English

English

The prospect of valuing privately held assets held in a marital estate can greatly increase the complexity of a typical domestic relations matter. Further, when these assets consist of financial incentives, such as a carried interest in a private equity fund or a performance fee in a hedge fund, the complexity of a case can increase exponentially. Many family law practitioners may find themselves so deep in a sea of technical terms and winding fund structures that efficient and effective resolution of such cases may prove elusive. However, a general understanding of private equity and hedge funds, their manager incentives (i.e., carried interests and performance fees) and the valuation of these assets can assist the family law practitioner in cutting the Gordian knot created in these matters.

Private Equity and Hedge Funds Defined

Private equity and hedge funds are professionally managed pools of capital that invest in the equity, debt, and other securities issued by companies (both public and private), derivative investments (such as futures and options in indexes), currencies or commodities, and other securities. These vehicles are usually funded by pension funds, endowment funds, and accredited investors with the goal of generating a higher rate of return than is typically available in other asset classes. Given the strategies employed by the funds and the asset classes in which they invest, these vehicles can also provide a greater degree of diversification than their investors may otherwise enjoy.

Private Equity Funds

Private equity funds typically fall into three categories, including venture capital, buyout, and mezzanine and distressed funds. Funds generally make controlling equity investments in private or public companies while focusing on long-term appreciation in these assets (i.e., maximizing exit multiples) over a three- to 10-year investment horizon. For many of these investments, a fund will employ significant leverage (i.e., debt financing) to enhance equity rates of return.

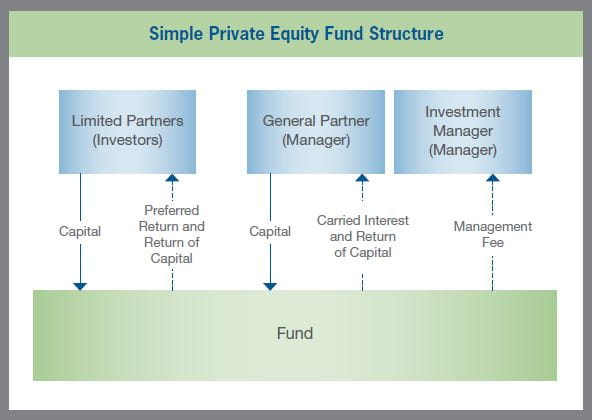

Private equity funds are usually organized as limited partnerships with investors (the limited partners) providing capital and the managers of the fund serving as the general partners. As illustrated in the following table, a common private equity fund structure includes two management-related entities: a general partner and an investment manager. Additionally, some funds employ a master feeder structure whereby investors contribute capital to onshore and offshore feeder entities, which then invest this capital in a master fund that makes all portfolio investments on behalf of the fund.

The managers of a private equity fund, through the general partner and investment manager, are responsible for making all decisions surrounding the activities of the fund, including acquisitions, capital calls, divestitures, etc. In exchange for this oversight, the managers receive a management fee (often 2% of committed capital / assets under management), reimbursement for fund expenses, and a carried interest. Conversely, the investors in the private equity fund (i.e., the limited partners) receive a preferred return on their contributed capital, which accrues until the fund begins making distributions. Preferred returns generally range from 7% to 10% per annum.

Hedge Funds

Hedge funds operate similarly to mutual funds in that investors can buy and sell interests in a fund at a price based on the underlying net asset value of the fund. However, hedge funds are able to invest in a broader array of securities than mutual funds, such as derivatives, and can also take short positions in these securities. These funds are often set up as limited partnerships or limited liability companies, with the investors comprising the limited partners or members of the fund and the managers acting as the general partner or manager. Hedge funds are also characterized by the investment strategies they employ, with common fund strategies including: 1) equity long/short; 2) tactical trading; 3) relative value; and 4) event driven.

Unlike private equity funds, hedge funds often employ shorter-term investment strategies, with some funds even focusing on executing high-volume, small-margin trades hundreds or thousands of times per day. Moreover, many hedge funds develop extensive trading algorithms to analyze information and aid in the direction and execution of proprietary trading strategies. Like a private equity fund, the managers of a hedge fund make all substantive decisions regarding the fund’s operations and investment activities. For their services, the managers receive a management fee, reimbursement for fund expenses, and a performance fee or allocation, which represents a percentage of the fund’s returns over a high-water mark or other hurdle.

Incentives for Managers of Private Equity and Hedge Funds

The purpose of a private equity or hedge fund is to raise capital, invest that capital, and earn a rate of return higher than conventional investments. The success or failure of a private equity or hedge fund is highly dependent upon the capabilities of the manager. Accordingly, certain vehicles have been developed in order to reward the managers of these funds for the successful deployment of the fund’s capital. These vehicles include a carried interest in a private equity fund and a performance fee in a hedge fund.

The Private Equity Fund Carried Interest

A carried interest in a private equity fund represents an economic benefit that accrues to the general partner independent of the general partner’s investment contribution. A typical carried interest receives 20% (but this amount can range between 10% and 40%) of the private equity fund’s distributions after: 1) all investment and management expenses have been paid; 2) invested capital has been returned to all partners; and 3) accrued preferred returns have been paid to the limited partners. Effectively, the carried interest holder only receives distributions when the private equity fund generates an annualized return in excess of the preferred return.

The Hedge Fund Performance Fee

A performance fee in a hedge fund also represents an economic benefit that accrues to the manager. Performance fees are generally 20% of fund returns, but may range as high as 50% in some instances. Further, to ensure that managers only receive performance fees when the value of a hedge fund is rising, these fees are generally only paid out when the net asset value of the fund is above the level at which the performance fee was last paid. This level is commonly referred to as the high-water mark.

Valuation of Carried Interests and Performance Fees

Carried Interests

The value of an asset is derived from its expected future cash flow after consideration of the risk associated with realizing this cash flow. A carried interest represents a share in the residual claim on a private equity fund’s distributions after the return of invested capital and the payment of management fees and accrued preferred returns. As such, the cash flow potential of a carried interest is dependent upon the fund generating a sufficiently high rate of return. Two commonly used methods to value carried interests include a discounted cash flow method and an option pricing method.

Discounted Cash Flow Method

The discounted cash flow method projects a carried interest’s expected future cash flows and discounts them at a rate of return commensurate with the risk inherent in realizing those cash flows. This approach requires making assumptions regarding the private equity fund’s rate of return and investment holding period, and then applying an appropriate rate of return to these cash flows over the specified holding period.

The rate of return used to discount the projected cash flows is correlated with the expected portfolio return for the entire fund and, thus, can be derived in part from this return. Further, since the fund’s investors receive preferred returns before any net proceeds are paid to the carried interest holders, the projected cash flows attributable to the carried interest are riskier than the projected cash flows associated with the invested capital. As a result, the rate of return applicable to the carried interest is generally higher than the gross portfolio rate of return of the underlying assets.

Option Pricing Method

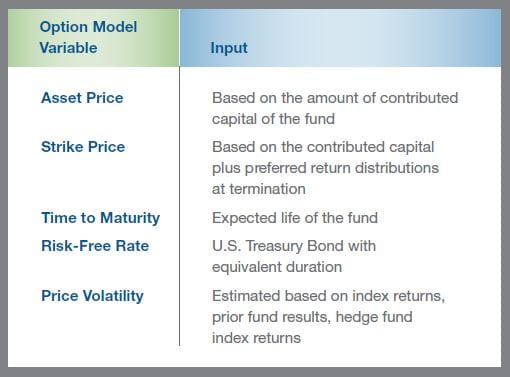

A carried interest may also be valued using standard option pricing theory. A carried interest is similar to a simple call option as it gives the holder the right to the value of an asset over a specified threshold (i.e., the strike price) for a specified period of time. As it relates to a carried interest, the strike price is the capital contributed by investors plus the accumulated preferred return at fund termination.

Option pricing models are arbitrage pricing models that were developed using the premise that if two assets have identical payoffs, they must have identical prices to prevent arbitrage opportunities (i.e., riskless profit). These models consider five variables in calculating the price of a traditional call option, including: 1) asset price; 2) strike price; 3) time to maturity; 4) risk-free rate of return; and 5) the price volatility of the underlying asset (i.e., risk). The following chart details the inputs used for each of these variables in the valuation of a carried interest.

Performance Fees

Similar to a carried interest, the value of a performance fee in a hedge fund is derived from its expected cash flow after consideration of the risk associated with realizing the expected cash flow. However, a performance fee in a hedge fund can differ from a carried interest in a few ways. First, many funds do not have a return hurdle that must be met before distributions are made to the performance fee holders. Second, unlike private equity funds, many hedge funds do not have specific termination dates. Finally, while private equity investors’ capital is locked up for the duration of a fund, hedge fund investors can usually withdraw their capital after meeting certain fund-specific requirements. Thus, while a discounted cash flow method may be used to value a performance fee, the option pricing method is generally not applicable.

Discounted Cash Flow Method

Similar to the valuation of a carried interest, applying a discounted cash flow method requires making assumptions about the hedge fund’s expected returns and the risk associated with realizing those returns. However, as discussed above, there are three areas where a performance fee valuation may differ from a carried interest valuation, including the term of the fund, the hurdle rate that must be met before distributions are made, and investor redemptions.

Term of the Fund

Most private equity funds have a finite life specified in the fund’s private placement memorandum or operating/partnership agreement. The term of the average private equity fund is between three and 10 years. Conversely, many hedge funds do not have a specific term and some hedge funds are perpetual (i.e., no termination date). Thus, while a carried interest may be valued using a discrete or finite set of projected cash flows, the valuation of a performance fee may require the use of a discrete set of cash flows coupled with a residual period that is capitalized into perpetuity.

Hurdle Rate

As discussed above, a carried interest is a residual interest in the cash flows of a private equity fund because the fund must return investors’ contributed capital and the accrued preferred return before making distributions to the carried interest holders. Thus, a carried interest has no value unless the underlying private equity fund generates a return in excess of the preferred return.

A typical hedge fund only requires that a high-water mark is met before distributions are made to the performance fee holders. The high-water mark feature ensures that the performance fee is only paid when the hedge fund’s net asset value (i.e., the net value of all the fund’s underlying investments) has increased since the last time the fee was paid out. In effect, the holder of the performance fee receives distributions on all positive returns generated by the fund since the last performance fee distribution was made.

Investor Redemptions

Investments in private equity funds are generally illiquid as most funds forbid the withdrawal of limited partner capital prior to the termination of the fund.[1] Thus, in projecting the returns expected to be generated by the fund, no consideration needs to be given to redemptions of investor capital. In a typical hedge fund, however, investor redemptions are generally allowed upon written request of the investor and after a relatively short lock-up period has been met. As such, a reduction in capital due to investor redemptions must be considered when projecting the future returns of the fund.

Conclusion

The existence of complex financial incentives in a marital estate can create hurdles to the efficient and effective resolution of marital dissolution matters. However, an understanding of the structure and purpose of these incentives, as well as the underpinnings of the valuation of these assets, can add a great deal of clarity to a case.

- Many institutional investors have recently begun selling their private equity limited partners interests in private, secondary market transactions. While this may be an option for some private equity fund investors to gain liquidity, there are still several steps that must be taken such as getting approval of the general partner of the fund, finding a buyer, etc., before an interest can be sold. Further, this would have no effect on the aggregate invested capital of the fund as these sales are executed on the secondary market and are not redemptions by the fund.