Italiano

Italiano

New tariffs and their impacts on U.S. businesses have been at the forefront of recent news. While the automotive industry received a lot of this attention, tariffs are only its latest headwind. The U.S. automotive industry began reporting sales declines prior to COVID-19, which were then exacerbated from pandemic-induced parts and labor shortages, the war in Ukraine, a United Auto Worker’s Strike (UAW) and high interest rates. In addition to sales declines, the rapid pace of technological advancement has both shortened vehicle platform lives and contributed to increased warranty and recall expenses, further straining the profitability of automotive companies.

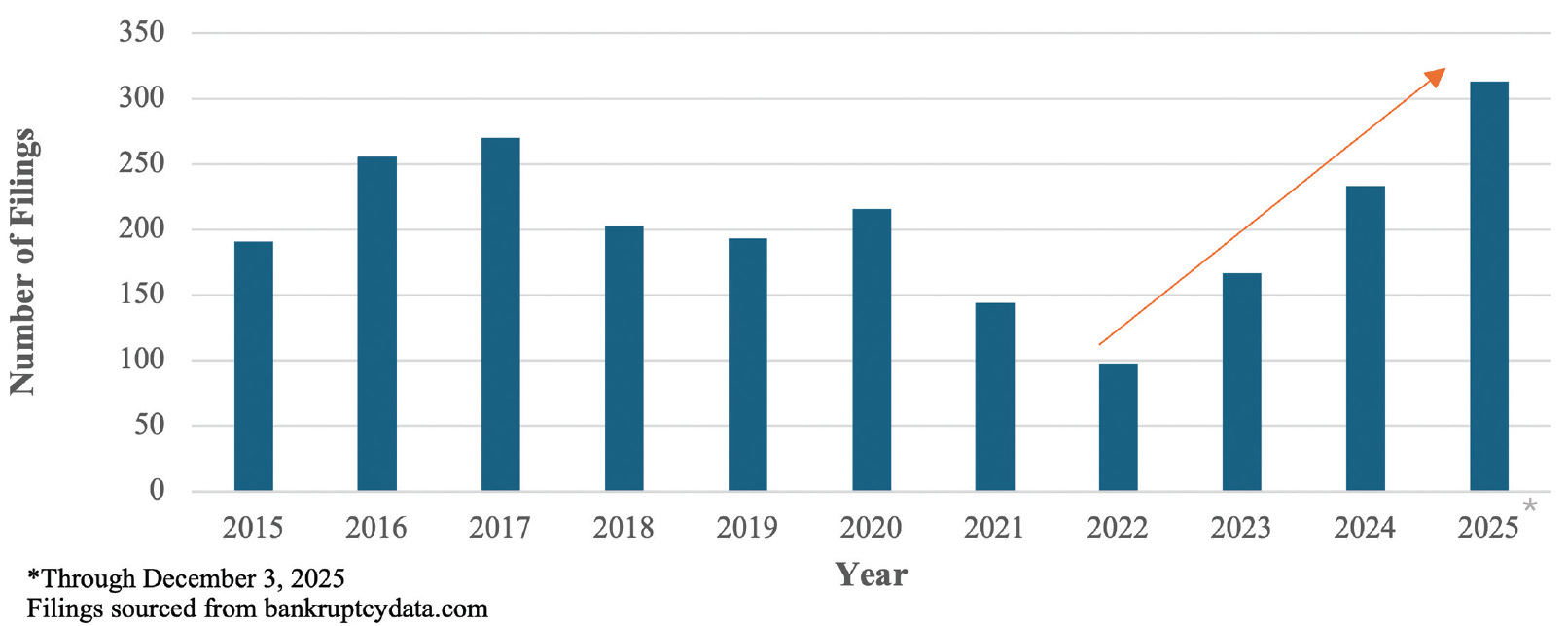

These challenges are reflected in Exhibit 1, which shows that automotive-related1 bankruptcy filings have increased since 2022. Further, the number of filings through early December 2025 have exceeded those of any other year over the last decade. These challenges hit across many subsectors within the automotive industry, with a few notable examples.

Exhibit 1: Bankruptcy Filings in the Automotive Industry (2015-25)

Challenges Facing the Industry

Parts Suppliers

Bohai Trimet, a German supplier of gearboxes and body parts for Volkswagen, filed for bankruptcy in April 2025.2 Volkswagen had reported a 15 percent drop in revenue in 2024 compared to the previous year, attributed to competitive pressures and rising supplier costs. The company has announced plans to lay off 35,000 employees by 2030 as part of its restructuring efforts.

In North America, Accuride, a leading vehicle wheel manufacturer producing 20 million wheels annually, filed for chapter 11 protection in October 2024. The company sought a consensual restructuring of its debt to continue operating as a going concern.3

Electric Vehicle Manufacturers

Fisker Inc. filed for chapter 11 protection on June 18, 2024, citing cash-flow problems that forced it to halt vehicle production and lay off staff. Fisker ultimately liquidated its operations, selling its remaining $46 million fleet to American Lease and transferring intellectual property to creditors.4

Lordstown Motors, an electric-vehicle (EV) manufacturer specializing in pickup trucks, filed for chapter 11 in June 2023 due to persistent cash-flow concerns that began in 2021.5

Battery-Makers

Northvolt, a Swedish battery manufacturer, filed for bankruptcy in March 2025 due to rising capital costs, geopolitical instability, supply chain disruptions, shifts in market demand, and concerns over production efficiency.6

Used-Car Retailers

Vroom, a used-car retailer and e-commerce company, discontinued its e-commerce vehicle sales and dealership operations in January 2024 as part of its restructuring plan.7 Vroom filed for chapter 11 in November 2024 and subsequently announced an equity-to-debt recapitalization plan, completing the recapitalization of its unsecured convertible senior notes in January 2025.8

U.S. Tariffs

U.S. tariffs are expected to put further financial strain on an already reeling industry. For example, Ford Motor Co. projected tariffs to cost $2 billion in 2025;9 General Motors (GM) forecasted tariffs to cost $4 billion to $5 billion annually;10 Volkswagen reported $1.5 billion in U.S. tariffs as of the second quarter of 2025;11 and Toyota projects $9.5 billion in U.S. tariff costs for fiscal year 2026.12

Responses to Challenges

The U.S. automotive industry has been operating in a challenging environment where additional tariffs are creating further uncertainties. The automotive supply chain is highly complex and competitive, with suppliers operating on thin margins. Further, suppliers typically work with fixed-fee contracts and cannot raise prices to cover tariff costs without an agreement from customers further up the supply chain.

Thus, the current environment is one in which many automotive companies have already faced multiple periods of financial strain, will be unlikely to absorb tariff costs with profits, and are contractually bound to fixed-fee contracts. As such, automotive companies will need to develop strategies to ensure their survival over the short and long term, which might include contract renegotiation, reorganization of supply chains, mergers and acquisitions, and divestitures.

Contract Negotiation

Many automotive suppliers and their legal counsel are already evaluating how existing contracts could be modified to absorb additional product costs that were not contemplated when the contracts were executed. Similarly, original equipment manufacturers (OEMs) likely understand that their supply chains will need to pass on some costs. For example, Stellantis has already publicly signaled that it is working on a plan to help eligible suppliers offset increased costs from tariffs.13 To be effective, suppliers will need to identify and justify price increases up the supply chain. Identifying and forecasting these increased costs for negotiation requires consideration of many different factors.

Identifying the exact costs of tariffs can be challenging for some suppliers, as cost-accounting systems use allocation methodologies to price material, labor and overhead costs to specific products. These systems often consider production forecasts to develop pools of costs to allocate and allocation bases (e.g., machine hours) to determine specific product costs.

Significant changes in materials used, volumes and throughput might lead to unexpected variances. For example, consider a supplier that is currently running three shifts and allocates all overhead costs among all shifts. If a large customer shuts down a plant and volume drops so that only two shifts are required, its overhead pricing based on spreading costs over three shifts will now be off.

When developing negotiation strategies, suppliers will be well served to understand how its product-cost analyses are prepared and any sensitivities to alternate scenarios. Further, due to the fluid and evolving nature of tariffs, flexible pricing models might offer advantages over fixed per part increases.

Supply Chain Adjustments

Many automotive manufacturers and suppliers are already re-evaluating their supply chains and where they are sourcing their products. Some OEMs have already announced plans to increase U.S.-manufactured products. GM announced plans to increase production of its light-duty trucks at its assembly plant in Fort Wayne, Ind.14 Honda announced plans to produce its next-generation Civic Hybrid in Indiana instead of Mexico.15 Hyundai announced plans for large investments of U.S. onshoring, including a steel plant in Louisiana.16 Stellantis has also announced plant closures in Canada and Mexico as a result of tariffs.17

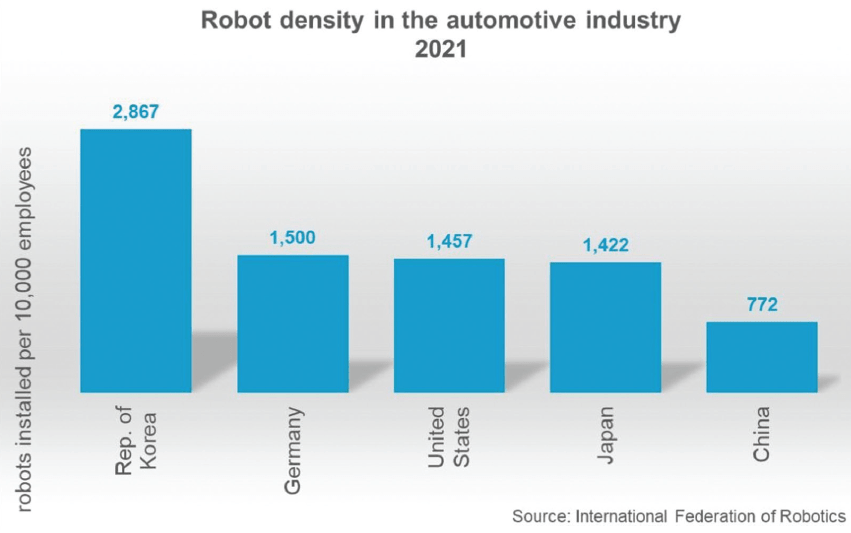

Automotive assembly and part plants are often massive billion-dollar facilities that cannot easily be relocated. Even smaller plants with less infrastructure investment needed will still require assembling and training a workforce, which makes relocating a challenge. Nevertheless, the ability to onshore parts production might be a new competitive advantage if the current tariff structure holds. To achieve this, U.S. automotive manufacturers might need to increase automation to compete with countries with lower labor costs, even with tariff protection. Exhibit 2 demonstrates that U.S. automotive robot density is higher than many other nations but still well below the global leader, South Korea.

Further, Tesla has been a leader in factory automation and robots for years.18 Even as an industry leader, Tesla still plans to increase its use of automation as part of a plan to reduce production costs by 50 percent in future vehicle models.19

In addition, smart manufacturing advancements in machine-learning and artificial intelligence are resulting in increased efficiency, production optimization, trackability, quick turnaround, decreased downtime and safer working conditions.20 As automotive manufacturers and their suppliers evaluate their supply chains, increased automation and smart manufacturing toward an onshoring strategy might offer competitive advantages.

Making investments in onshoring and factory automation is a long-term strategy that will involve careful capital budgeting to consider the investments needed and expected returns. Automotive manufacturers and their suppliers also will need to consider how they will finance these projects and any operating shortfalls as they continue to navigate through a challenging economic climate.

Exhibit 2: Robot Density in the Auto Industry

Mergers and Acquisitions

As consumer demand begins to rebound and financing costs decline, large-scale M&A in the automotive industry is expected to gain significant traction, particularly in battery and EV technologies.21 The industry is witnessing a wave of consolidation as companies seek to pool resources, mitigate risks and compete more effectively in the global market.

In an industry where technology is rapidly evolving, consolidation offers access to new technologies, expertise or intellectual property, which could help create advantages in product design and innovation. For example, in early 2025, American Axle & Manufacturing (AAM) entered into a definitive agreement to acquire Dowlais Group; ABC Technologies successfully completed its acquisition of TI Fluid Systems; and the merger between Schaeffler and Vitesco Technologies was completed in October 2024.22

Divestitures

Automotive companies and suppliers are also divesting assets and business lines as strategic tools for realigning their operations, reducing debt and restructuring their portfolios for long-term growth.23 Divestitures allow auto companies to shed noncore assets, focus on strategic priorities, and generate cash for innovation and growth. By simplifying their business structure, companies improve efficiency, reduce costs and better manage resources. As the auto industry evolves with such trends as electrification and sustainability, divestitures enable a quick pivot from outdated technologies in order to remain competitive in the market.

For example, Stellantis announced that it might divest some of its brands in 2026, marking a strategic pivot aimed at refining its focus. Similarly, Asbury Automotive Group, a major operator of auto dealerships, plans to utilize at least $250 million in divestitures to reduce its debt following its acquisition of Herb Chambers Cos.

Conclusion

Tariffs represent new challenges to an industry that has been navigating several obstacles and headwinds for the last half decade. These challenges could create, or increase, financial hardships to automotive companies. Contract renegotiation, reorganization of supply chains, mergers and acquisitions, and/or divestitures could offer solutions to some of these challenges and position automotive companies to continue as going concerns where they might otherwise be in doubt.

Reprinted with permission from the ABI Journal, Vol. XLV, No. 3, March 2026.

- This includes businesses engaged in automotive manufacturing, retail, parts distribution, rental/leasing, technology mobility, towing and repair.

- Colette Bennett, “German Auto Parts Maker Files for Bankruptcy,” TheStreet (April 25, 2025).

- Kirk O’Neil, “Another Iconic Auto Parts Brand Files for Chapter 11 Bankruptcy,” TheStreet (Oct. 10, 2024).

- Dietrich Knauth, “Fisker Bankruptcy Plan Approved After Deal on Vehicle Tech Support,” Reuters (Oct. 11, 2024).

- Michelle Toh, “Lordstown Motors Files for Bankruptcy and Sues Former Partner Foxconn,” CNN (June 27, 2023).

- “Northvolt Files for Bankruptcy in Sweden,” Northvolt (March 12, 2025).

- Kirk O’Neil, “Distressed Automobile Lender Files for Chapter 11 Bankruptcy,” TheStreet (Nov. 13, 2024).

- “Vroom Completes Recapitalization,” Vroom Press Release (Jan. 14, 2025).

- Breana Noble, “Ford Issues Tariff-Hit Guidance After Reporting Q2 Loss from Special Charges,” The Detroit News (July 30, 2025).

- Nora Eckert & Nathan Gomes, “Trump Tariffs Take $1 Billion Bite Out of GM Earnings, Shares Fall,” Reuters (July 22, 2025).

- Sam Meredith, “Volkswagen Cuts Guidance After Taking $1.5 Billion Hit from U.S. Tariffs in First Half,” CNBC (July 25, 2025).

- Daniel Leussink, “Toyota Warns of $9.5 Billion Tariff Hit, Slashes Annual Profit Forecast,” Reuters (Aug. 7, 2025).

- Robert S. Miller, “Stellantis May Step In to Help Suppliers Shoulder Tariff Costs,” Mopar Insiders (April 8, 2025).

- Kalea Hall, “GM to Increase Truck Production in Indiana Following Trump’s Tariffs,” Reuters (April 3, 2025).

- Maki Shiraki, “Honda to Produce Next Civic in Indiana, Not Mexico, Due to U.S. Tariffs, Sources Say,” Reuters (March 3, 2025).

- Seema Mody, “South Korea’s Hyundai Announces $21 Billion U.S. Investment,” CNBC (March 24, 2025).

- Chris Isidore, “Tariff-Related Layoffs Hit Five U.S. Auto Plants that Supply Factories in Canada and Mexico,” CNN (April 3, 2025).

- Steve Greenfield, “Rising Labor Costs Propel Automakers Toward Robotics and Automation,” CBT News (Jan. 19, 2024).

- Id.

- “How Automation Is Driving the Future of Automotive Manufacturing,” USC Consulting Grp. (Feb. 22, 2024).

- “Automotive: U.S. Deals 2025 Midyear Outlook,” pwc.

- Dhruva Gogoi, “Auto Supply Chain: Merge or Miss Out?,” S&P Global (April 24, 2025).

- “Automotive: U.S. Deals 2025 Midyear Outlook,” pwc.