English

English

Background

Debt securities occasionally include equity instruments such as warrants or options. When debt is issued with an equity-like instrument, it is important to determine whether the instrument is freestanding or embedded. A freestanding financial instrument is defined as an instrument that is either (i) entered into separately and apart from any of the entity’s other financial instruments or equity transactions, or (ii) entered into in conjunction with some other transaction and is legally detachable and separately exercisable.1 U.S. GAAP requires a discount on the issue price of debt based on the value of a freestanding equity instrument at the time of investment.2 Specifically, ASC 470-20-25-2 stipulates that the “portion of the proceeds allocated to the warrants shall be accounted for as paid-in capital,” and the “remainder of the proceeds shall be allocated to the debt instrument portion of the transaction.”3 Thus, the debt and the freestanding equity instrument are accounted for separately.

Ultimately, the issue price of debt equals the amount issued minus any stated original issue discount (OID) minus the value of the freestanding warrants at investment. Similarly, the par value equals the issue price of the debt at investment plus any stated OID plus the value of the freestanding warrants as a percent of debt issuance.

Why Do Issuers Issue Equity With Debt?

Typically, issuers that provide equity with debt carry higher risk. For example, the issuing company may be a newly combined entity with integration risk, be in the early stages of development with expansion risk, or have other risk characteristics. In return for the added equity component, the issuers may receive a lower interest rate, all else equal, and potentially a higher dollar commitment.

Why Do Credit-Focused Funds or Other Investment Firms Accept This Structure?

Debt investments have modeled cash flows as described in a credit agreement and do not have much upside beyond what is known at the time of investment. Warrants, when converted to common equity or sold to another party, provide additional returns. Further, debt has a stated maturity, while warrants can be held beyond the debt maturity, which acts like a continuation vehicle for firms beyond the stated maturity of debt. Additionally, refinancing typically occurs at par, while a buyout of the warrants would occur at the fair value of the warrants, or they can be converted to common. If common stock value rises, value to warrant shareholder increases.

Methodologies to Determine Fair Value

In determining the fair value of an equity instrument, there are two commonly used methodologies: the fully diluted method and the option pricing method.

Fully Diluted Method

The fully diluted method is used for scenarios such as when the issuer has a simple equity structure, an exit is expected in the near-term, the warrants were issued with a low strike price, and/or there is a lack of information. When determining the value of the equity instrument using the fully diluted method, the issuers equity value is allocated equally among all share classes as if they are pari passu. Downsides to the fully diluted method include the lack of consideration to additional upside or preferences offered to each specific share class, such as a guaranteed return to preferred shares prior to common stock, warrants, or options receiving any value. Additionally, the fully diluted method is not a forward-looking methodology such as an option pricing model.

Option Pricing Model (OPM)

Option pricing models are typically used for complex capital structures using a series of Black-Scholes models to allocate the equity value by creating a portfolio of artificial options with specific strike prices, or breakpoints, and using each security’s liquidation preference.4 The OPM method considers the preferences offered to each specific class of preferred shares, common shares, restricted shares, options, and warrants, rather than allocating the subject equity value to all share classes equally as done in the fully diluted basis method.

Discounts for Lack of Marketability (DLOM)

A discount for lack of marketability may be used whether the equity instrument is valued using a fully diluted method, an OPM, or a combination of the two. DLOMs are used to adjust the value of closely held and restricted securities. The theory behind a DLOM is that a valuation discount exists between a security that is publicly traded, which has a marketplace, and the market for a privately held security, which has little or no marketplace.5 Warrants issued with debt may be subject to lock-up terms, whereby the warrants are unable to be sold for a strict period of time. Thus, it is customary to include a discount for lack of marketability to account for the illiquidity of the security. The Finnerty put option model is commonly used to calculate the DLOM and uses an average-strike put option. The strike price is based on the predetermined period average value of the underlying asset.6

Example

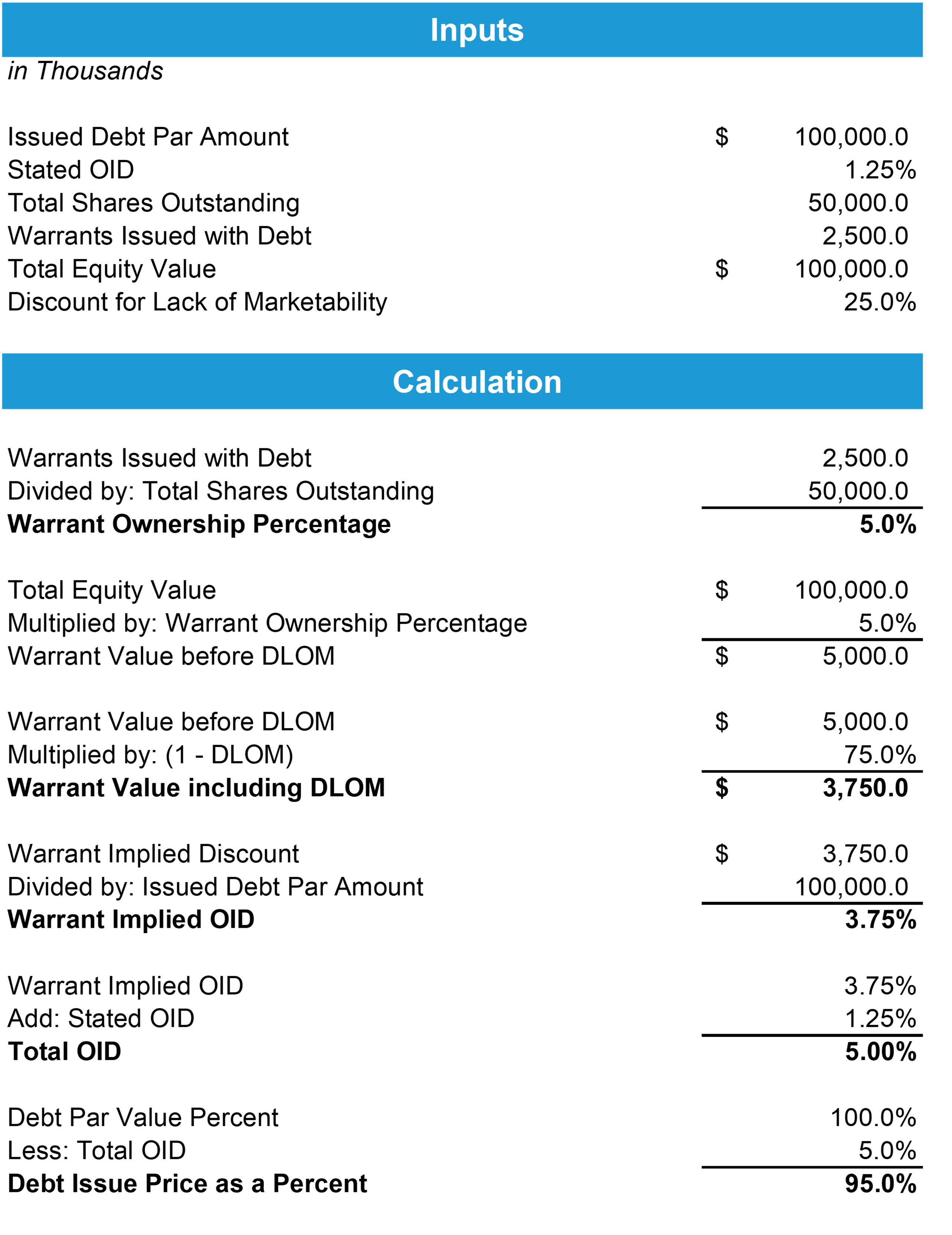

In this example using a fully diluted method, we assume the following facts: $100.0 million in debt was issued with a stated 1.25% OID, there are 50.0 million shares outstanding (including the freestanding warrants issued), 2.5 million warrants were issued with the debt, the equity value is $100.0 million, and the discount for lack of marketability was determined to be 25.0%.

First, we calculate the warrants’ ownership percent as a percent of the fully diluted shares – this is 5% (2.5 million shares divided by 50 million shares times 100%). Next, we apply the 5% ownership to the total equity value of $100 million, which would imply a freestanding warrant value of $5 million, before the DLOM. Then, the discount is applied to the subject warrant value for the lack of marketability by multiplying the subject interest by one minus the DLOM of 25%. The resulting equity value available to the warrants equals $3.75 million. This value is used as an implied discount on the debt. Thus, the value allocated to the debt at issuance is $96.25 million, prior to the stated OID, and the warrant implied OID equals 3.75%. After applying the stated OID of 1.25% and the implied warrant OID of 3.75%, the issue price of the debt equals 95% or $95 million.

Conclusion

A discount on the issue price of debt for a freestanding equity instrument issued in conjunction with the debt is required to calculate the fair value of debt and implied OID at investment. Additionally, credit-focused funds or other investment firms accept warrants, as they can provide additional upside over the contractual cash flows of the debt structure, while issuers can receive more favorable terms than issuing debt without the equity-like instruments.

Ultimately, creditors that seek to enhance returns via attaching warrants to debt need to ensure they value the equity interests separately from the debt component for financial reporting purposes. Stout’s valuation professionals can provide independent guidance in this process.

Jake Marinelli also contributed to this article.

- PWC, “Chapter 5.3: Equity-linked instruments model,” December 31, 2022.

- Marcum LLP, “Drafting Considerations for Attorneys Blog Series: Debt Issued With Warrants and Convertible Debt,” September 8, 2016.

- PWC, “Chapter 8.4: Accounting for freestanding instruments issued together,” December 31, 2021.

- BDO USA LLP, “Demystifying Valuation Methodologies: Part 1 - The Option Pricing Model (OPM),” November 19, 2019.

- Investopedia, “Discounts For Lack of Marketability (DLOM): Role in Valuation,” May 29, 2020.

- Withum Smith+Brown, PC, “Discount for Lack of Marketability: Finnerty Model,” October 17, 2017.