Italiano

Italiano

An abundance of available capital is sustaining peak levels of merger and acquisition (M&A) activity across numerous industry sectors and companies of all sizes. Investor interest is coming from more directions than ever before – from industry, strategic buyers, private equity, family offices, and even wealthy individuals. A classic scenario of demand outstripping supply is causing buyer lists to expand, competition to remain stiff, and sellers to be extremely prudent in selecting the ideal winning bidder.

Once that winning bidder is selected, what transpires next is the inevitable yet vital due diligence phase of an M&A transaction. A productive and collaborative due diligence process is critical to achieving a successful outcome of a transaction. However, due to a large number of factors, it also has the potential to vary greatly from one transaction to the next and be rife with hurdles and pitfalls if not anticipated and managed correctly from start to finish.

As financial advisors to buyers and sellers, we have sat on both sides of the table and experienced a vast number of due diligence scenarios – some with very positive outcomes and others much less so. What we have learned over the years is that there are approaches you can take to help ensure a smooth process. We examine some practical insights and real-world experiences to better inform buyers, sellers, and their respective advisors as they anticipate and navigate the due diligence process.

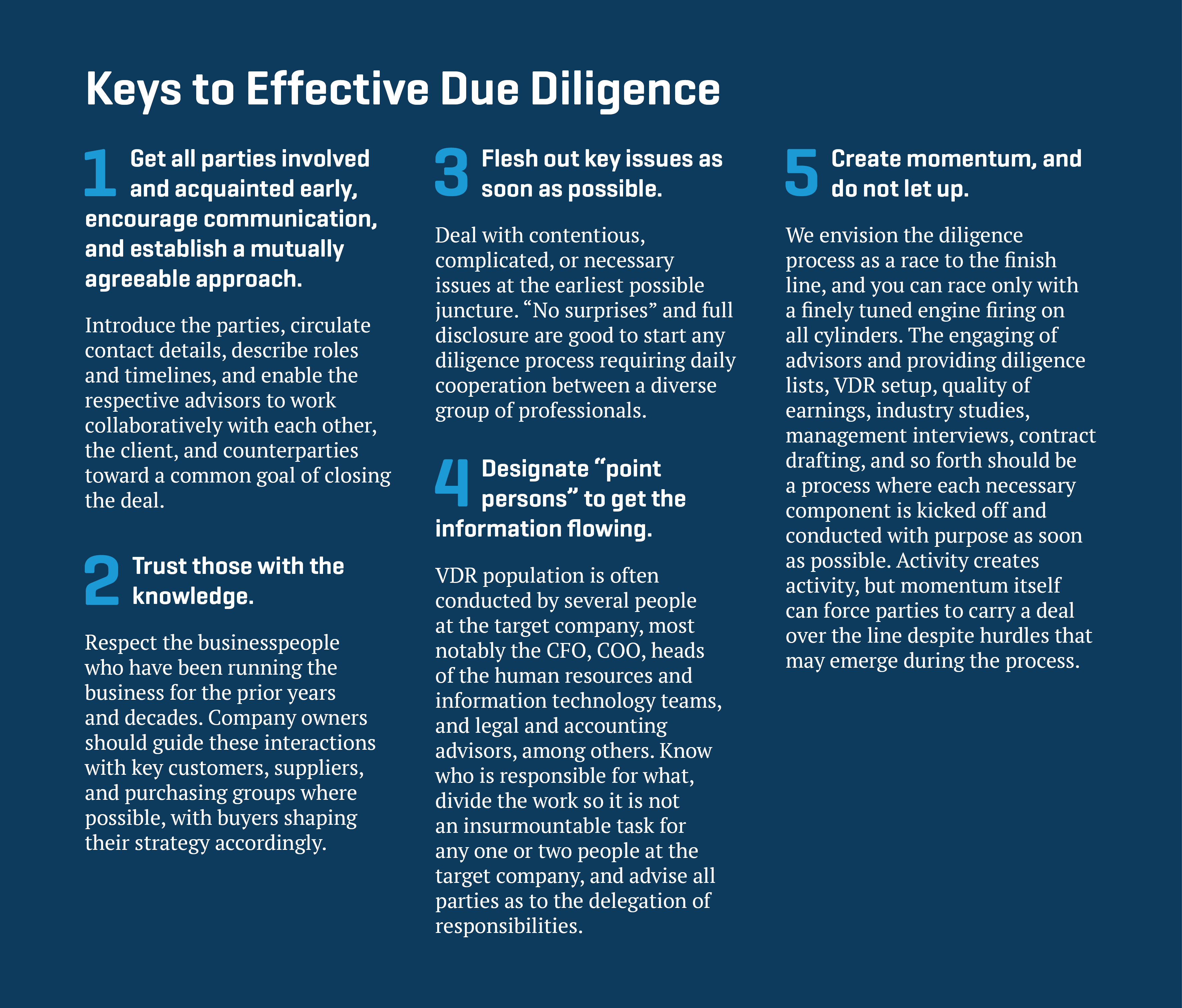

Meet the Entire Diligence Team – Early and Often

Insight

Identify which key stakeholders will be involved and representing each side in the due diligence process as early as possible. Meet each other, then begin establishing mutual expectations for approach, level of detail required, and anticipated timeline.

It is common that representatives of the buyer, such as the investors themselves, the investors’ attorneys, accountants, compliance officers, professional consultants, and other specialized service providers (depending on the industry), will all participate in due diligence in some fashion. Representatives of the seller are typically the CEO, CFO, COO, and the most senior members of their support staff, along with the investment banker, the sellers’ attorney, and an accounting firm. The number of participants can escalate quickly. Establishing clear expectations and lines of communication at the very beginning will go a long way toward maintaining an efficient pace, acknowledging outlying circumstances, and holding all parties accountable to the process.

Real-world scenario

A U.S.-based company with a significant presence in Japan had entered into a letter of intent (LOI) to be acquired by a large multinational organization headquartered in Japan. The two parties had established exceptional goodwill after months of solid work by the respective deal teams. The stage was set for what should have been a rapid and successful due diligence phase and closing, followed by immediate recognition of synergies and expanded business opportunities for the combined entity.

However, it was not until weeks after the commencement of financial and legal diligence that the buyer's compliance team – a new set of people with narrowly defined tasks initiated several weeks after diligence had begun – was finally introduced to the deal. Immediately, the nature of communication changed, and transaction momentum was halted.

The introduction of a new, unexpected set of diligence resources at this juncture raised alarm in the seller. The compliance team became the driving force, and the commercial reasons for doing the deal took a back seat, along with the original deal team. Lack of communication raised further alarm. The deal slowed, a new set of "issues" arose that were not central to the seller, and the buyer pulled back. Goodwill evaporated, and ultimately the deal failed.

An introduction to the whole diligence team on day one, combined with earlier identification of the buyer’s internal issues, would have enabled the seller to better anticipate and accommodate the buyer’s additional diligence requests and extended timeline. This would allow the buyer to take the time needed to conduct the research required to clear internal hurdles, satisfy key stakeholders, and complete the transaction.

Trust Those With Firsthand Knowledge

Insight

When it comes to dealing with key suppliers, customers, industry collectives/bodies, or purchasing groups, an honest business owner knows best. The business owner who is closest to these relationships should be respected for his or her knowledge and empowered to guide these interactions where possible. The buyer’s team can then shape their strategy accordingly.

Prospective buyers need to gain a thorough understanding of customer and supplier concentration, along with the strength and viability of those relationships. And it is not uncommon as part of the due diligence process that a buyer will seek validation. Arguably, this is a condition that should and will be met. However, the omission of key personnel from the process can jeopardize the deal.

Real-world scenario

A one-sided franchise agreement (weighted toward the large global supply partner of the seller) needed to be either assumed and renegotiated at a future date, or renegotiated during due diligence to make it palatable to a private equity buyer. Heading into the LOI signing and due diligence period, advice from the seller, the seller’s banker, and the global supply partner was that this agreement could be assumed and subsequently modified to achieve consensus on the majority of items in question after the transaction was complete.

The buyer opted to renegotiate during the due diligence phase, and detailed discussions held in good faith with all parties and identifying the key gating items had the transaction on track toward agreement. However, a critical issue was becoming visible. The buyer’s side stalled in engaging a financial due diligence advisor concurrently, and they had conducted only basic financial due diligence while trying to first negotiate the franchise supplier agreement to conclusion. While attorneys were getting stuck on certain franchise agreement sections, there was no other engine or momentum factor driving the diligence forward. All other processes had been put on hold. As the franchise agreement stalled in the hands of the attorneys, exclusivity lapsed, goodwill evaporated, and the transaction splintered.

Keep Information Flowing at a Rapid Pace

Insight

One of the most frustrating reasons for lack of or loss of momentum is that information simply doesn’t flow fast enough between buyer and seller. A buyer or seller may have his or her finger on the engagement trigger as far as advisors are concerned, but if the other party is not providing relevant information in a timely manner, an engagement could be deemed a waste of time and money.

Although a transaction can take several months to complete, it is critical that both parties demonstrate a continual sense of urgency in communications and in producing the due diligence information and responses required to sustain forward progress toward closing.

Real-world scenario

A negotiated proprietary deal between an entrepreneur-owned company and an industry-leading private equity firm saw a mutually satisfactory LOI signed within about 40 days of the initial meeting between the parties. True to form, the buyer immediately engaged a world-class financial diligence firm, the investment banker, and kicked off financial, legal, human resources, insurance, and risk diligence within days of signing the LOI, with the investment banker coordinating communications between the involved parties. Matching the buyer “punch for punch,” the seller’s top three managers were engaged to immediately attack the diligence lists, rapidly provide virtual data room (VDR) uploads, and provide access to the first- and second-tier management teams and to outside accountants.

Momentum was attained and held at a blistering pace, and the respective teams pushed each other through a multi-month process. Both teams fully understood the need for speed and the probability that it would increase the chances of a successful outcome for both sides.

Stay Informed

While there are myriad factors that can impact the due diligence phase, for better or for worse, being aware of real-world scenarios will help better inform buyers, sellers, and advisors how to avoid unnecessary challenges or surprises. By doing so, they can keep deals moving in the right direction, ultimately leading to a successful transaction.