English

English

The frequency of mergers and acquisitions (M&A) in the residential development (or homebuilding) industry is generally tied to the cyclical nature of the housing industry itself. In periods of measured growth, with increases in both home values and new construction activity, the M&A market is very active. Conversely, in times when the real estate market is depressed, the M&A market generally retracts until the residential market begins to show signs of improvement.

Given the recent growth in the housing industry, the number of mergers and acquisitions in the residential developer industry through midyear 2017 already matched the total for the previous year. Additionally, U.S. residential development companies are being acquired by buyers from the global market (primarily Japan, China, and Europe) as these outside investors look to capitalize on the growing U.S. market. Several years ago, this would have been considered an anomaly, as most transactions involving residential developers included only U.S. companies, with limited global interest.

In a transaction involving a residential development company that complies with U.S. generally accepted accounting principles, a purchase price allocation (PPA) is required to satisfy financial accounting requirements. A PPA is the process of allocating the transaction price to the various tangible and intangible assets and liabilities acquired in the transaction under the “fair value” premise. Specifically for the real property component of the PPA, fair value is typically allocated among land, building, and site improvements for conventional owner-occupied real property.

Within the context of a purchase of a residential development company, the bulk of the assets acquired consist of the real property assets – which would primarily include subdivisions under various stages of development. Intangible assets and liabilities relating to the business would also be assigned a fair value, though the business enterprise value typically makes up a small portion of the overall purchase price. The majority of the purchase price is tied to the real property. The following case study outlines the typical stages of development for a residential subdivision at the time of acquisition, the appropriate valuation methodology to determine fair value, and an allocation of said fair value between land and building improvements.

Case Study – A Closer Look at the Acquisition

In the following example, assume that an acquirer purchased a regional residential development company. At the time of the transaction, the company maintained 50 active subdivisions under development and 10 subdivisions planned for future development. In addition, 10 land sites are not yet owned by the company but have land purchase option agreements in place for potential future residential development. As part of the PPA, the fair value of the real property associated with a subdivision is typically allocated between land and building value.

Approaches to value

Current real property appraisal theory includes consideration of several appraisal approaches, including a Cost Approach, a Sales Comparison Approach, and an Income Capitalization Approach. A specific appraisal assignment may use one or more of these valuation approaches based on the definition of value and on the quality and quantity of data available for the analysis.

In a subdivision analysis, the Sales Comparison Approach and the Income Capitalization Approach are the primary methods applied to determine fair value. The Sales Comparison Approach is applied to estimate the land value for unentitled land, as this is raw, undeveloped land with no government approvals in place. The value of the land associated with an active or entitled subdivision is estimated using the subdivision development method of the Income Capitalization Approach. In this approach, a form of discounted cash flow (DCF) analysis, direct and indirect costs are deducted from an estimate of the anticipated gross sales price of the finished homes, and the net sales proceeds are discounted to a present value at a market-derived rate over the development and absorption period.

Stages of subdivision development

The initial step in the analysis is to identify the stage of development for each subdivision, as this will drive the appropriate approach to value and the corresponding input assumptions. The various potential stages of development in an assumed transaction, and the appropriate valuation methods for each, are as follows.

Active subdivisions – These are subdivisions that are in the sell-off period as of the acquisition date. Active subdivisions generally include four components: 1) vacant lots or home sites remaining to be sold, 2) homes under construction, 3) model homes, and 4) homes under contract but still under construction. Active subdivisions are valued using the Income Capitalization Approach (subdivision development method).

Active subdivisions (with option lots) – Certain active subdivisions may include option lots. These lots are part of an active subdivision but are not owned by the company as of the acquisition date. Instead, they are under contract for purchase at a specified later date (with the purchase price and timing based on a “takedown schedule” included in the land purchase contract). Active subdivisions (with option lots) are valued using the Income Capitalization Approach (subdivision development method). The purchase price and corresponding future sale of the option lot are modeled into the DCF analysis.

Future subdivisions – These are land sites that are either entitled for future residential development, or unentitled and still awaiting government approval before development can commence. Future subdivisions that are entitled (meaning that all plans and approvals are in place) are valued using the Income Capitalization Approach (subdivision development method), given that development is expected to begin in the near term. Unentitled, raw vacant land is valued using the Sales Comparison Approach because government approvals are not in place and development will not likely occur in the immediate future.

Land purchase option contracts (“option contract”) – These are parcels of land that have been earmarked for future development by the company. These parcels are not owned by the company as of the acquisition date. Rather, the company has entered into a land option contract with the land owner to purchase the land at a predetermined price once all government approvals (entitlements) are obtained. Typically, under these contract agreements, the company is responsible for obtaining all entitlements.

Within the PPA, it is important to quantify any value that the acquirer might realize through the assumption of an option contract. Under typical scoping parameters, option contracts signed within 12 months of the acquisition date are assumed to be at market and would have no material value to the acquirer. Additionally, option contracts that have a low probability of obtaining site plan approvals and moving forward with development, as identified by the company, are generally excluded from the valuation. All option contracts that fall outside of these scoping parameters are typically included in the valuation to determine the fair value of the option contract. Option contracts are valued using the Income Capitalization Approach (subdivision development method).

Valuation scenario #1 – Active subdivision

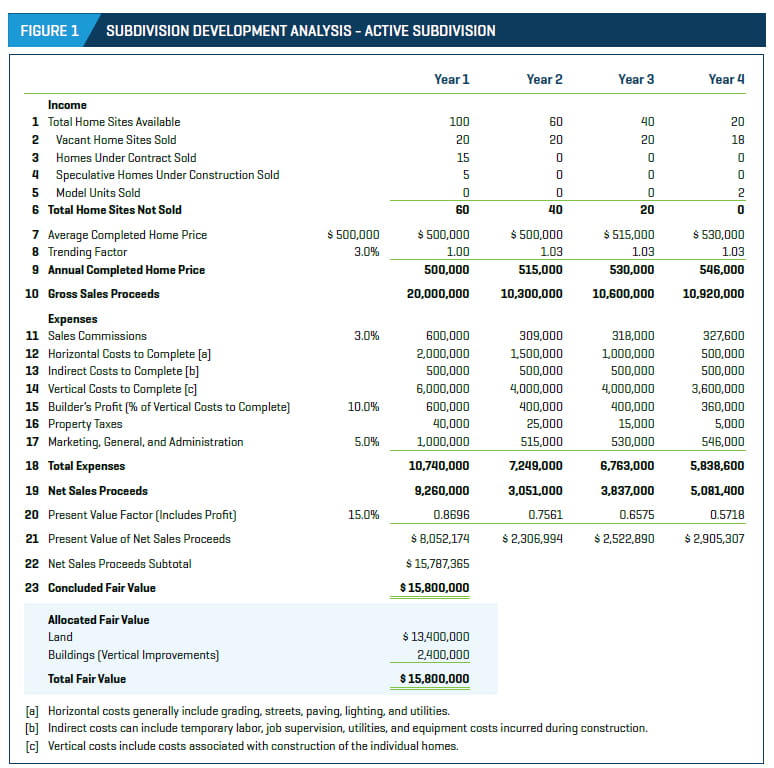

In the valuation of an active subdivision, the subdivision development method of the Income Capitalization Approach is applied. As shown in Figure 1, gross sales proceeds are estimated by determining the total number of housing units sold in each respective year of the absorption period until a complete sell-out of the subdivision has occurred. In this example, the subdivision is expected to have a complete sell-out of all housing units in four years. Income is generated through the sale of vacant home sites (including the purchase of the home), homes under contract as of the acquisition date (with construction not yet complete), speculative homes under construction, and model units. After determining the gross sales proceeds, expenses and holding costs must be deducted in order to determine the net sales proceeds. Typical expenses to the developer include sales commissions, cost to complete horizontal and vertical improvements (infrastructure and individual homes), indirect costs, builder’s profit, and marketing/general administrative costs.

The discount rate, which is applied to the net sales proceeds to calculate the present value of the annual cash flows, is a critical assumption in the analysis, as it reflects the risk associated with the sell-off of each subdivision. Additionally, the discount rate typically includes entrepreneurial profit, which is the profit that the developer expects to receive for its contribution to the project. The discount rate is determined through several data sources, including national investor surveys and discussions with market participants, along with property-specific characteristics such as location and length of the sell-off period. In an acquisition of 50 subdivisions, the discount rate will likely vary among properties as the individual characteristics of each subdivision are taken into consideration.

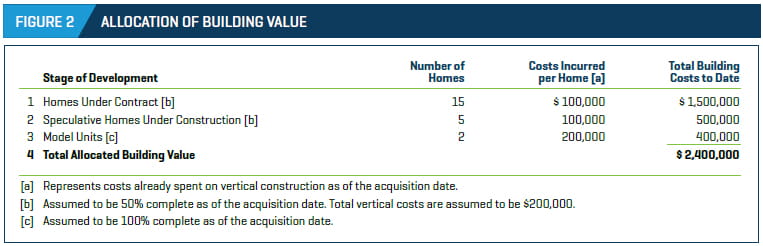

The final step is to allocate the fair value between land and building improvements. In this case, building improvements represent the completed or partially completed vertical improvements associated with the homes under contract (with partially complete construction), speculative homes under construction, and model homes. The allocated building value is equal to the vertical costs incurred as of the acquisition date for the building improvements. As shown in Figure 2, the allocated building value is $2.4 million. Thus, the remaining $13.4 million is allocated to the land (as shown in Figure 1).

The valuation for future subdivisions that are entitled for development would follow an approach similar to the one displayed in Figure 1. However, the key differences would likely be 1) a longer ramp-up period to begin sell-off of the home sites, and 2) a higher discount rate given that the development is at the beginning stage as opposed to the middle or end of the sell-off period.

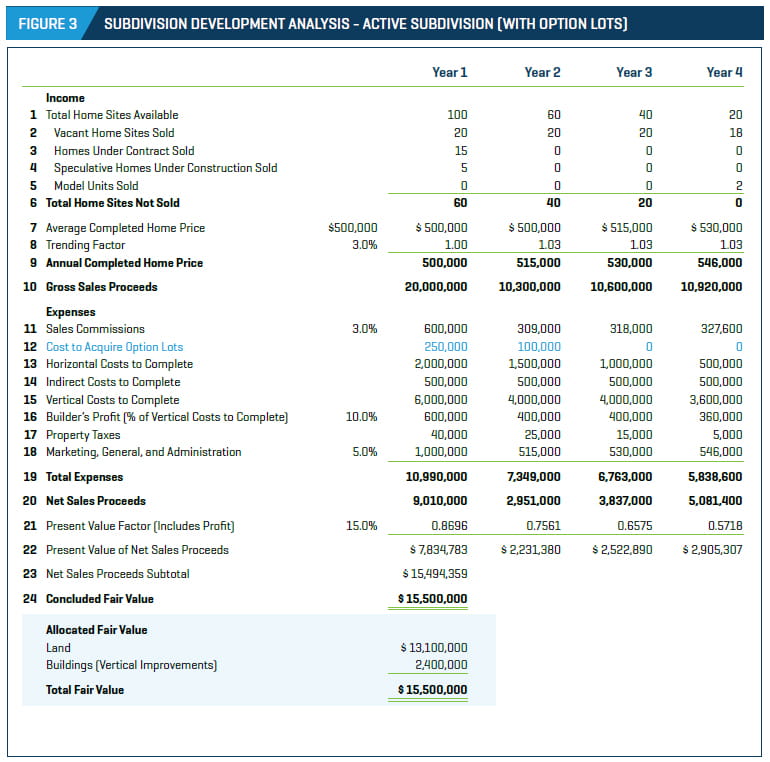

Valuation scenario #2 – Active subdivision with option lots

The Valuation Approach for active subdivisions with option lots is similar to the analysis presented in Figure 1, with one caveat. Because option lots are not owned by the company as of the acquisition date, the cost of acquiring such lots must be factored in to the cash flows. In Figure 3, the cost to acquire the option lots is shown as a line item expense, as all other inputs and assumptions remain similar.

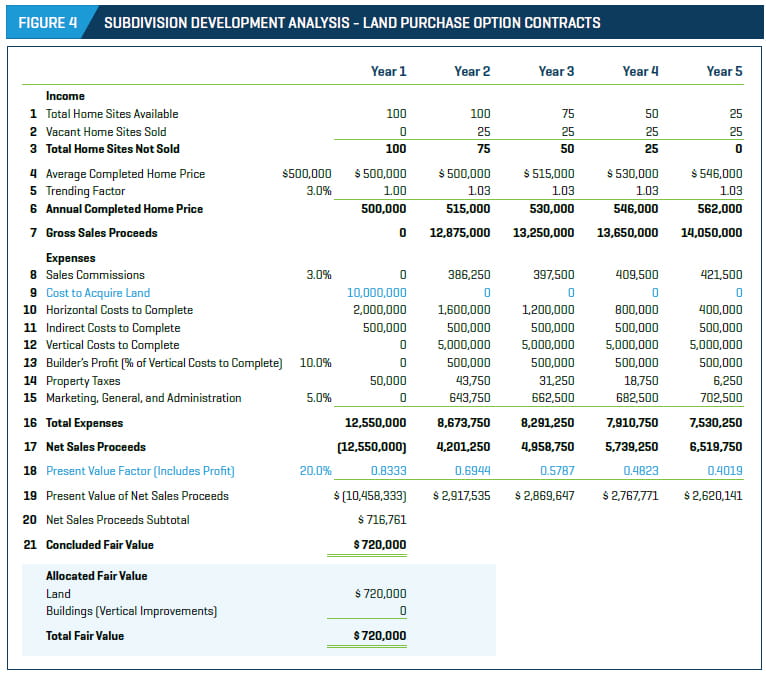

Valuation scenario #3 – Land purchase option contracts

The subdivision development method is also applied in the valuation of an option contract. In this case, because the land is not owned by the company as of the acquisition date (rather, the land is under contract for purchase), the purchase price of the land must be modeled into the analysis. Additionally, the discount rate should be increased to reflect the risk associated with a subdivision that has not obtained all government approvals and is at the early stages of planning and development. Figure 4 outlines the Valuation Approach and allocation for an option contract analysis. Because there are no vertical improvements on the land as of the acquisition date, all of the value is allocated to the land.

Obtaining Credible Results

As with any PPA assignment, it is imperative to work with the client and the audit team to develop a scope of work that creates credible valuation results. In this case, the client is an informed investor in this property type and thus has valuable industry knowledge that can be used in the appraisal process. Additionally, internal company models, which typically detail the historical and expected future performance of each subdivision (including prior home sale prices and construction costs), can be used to formulate certain key assumptions in the valuation.

An acquisition of a residential development company presents many unique challenges from a real estate valuation perspective, given the varying stages of development that may be in place as of the acquisition. An understanding of the valuation methodologies associated with a subdivision development will be key in producing a credible estimate of fair value that can be used as part of the greater purchase price allocation.