Français

Français

Introduction

Given the economic turmoil observed across a variety of industries in recent years, the possibility of preference demand letters has been a significant concern for creditors of all types. According to §547 of the Bankruptcy Code, after filing for bankruptcy the debtor may recover transfers occurring in the 90 days prior to the filing, provided the transfers meet certain criteria. Conversely, the creditor has several defenses to defend against preference claims in order to retain transfers previously received.

One such defense frequently employed by creditors has been the industry ordinary course defense. This defense often involves reference to public sources of industry information in order to establish that the transfers were ordinary based on observed payment practices in the relevant industry. However, depending on the information available, data obtained directly from the creditor or debtor relating to historical accounts payable transactions, accounts receivable transactions, and other indications of payment practices may provide an alternative or complement to defining industry ordinary course for payment practices.

Preference Background

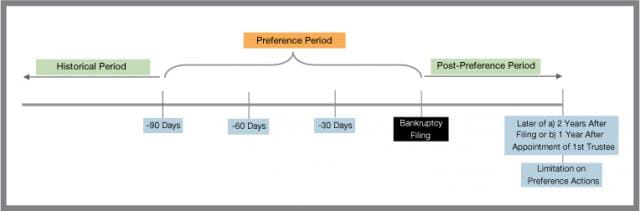

By definition, a preferential transfer is any “transfer” to or for the benefit of the creditor during the 90 day period counting backwards from the bankruptcy filing date. A “transfer” is anything of value, whether or not tangible, that the bankrupt customer gave any creditor or gave up for the benefit of a creditor for any reason.

Preference cases are likely to be prevalent in coming years. According to the statute of limitations as outlined in §546 of the Bankruptcy Code, preference actions may not be commenced after the later of: a) two years after the entry of the order for relief; or b) one year after the appointment or the election of the first trustee.1,2

Typically, trustees wait to commence such actions in an effort to maintain vendor relationships for as long as possible. Oftentimes, trustees file a host of preference claims immediately prior to the cut-off date indicated by the statute of limitations. Bankruptcy preferences and any adversary proceedings brought to recover bankruptcy preference claims are often the last step in the bankruptcy process, whether it is filed under Chapter 7 or Chapter 11.

Creditor Defenses to Preference Claims

A creditor will often defend a preference claim by proving that the alleged transfers are not preferential and thus not recoverable by the debtor. While there are several approaches to defending preference actions, an increasingly common defense used by creditors is the ordinary course defense where the creditor seeks to demonstrate that the transfers occurred consistent with the ordinary course: a) in the industry; or b) in the relationship between the parties.

Prior to 2005, in order to defend preference actions, it was necessary for the creditor to demonstrate that the transfers were made according to the ordinary course in the industry and between the parties. The Bankruptcy Abuse Prevention And Consumer Protection Act Of 2005 amended §547(c)(2) of the Bankruptcy Code, making it necessary only to prove the transfers occurred in the ordinary course within the industry or between the parties, attempting to make the ordinary course preference defense easier and less costly.3

While the creditor may defend against preference actions through the ordinary course defenses as well as arguments for new value and contemporaneous exchange, this article will focus on issues pertaining to the industry ordinary course defense. However, the arguments of ordinary course between the parties, new value, and contemporaneous exchange are also important to consider as possible defenses to preference claims.

Ordinary Course Defense to Preference Claims

Ordinary Between the Parties – Subjective Test

In establishing the ordinary course defense relating to the relationship between parties, the timing and method of transfers between the parties is often of primary importance. Preference period transfers are typically analyzed to establish whether they were consistent with transfers made historically. While the subjective test is an important consideration in the ordinary course defense, the focus of this article will be on the objective test relating to established industry ordinary course.

Ordinary in the Industry – Objective Test

Comparisons to industry standards are often used to establish a reasonable basis for ordinary course. As stated by Scott Blakeley and Terry Callahan of the Credit Research Foundation, when establishing the industry ordinary course defense, “although the industry standard does not require a creditor to establish the existence of a uniform set of business terms, it does require evidence of a prevailing practice among similarly situated members of the industry facing the same or similar problems.”4

Many factors may impact the court’s ruling on whether the alleged preferential transfers occurred within industry “ordinary course.” In the bankruptcy case of Smith Road Furniture, the court made a special point that “the more established the trade relationship between the parties, the more that a creditor will be permitted to deviate from the industry standard and still qualify for the ordinary course of business exception. However, it is the creditor’s burden to establish the industry payment standard.”5

In general, issues commonly considered by courts in determining whether the alleged preferential transfers were ordinary include, but are not limited to:

If any of these factors are present, a court may find that the transfer does not qualify for an ordinary course of business defense.6

Sources of Data Utilized to Define Industry Ordinary Course

When defining industry ordinary course, the creditor will often refer to sources of public information pertaining to Payment Days, Days Sales Outstanding (“DSO”),7 and Days Payable Outstanding (“DPO”).8 Such sources of information may include Capital IQ, the Risk Management Association, Dunn & Bradstreet reports, and information from the Credit Research Foundation.

Limitations of Common Industry Publications

While the common industry sources for payment and credit information mentioned can be helpful, they can also pose certain limitations. Certain sources have been provided information anonymously and the information may or may not have been audited or verified for accuracy or consistency. Further, these sources of information do not provide information in a format that is searchable, sortable, or otherwise well-suited for analysis beyond the quartile metrics stated in the publication. For example, these sources of information will not allow an analysis of distribution of industry conduct; rather, they will frequently only provide a 25th percentile, median (50th percentile), and 75th percentile. The remaining distribution on either side of these percentiles can still be considered ordinary in an industry but can be difficult to assess without significant additional information.

Most public sources of information are also only published on a periodic basis. This can limit the degree of analysis that can be performed in industries or economic circumstances that are fluctuating over a shorter period. As such, while these sources provide an indication of industry standards, if more detailed information is available from the creditor or debtor, it should be reviewed and analyzed to assist in further understanding ordinary conduct in an industry.

Using Company Data to Establish Industry Ordinary Course

Given the limitations that are sometimes observed with industry data, it is often relevant to consider records from the creditor and debtor detailing receivables and payables transactions and balances specific to their customer and supplier or vendor base. Such information can be utilized as an additional proxy for ordinary course with respect to payment behavior between suppliers and customers in the industry.

Similar to an analysis giving primary consideration to public sources of information, an analysis of industry ordinary course based on company data will often require consideration of key metrics relating to payment practices.

Use of Creditor Data

The analysis of the creditor’s data will often start with an identification of the customers most relevant for defining the appropriate industry. For example, if the creditor is a supplier of electronic components, it may supply such products to both the Automotive and Aerospace Industries. It may be necessary to identify those customers within the creditor’s accounts receivable and payment receipt information that are most similar to the debtor.

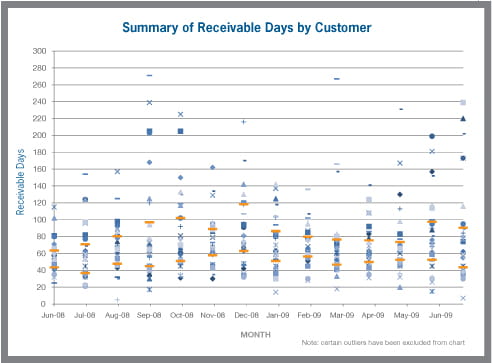

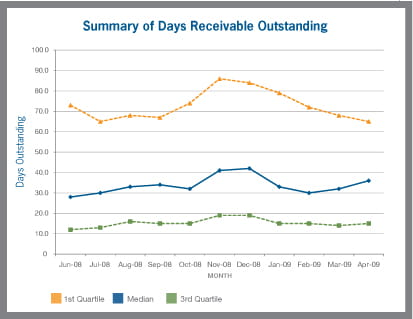

Once the relevant customer data is identified, it is then often necessary to analyze the data based on several common payment metrics such as DSO or Payment Days (giving consideration to any fluctuation in payment terms offered to individual customers).9 For example, if information is obtained from the creditor detailing the monthly aging of accounts receivable for each customer in total, such data may be utilized to calculate average DSO. Alternatively, if information is available regarding individual invoices outstanding for each month, actual DSO may be calculated for each invoice. Further, if information is available regarding when payments were made on individual invoices, such data can be utilized to calculate actual Payment Days for these invoices.

As indicated in the following charts, this analysis provides the opportunity to evaluate several factors that may not be transparent in the use of common industry publications. This approach facilitates an investigation of how overall payment trends may have changed over time for the industry, how the distribution of payment practices (how flat or tall the bell curve is) has changed over time, and whether any sub-group of the industry appears to have unique payment practices that should be further investigated. In general this approach, if available, can provide for a more precise analysis and one more capable of identifying an “industry” of companies that were similarly situated to the creditor and debtor at the time of the transfers.

Based on an analysis of average, median, quartile, and percentile values for each metric, an ordinary range for each metric may be established. While the most direct comparison to payment practices on individual invoices is Payment Days, accounts receivable metrics such as DSO are also often a reasonable proxy. Based on this analysis, a reasonable range for ordinary payment practices may be established.

Use of Debtor Data

Similar to the analyses that may be performed based on creditor data, it is also often relevant to consider historical payables and payment information specific to the debtor and its relationship with its suppliers.

Such an analysis will once again require a certain degree of analysis in order to identify the most appropriate companies to include in defining the industry. Once the industry is defined, metrics may be calculated in order to determine ordinary payment practices between the debtor and its suppliers. However, instead of receivables information, the relevant data will most often relate to accounts payable information and payments made by the debtor to its suppliers.

If sufficient information is available, both the creditor and debtor data may be utilized to assess industry ordinary course. If such information results in observations of industry ordinary course that are consistent with other information considered, the conclusions regarding industry ordinary course may be strengthened. In the event there are differences among different sources, it may be appropriate to assess the reasonable explanations for those differences and whether the information provided from one data source may be more reliable or applicable than another.

Conclusion

Comparisons to industry standards are often used to establish a reasonable basis for ordinary course. Establishing the industry ordinary course defense requires evidence of a “prevailing practice among similarly situated members of the industry facing the same or similar problems.”10 In gathering such evidence, a creditor will often refer to sources of public information pertaining to Payment Days, DSO, and DPO.

However, due to the limitations of these publicly available sources of information, it is often relevant to consider records from the creditor and debtor detailing receivables and payables transactions and balances. Such information can be utilized as an additional proxy for industry ordinary course. The analysis of industry ordinary course in bankruptcy preference matters can be significantly improved with the combination of a) consideration of publicly available research and b) information that can be gathered through discovery from both the debtor and creditor on their actual payment practices during the preference period.

1 U.S. Code Collection, §546 Limitations on Avoiding Powers, Cornell University Law School, 14 July 2009, <law.cornell.edu>.

2 In the event the bankruptcy case is closed or dismissed prior to these two events, this will mark the cut-off date for preference actions.

3 Andrew C. Kassner, “The Bankruptcy Abuse Prevention And Consumer Protection Act Of 2005: The Impact On Chapter 11 Re-Organization - Part II,” The Metropolitan Counsel, 1 June 2006.

4 Scott Blakeley and Terry Callahan, “In Defense of a Preference,” The Credit Research Foundation, 2004.

5 Scott Blakeley and Terry Callahan, “In Defense of a Preference,” The Credit Research Foundation, 2004. In re Smith Road Furniture, Inc., 304 B.R. 793 (Bankr. S.D. Ohio 2003).

6 Scott Blakeley and Terry Callahan, “In Defense of a Preference,” The Credit Research Foundation, 2004.

7 T his metric is often referred to as Accounts Receivable Days Outstanding (“ARDO”). Note that these metrics are not appropriate as direct comparison to Payment Days on individual invoices. Such metrics only measure the company’s receivables in aggregate, and do not provide Payment Days specific to individual invoices, which are often in dispute in the preference action. However, these metrics may be utilized as a reasonable proxy for industry ordinary course.

8 T his metric is often referred to as Accounts Payable Days Outstanding (“APDO”)

9 T his metric is typically calculated based on the time from the invoice date to payment date.

10 Scott Blakeley and Terry Callahan, “In Defense of a Preference,” The Credit Research Foundation, 2004</law.cornell.edu>