English

English

Through the release of the Financial Accounting Standards Board’s (FASB) Accounting Standards Update (ASU) No. 2011-08, a qualitative assessment to the goodwill impairment process (i.e., the “Step 0 Test”) is allowed as a precursor to the traditional two-step quantitative process. In general, the Step 0 Test allows an entity to first assess qualitative factors to determine whether there is more than a 50% likelihood that the fair value of a reporting unit is less than its carrying value. In order to make this evaluation, the FASB outlines relevant examples and circumstances to consider, including:

- General macroeconomic conditions such as a deterioration in general economic conditions, limitations on accessing capital, fluctuations in foreign exchange rates, or other developments in equity and credit markets

- Industry and market conditions such as a deterioration in the environment in which an entity operates, an increased competitive environment, a decline in market-dependent multiples or metrics (in both absolute terms and relative to peers), a change in the market for an entity’s products or services, or a regulatory or political development

- Changes in cost factors such as increases in raw materials, labor, or other costs that have a negative effect on earnings and cash flows

- Overall financial performance for both actual and expected performance

- Entity- and reporting unit–specific events such as changes in management, key personnel, strategy, or customers; contemplation of bankruptcy; litigation; or a change in the composition or carrying amount of net assets

- A sustained decrease in share price in both absolute terms and relative to peers, if applicable

In reviewing public filings and press releases where impairment is indicated, there is often more than one factor cited as the reason for the impairment occurring, making it critical for entities considering the implementation of the Step 0 Test to understand the magnitude a factor may have on a fair value conclusion. The following case study provides some insight into how different qualitative factors may be determined and ultimately used to form a Step 0 Test conclusion.

Case Study

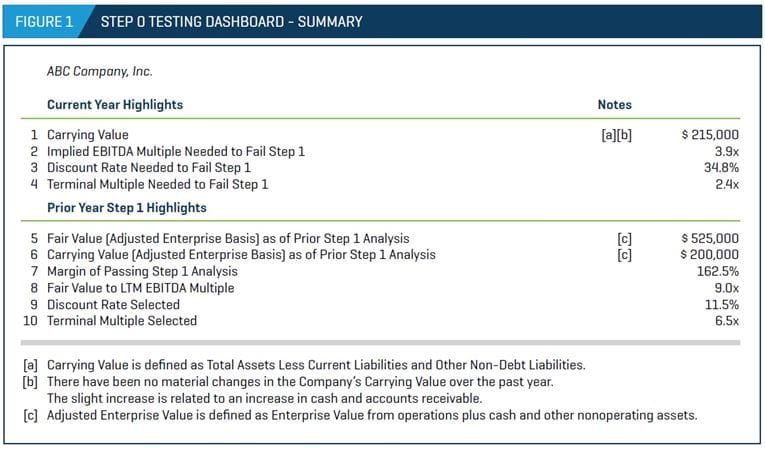

ABC Company, Inc. (“ABC,” or the “Company”), composed of a single reporting unit, is focused on high-end services in its industry. The Company has experienced significant growth over the past several years, while maintaining higher-than-average earnings before interest, taxes, depreciation, and amortization (EBITDA) margins. The Company performed its annual goodwill impairment test one year prior (the “CY-1 Test”), which resulted in a fair value of $525 million compared with a carrying value of $200 million (i.e., a cushion of $325 million, or 162.5%), as seen in Figure 1. Given ABC’s historical cushion of fair value over carrying value and its recent financial performance relative to its peers, the Company believes that a low probability of impairment exists for its current fiscal year impairment test (the “CY Test”). Thus, the Company has elected to perform a Step 0 Test.

In addition to a review of general quantitative factors, ABC’s Step 0 Test consists of an in-depth qualitative factor analysis. Applicable qualitative factors are segregated by valuation methodology.

In general, the Step 0 Test may prove to be much less time-consuming for public companies and/or companies with a good set of public company comparables, or in a market with a number of recent comparable transactions. This is because the availability of market data to support general quantitative assumptions will be more robust.

Market Approach Considerations

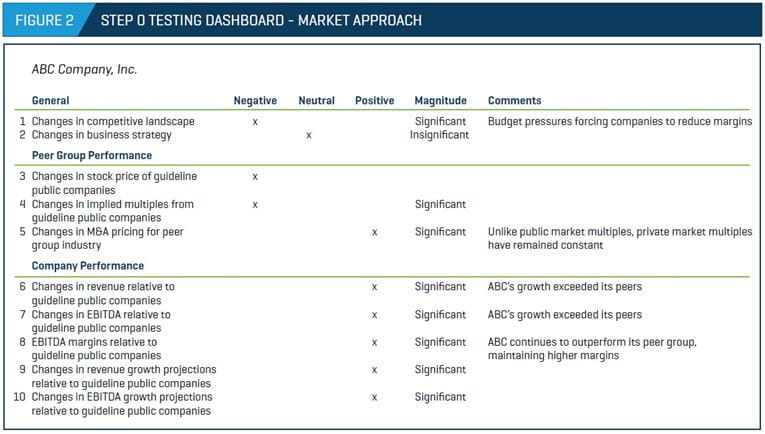

To investigate the sensitivity around the changes in the market approach factors from ABC’s CY-1 Test, the following quantitative factors were considered.

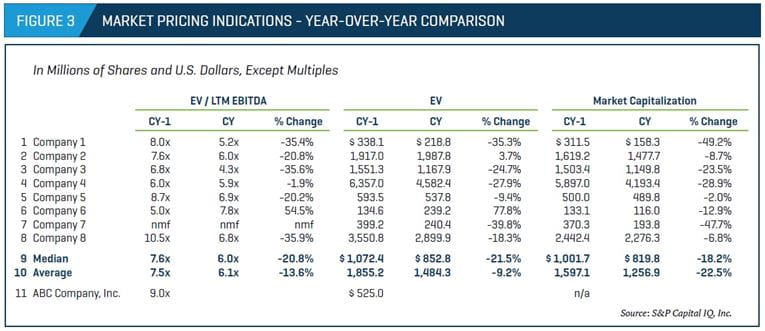

To help support the magnitude and overall impact of the qualitative factors outlined in Figure 2, trends in the public market data were reviewed to provide some quantitative support for the Step 0 Test. As shown in Figure 3, companies in ABC’s peer group were trading at median and average multiples of 6.0x and 6.1x latest 12 month (LTM) EBITDA, respectively, as of the CY. For the CY-1, those same companies were trading at median and average multiples of 7.6x and 7.5x LTM EBITDA, respectively. ABC’s implied LTM EBITDA multiple (based on the fair value concluded from the CY-1 Test) was 9.0x, which implied a premium relative to the guideline public companies. The current carrying value of ABC implies a 3.9x EBITDA “hurdle” multiple, which is well below the range of multiples exhibited by the guideline public companies (the lowest is 4.3x) as of the CY. [Although not presented herein, guideline transactions should also be considered when determining appropriate EBITDA multiples, as there can often be overriding factors that suggest one approach is more appropriate than is another in a given situation. For example, in ABC’s industry, sales of public companies have resulted in significant premiums being paid over the target’s market value.]

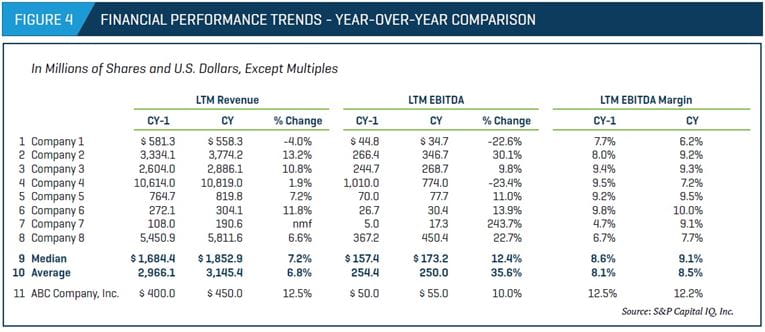

Because there are a number of factors that can influence an appropriate multiple to select (e.g., growth factors, profitability, and risk), ABC’s performance relative to its peer group was also considered. As shown in Figure 4, ABC outperformed its peer group in regard to revenue growth over the past year; however, its recent EBITDA growth was in line with its peer group. ABC’s current EBITDA margin, while slightly lower than the CY-1, is approximately 400 basis points higher than the median and average peer group margins. These factors suggest that an appropriate EBITDA multiple for ABC may be higher than that of the guideline public companies and, at a minimum, higher than the 3.9x LTM EBITDA hurdle multiple implied from the current carrying value.

Income Approach Considerations

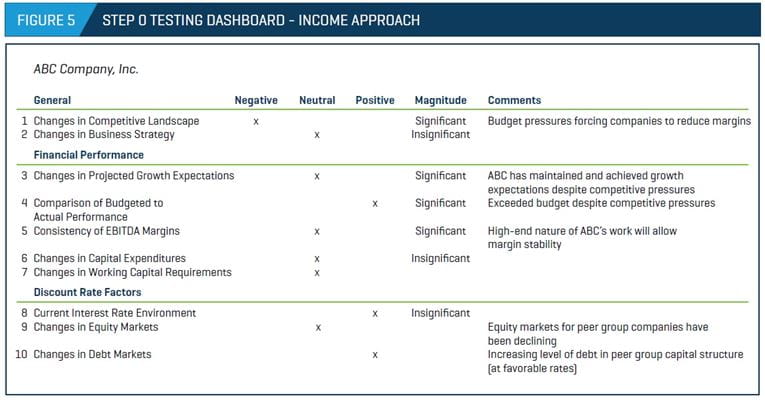

To investigate the sensitivity around the changes in the income approach factors from ABC’s CY-1 Test (Figure 5), the following qualitative factors were considered (some of which overlap with the market approach assessment). ABC exceeded its CY budget, despite competitive pressures to reduce margins and government budgetary constraints. The Company has been able to maintain its profit margins, as the high-end nature of its services in niche markets has not been impacted to the same extent as the general industry. Furthermore, favorable interest rates have allowed companies in the industry to recapitalize with a higher percentage of debt in their capital structure than historical averages. Overall, these specific factors support the more-likely-than-not assumption that fair value exceeds carrying value.

In general, the income approach assessment may require further quantitative analysis because various inputs may be more or less sensitive than others in terms of impact on fair value (e.g., discount rate, long-term growth rate, sustainable margin level).

Case Study Takeaways

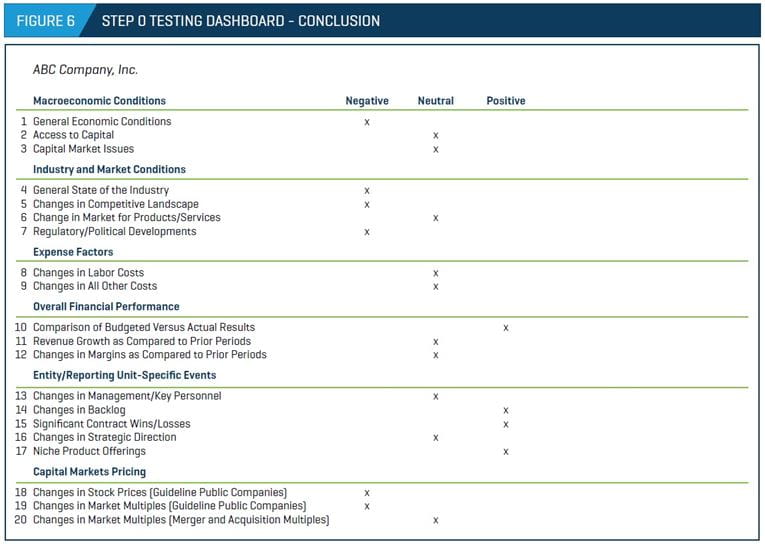

Assessing the magnitude of the impact of each qualitative factor may be challenging without some level of quantitative support. Moreover, ignoring a determination of the magnitude of each qualitative factor may result in an ambiguous Step 0 Test result. For example, simply using the summary factors in Figure 6 without commentary or indications of magnitude would make it difficult to clearly support a more-likely-than- not conclusion since certain company-specific trends may offset or dominate over negative industry or market conditions (or vice versa).

Indefinite-Lived Intangible Assets

Similar to the goodwill test, the FASB also introduced a qualitative assessment to the impairment process for indefinite-lived intangible assets via the release of ASU No. 2012-02. While a number of the aforementioned factors could be applied to an intangible asset Step 0 Test (e.g., discount rate considerations, changes in revenue/profits, and future growth expectations), the applicability of such factors could depend on the type of valuation methodology used for the subject intangible asset (e.g., relief-from-royalty approach, multi-period excess earnings, cost approach). It will also be important to understand whether there has been any shift in the relevance of the subject intangible asset to the overall business. For example, a new product introduction or shift in market share could negatively impact the market royalty rate applicable to an indefinite-lived intangible asset, such as a trade name. Other common indefinite-lived intangible assets include franchises, Federal Communications Commission licenses, and customer-related assets. These assets have unique value drivers and will need to be reviewed individually to determine the likelihood of impairment.

Consider Supplemental Quantitative Analyses

The Step 0 Test certainly provides increased flexibility to simplify the annual impairment testing process. However, given the aforementioned FASB factors to consider when applying the Step 0 Test, it does not imply that no analysis needs to be performed. The case study cited a number of market-based metrics that may be considered within the constructs of performing a Step 0 Test, many of which could require supplemental quantitative analyses. Further, these supplemental analyses will likely be of greater importance to the extent the “gap” between fair value and carrying value in prior impairment tests is small, yielding a greater level of scrutiny during the review process.

This is an updated version of an article published in the Spring 2012 issue of The Journal.