English

English

Overview

A freeze partnership transaction in an estate planning context utilizes the financial attributes of preferred and common equity to transfer wealth from one generation to another in a tax-efficient manner. Typically, the senior generation is motivated to transfer wealth to the junior generation, but desires the security of a continued stream of fixed income. A preferred partnership is a limited partnership or LLC (“PLP”) with at least two classes of equity, including a preferred class and common class. The preferred interests may be issued in exchange for capital contributions at the inception of the PLP, or may be issued in exchange for interests in an existing family limited partnership or LLC as part of a recapitalization. This PLP structure is particularly beneficial when transferring assets that are likely to appreciate quickly. A transfer of a noncontrolling interest in the common equity of the freeze partnership further enhances the benefits of this technique, since valuation discounts for lack of control and lack of marketability may be warranted.

The term “freeze partnership” refers to the fact that the preferred equity class receives a fixed rate of return and any future appreciation in excess of that fixed rate of return benefits the common equity class. The benefits to the preferred equity class typically include liquidation and net cash flow preferences. For estate tax purposes, a preferred interest is valued by discounting the payment stream based on an appropriate current market yield, thus “freezing” its value.

Partnership freezes involving related party transfers are generally governed by Internal Revenue Code Section 2701 and the accompanying regulations. To the extent the provisions of Section 2701 are not followed, the preferred interest is assigned a value of zero, thereby allocating all of the equity value to the junior equity interest. This treatment acts as a penalty by artificially increasing the amounts subject to gift tax. In addition, any preferential rights granted to a preferred interest found not to be mandatory or “qualified” payment rights are disregarded. For example, if distributions to the preferred class are optional or noncumulative, a zero value could result. Section 2701 also requires the value of the common equity to be at least 10% of the total value of all partnership interests, plus total debt owed by the partnership to family members (i.e., the “10% minimum value rule”). Given the potential pitfalls associated with Section 2701, the preferred interest is typically designed to pay a fixed, cumulative, annual preferred return. In addition, the holder of the preferred interest is usually entitled to a liquidation preference of the priority return of contributed capital upon dissolution of the partnership.

From a planning perspective, there are many factors to consider in establishing the structure of a freeze partnership, beginning with the nature of the assets contributed. The risk and return attributes of the assets have a direct bearing on the determination of the appropriate market yield of the preferred equity in the PLP. In addition, consideration should be given to whether the assets generate sufficient income to satisfy the preferred dividend payments. Furthermore, the allocation of capital between preferred equity and common equity can have a significant impact on the analysis. A valuation analyst should be consulted early in the process of structuring a freeze partnership to assist with the determination of the financial impact associated with these decisions.

Valuation Guidelines

Revenue Ruling 83-120 outlines the primary guidelines established by the Internal Revenue Service for valuing preferred stock of closely held businesses and is also applicable in the analysis of preferred interests in freeze partnerships. Revenue Ruling 83-120 indicates the following factors should be considered:1

- Analysis of the stated dividend rate and the risk associated with this payment

- Identification of cumulative versus non-cumulative dividends

- Ability of the company to pay the preferred stock’s liquidation preference at liquidation

- Existence of voting rights

- Consideration of redemption privileges

Under these guidelines, the value of a preferred stock instrument is equal to the present value of the future cash flows expected from the instrument, using an appropriate market rate of return to discount the expected cash flows. The rate of return on the preferred stock, and thus its value, relates to its perceived risk.

Valuation Process

The first step in the valuation process is to determine the future cash flows that will be due to the preferred equity being valued. These projected cash flows will typically reflect the rights and preferences of such preferred equity pursuant to the PLP’s governing documents, such as the limited partnership agreement.

The second step is to establish an appropriate market yield on the preferred equity. In doing so, it is often necessary to perform an analysis of the expected returns on the PLP’s various asset groups and the PLP as a whole. This is accomplished through the identification of benchmark rates of return on securities with similar characteristics and features to the instrument being analyzed. In order to reflect an appropriate rate of return on the subject preferred interest, these benchmark rates of return are then adjusted based on the specific attributes of the credit quality and risk profile of the preferred instrument. The concluded market yield is then applied to the expected future cash flows to derive a determination of the Fair Market Value of the preferred equity.

Mathematically, the present value of a nonconvertible perpetual preferred stock is as follows:

- PV of Preferred Stock = Preferred Dividend/Market Yield

The following analysis is generally performed in the determination of an appropriate market yield for a specific preferred stock issue, including assessment of risk, identification of comparable preferred stock issues, and an analysis of qualitative factors.

Assessment of Risk

Pursuant to Revenue Ruling 83-120, the primary factors to consider in assessing the risk of a preferred stock instrument are its income protection and asset protection. Income protection refers to the extent to which earnings and cash flows may decline before the subject company is rendered unable to meet its regularly scheduled dividend payments. Income protection is generally measured through the calculation of the subject company’s fixed charge coverage ratios. A higher coverage ratio reduces the risk that the subject company will be unable to make its regular dividend payments, thus indicating a lower yield is applicable, all else held constant.

Asset protection relates to the likelihood of an investor receiving full liquidation payment in a liquidation scenario. In other words, after all outstanding liabilities have been settled, this factor measures the likelihood that the company will be able to satisfy its obligations to the preferred equity class. The higher this coverage ratio, the greater the protection afforded to the preferred equity holder in a liquidation event, thus indicating a lower applicable yield, all else held constant.

Identification of Comparable Preferred Stock Issues

In addition to the ratios described herein, an analysis of several other financial ratios is often considered in order to determine the appropriate market yield of the preferred equity being valued. These ratios are used to compare the financial attributes of the subject company with publicly traded companies that have preferred stocks with similar rights and privileges. Ideally, it is best to identify publicly traded securities that have features similar to the subject preferred equity, such as maturity, issuance date, PIK, and conversion features. Once a comparative group of publicly traded preferred stocks is identified, it is necessary to identify the rating assigned to each preferred stock by certain rating agencies. Analysis of the indicated yields of the comparable publicly traded preferred stock is used to determine the appropriate market yield applicable to the preferred equity of the subject company.

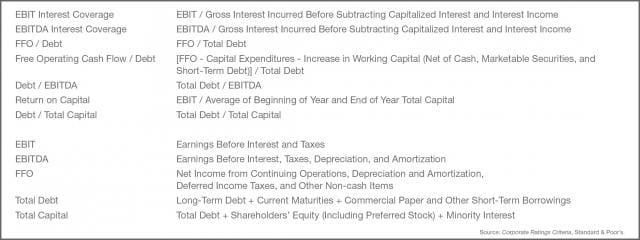

Definitions of Ratios and Components

Analysis of Qualitative Factors

In addition to quantitative analysis, it is also appropriate to consider certain qualitative factors in assessing the risk of a particular preferred equity instrument. In fact, the rating agencies analyze qualitative factors in detail when assigning individual ratings to preferred stock. These factors may include the industry and economic outlook, competitive environment, depth of management, federal regulations, ability of lenders and stockholders to affect dividend policy, and trends in revenue and supply sources.

Determination of Market Yield – Case Example

The following example presents a credit rating analysis used to determine the market yield for preferred equity of FreezeCo, LP (“FreezeCo”), an industrial manufacturing company that is being recapitalized to accommodate planning as a freeze partnership. Certain financial ratios were considered and calculated for the company based on its historical three-year average results. These ratios were identified as those commonly considered by industry analysts in evaluating the economic strength of companies, and are thus utilized in our analysis in order to indicate an appropriate rating category to use in identifying comparable preferred securities.

Credit Rating Analysis

Because FreezeCo, a closely held company, does not currently maintain a corporate credit rating, we calculated its financial ratios as outlined in Standard & Poor’s (“S&P”) Corporate Ratings Criteria and compared those ratios to those outlined in S&P’s 2011 Adjusted Key U.S. Industrial and Utility Financial Ratios.

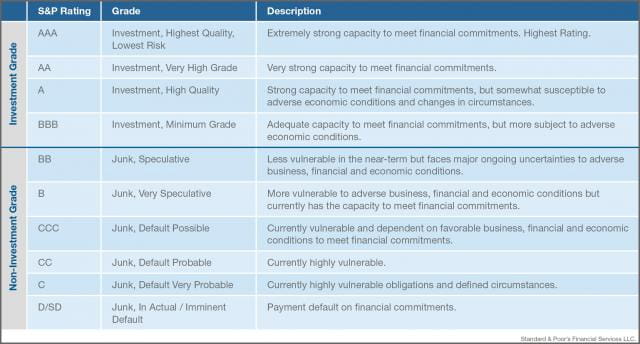

S&P provides credit ratings for an issue based on the creditworthiness of an obligor with respect to a specific financial obligation, a specific class of financial obligations, or a specific financial program. It should be noted that each of these ratios incorporates the debt service obligations of a company, but not the preferred stock obligation. Any outstanding debt obligations are senior to the preferred stock issues and a company must make its interest payments prior to paying preferred stock dividends. Similarly, in a liquidation scenario, long-term debt obligations must be satisfied before liquidation proceeds are distributed to the preferred stockholders. A summary of these ratios, segmented by S&P credit rating, is provided in the following table.

Standard & Poor's - Key Industrial Financial Ratios, Long-Term Debt

Based on FreezeCo’s three-year average operating results and capital structure, an appropriate corporate credit rating applicable to the company’s long-term debt was determined to be rated “A.” The dividend payments and liquidation preferences of a preferred stockholder are inferior to debt holders. For this reason, as outlined by S&P, preferred stock is generally rated lower than debt. Specifically, when a firm’s corporate credit rating (“CCR”) is considered investment grade, its preferred stock is typically rated below its CCR. Investment grade is defined as those issues maintaining a rating in the four highest categories, including AAA, AA, A, and BBB. Debt rated as BB or lower is generally considered speculative grade, for which preferred stock is typically rated three notches (or one rating category) below its respective CCR. Based thereon, an appropriate rating attributable to FreezeCo’s preferred stock is determined to be BBB.

Analysis of Publicly Traded Preferred Stock

Based on FreezeCo’s indicated preferred stock rating, we have analyzed the yields of 236 publicly traded preferred stock issues in the industrial category and the yields of 235 publicly traded preferred stock issues rated BBB. This analysis is presented in the adjacent chart.

Preferred Rates of Return

Based on FreezeCo’s indicated preferred stock rating, the yields of publicly traded preferred stock, and in consideration of certain specific factors, a base market yield of 5.0% is selected. The indicated preferred stock yields are based on securities that are publicly traded. Given the specific risk factors impacting the preferred interest relative to publicly traded securities, such as lack of marketability and the potential for subordination, a 200 basis point adjustment is applied in the instant case to yield a concluded market yield of 7.0%.

Concluded Preferred Rate of Return

Other Considerations

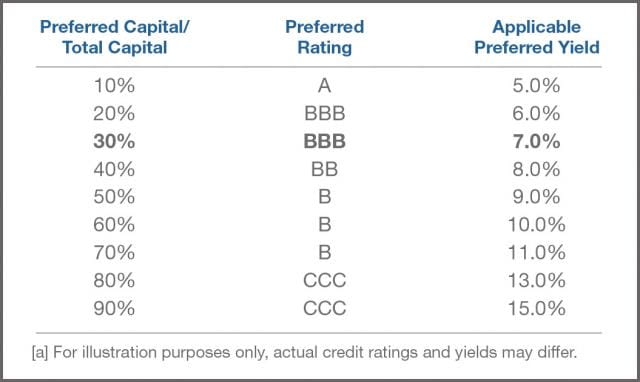

In selecting an appropriate yield, it is important to consider that as the proportion of the PLP’s preferred equity increases in relation to the Fair Market Value of the entity’s total capital, the appropriate market rate of return for the preferred interest will approach the entity’s market rate of return of the equity. Conversely, as the proportion of the entity’s preferred equity decreases in relation to the Fair Market Value of the entity’s total capital, the return for the preferred interest will trend towards the entity’s debt rate of return.

Sensitivity Analysis [a]

Once the appropriate market yield is determined, it is then applied to the expected future cash flows of the preferred equity to derive a determination of the Fair Market Value of the preferred equity. To the extent the estate planning transaction includes a gift of a noncontrolling interest in the common equity of an entity, additional steps include subtracting the preferred equity value from total equity value to derive the value of common equity and applying valuation discounts to the common equity interests.

Conclusion

Valuation analysts play a key role in assisting estate planners with freeze partnership transactions. Successful planning is achieved by involving valuation analysts early in the process of designing the attributes of a preferred security. A consultative process will allow estate planners to make informed decisions on factors impacting the appropriate preferred rate, to avoid the potential pitfalls associated with Section 2701, and to ensure the client’s objectives are met.

1 Rev. Rul. 83-120, 1983-2 C.B. 170.