- and equipment-intensive operations due to horizontal drilling and fracking. The percentage of rigs drilling horizontal wells has increased from 20% in 2007 to nearly 70% in 2014. As mentioned previously, investor pressures intensified beginning in 2012 for E&P companies to become more focused on internal cash flow generation, lower well costs (particularly relative to lateral length), and faster development. As a result, advances such as shortened horizontal drilling times and multi-well pad drilling have been more broadly deployed and have put pressure on margins and equipment utilization in this segment of the industry.

The offshore oil and natural gas industry has also undergone significant changes over this time period. E&P companies have ventured into deeper and more challenging development environments as the next frontier for large projects, pushing the envelope on technological capabilities. The Macondo tragedy and subsequent moratorium halted activity on these massive projects in the Gulf of Mexico. As oil prices remain attractive for development and the government and industry have adapted to the new regulatory scheme, exploration and development of these projects has resumed and in many cases expanded following successes. Recent oil prices and improvements in technology to identify drilling targets have also increased drilling on the shallower shelf.

Transaction Market Activity

With this back-drop of OFS industry conditions set, we will now provide an overview and discussion on the transactional activity in the industry, including the OFS merger and acquisition environment, a recent increase in OFS spin-offs, and the continued use of OFS MLP structures.

M&A Market

M&A activity in the OFS industry collapsed in 2009 from its historically high level in 2008 as a result of the fallout from the Great Recession. M&A activity was particularly robust in 2008 and the years leading up to that point as demand for OFS grew rapidly and participants sought to provide a broad range of services for E&P companies. M&A activity rebounded to strong levels in 2010 and 2011, driven primarily by consolidation by large players. The downward trend in 2012 and 2013 reflects a slowdown in deal activity which has been driven by companies’ focus on internal efficiencies and operations due to pressures from the E&P industry. Many of the major global diversified oilfield services players generally spent 2013 integrating prior acquisitions and/or consolidating existing product and service offerings for improved efficiency and profitability. The largest OFS deal in 2013 was General Electric’s (“GE”) acquisition of Lufkin Industries Inc. (“Lufkin”), primarily an oilfield pump manufacturer, for $3.1 billion which accounted for approximately 20% of the total transaction deal value in 2013. GE has grown its oil and gas business through a number of acquisitions in recent years, and the acquisition of Lufkin was targeted to expand GE’s support division with artificial lift capabilities.

In 2013, drilling rig owners and operators within the OFS Industry continued to consolidate and focused on specializing by asset type. For example, the acquisition of a 49.1% interest in Sevan Drilling ASA by Seadrill Limited (“Seadrill”) for approximately $589 million is an example of a company attempting to specialize its product and service offering by gaining exposure to ultra-deepwater rigs. The oilfield products manufacturing segment remained robust throughout 2013, with deals primarily focused on strengthening the global suppliers’ positioning in key markets and implementing cost efficiencies within supply chains.5

Looking forward, M&A activity has been rebounding through the middle of 2014 as a result of improved activity levels in the market as well as the strengthening of the capital markets. One of the major deals that has closed thus far in 2014 was C&J Energy Services, Inc.’s (“C&J”) acquisition of the hydraulic fracturing business of Nabors Industries, Ltd. for approximately $2.9 billion. The new company, C&J Energy Services Ltd., will be incorporated in Bermuda and run from its current offices in Houston. According to C&J, the acquisition was made in an effort to improve profitability through utilization improvements over the larger fleet and reducing overall taxes by being incorporated offshore. The acquisition represents another signal that the fracking business is improving following a difficult 18 months.

OFS Spin-off Activity

In addition to the M&A activity previously discussed, the market is also rewarding firms that concentrate on their core business and improve operating efficiencies. As such, many OFS companies are increasingly using spin-offs as a strategy to unlock value. A spin-off allows companies to separate part of their businesses by creating a new publicly-traded entity. As a result, companies can focus on the strategic and operational plans of the separated entity without diverting human and financial resources from the parent company. Also, the parent company and its spin-off may have different capital requirements that may not be optimally addressed under a single capital structure. In a pure play spin-off, a parent company distributes 100% of its ownership interests in a separate entity as a tax-free dividend to its existing shareholders. Upon completion of the spin-off, the parent company and the separated company are both publicly traded companies that have exactly the same shareholder base. The pure play spin-off structure is more transparent and may attract investors who more highly value the separated operations.

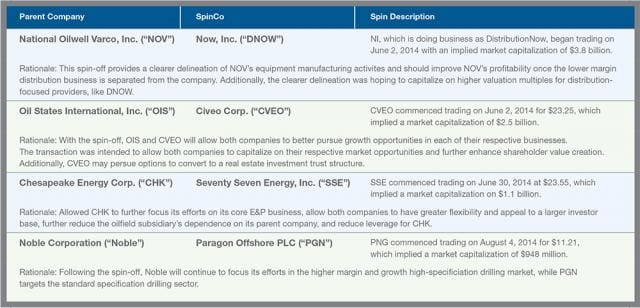

Below we present the recent spin-offs involving OFS companies. In each of these instances, the parent company has sought to provide greater clarity of the operating units by separating the business units. Following the success of MRC Global’s IPO in 2012, NOV has sought to achieve a similar, higher multiple for its supply business which was created by combining Wilson Supply, which it acquired in 2012, with its own supply business. The Civeo Inc. (“CVEO”) spin-off by Oil States International Inc. (“OIS”) is the second major step in retooling OIS’ business over the last year, following a divestiture of Sooner, Inc., a tubular service distribution company. These moves have streamlined its focus as a technology-driven and equipment manufacturing-oriented business, which have received premium valuations by the market. Chesapeake Energy Corp.’s spin-off was executed to achieve the benefit of improved transparency and focus as well as to reduce indebtedness for the parent. Paragon Offshore Ltd. (“PGN”) follows a trend in the contract drilling market whereby many companies have sought to increase focus on particular service lines. Each of these newly spun-off companies has received a positive response in the markets, with the exception of PGN, which has declined in a difficult trading environment over its first two months.

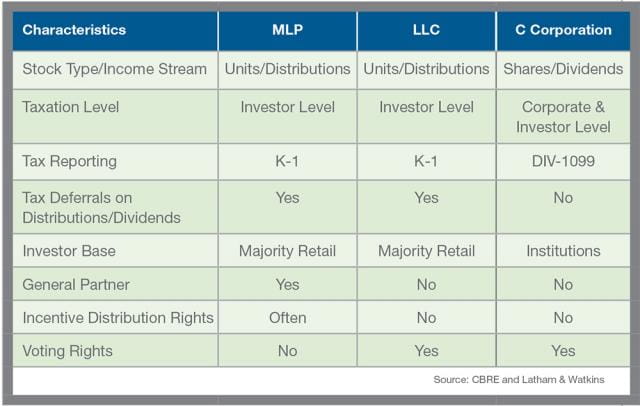

Master Limited Partnerships

While 2014 is on pace to be among the most active years for initial public offerings (“IPOs”) in U.S. market history, U.S. IPO activity has been relatively muted in the OFS industry. Through the first seven months, only five IPOs have been completed. One trend that we observed among the IPOs is the continued and broadening use of MLP structures by OFS companies. Over this time period, the two largest IPOs were MLPs, which raised proceeds of nearly five times that of the three corporate issuers.

An MLP is a state law partnership or limited liability company that does not pay federal income taxes and is publicly traded on a securities exchange. Following what some deemed as an abuse of the structure in the 1980s, MLPs were required to ensure that 90% or more of their gross income is “qualifying income” to maintain partnership status under Section 7704(c) of the U.S. Internal Revenue Code of 1986, as amended (the “Tax Code”).

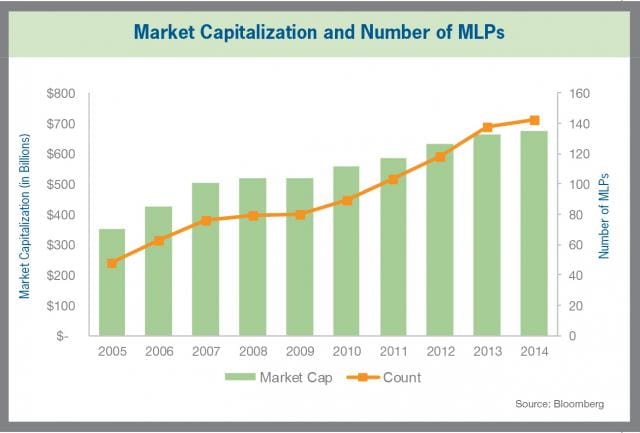

The modern trend in MLPs has been predominantly driven by the midstream oil and gas industry, which popularized the use of the structure beginning in 1997 and 1998. Such MLPs generally produce regular, reasonably predictable cash flow and distributions. Since then, and buoyed by their high yields in a low yield investing environment, MLPs have become a major asset category in U.S. capital markets, attracting substantial investment flows and acquiring and developing vast energy assets. IPO activity among MLPs was the highest on record in 2013, as 28 companies completed their initial offerings in the year. As of June 30, 2014, MLPs had a total market capitalization of approximately $635 billion, the vast majority of which were engaged in midstream activities such as gathering, processing, transportation, and storage. Approximately 20% of all MLPs engage in real estate, investment and financial activities, hotels, motels, and restaurants.

While the capital markets have been highly receptive to MLPs following their strong performance, there is a clear broadening of industry segments utilizing the structure both in OFS as well as other areas of the energy sector, like refining. Companies outside the traditional midstream space have increasingly received Private Letter Rulings (“PLRs”) from the IRS as to determinations of their qualifying income. For example, in 2013, the IRS released 30 PLRs compared with 21 in 2012 and 11 in 2011.6

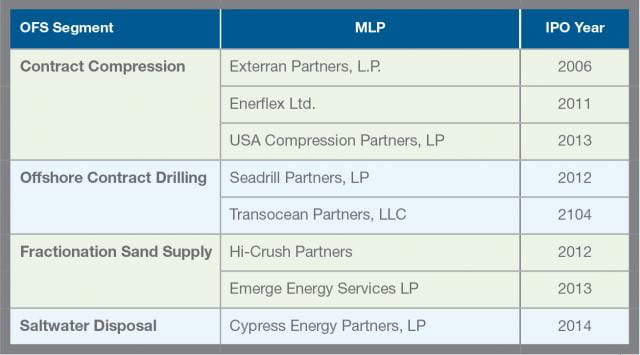

This broadening use of the MLP structure can clearly be seen in the OFS industry. OFS segments that have seen a rise in companies using the MLP structure have included the natural gas compression segment, the offshore contract drilling services segment (Seadrill and Transocean Partners, LLC debuted in 2012 and 2014, respectively), and the saltwater disposal segment (Cypress Energy Services debuted in 2014). Clearly investor demand continues to support this new OFS MLP concept. Although many of the companies have not traded over a cycle.

Following the increase in MLPs in recent years, the IRS elected to temporarily put a pause on issuance of PLRs in March 2014 until further study can be conducted to better understand tax implications and what the appropriate rules should be going forward.7 While the length of the delay was not known as of the date of this publication, investors and OFS industry participants will need to proceed with caution in the interim. In 2013, the IRS conducted a similar review on non-traditional real estate investment trusts (“REIT”) such as timber, data centers, document storage facilities, and cell towers. In the second half of 2013, the IRS resumed ruling on REIT PLR requests.8

Conclusion

Although the OFS industry has experienced lower transaction activity levels in recent years, M&A market activity appears to be rebounding in 2014 as spending by E&P companies remains strong. The OFS companies are expected to remain focused on strengthening their core businesses and improving operating efficiencies by continuing to seek ways to streamline operations and strategically separate business segments. As a result, investors and companies are expected to seek additional shareholder value through transactions to support such ends.