English

English

With over 23 million small businesses in America1 and a significant portion of their owners nearing the retirement age over the next two decades, succession planning is an ever-pressing issue that often times gets overlooked. For example, a survey performed in 2012 by the AICPA found that 54% of multiowner firms did not have a written, approved succession plan in place, yet 79% of business owners expected succession planning to be a significant issue in the next 10 years.2 While there is no set timeframe on when a business owner should begin the succession planning process, a rule of thumb is that he or she should start at least five years prior to his or her anticipated exit from the business. Therefore, it is imperative that business owners start early towards planning for this goal. This article is not meant to serve as a comprehensive guide, but rather is designed to serve as a structural aid for business owners when starting the succession planning process.

Don’t Let Life Do the Planning for You

A succession plan provides a roadmap to achieve a successful exit. Doing so forces the owner to focus on the execution of the overall strategic plan of the business and to implement value creation strategies to enhance the value of the business over the owner’s remaining time with the company. A well-thought out and executed succession plan not only makes sense from a financial point of view, but also gives the owner greater control over how and when that exit occurs. Further, a successful succession plan allows for greater multi-generational wealth creation, provides for greater options that align to the owner’s long-term goals for the business (e.g., keeping the company a family-owned business), and reduces stress and uncertainty among family members and employees. In the words of Stephen Covey, “Begin with the End in Mind.”3

The individual parts of the planning process should not be viewed in a vacuum but rather as components of a more global strategic plan. The areas of planning that have to be dealt with are reflected in the below graphic form.

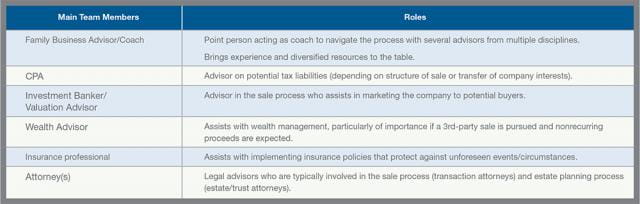

Getting the succession planning process started takes planning and organization on the part of the business owner and his or her team. The table on the next page outlines the four steps necessary to achieve the best results regardless of the mode of exit. The steps include: 1) assembling a team, 2) creating a baseline value, 3) determining the necessary future value, and 4) creating a plan to bridge the gap between the two values.

Assembling the team is a very important step. Experts in the areas previously highlighted should be thought of as members of a team and should meet on a regular basis with the business owner to work towards the business owner’s success. The team members and their prospective roles are presented in the above table.

No business owner wants this many primary professionals at one time; however, some are essential as part of the primary team and others will fill specific roles when and if their expertise becomes necessary. Most owners have one person that they trust to have their best interests at heart. This could be an employee, colleague, business associate, or one of the team members described above. That person should be the team leader. Some mix of other professionals can be added based on their relationship to the owner and the team leader.

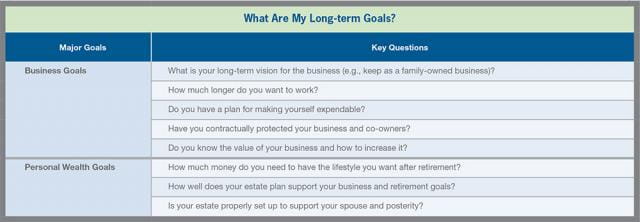

The first step to succession planning requires that the business owner take an introspective look at his or her business and personal goals to determine which exit opportunity to pursue. The following tables highlights some key questions that the business owner should consider when thinking about long-term goals and priorities that will then drive the direction of the succession plan. We will all leave our business, either feet first or on our own terms.

Depending on the answers to the questions listed above, which only lists but a small sample of general questions that should be considered, the business owner generally has three exit options available: 1) sell to a third party (either a strategic or a financial buyer); 2) sell to an employee(s); or 3) transfer interests to family members. Regardless of the method of exit, the business should be in a condition which will promote the most favorable valuation. Therefore, a current valuation and an understanding of what drives value is important as a starting point.

Understanding the Value of the Business

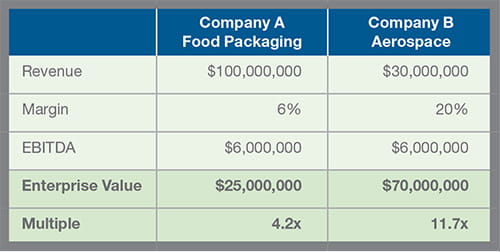

The business owner should have a general idea of what the business is worth. It is hard to know where you want to go if you don’t know where you are now. Importantly in this process, the business owner should understand what value drivers to focus on to maximize his or her potential value. Many times the factors that drive value are not based solely on the size of the company or its revenues (although this certainly has an impact on valuation). For instance, the following is a very basic example of two companies generating the same level of profits but with very different profit margins.

For most operating companies, value is often determined by looking at the Enterprise Value (“EV”) of the company, calculated as EV = (EBITDA x Multiple). Subtracting debt and adding cash result in the Equity Value of the company. Earnings, before interest, taxes, depreciation, and amortization (“EBITDA”) is often times a “quantitative” measure of a firm’s profitability and is often viewed as a proxy for a firm’s operating cash flow. The valuation multiple is a qualitative input that takes into consideration many factors of a company and is derived from comparable companies.

In our example, Company A and Company B have the same level of operating Cash Flow, but Company A generates significantly higher revenues of $100 million compared to Company B’s revenue of $30 million. However, its stronger profit margin, the industry that the company operates in, the use of trademarks, the amount of operating leverage that exists in the business, potential growth factors, and the use of any patented technology unavailable to other competitors are just some reasons why Company B would trade at a significantly higher valuation multiple than Company A. Other value drivers can include the degree to which the company has proprietary products, industry leading technology, above average profit margins, a strong management team, a diversified but resilient customer base, and long-term contracts in place. These value factors are uncovered during the due diligence process and play a role in determining the ultimate value of the company.

In summary, the valuation of a company is more complex than merely looking at top line revenues or operating profit. The table below provides hypothetical (but highly plausible) examples of indicated offer prices and the implied valuation multiple for the two companies. This is an example of how the summary financials previously presented cannot definitively indicate valuation without knowing the various value drivers of the business and their impact on the valuation multiple.

To enhance the value of your company, start thinking about the various characteristics that exemplify high quality businesses. What is the quality and depth of the management team? Does the firm have substantial “Key person risk” in the business owner, and is the knowledge of the company’s procedures, management style, and decision making process “institutionalized”? The ultimate goal is that dependence is reduced on the business owner with the business being self-sufficient and successful.

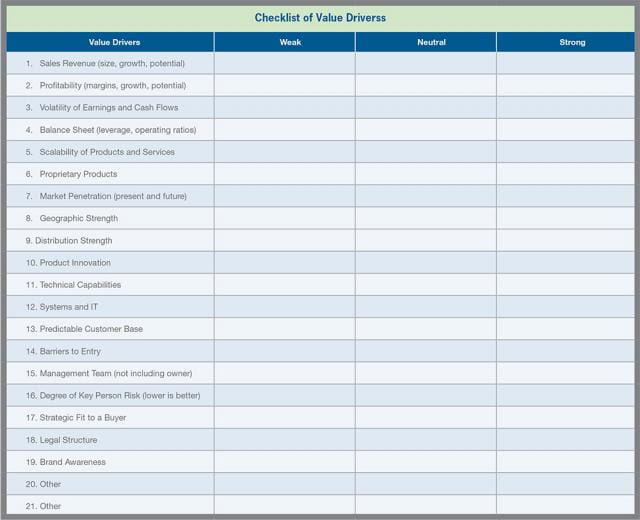

When looking at the business operations, the business owner should identify where the business stands within its local or national market and what potential growth there is for the business. Would expansion require additional staffing and resources that are beyond the resources of the existing business or can the “low-hanging fruits” be harvested to generate additional value? If the company has a strong management team, excess manufacturing capacity, a built-out information systems, etc. to layer on additional products and services, growing the business only requires marginal effort and costs (i.e., operating leverage). Furthermore, increased product offerings can offer greater cross-selling opportunities with the acquirer’s firm. However, the business owner must be mindful of the timeframe needed to achieve such goals relative to his or her expected exit year if pursuing such a strategy. Therefore, it is even more important that the business owner have an “institutionalized” road map to achieve such goals, particularly if an unexpected event occurs prior to the anticipated exit date. To assist in measuring what areas to improve upon for the business, use the table at the end of this article to help in identifying the strengths and weaknesses of the company’s value drivers.

Selling the Business to Employees

Rather than sell to a third party, a second option is to sell the business to existing employees. When considering this option, one critical decision is whether to structure the sale as an upfront transaction or over an extended period of time, and if the latter is chosen, to what degree or role the business owner will play during the transitional period. Importantly, one of the key determinants in what path is chosen is how the transaction will ultimately be funded. Often times, employees will lack the necessary upfront capital to purchase the entirety of the company from the business owner. Options for funding the transaction can include establishing an employee stock option plan (“ESOP”), recapitalizing the business (with debt or by issuing different classes of equity), issuing seller notes or other forms of deferred compensation. The business owner must also consider the tradeoff that exists between maximizing his or her sale proceeds as it is more likely that the sale to a third-party strategic or financial buyer will result in a higher offer price given synergies, cost reductions, or leverage that the two types of buyers may utilize. As is the case when selling the business to employees or to family members, the main deciding factor typically falls on the business owner’s long-term vision for the company (e.g., retaining the company’s name, culture, etc.).

Transfer the Business to Family Members

The third option includes transferring the business to family members. If selecting this option, the business owner should start developing his successor(s) (if this has not happened already). To ensure a successful transition under this option, the business owners and the advisors should understand the family dynamics in play and consider any tension that exists between active and passive family owners. The business owner may have to weigh equalizing his estate planning options around what types of assets to transfer to his heirs and how best to do so without antagonizing or appearing biased. It is also important to consider any tension between family owners and non-family executives and what role they will play once the business is fully transitioned to the next generation. To mitigate any issues that may arise concerning family members wishing to liquidate their interests or acquiring shares from other family members, be sure to have a well-defined, but flexible buy-sell agreement in place. Proper succession planning should also consider the use of revocable or irrevocable trusts, generation skipping trusts (“GSTs”), grantor retained annuity trusts (“GRATs”), or other legal structures to minimize tax liabilities during the wealth transfer process. The business owner should work closely with an estate and trust attorney to plan accordingly based on the objectives and timeframe of the owner.

Conclusion

Regardless of what option the business owner selects, it is imperative that the business owner begin creating a roadmap to ensure a smooth and successful succession plan. To achieve an effective succession plan, the business owner should gather a trusted team of financial and legal professionals as early in the process as possible. It is critical that the business owner ensures that all professionals associated with the succession planning process are on the same page and planning with the same goal in mind.

Remember, it is never too early to start planning. Start working on your business, not in your business!