Italiano

Italiano

Industrial services showed extremely favorable signs of growth in first quarter of 2018, signaling that the economy is following suit. Three-year revenue compound annual growth rates for our environmental, equipment rental, and facilities segments each turned positive since the fourth quarter of 2017, and last-12-month revenue is up across all industrial services segments during this same period. According to Bloomberg, U.S. service industries expanded in February near the fastest pace in at least a decade. This momentum is a result of consolidation and realized synergies, coupled with positive macro trends across key sectors such as manufacturing and construction which have resulted in organic growth. Trading multiples have remained relatively flat with a slight decrease from peak levels in the fourth quarter of 2017, primarily due to improving earnings, which should potentially drive interest from private equity buyers.

Key Takeaways

- Continued strong overall industrial services M&A activity

- Revenue growth across all segments

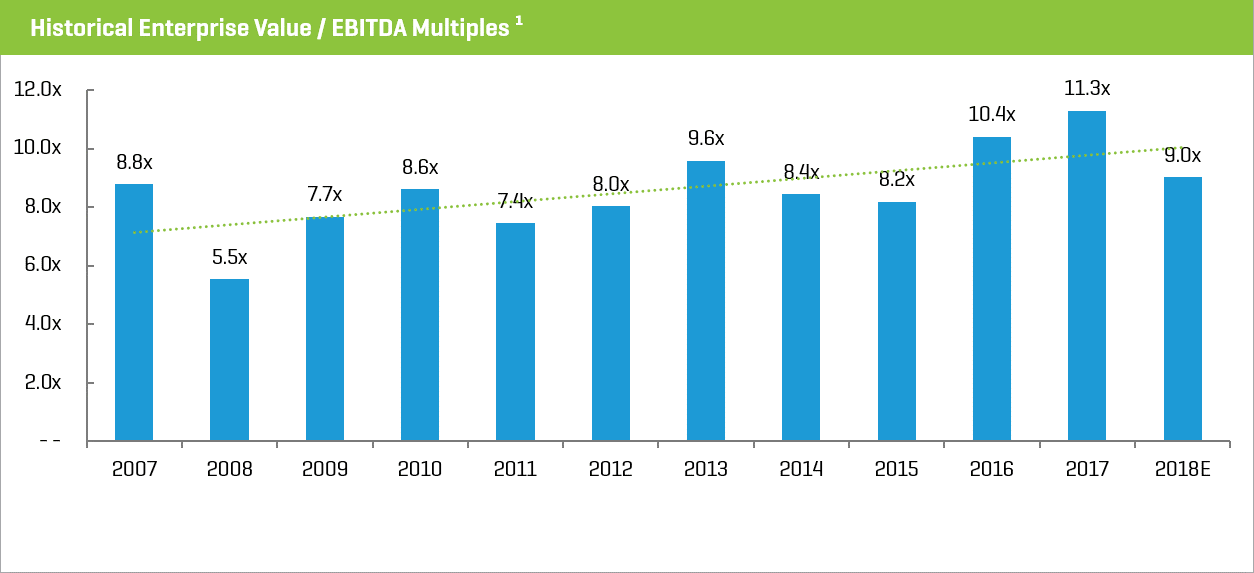

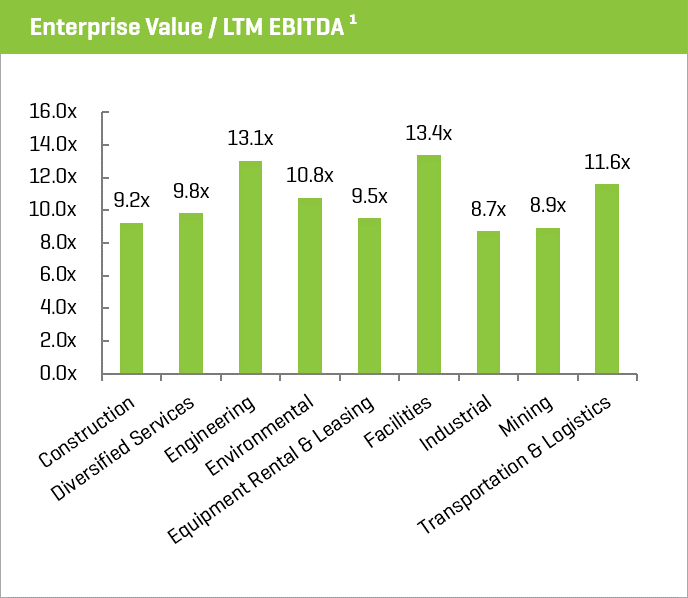

- Valuation multiples remaining near all-time highs

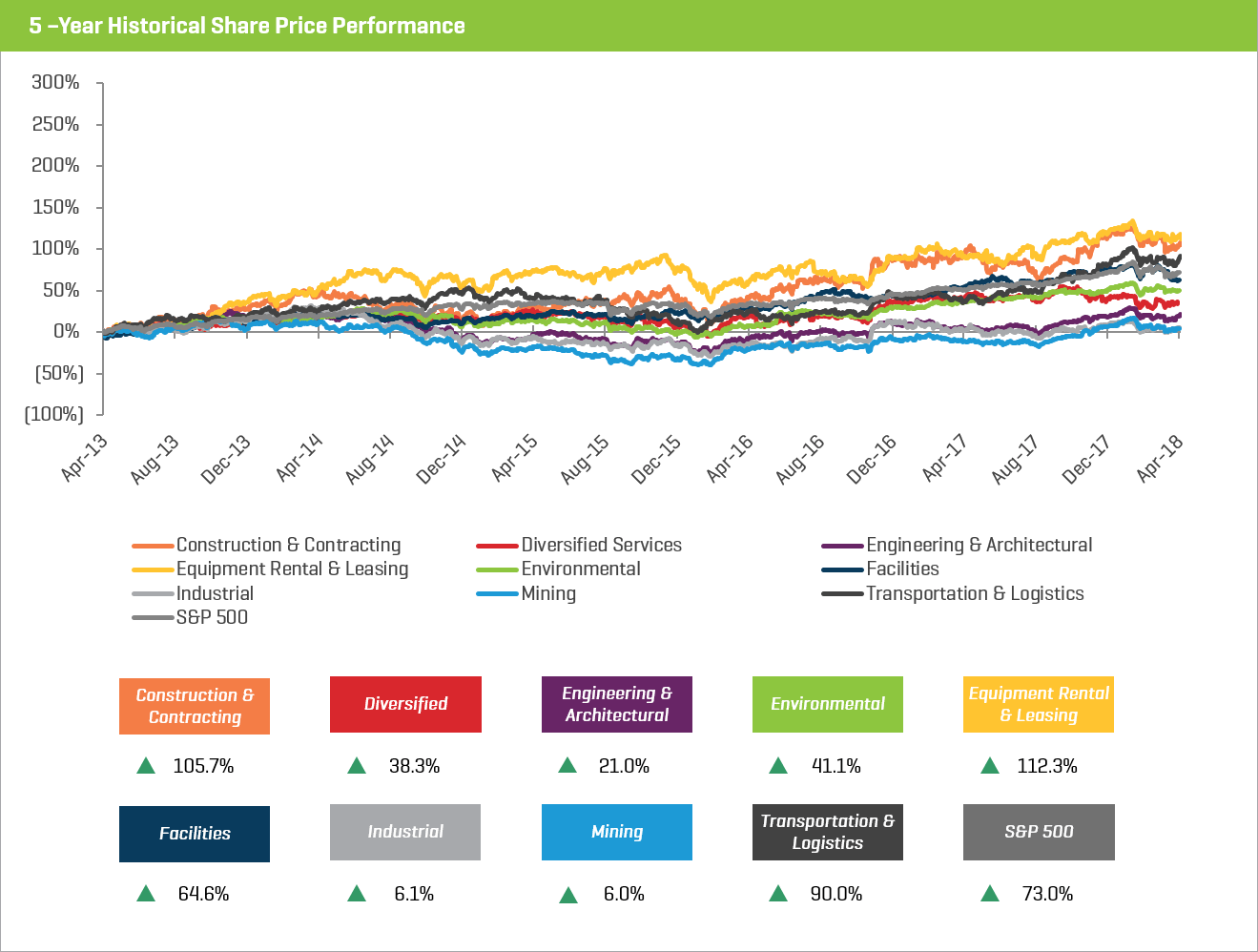

- Public equity performance remains positive

- Cross-border M&A activity surged

- Continued low cost of capital and high capital availability

- Key macroeconomic indicators seeing coordinated strength

Industry Statistics

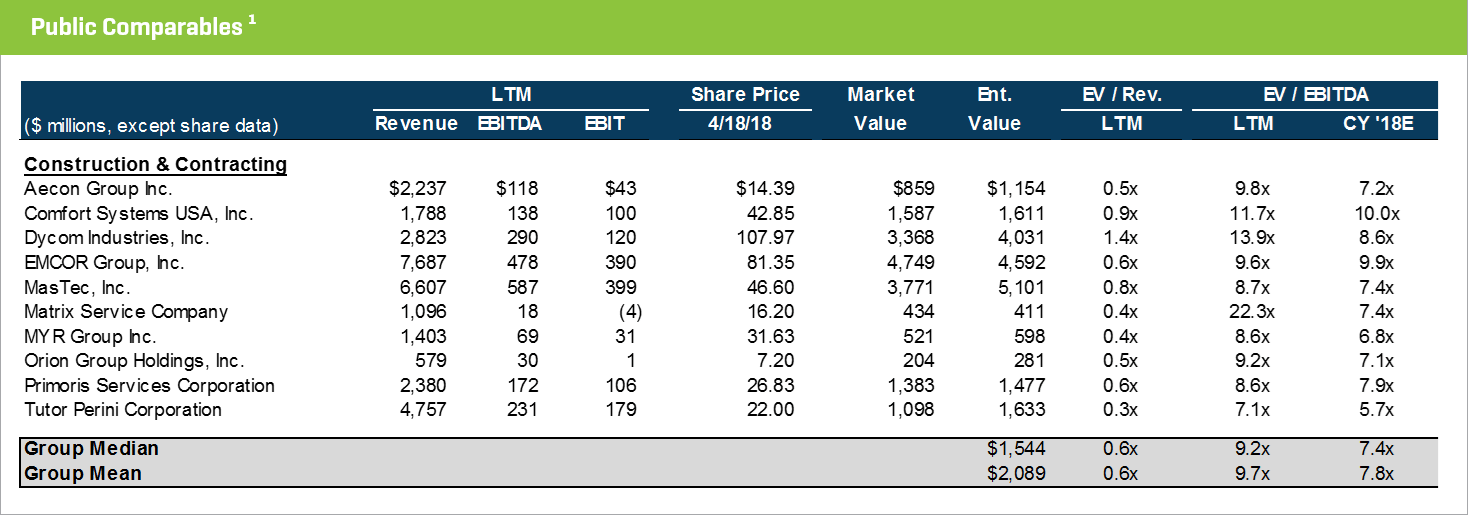

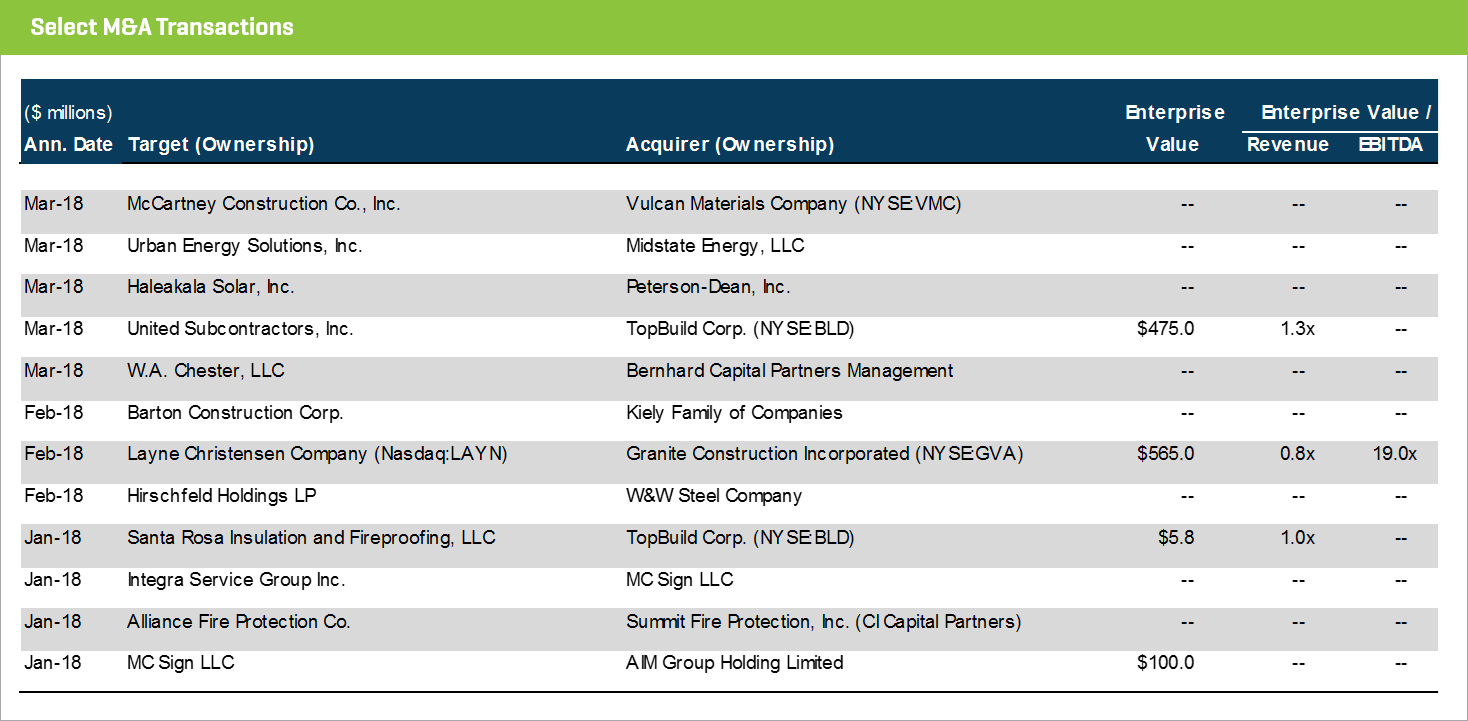

Construction & Contracting Services

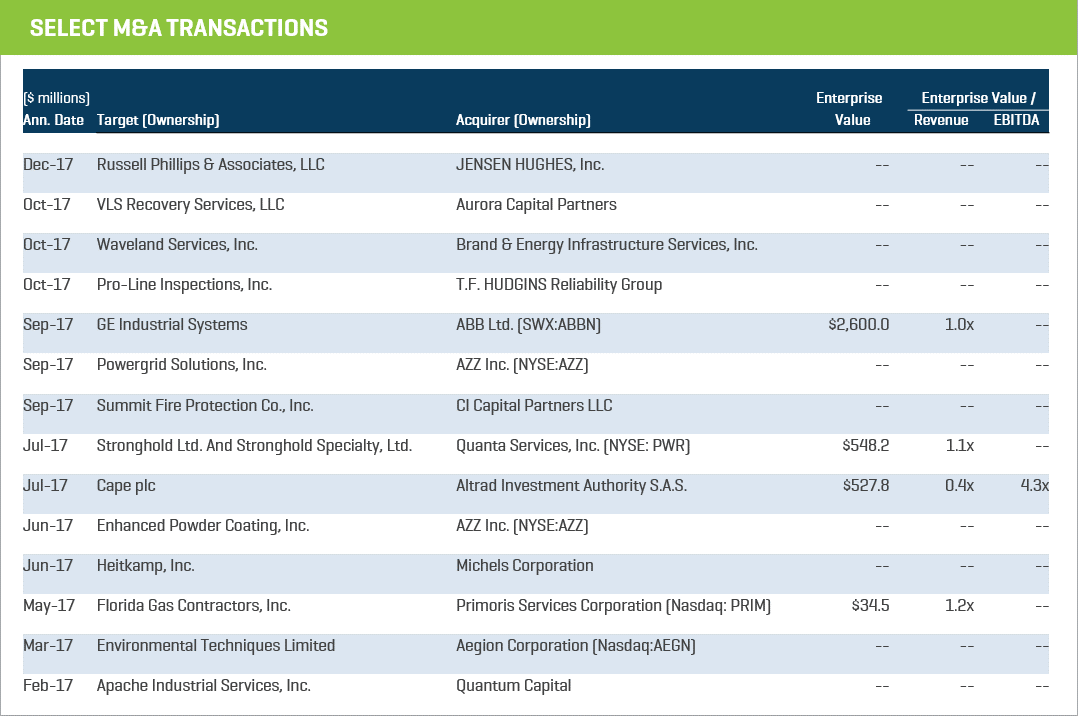

The construction segment saw a handful of strategic transactions poised towards expanding geographical reach and creating additional growth platforms. Notable transactions include:

- Granite Construction Inc. (NYSE:GVA) announced acquisition of U.S.-based Layne Christensen Company (Nasdaq:LAYN), in a stock-for-stock transaction valued at $565 million, representing a 33% premium and a forward multiple of 8.2x 2018 expected EBITDA

- TopBuild Corp. (NYSE:BLD) announced acquisition of U.S.-based United Subcontractors, Inc., in an all-cash transaction valued at $475 million, as well as TopBuild’s acquisition of Santa Rosa Insulation and Fireproofing LLC

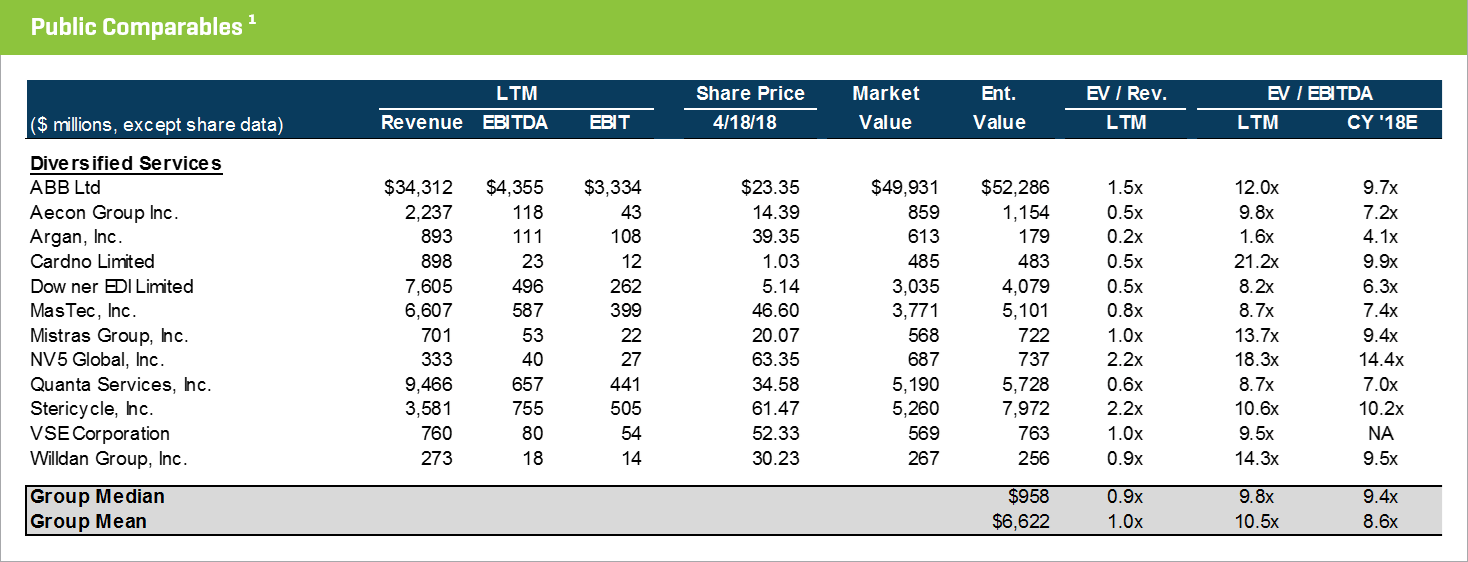

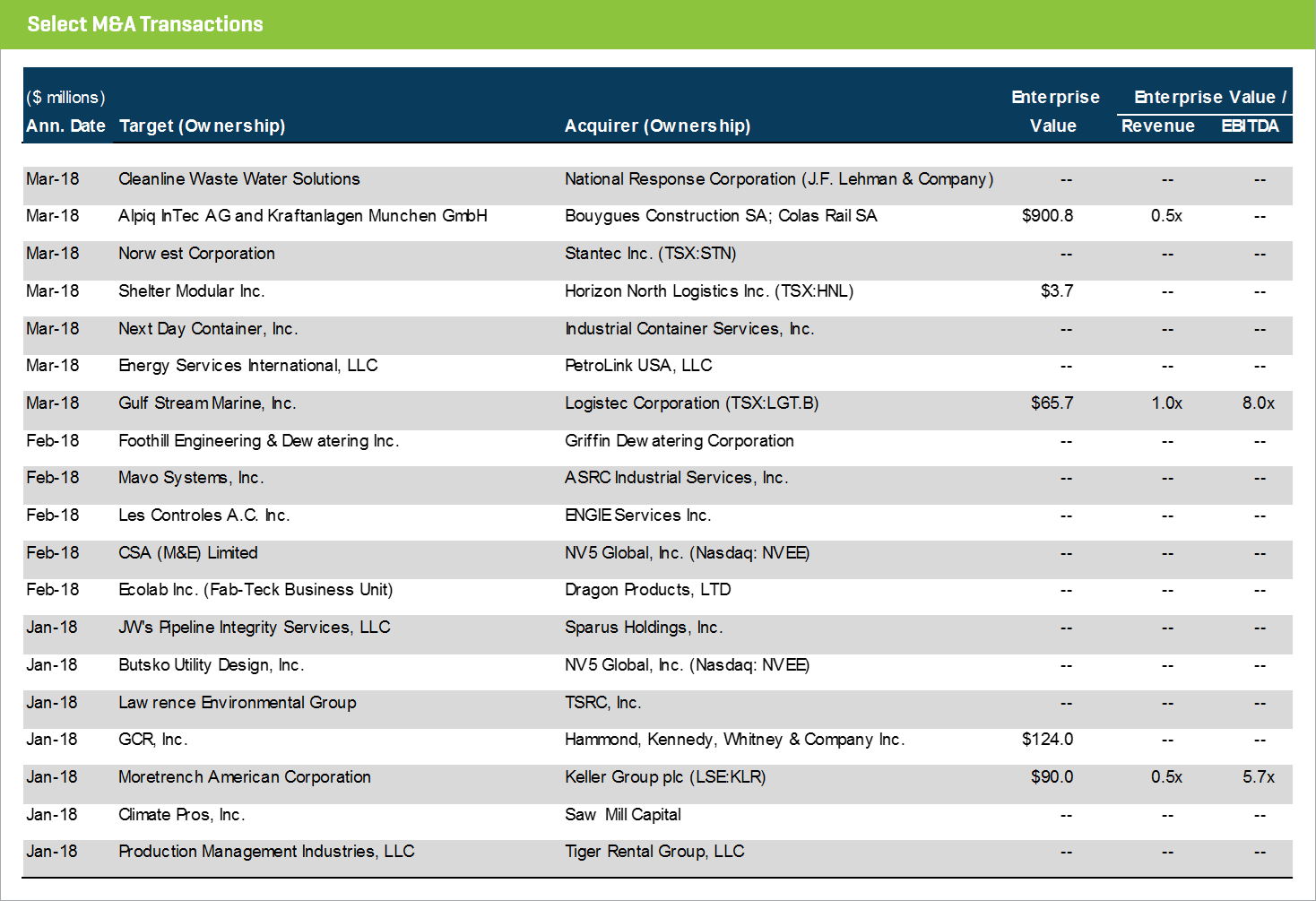

Diversified Services

Diversified services transactions were fueled by both cross-border and private equity interest, as both types of buyers look to diversify capabilities and portfolios. Notable transactions include:

- Logistec Corporation’s (TSX:LGT.B) acquisition of U.S.-based Gulf Stream Marine, Inc., which establishes a stronghold in the U.S. Gulf and drastically expands Logistec’s network of terminals in the USA

- NV5 Global, Inc’s (Nasdaq:NVEE) acquisitions of Hong Kong-based CSA (M&E) Limited and U.S.-based Butsko Utility Design, Inc., which marks NV5’s eighth and ninth acquisition in the last year

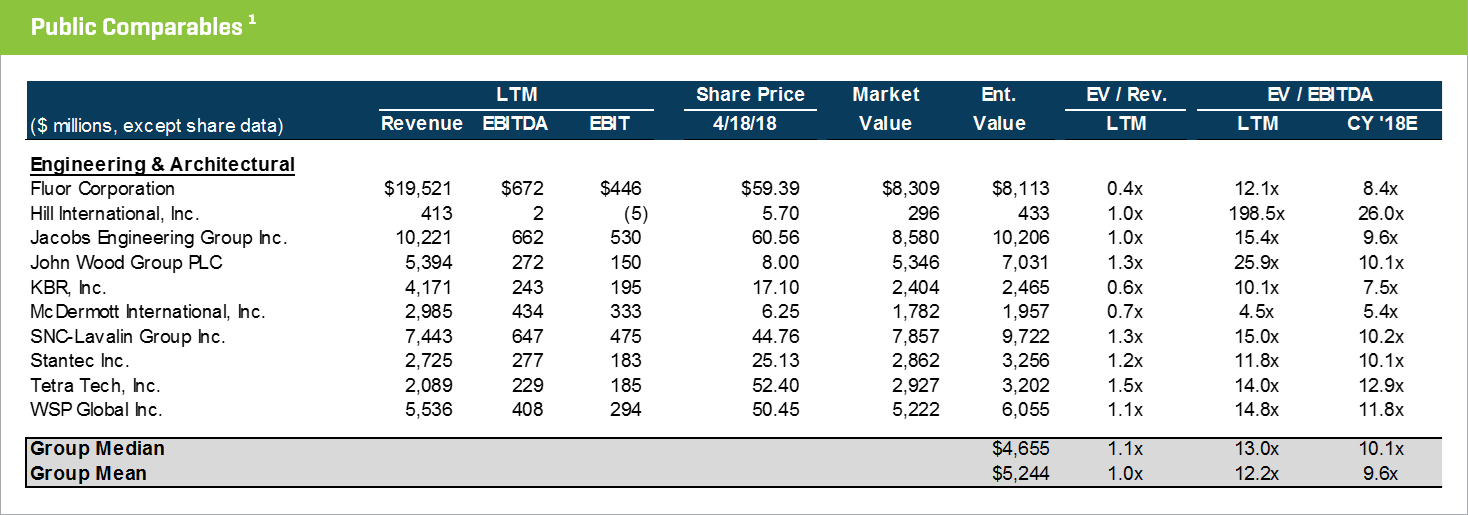

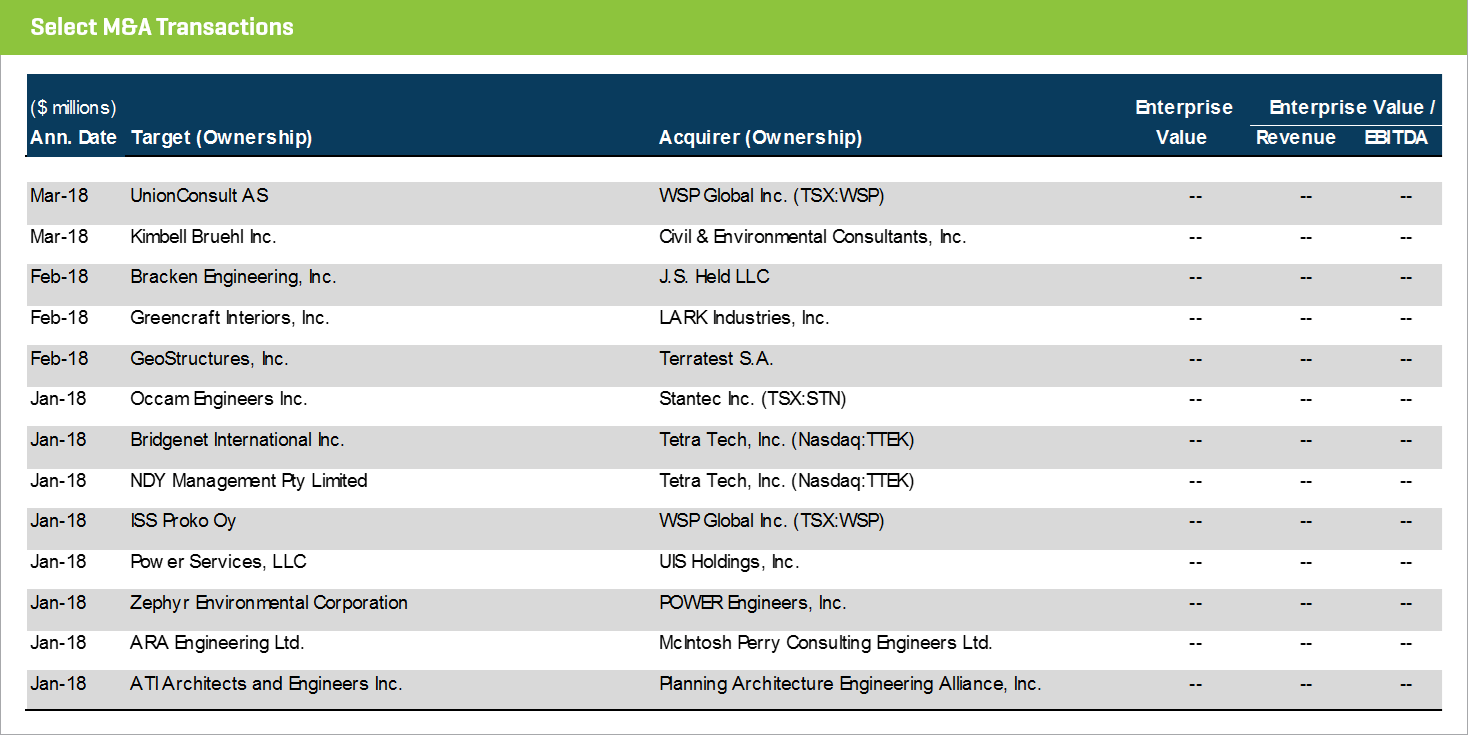

Engineering & Architectural Services

Industrial conglomerates such as WSP Global, Tetra Tech, and Stantec dominated M&A activity within engineering & architectural services throughout the first quarter of 2018. Notable transactions include:

- Stantec Inc’s (TSX:STN) announced acquisition of U.S.-based Occam Engineers Inc., which will strengthen Stantec’s water, transportation, and public works service capabilities in the Southwestern United States

- Tetra Tech, Inc’s (Nasdaq:TTEK) acquisition of U.S.-based Bridgenet International Inc. and announced acquisition of Australia-based NDY Management Pty Ltd, which expands Tetra Tech’s aviation technology solutions in the U.S. and expands reach throughout Australia and the Asia-Pacific region

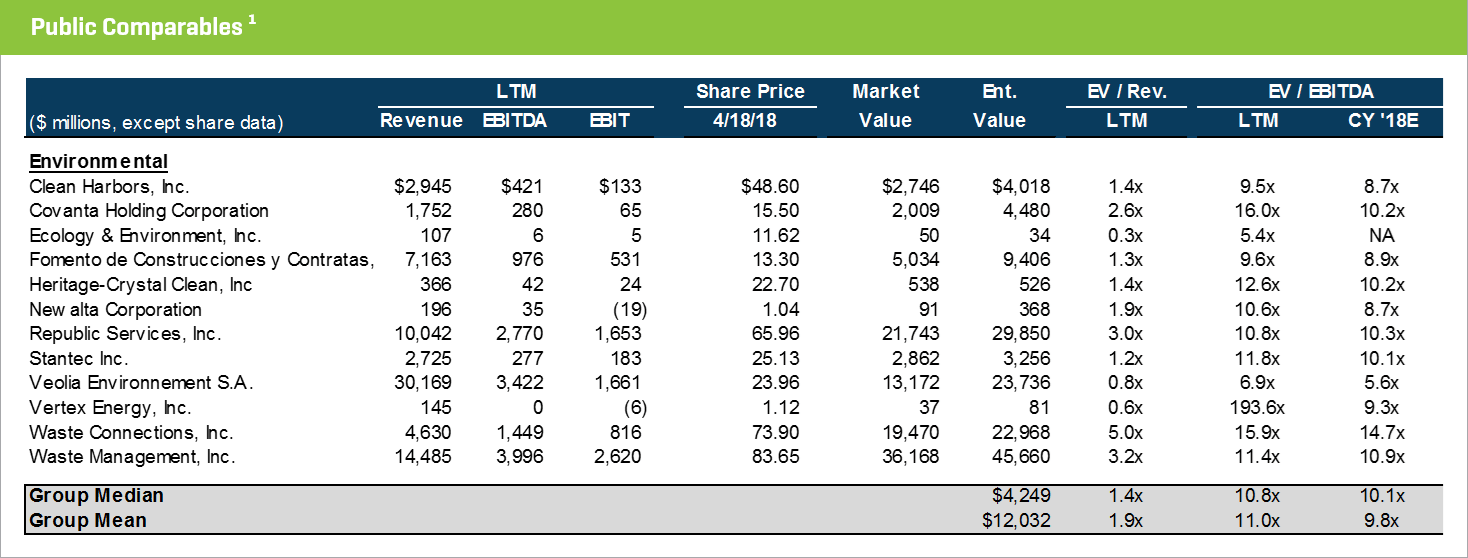

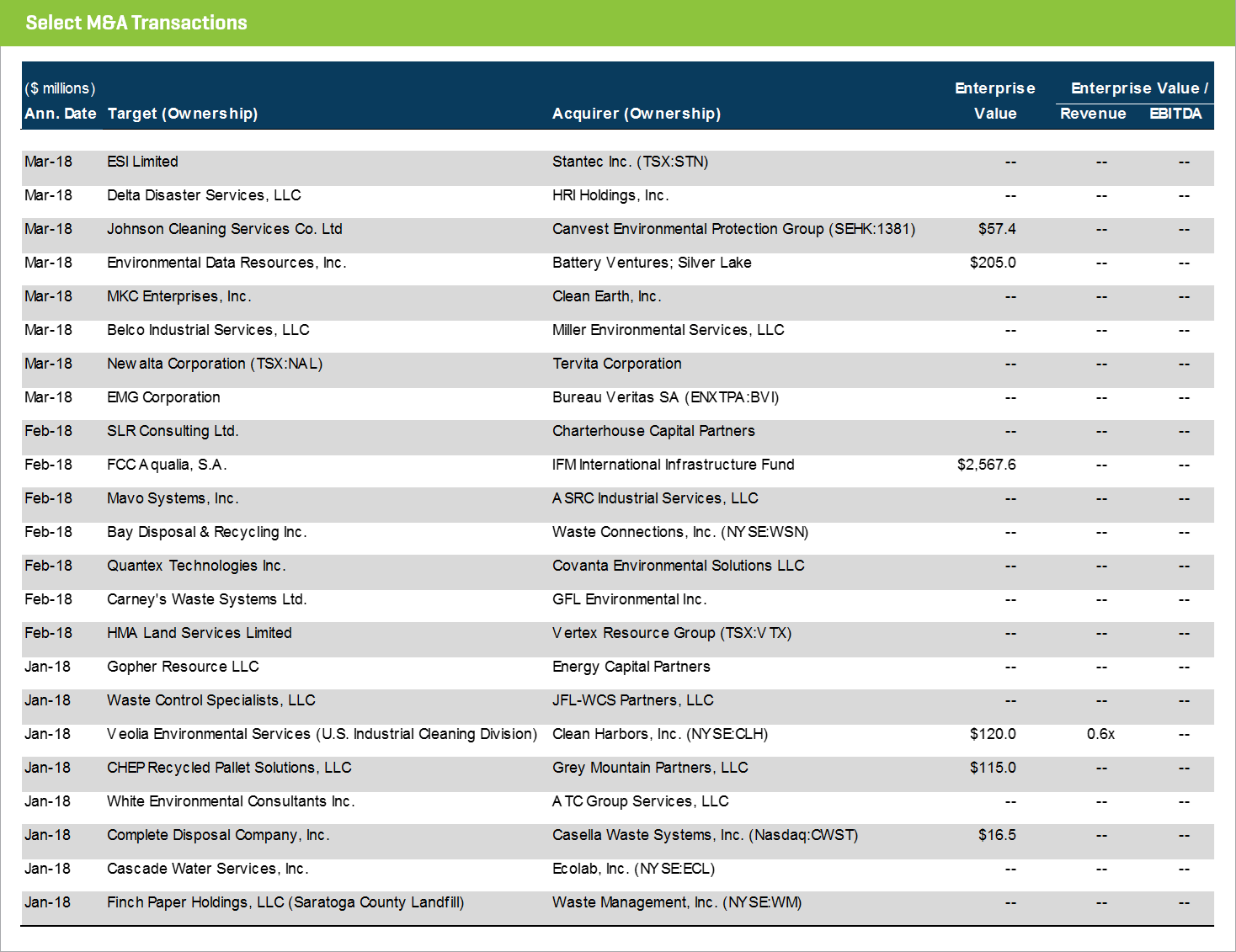

Environmental Services

The environmental services segment continues to blossom and has resulted in robust M&A activity from both strategic buyers and private equity. Notable transactions include:

- Clean Harbors Inc. (NYSE:CLH) acquired the U.S. Industrial Cleaning Services Division from France-based Veolia Environnement S.A. (ENXTPA:VIE), in an all-cash transaction valued at $120 million. Clean Harbor expects the division to generate EBITDA of $15 million-$20 million, giving the transaction a forward looking EBITDA multiple of 6x-8x

- Waste Connections, Inc. (NYSE:WCN) acquired U.S.-based Bay Disposal & Recycling Inc., which includes four collection operations, five recycling facilities, one transfer station, a C&D landfill, and approximately $70 million in annualized revenue

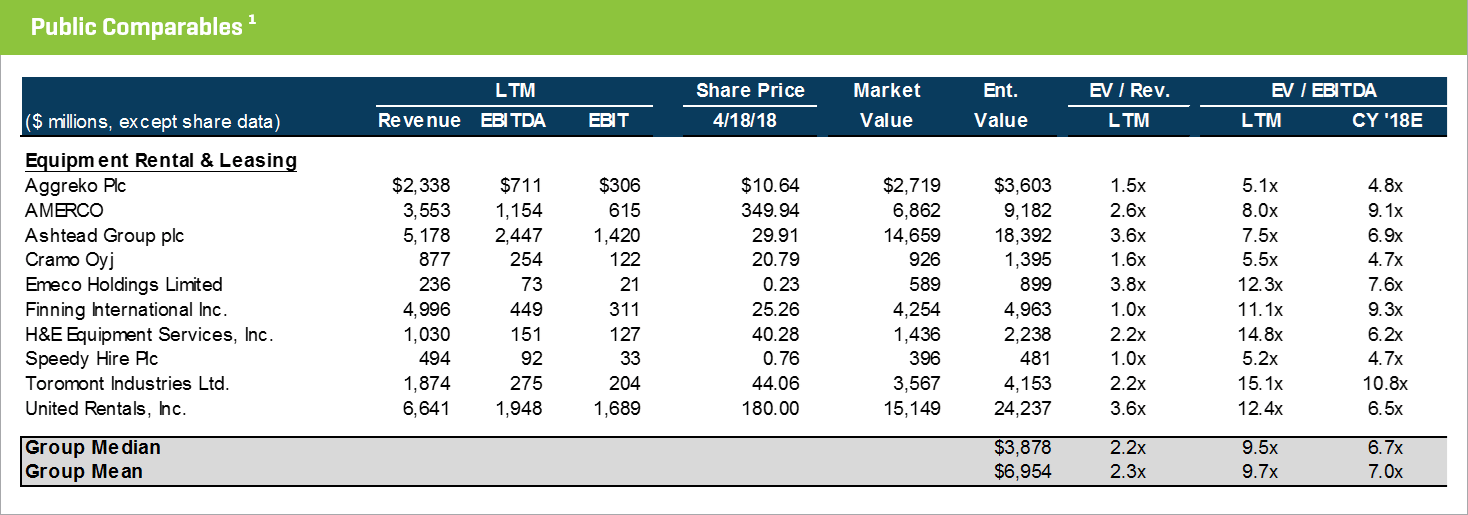

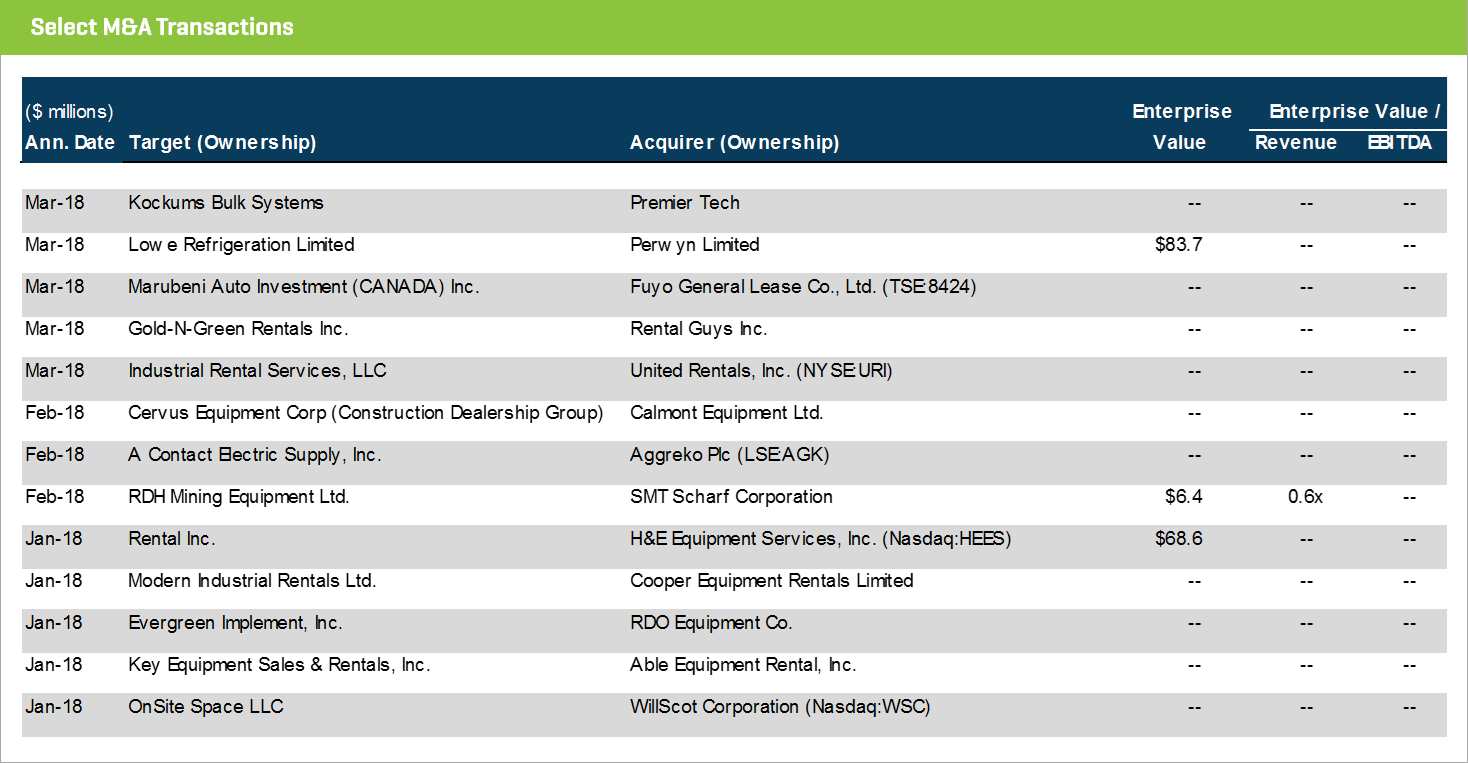

Equipment Rental & Leasing

The equipment rental and leasing segment saw a handful of strategic transactions that are meant to increase market share and position, and ensure competitiveness. Notable transactions include:

- H&E Equipment Services, Inc. (Nasdaq:HEES) acquired U.S.-based Rental Inc. for approximately $69 million, which includes five branches located throughout Alabama and Florida, and a rental fleet size of approximately $36 million

- United Rentals, Inc. (NYSE:URI) acquired the assets of U.S.-based Industrial Rental Services, LLC, which reinforces United’s commitment to the growing demand of industrial safety and expands the company’s tool solutions specialty rental fleet with products such as isolation blinds and communication systems

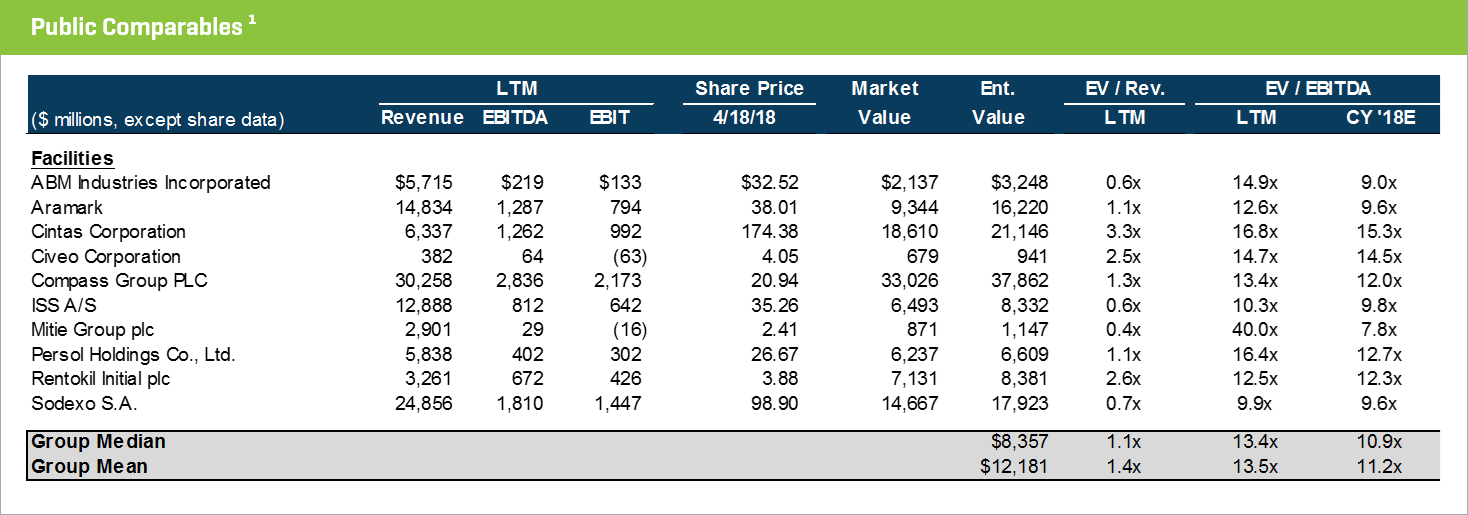

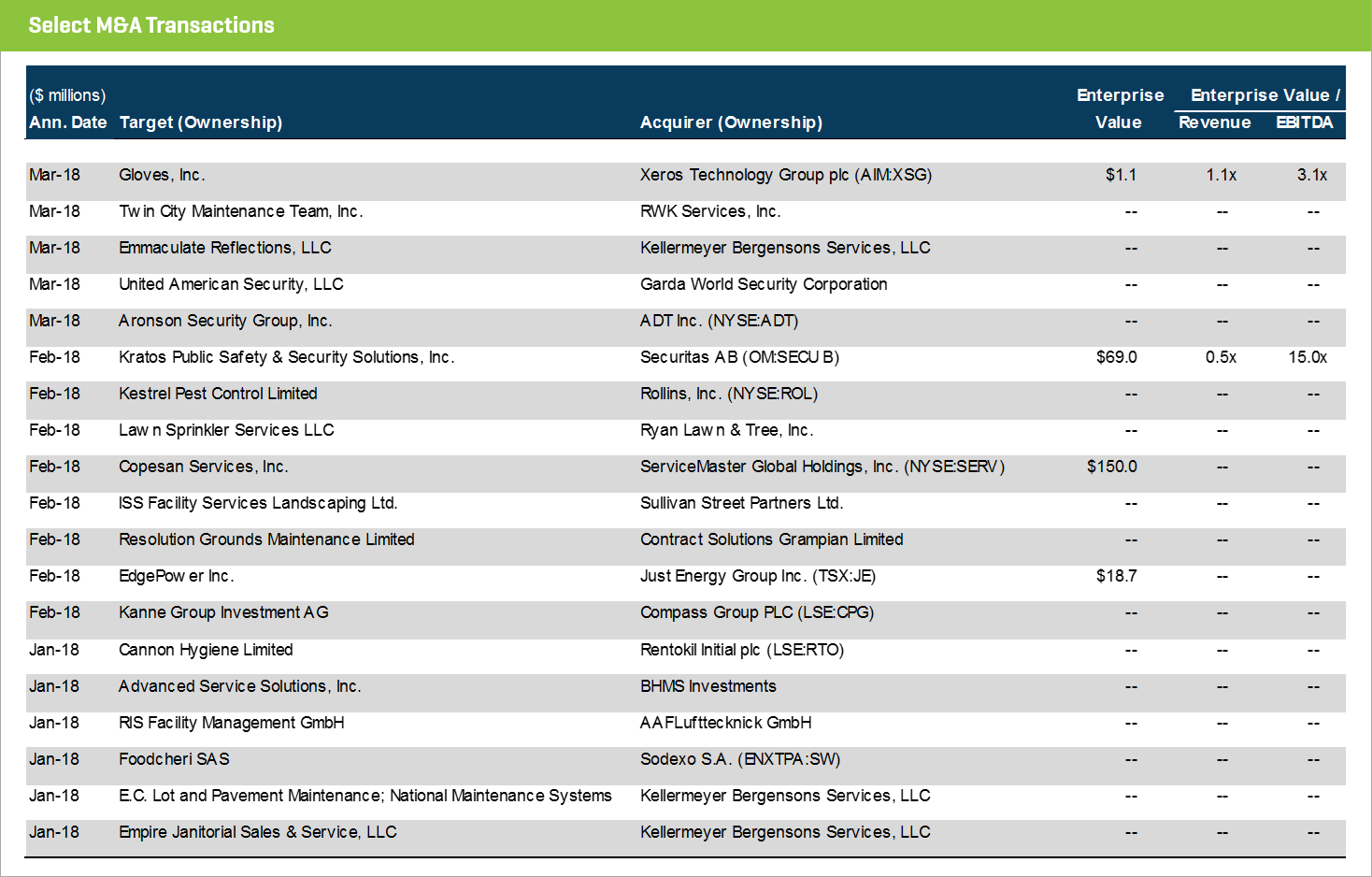

Facilities Services

The facilities services segment continues to leverage M&A as a primary growth tactic despite having the highest trading multiples out of all nine groups. However, these are justified in part, due to significant cost synergies anticipated to be realized post transaction by acquirers. Notable transactions include:

- Sullivan Street Partners announced that it will acquire UK-based ISS Facility Services Landscaping Ltd. from ISS A/S, and will trade under the name Tivoli Group Limited. It is anticipated that this transaction will result in the transfer of around 1,100 operational staff and support functions to Sullivan Street Partners

- Kellermeyer Bergensons Services, which is owned by GI Partners, announced and completed three U.S. based acquisitions since January. These include Empire Janitorial Sales & Service, East Coast Lot and Pavement Maintenance, and Emmaculate Reflections, LLC

Industrial Services

Industrial services M&A activity continues to be driven by large conglomerates and private equity interest. Strategic buyer activity was motivated by anticipated long-term benefits for both the target and the acquirer, due to complementary product mix and integration. Notable transactions include:

- Primoris Services Corporation (Nasdaq:PRIM) announced the acquisition of U.S.-based Willbros Group, Inc. (OTCPK:WGRP) and will pay $0.60 per share for all of the outstanding common stock, plus provide up to $20 million in bridge financing, which values the transaction at approximately $140 million

- Brookfield Business Partners L.P. (TSX:BBU.UN) announced the acquisition of U.S.-based Westinghouse Electric Company, a bankrupt nuclear services company owned by Toshiba Corp, for $4.6 billion. Brookfield plans to use $1 billion of equity and $3 billion of long-term debt to finance the transaction

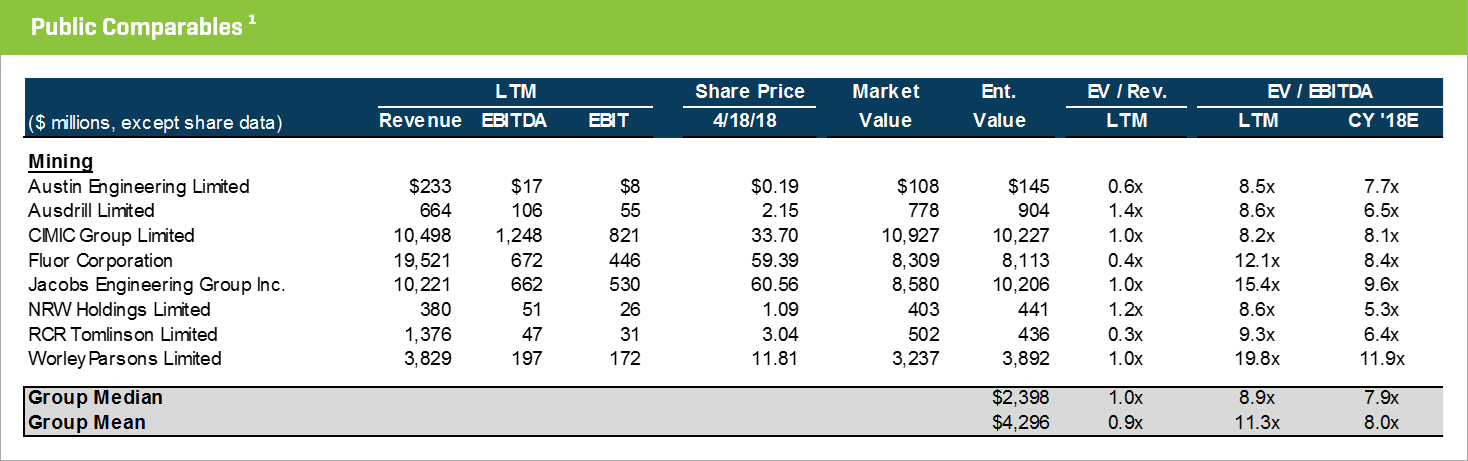

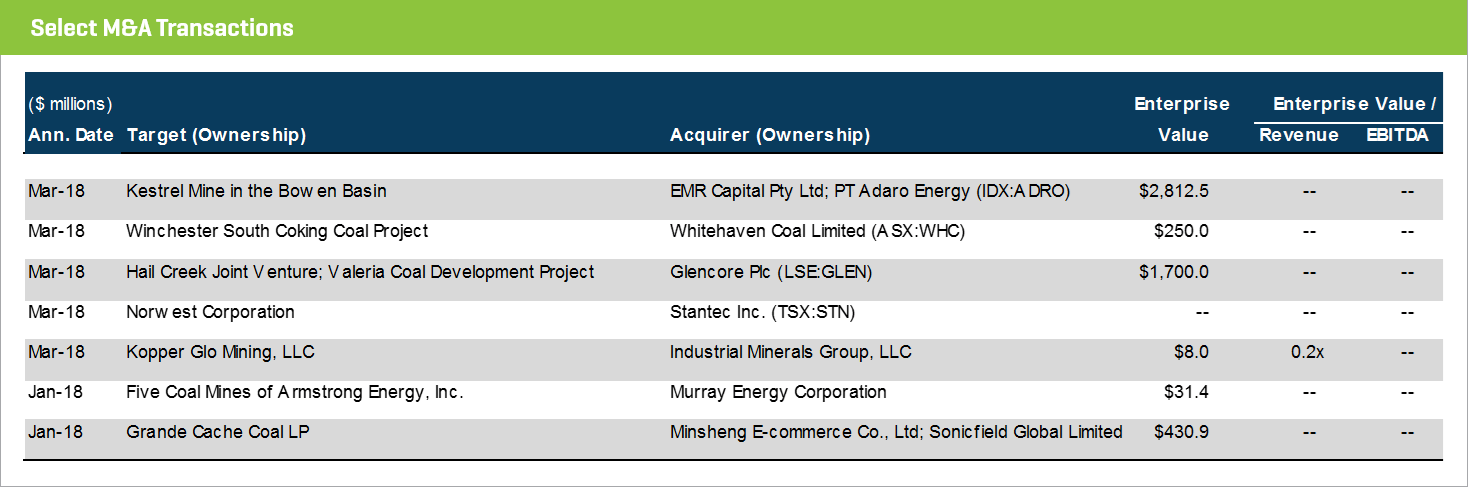

Mining Services

The mining services industry is beginning to see positive momentum after a handful of challenging years. Stout’s mining services segment has seen an average increase in LTM revenue between December 2017 and April 2018 of 15.5%, a 1.1% increase in average EBITDA margin, and a reduction in the average EV/EBITDA multiple from 11.7x to 8.9x. These favorable dynamics are beginning to drive additional M&A activity. Notable transactions include:

- Stantec Inc. (TSX:STN) announced the acquisition of Canadian-based Norwest Corporation, which will strengthen Stantec’s mining capabilities in Canada and across the 4 locations Norwest operates throughout the U.S.

- Glencore Plc (LSE:GLEN) announced the acquisition of Australia-based Hail Creek Joint Venture and Valeria Coal Development project for $1.7 billion. Hail creek is said to have JORC resources of 794 million tons with proven and probable reserves if 142 million tons

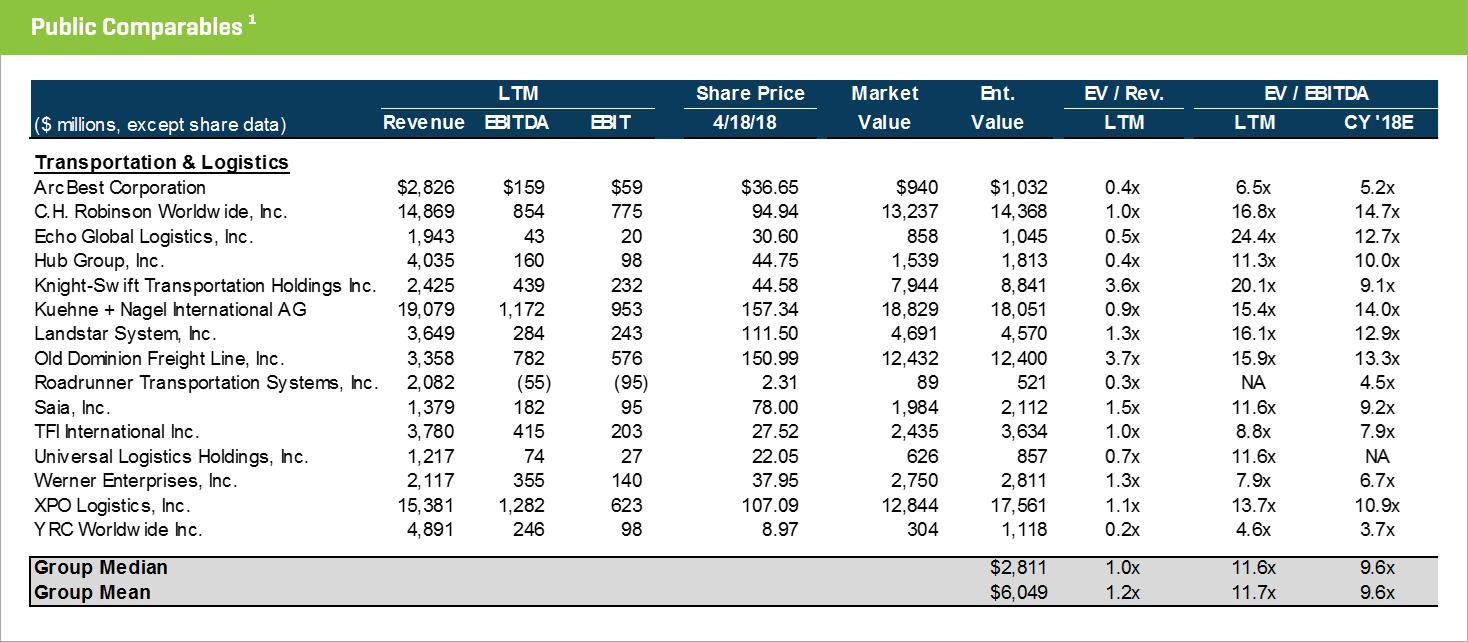

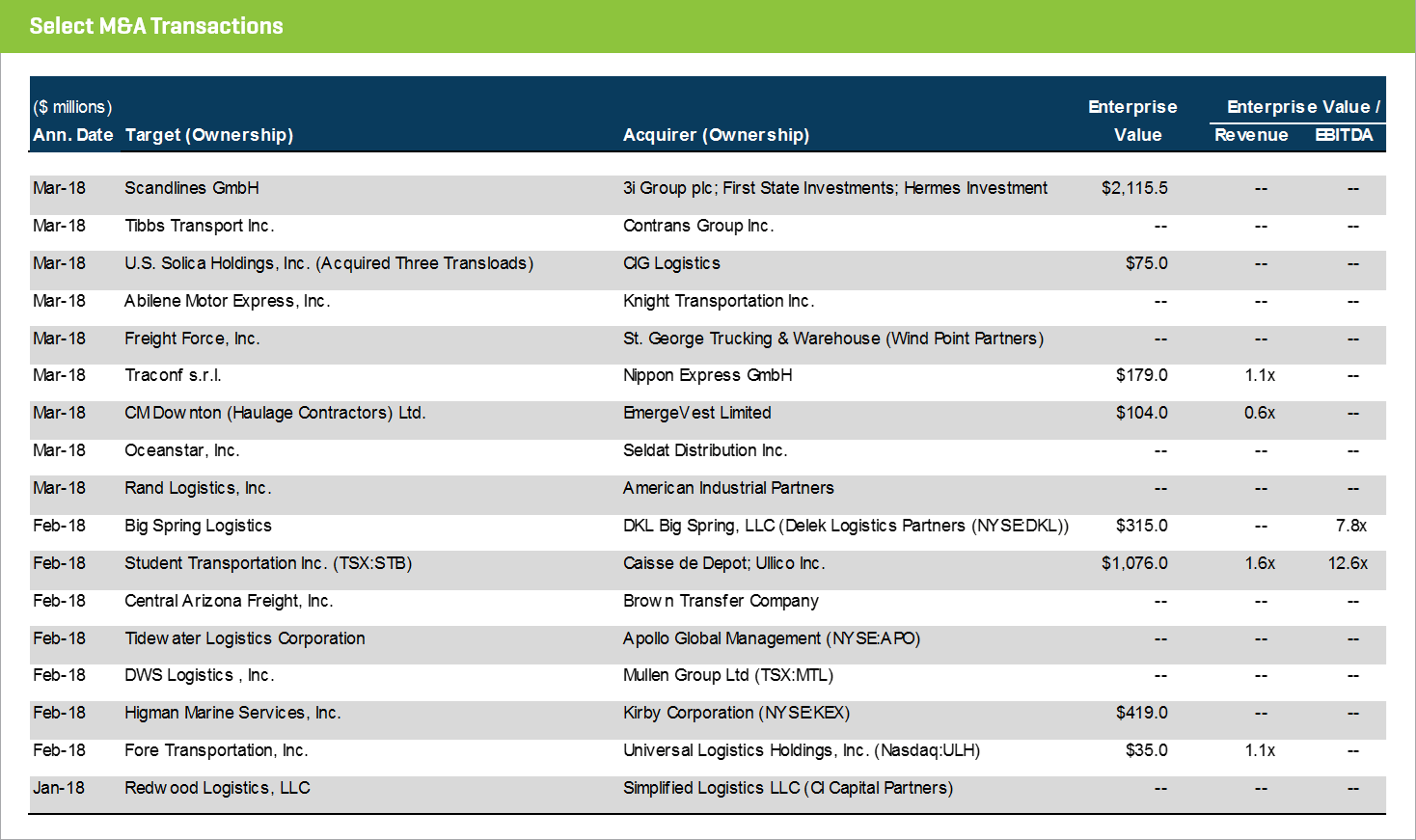

Transportation & Logistics

Transportation and logistics M&A activity continues to uptick as the industry evolves and consolidation becomes more favorable. Notable transactions include:

- Caisse de Depot and ULLICO Inc. announced the acquisition of Canadian-based Student Transportation Inc. (TSX:STB) for approximately $1.1 billion, representing a 27% premium to the 20-day volume weighted average stock price

- Knight-Swift Transportation Holdings Inc. (NYSE:KNX) acquired U.S.-based Abilene Motor Express, Inc. which represents Knight-Swift’s first sizeable acquisition since the two merged last year. Abilene is estimated to generate approximately $100 million in annual revenue

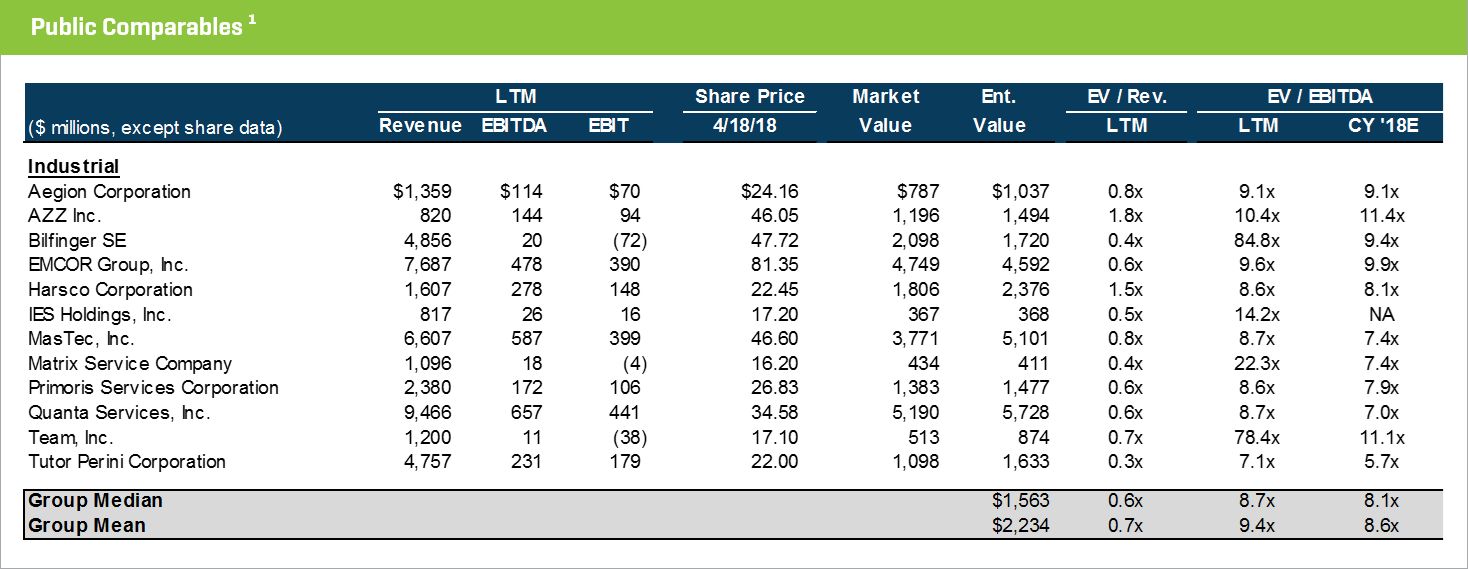

- Multiples above 20x are excluded from the mean/median calculation