English

English

Oil and natural gas valuation in an estate-planning context is becoming more important, as mineral ownership has created vast amounts of wealth in the past decade. New technologies have unlocked shale1 plays and brought older oil fields back to life. Furthermore, due to the proliferation of independent and, in many cases, private equity-backed oil and gas companies, oil and gas wealth is in the hands of more and more individuals. Estate planners advising clients who hold these assets need to know how minerals, especially non-producing minerals, and oil and gas holding entities are valued and what the Treasury regulations have to say about determining the Fair Market Value (FMV) of oil and gas interests.

Nature of Interests

Before you can understand the valuation techniques, it’s important to know the exact nature of the oil and gas interests being valued. Does the client hold primarily working interests, royalty interests, or a combination of the two? Are the interests held directly or indirectly through an entity such as a family limited partnership (FLP)? The answers to these questions dictate valuation data sources and methodology.

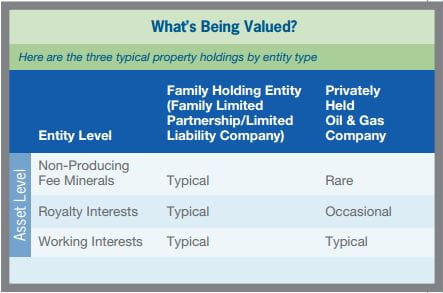

Here’s a simplified example, which helps to convey the definitions of, and differences among, various types of mineral interests. The most basic type of mineral interest is the fee mineral interest, representing a perpetual ownership of the mineral rights on a property, which may be separate from the land ownership. Consider a rancher who owns his land (surface rights) and underlying minerals in fee and is approached by an oil and gas company that has reason to believe oil and gas deposits may be found on (under) the ranch. The rancher may lease his minerals to the oil company in exchange for an upfront signing payment (a lease bonus) and a royalty interest in future oil and/or gas revenues. The oil company is the leasehold or working interest owner and pays all costs to drill and operate the lease. The rancher is the royalty interest owner and doesn’t bear any share of such expenses. If the rancher hasn’t leased his minerals, his ownership is called a “non-producing fee mineral interest.”2

Most of the research on oil and gas valuation focuses on working interests. Very little research has been published, and the Internal Revenue Service offers no guidance that I’m aware of, on the valuation of non-producing minerals.

Non-Producing Fee Minerals

Non-producing fee minerals are often owned directly by individuals or indirectly through FLPs or limited liability companies and often are involved in estate-planning transactions. For example, family ranches or farms (and underlying minerals) in south Texas (Eagle Ford shale), North Dakota (Bakken shale), West Virginia/Ohio (Utica shale) or Pennsylvania (Marcellus shale) have created dramatic wealth in recent years. Petroleum engineers (PEs) usually don’t want to provide valuations of non-producing minerals if geological and reservoir data don’t exist, so there are a limited number of valuation experts in this area.

In some cases, non-producing minerals are simply included with producing minerals in a valuation. For example, if the producing minerals (royalty interests) are valued using a cash flow multiple, the non-producing minerals often get overlooked and are implicitly assigned no value. Some clients will value the non-producing minerals at a token $1 per net acre, not knowing how else to do so. The best and most defensible approach for valuing non-producing minerals is to use a price per net acre multiple (the market approach) for an arm’s-length comparable mineral sale (as opposed to a working interest sale) that occurred near the valuation date. While this information has rarely been available in the past, our relationship with EnergyNet, Inc., an oil and gas advisory firm headquartered in Amarillo, Texas, allows us access to such data.3

In situations in which there isn’t sufficient market data or the subject non-producing minerals have significant value (because they’re located in an active area of exploration), an income approach can be used. Sophisticated mineral buyers who have geoscience and engineering professionals on staff rely on this approach. These professionals will develop a cash flow projection based on:

- Type curves or expected production profiles for nearby or

analogous wells- The number of rigs operating in the area

- Oil and gas price levels and economic return to operator’s

working interest- Lease terms in area or actual terms, if minerals

are leased- Unit sizes/current field spacing requirements in

the area (number of wells

The following factors impact the selected discount rate applied to

the projected cash flow stream:

- Whether minerals are already leased and, if so, the

operational and financial strength of the operator- Operational and mechanical risk

- Environmental risk (hydraulic fracturing and water use/

discharge issues)- Commodity price risk

It’s important to remember that a sophisticated valuation model may be built, but the subject minerals may never be leased, because oil operators in the area might, ultimately, deem them not prospective for exploration. The valuation must, therefore, consider the probability that the subject minerals won’t be leased and won’t generate income.

Another method for valuing non-producing minerals in an estate or gift tax valuation context is to rely on a simplistic approach called the “Multiple of Lease Bonus.” The method is to multiply the lease bonus per acre in effect at the valuation date, by the number of net mineral acres held by the client. The selected multiple or lease bonus per acre is increased if nearby drilling and production results are favorable.

Working and Royalty Interests

Income and market approaches can be used to value working and royalty interests.

Income approach. The predominant methodology for valuing working interests and royalty interests4 is an income approach, since it can be tailored to the specific property interest in question. The reserve (or engineering) report is the basis for this approach.

A PE prepares a reserve report, which contains a projection of the net cash flow the oil and gas interests are expected to generate. The PE will consider various geological and reservoir data to estimate the amount of remaining economically recoverable volumes of oil, gas, and natural gas liquids (the reserves) and the time at which such reserves will be brought to the surface and sold. The projection for each lease or well (the 8/8ths interest) is then netted to the subject interest. For valuation purposes, NYMEX oil and gas futures prices (NYMEX strip pricing), adjusted for basis differentials, are most commonly used. Lease operating costs (electricity, labor, and maintenance), taxes (severance and ad valorem), and capital expenditures for drilling additional wells are deducted. A pre-income tax cash flow projection results from this analysis. The reserve report will show a matrix of values resulting from discounting the cash flow stream at various discount rates.

For instance, the present value of the projected cash flow stream using a 10 percent discount rate is referred to as the “PV-10” value of the reserves.

The discount rate applied to the projected cash flows should properly account for the riskiness of the subject cash flow stream. The reserve report facilitates this process by categorizing the projected cash flow streams into various risk categories. The least risky category is the proved developed producing (PDP) reserves. The next categories on the risk spectrum include proved developed not producing (PDNP) and proved undeveloped (PUD) reserves. The sum of these three categories is known as “proved reserves” or “1P reserves.” Additional unproved reserve categories include probable and possible reserves.

There are three common methods for converting a reserve report to an FMV:

- Perhaps the most accurate, but admittedly anecdotal, approach is to interview or survey investment bankers or property brokers in the oil and gas acquisition and divestiture (A&D) market regarding discount rates in effect at the valuation date. Discount rates are dependent on reserve category, location, product type (oil versus gas) and size of transaction. For example, an A&D firm might show statistics indicating that oilweighted Permian Basin PDP properties were transacting at PV-75 near the valuation date.

- Another approach involves using data contained in an annual survey (the SPEE survey) conducted by the Society of Petroleum Evaluation Engineers.6 The SPEE survey polls about 100 experienced PEs and other experts who work in the context of A&D transactions. The section of the survey most commonly cited deals with risk adjustment factors (RAFs) used for acquisitions. The RAF isn’t a discount rate in the traditional sense, as used in the first method, but rather a “haircut” factor. While this methodology is simple, and the valuation conclusion is clear (and presumably defensible), it can be overused as a one-size-fits-all solution. For example, I interviewed an active property buyer in the Gulf of Mexico recently and found that use of the SPEE RAFs, without any further adjustment, would have significantly overvalued the offshore properties.

- Another source for the discount rate is the cost of capital7 for publicly traded guideline companies. The reserve base of the guideline public companies should be sufficiently comparable to the subject properties, particularly the ratios of PDP and PUD reserves to total reserves. This approach requires a number of adjustments to reflect the public companies’ general and administrative cost structure, growth profile and marketability, which aren’t characteristics of the subject static oil and gas reserve base.

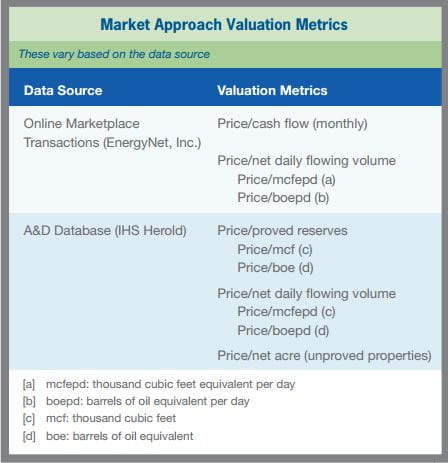

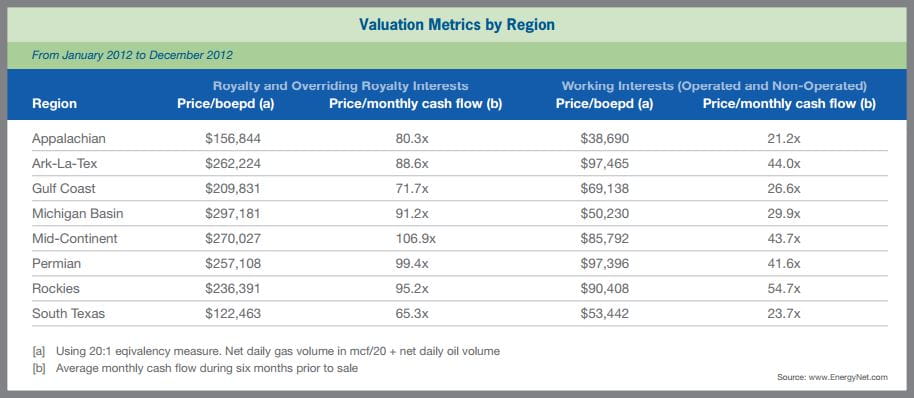

Market approach. The market approach involves applying comparable transaction metrics to the subject oil and gas property’s measures. Typical market approach valuation metrics are shown above, and sample valuation metrics by producing basin from January 2012 to December 2012 are shown on the following page. The drawback to this approach is the difficulty in finding comparable transactions. Oil and gas properties aren’t generic, and each property set can have its own unique profile. In determining whether a transaction is sufficiently comparable to the subject interest, consider whether the transactions have a similar:

- Time period (a similar oil and gas price environment)

- Basin and, if possible, same producing horizon

- Asset size

- Oil percentage of reserves

(oil versus gas-oriented transactions)- Percentage of reserves developed/undeveloped

- Reserve life ratio (proved reserves divided by current

production rate on annual basis – the r/p ratio)- Upside potential, a subjective factor

Entities Holding Properties

In most cases, valuation of the oil and gas properties is the first step in entity valuation. You may also need to value other assets, such as hedges, midstream assets, and leasehold acreage not previously considered. Using these values, the balance sheet is marked to market, and a net asset value is calculated once liabilities are subjected. I also consider the potential impact of the entity’s general and administrative cost and tax structures on valuation. Discounts for lack of control/minority interest and lack of marketability are also considered in an entity level valuation. Publicly traded guideline companies can also assist in the valuation if sufficiently comparable to the subject entity.

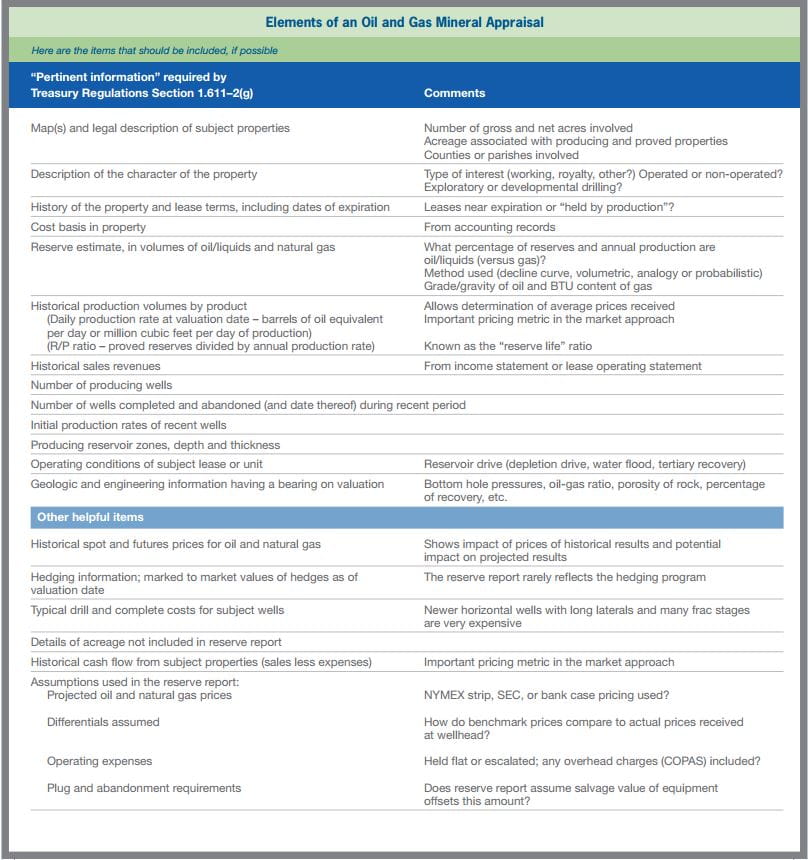

Treas. Regs. Section 1.611

While not specifically addressing estate and gift tax purposes, Treasury Regulations Section 1.611 provides some guidance with respect to determining the FMV of oil and gas properties. Treas. Regs. Section 1.611-1(d)(2) provides that “the fair market value of an [oil and gas] property is the amount which would induce a willing seller to sell and a willing buyer to purchase.” This language is consistent with the definition used for estate tax valuation (Treas. Regs. Section 20.2031-1(b)).

Section 1.611-2(d)(1) provides that “the value should be determined in light of conditions and circumstances known at the valuation date, regardless of later discoveries or developments.” This language is consistent with the general framework for estate and gift tax valuation precluding post-valuation date information.

Section 1.611-2(d)(2) says “the market approach (comparable transactions) is preferred to the income approach (discounted projected cash flows).” This provision isn’t consistent with current industry practice, which favors the income approach based on a reserve report as discussed previously. Treas. Regs. Section 1.611-2(g) lists information to be submitted in an FMV analysis.

The IRS’ Oil and Gas Handbook (Section 4.41.1.3.7.6) doesn’t add any new guidance on oil and gas property valuation, but rather refers back to Treas. Regs. Section 1.611.

1 Shale is a type of sedimentary rock composed of silt and clay. New technology has

allowed extraction of many shale deposits, which were once thought to be uneconomical.

2 Except for cases in which an oil company owns the fee mineral interest, it’s very rare for

a fee mineral interest owner to have the expertise or capital to drill a well and explore his

own mineral base; therefore, for the purpose of this article, unleased mineral interests are

essentially considered non-producing mineral interests.

3 EnergyNet, Inc.’s database isn’t publicly available, but it will assist clients with the sale of their oil and gas properties and will make valuation metrics available to such clients.

EnergyNet, Inc. is unique in that it markets not only traditional oil and gas properties, such as working and royalty interests, but also numerous fee mineral properties, including

non-producing fee minerals.

4 I combine working and royalty interests for this discussion. Market evidence described later in this article shows that cash-flow multiples for royalty interests are higher than working

interests. This implies that a distinction should be made in the valuation of the two property types, although such distinction is rarely made.

5 That is, PV-7 instead of the PV-10 shown in the reserve report. The projected cash flows in the reserve report would be discounted at 7 percent instead of 10 percent.

6 Survey of Parameters Used in Property Evaluation.

7 The (pre-tax) weighted average cost of capital is used.