Deutsch

Deutsch

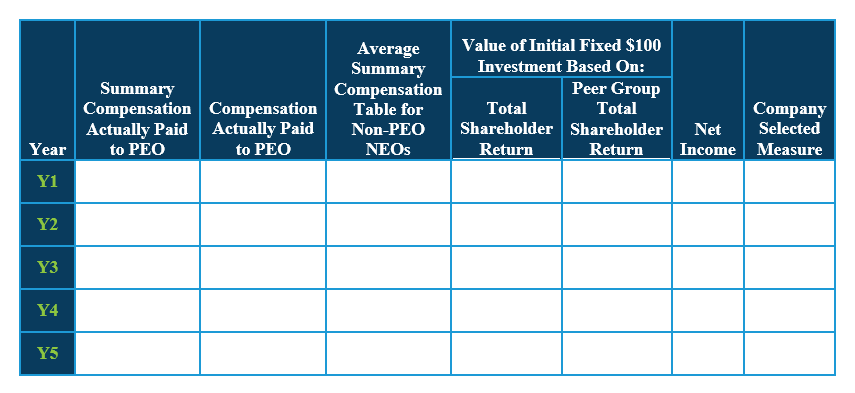

The Securities & Exchange Commission (“SEC”) has adopted new annual compensation disclosures requiring reporting companies (except foreign private issuers), registered investment companies, and emerging growth companies to disclose the relationship between executive compensation actually paid and a company’s financial performance for the previous three years beginning with fiscal years ending after December 16, 2022, with an additional year added for the next two annual reporting periods, for a total of five years (three years total for smaller reporting companies). These new compensation disclosures are incremental to the current annual compensation reporting requirements and are required to be presented in a tabular format similar to the table below.

Determining the compensation actually paid to executives will be more complex for equity-based awards issued to executives.

Unvested equity-based awards will need to be reported in the table at fair value as of the effective date of the disclosure (as opposed to grant date fair value), with changes in fair value of unvested equity-based awards reported in each reporting period.

This will require companies to use a valuation framework in order to estimate fair value. Equity-based awards for which fair value will need to be determined include, but are not limited to, the following:

- Stock options

Typical valuation framework – Option Pricing Model - Total shareholder return awards

Typical valuation framework – Monte Carlo Simulation - Option or restricted unit grants with “market-vesting” conditions (i.e., stock price targets or trading thresholds)

Typical valuation framework – Monte Carlo Simulation - Restricted unit grants with time or “performance-vesting” conditions (i.e., financial metric targets)

Typical valuation framework – n/a, public stock price is relied upon in most cases

For the initial year of adoption, we recommend companies begin preparing the required compensation disclosures for the two earliest reporting periods as soon as possible, given the effort and learning that may be involved. Additionally, while it may or may not be required for compliance with Section 404 of the Sarbanes-Oxley Act, companies should determine whether appropriate internal controls over the fair value of equity-based awards and the related new disclosures should be established to help ensure such disclosures are complete and accurate.