Fed Rate Hike and the Impact on the Emerging Markets

Fed Rate Hike and the Impact on the Emerging Markets

The proposed termination of the U.S. Federal Reserve System’s (the “Federal Reserve”) zero rate policy has enhanced the concerns of hyper volatility and possible crisis in the capital markets of emerging market economies. The fear is completely understandable: global equity markets dropped sharply after the Federal Reserve indicated in May 2013 the expected tapering of its quantitative easing policy (“QE”). This tapering resulted in significant capital outflow, sharp currency depreciation, and increased market volatility for the emerging market economies.

As the excessive supply of liquidity will start evaporating post the hike in the federal rate, what will happen to the emerging market economies? Will they be able to maintain their reputation as lucrative investment destinations or is another financial crisis looming on the horizon?

This is How it all Started

The Federal Reserve undertook extraordinary measures to restore the financial well-being of the U.S. economy post the 2008 global financial crisis. The QE was primarily implemented by buying the treasury bonds and other assets in large quantities, which drove the short-term interest rates near zero and reduced the long-term interest rates in the U.S.

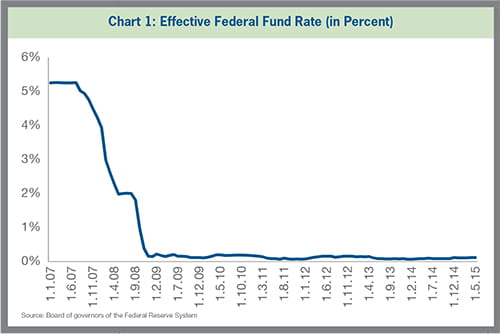

On December 16, 2008, the Federal Open Market Committee decided to maintain the federal funds rate near zero. From December 16, 2008, to June 30, 2015, the Indian benchmark index — NIFTY 50 (“Nifty”) — ascended from 3,041.75 to 8,368.50, yielding an annual rate of return of approximately 17 percent. During the same period, the Chinese benchmark index — SSE Composite Index — increased from 1,976.82 to 4,277.22, yielding an annual rate of return of 12 percent.

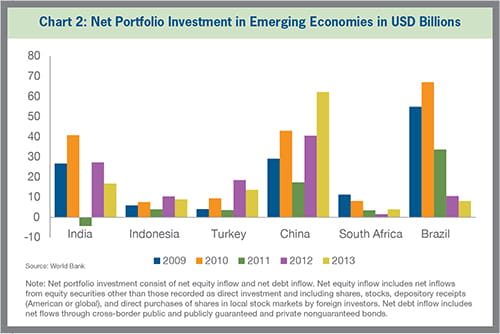

From 2009 to 2013, the emerging markets saw the net portfolio investment of USD 588 billion, led by China with net portfolio investment of USD 192 billion, followed by Brazil and India with net portfolio investment of USD 174 billion and USD 107 billion, respectively.

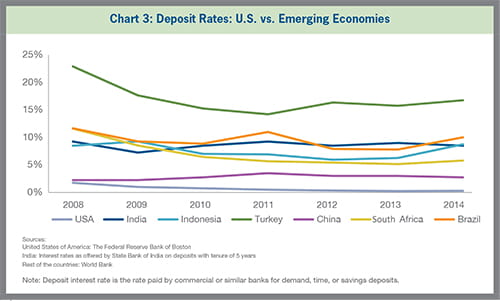

Lower interest rates did play a role in supporting the struggling U.S. economy, but it also created an artificial supply of liquidity. Lower cost of capital coupled with a potential opportunity to earn a higher rate of return prompted portfolio managers to invest heavily in financial assets of the emerging market economies. Bank deposit rates in the U.S. dropped from 1.75 percent in 2008 to 0.25 percent in 2013. During the same period, deposit rates in India remained in the range of 7 to 9 percent. Chart 3 shows the comparative advantage enjoyed by the emerging market economies vis-à-vis the U.S. in terms of bank deposit rates. Even after factoring the applicable default and exchange rate risks, investing in the emerging market economies was an attractive proposition for most portfolio managers.

Lessons from History

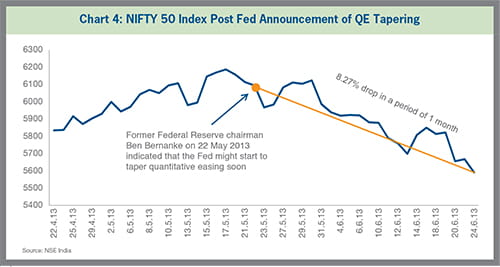

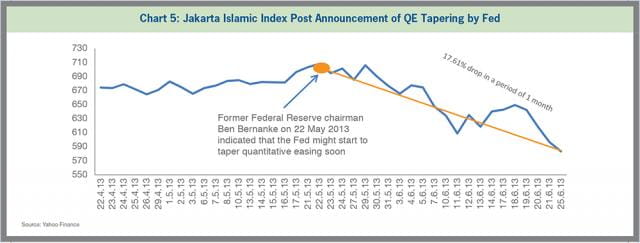

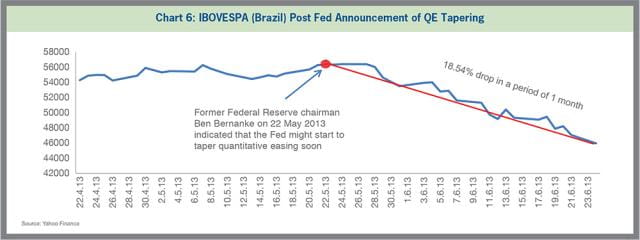

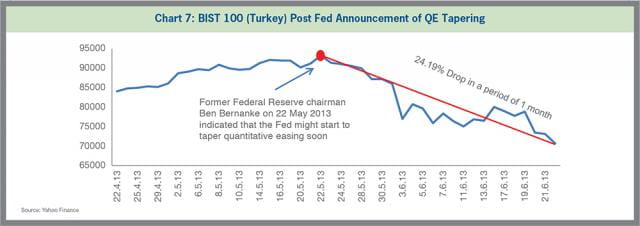

Although history does not always repeat itself, it can be a good indicator of future events. Global equity markets dropped sharply in May 2013 after the former Federal Reserve Chairman, Mr. Ben Bernanke, indicated that the Federal Reserve may start to taper the QE soon. Post the announcement, the emerging markets saw significant capital outflow, sharp currency depreciation, increased market volatility, and higher long-term interest rates. The impact was more acute for those countries that had large current account deficits, limited public finances, and large borrowings in foreign currency. Nifty declined by 8.27 percent in the month following the announcement of the tapering of QE. Similarly, the Jakarta Islamic Index, IBOVESPA — the Brazilian benchmark stock index — and BIST 100 — the Turkish benchmark stock index — lost 17.61 percent, 18.54 percent, and 24.19 percent, respectively, during the same period.

Historically, investors have reacted negatively to a fed rate hike. There have been 16 incidents of fed rate increases since World War II and the S&P 500 index experienced a decline of 5 percent or more during 80 percent of those instances. Today, in a world without borders, where global capital markets are intertwined, negative impacts on the emerging market economies cannot be ruled out, especially on countries with weak fundamentals.

Why is the Federal Reserve Raising the Fed Rate?

By keeping the short-term interest rates near zero for the past few years, the Federal Reserve has achieved most of its intended objectives. Low interest rates played its role perfectly in stimulating economic activity, whereby it spurred business spending on capital goods — an essential catalyst for an economy’s long-term performance. It also encouraged U.S. households to spend on housing and consumer durables. Low interest rates also proved to be an effective tool in improving the balance sheets of U.S. banks and thus their lending capacity.

For every benefit there is a price to pay, and so has been the case with maintaining low interest rates. Low interest rates contributed to the housing boom and increases in U.S. household debt levels. Artificially keeping interest rates low for an extended period of time may lead to high inflation. Further, low interest rates provide strong incentive to spend rather than to save. Keeping the fed rate low for an extended time period poses a risk of an overheated stock market, and all of the accomplished economic gains of the previous few years may reverse if the monetary discipline is ignored. Given the overall health of the U.S. economy, the downturn associated with higher interest rates looks minor compared to the very real danger of an asset bubble formation that could reverse the hard-earned economic gain if it bursts.

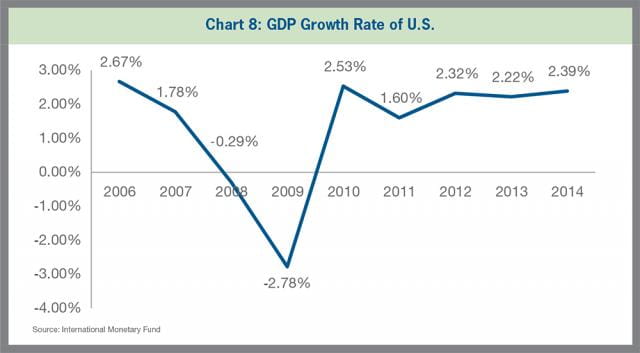

So far, the Federal Reserve has taken steps consistent with the new economic situation. Most notably, the Federal Reserve scaled down its bond buying program from USD 85 billion a month to USD 15 billion a month. Recently, the U.S. economy is on a stronger footing than ever during the last decade. Real GDP of the U.S. grew by 2.39 percent in 2014 and is expected to grow by 3.14 percent in 2015 (as projected by the International Monetary Fund). If this projected growth rate is achieved, it would be the highest growth rate for the U.S. economy in a decade (as shown in Chart 8).

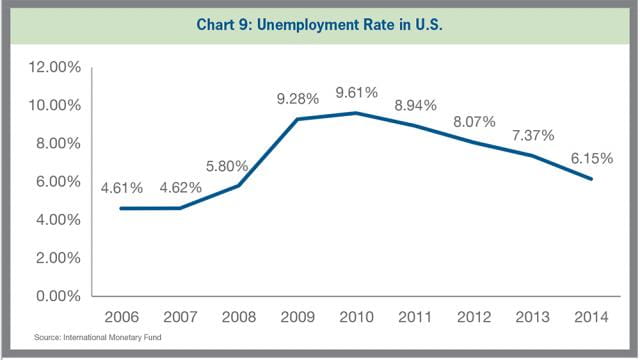

U.S. GDP growth has been accompanied by strong employment creation, as labor market conditions have improved significantly during the last five years. The unemployment rate has gradually decreased from a peak of 9.28 percent in 2009 to 6.15 percent in 2014 and is expected to further decrease to 5.47 percent in 2015 (as projected by the International Monetary Fund). The Consumer Price Index has also dropped significantly from 3.14 percent in 2011 to 1.61 percent in 2014. Although, inflation has declined below the Federal Reserve’s long-term goal of 2 percent, inflation is projected to rise gradually toward 2 percent over the medium-term on account of the improved labor markets and stability in energy prices.

By law, the Federal Reserve has statutory objectives to achieve maximum employment, stable prices, and moderate long-term interest rates. The macroeconomic data clearly indicates that employment and inflation are close to targeted objectives of the Federal Reserve. Therefore, raising the fed rate is consistent with legally mandated objectives for the Federal Reserve.

Impact of Fed Rate Hike on the Emerging Market Economies

The Federal Reserve’s actions often create a domino effect. In open market and global economies where the United States is the prime source of capital, action by the Federal Reserve will surely make ripples in the financial markets.

It is often said that “whenever the Federal Reserve sneezes, the emerging markets catch a cold.” Being a lower priority in global asset allocation, emerging markets are the first to have allocations withdrawn or reduced in an event of a crisis. A fed rate hike makes emerging markets significantly vulnerable as it ends an era of easy money, at least in the near term. During the period of near zero fed rates, this easy money was channelized into the global equity markets (including the emerging market economies). With higher interest rates, access to that money gets costly and the probability of an outflow of excess money from the emerging market economies becomes elevated.

Most of the emerging market economies are at the peak of the interest rate cycle and are on a path of gradual rate cuts. An interest rate cut in the emerging markets and a hike in the U.S. will negatively impact the risk return profile of the emerging market economies. The Federal Reserve action will essentially make the U.S. markets more attractive for global investors looking for stable and safe returns. However, the interest rate gap between the U.S. and the emerging markets is significant, and a small fed rate hike in the U.S. may not be attractive enough for the portfolio managers to completely abandon the emerging markets and move investments to the U.S.

The emerging market economies with weak macroeconomic fundamentals and with pending structural reforms are more vulnerable to a fed rate hike compared to reform-oriented economies with strong fundamental footing. On the other hand, the emerging market economies with large foreign exchange reserves, low dollar denominated debt, strong current account balances, and solid public finances are likely to manage the aftershocks of a fed rate hike more effectively.

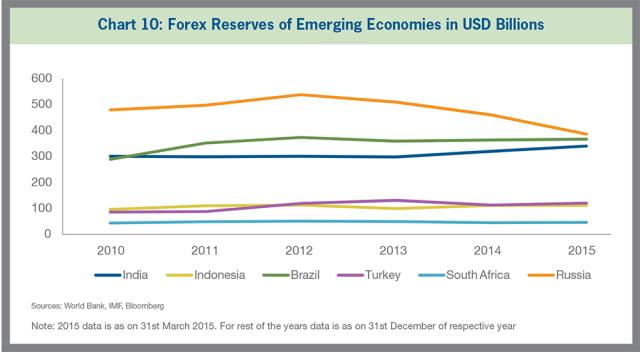

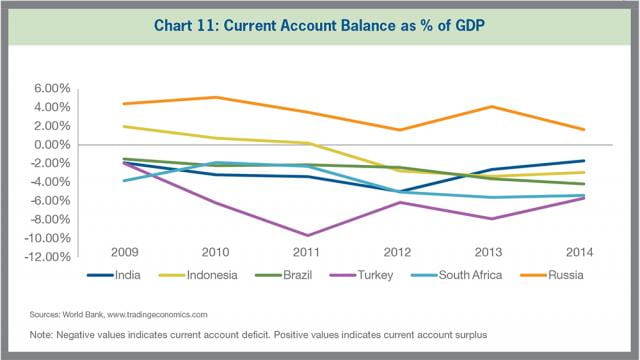

The Indian economy is in a much better state than it was two to three years ago. India has taken proactive steps compared to the other emerging market economies to control currency depreciation and to increase its foreign exchange reserves. India’s current account deficit has gradually decreased from 4.9 percent in 2012 to 1.7 percent in 2014. Its foreign exchange reserves increased from USD 298 billion as of December 31, 2013, to USD 340 billion as of March 31, 2015. Crude oil import constitutes a major component of India’s import basket; thus, softening of international crude oil prices will provide India an opportunity to further accumulate its foreign exchange reserves. India`s ratio of external debt to GDP remained steady within the range of 20 to 23 percent during the last three years. Further, the Indian equity market has been one of the better performing markets in the recent past and, even after a correction resulting from a fed rate hike, it will be able to attract fresh capital on account of strong macroeconomic fundamentals, structural reforms initiated by its new government, and its status as a bright spot in the bleak global economy. Thus the effect of an increase in the federal rate on Indian market is expected to be minor.

The Russian economy is currently in serious financial trouble. Its economy is suffering as a result of various international sanctions due to the Ukraine crisis and a sharp fall in energy prices — a major source of foreign exchange for Russia. Being a net exporter, Russia has had a positive net current account balance for the last few years but as a result of a sharp fall in energy prices, the current account balance has decreased from 5.1 percent of GDP in 2010 to 1.6 percent in 2014. Foreign exchange reserves also decreased from USD 497 billion as of December 31, 2010, to USD 386 billion as of March 31, 2015. Henceforth, Russian capital markets could see a significant capital outflow as a result of a fed rate hike.

Brazil has mixed macroeconomic fundamentals. Its foreign exchange reserves have increased from USD 289 billion as of December 31, 2010, to USD 367 billion as of March 31, 2015. Brazil’s external debt-to-GDP ratio has been in the range of 15 to 20 percent for the last few years. However, a major concern for the Brazilian economy has been its deteriorating current account balance. The current account deficit has increased from 1.5 percent of GDP in 2010 to 4.17 percent of GDP in 2014. The severity of an increase in the fed rate could be low to medium on Brazilian capital markets.

Indonesia, Turkey, and South Africa are the emerging market economies most prone to aftershocks of a hike in the fed rate. Indonesia’s current account balance has decreased from 1.9 percent of GDP in 2010 to negative 2.95 percent of GDP in 2014. During the same period, Turkey and South Africa have experienced an increase in their current account deficit from 1.95 percent and 3.84 percent, respectively, to 5.7 percent and 5.4 percent, respectively. During the last six years, foreign exchange reserves for Indonesia and South Africa remained fairly stable. Turkey has seen a gradual increase in its foreign exchange reserves from USD 86 billion as of December 31, 2010, to USD 121 billion as of March 31, 2015. The external debt as a percent of Gross National Income (“GNI”) for Indonesia has been steady at around 30 percent for the last few years, while external debt as a percent of GNI for Turkey and South Africa has increased from 41.3 percent and 29.9 percent, respectively, in 2010 to 47.9 percent and 40.7 percent, respectively, in 2013. Considering their weak macroeconomic fundamentals, Indonesia, Turkey, and South Africa are more likely to be impacted by a fed rate hike.

A fed rate hike is a long-term positive event for the global economy. Although it may create significant volatility in the emerging market economies in the short-term, the risk of a major financial crisis is limited as most of the emerging markets are much more fundamentally sound today than they were a few years ago. The emerging markets with weak macroeconomic fundamentals like Indonesia, South Africa, and Turkey may experience severe instability and capital outflow in the short-term, whereas China and India (with strong macroeconomic fundamentals) may not experience significant aftershocks.