English

English

In a panel discussion during the Stout Summit: Investment Funds and Alternative Assets, Elizabeth Kettler, Director in the Accounting & Reporting Advisory practice of Stout’s Transaction Advisory group, led a discussion on ESG (environmental, social, and governance) and its relevance to value creation within companies. The panelists included:

- Jamie Spaman, Managing Director, Stout

- Chris Hagler, Partner, ESG, Independence Point Advisors

- Sheffield Goodrich, Managing Director, ESG, Independence Point Advisors

This interview has been edited for length and clarity.

Elizabeth Kettler: To begin, can you provide some background on ESG and sustainability?

Chris Hagler: Companies have wanted to do the right thing for a while – they’ve had charitable foundations and been involved in philanthropic activity activities. Now this has shifted from being a nice to-do to a fiduciary responsibility.

ESG is a set of topics that a company should prioritize and take action on if/when they drive value for that organization or demonstrate a meaningful impact for stakeholders. Both investors and companies are looking at ESG issues.

Sustainability is the act of conducting your business in a way that is responsible as it relates to the materials that you use, and in a way that is respectful of the people in your organization and your community. Sustainability is about doing things in a way that enables the world to still be around for future generations.

Elizabeth Kettler: Can you create value with ESG initiatives?

Sheffield Goodrich: Yes, you can. There’s a diversity of the clients we work with, all at various levels of maturity in their approach to ESG through a value protection or value creation standpoint.

We started working with a client where the whole conversation began around compliance. As we had more discussions, it quickly pivoted to “So the SEC is asking us for this, but our customers actually have more advanced requests around understanding the greenhouse gas footprint of our products.”

After we worked with them to get an inventory of their greenhouse gas footprint, the engineers in the room looked at that data and said, “Wait, there are efficiency gains here. Now that we have all this data on the amount of energy that we use and the waste, let’s try to cut out as much as possible so that it can provide savings to the bottom line.”

After working with them for quite some time, we’re starting to have discussions about new products and services that they can offer to their clients that would help them address a need and help their clients’ interests.

Elizabeth Kettler: How does ESG lead to direct value creation?

Chris Hagler: There are factors like improved reputation and reduced risks — these are a bit harder to measure, but they are absolutely real. Improved reputation can improve turnover rates with your employees, or you can avoid risks to your reputation from a marketing perspective.

From a reduced risk perspective, these are very real risks that companies face as it relates to ESG topics. Safety, for example: If you can reduce your safety risks, you can reduce your costs as it relates to your safety reserves or your insurance.

There are factors that are a little bit more tangible as it relates to driving value. For example, increased revenue can come directly from ESG when building a business model around solving an ESG or sustainability challenge. For example, a food company could create a product line for organic food that is made without harming the environment. Or, in the business-to-business world, an Internet-Of-Things sensor could allow a manufacturing plant to run more efficiently, saving money while also advancing ESG initiatives.

Elizabeth Kettler: From your perspective, how does ESG factor into a company’s valuation?

Jamie Spaman: If you’re spending less on energy, that’s an easy translation to more profit that’s going to either increase your cash flows or increase your performance relative to your peers. Higher revenues and better margins all flow to the bottom line and increase cash flow.

Improved reputation is a little harder to quantify into a valuation model — maybe it shows up a little bit in higher revenues; because you have a better reputation, you’re able to attract more customers who are trying to achieve their own ESG goals. There can also be valuations benefits from reduced risk due to having a stronger customer base or less volatile cash flows.

Elizabeth Kettler: What is important to know about the upcoming disclosure rules proposed by the SEC, and what are the points that are being re-evaluated based on the comment letters received?

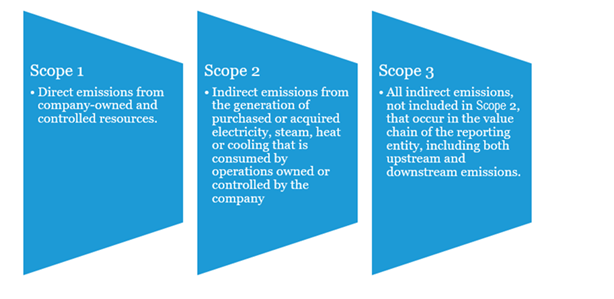

Sheffield Goodrich: First, you must understand your inventory of greenhouse gas (GHG) emissions. You may hear the terms “Scope 1, 2, and 3” being thrown around, and each has different disclosure requirements; essentially, the emissions for scope one and two that are being emitted by your organization, and scope three gets into broader value chain. We’re certainly all waiting to hear what ultimately gets determined on scope three – whether there will be a requirement for an audit.

Then there are disclosures of how climate is embedded into an organization’s governance, strategy, risk management, and metrics and targets. Those are the four components of the Task Force for Climate-related Financial Disclosures (TCFD) and the four biggest recommendations that the SEC’s rule is broadly based upon.

In summary, organizations need to think about the following: What is our inventory? Is that inventory of investor grade that can be reported on? And how do we embed climate risk into disclosures around governance, strategy, risk management, and metrics and targets?

Chris Hagler: Reporting to the SEC about climate risk isn’t exactly new. It’s been required since 2010. But, until now, a lot of companies basically put boilerplate information. But over the last couple of years, the SEC has gotten a little picker about enforcement. Now, a company must do more than just identify whether climate change could / could not be a risk to itself. There is now guidance on how you should look at climate-risk impact to your company, and how you should disclose it. This considers both the rule itself and how much the SEC decides to enforce the rule.

Elizabeth Kettler: What can companies do now to improve their ESG strategy?

Sheffield Goodrich: We recommend our clients form a cross-functional working group and start assessing the quality of their current disclosures. Look at all the current ESG reporting (e.g., to investors or the EPA) and do a gap analysis comparing this to the proposed SEC rule.

Chris Hagler: The other thing to remember is to gather the information and understand it for yourself, for operating your own organization, and then decide if, when, and how to disclose the information. It’s good management — focus on understanding the information first.