中文

中文

RESETTING EXPECTATIONS HIGHER

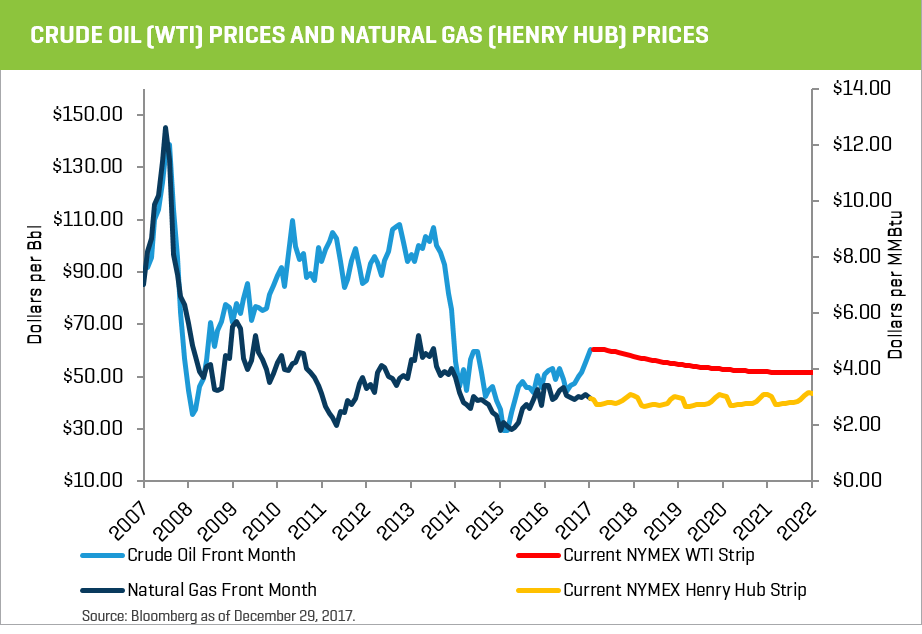

A combination of industry-specific factors propelled energy market performance in the fourth quarter of 2017. Crude oil prices increased from $51.67 to $60.42 during the quarter (a 17% increase) driven by continued crude inventory draws, stronger-than-expected global crude oil demand, and sustained OPEC production cuts.

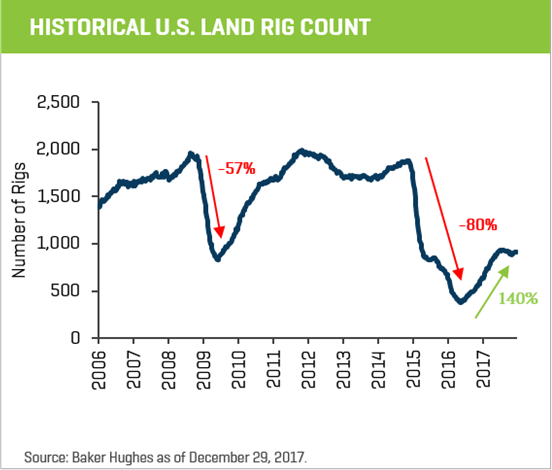

Despite the meaningful increase in crude oil prices, the average U.S. land rig count moderated during the quarter, declining approximately 3% from 927 to 902 rigs.

Many E&P companies remain cautiously optimistic regarding future crude oil prices, but they have not committed additional capital at this time. Producers have hedged a substantial portion of 2018 crude oil production at prices less than $60 per barrel. However, E&P companies have also retained unhedged crude production and will benefit as crude prices rise through improved cash flows and from a natural hedge against service cost inflation. Even if the land rig count remains stable to flat, more robust completion activity (longer laterals, more fracking stages, and increased proppant usage) may push service costs higher on a year-over-year basis.

Recent Capital Markets Trends

MARKED FINANCIAL IMPROVEMENT

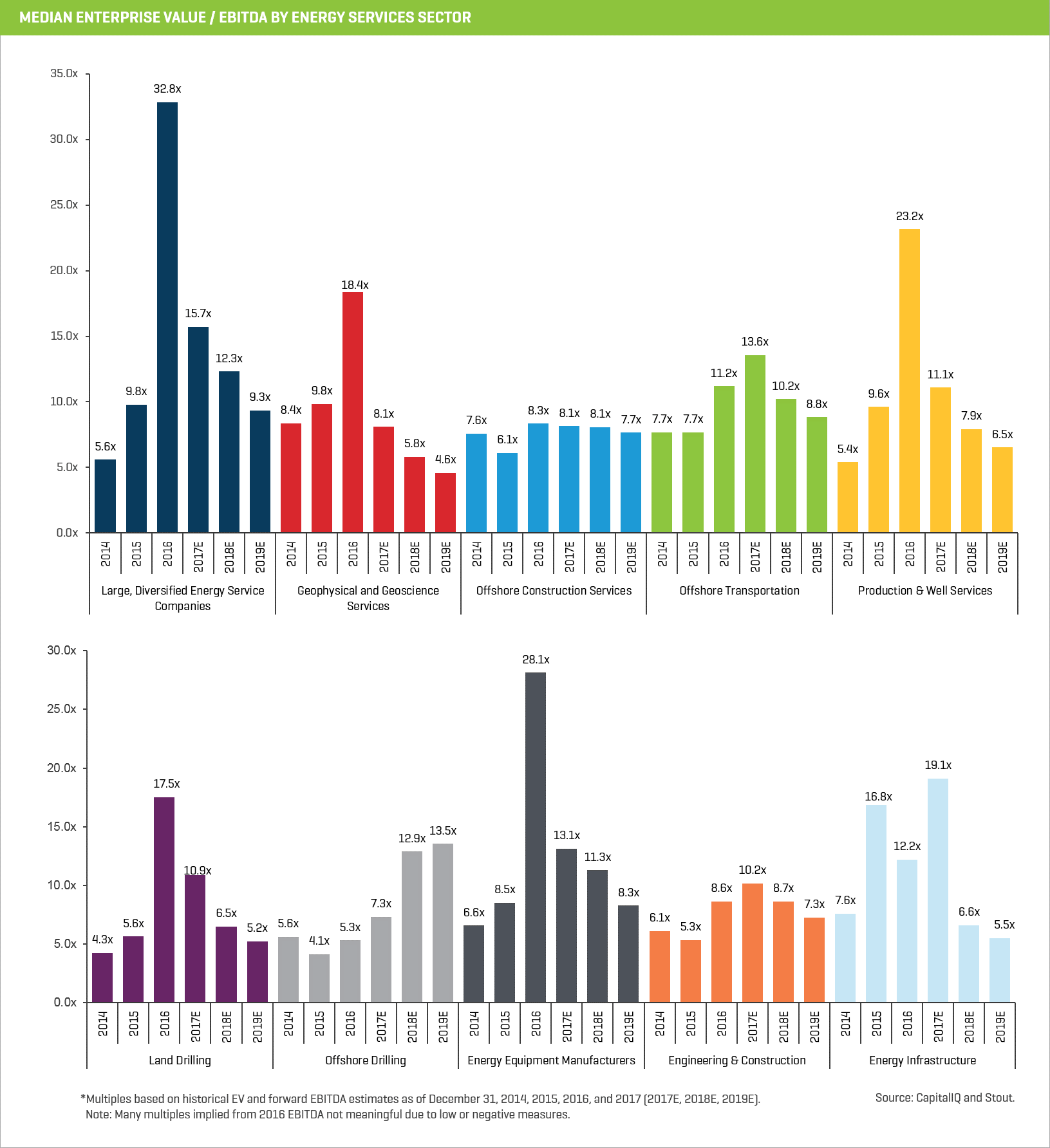

Financial performance in the third quarter of 2017 generally continued to improve in the energy service and equipment segment. For production and well service companies, third-quarter revenue increased, on average, by 20% compared with the prior quarter, and by 72% year over year. Third-quarter EBITDA margins increased to 12%, up from 8% in the second quarter and from negative 0.3% in the third quarter of 2016. While the growth may have stabilized from earlier quarters in 2017, it marked the highest quarterly EBITDA margins in this segment since the first quarter of 2015. Pressure pumping and other completion-related businesses continued to witness some of the best financial improvement. However, the potential for capacity additions in these areas will likely act as a throttle to pricing. Certain equipment manufacturers focused on onshore completion activity have also seen marked improvement in financial performance as service companies upgrade and refurbish their equipment. Offshore service businesses remain the most challenged as utilization and pricing continue to be depressed.

VALUATION LEVELS RISING BUT STILL LAGGING BROADER MARKET

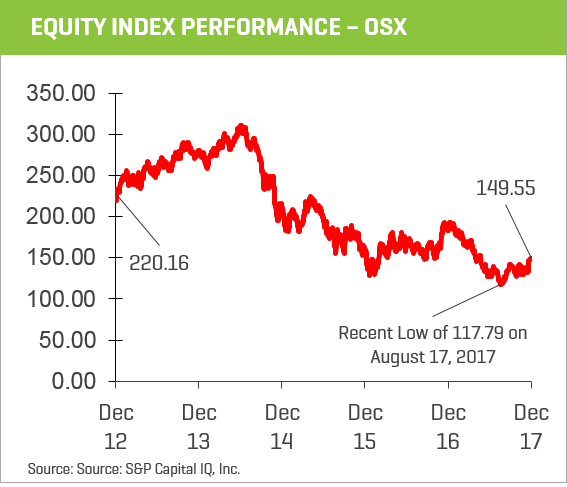

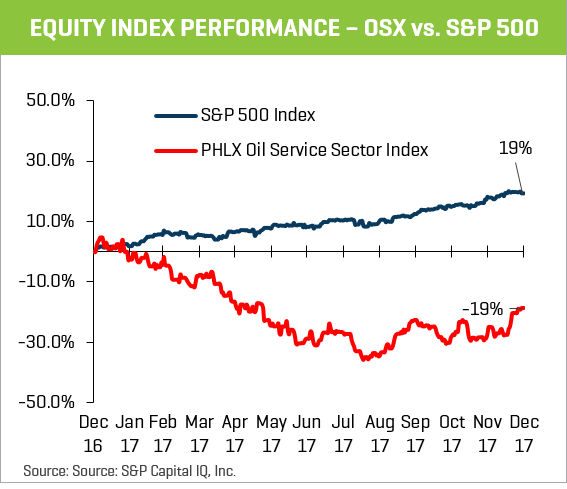

Public valuations for many energy service companies witnessed improvement in the fourth quarter, with the Philadelphia Oil Service Sector Index (OSX) increasing 5% during the quarter and 27% from its recent August 2017 low, though full-year performance was down by 19%. The S&P 500 Index increased 6% during the quarter and 19% during the full year, with the former performance likely reflecting the passage of recent U.S. tax legislation and the expectation of continued global economic expansion.

The relative energy underperformance may indicate lingering concerns regarding production growth in the industry, particularly with rapidly rising crude oil prices encouraging more activity. Despite WTI crude prices reaching $60.42 at quarter-end, the forward curve remained in deep backwardation (average 2018 and 2019 WTI prices were $59.40 and $55.94, respectively). Production growth, balance sheet conservatism (E&P companies living within their cash flows), service cost inflation, and global crude demand will all factor in energy and energy service company valuations.

(click to view larger chart)

Recent M&A Trends

M&A ACTIVITY REMAINS STABLE

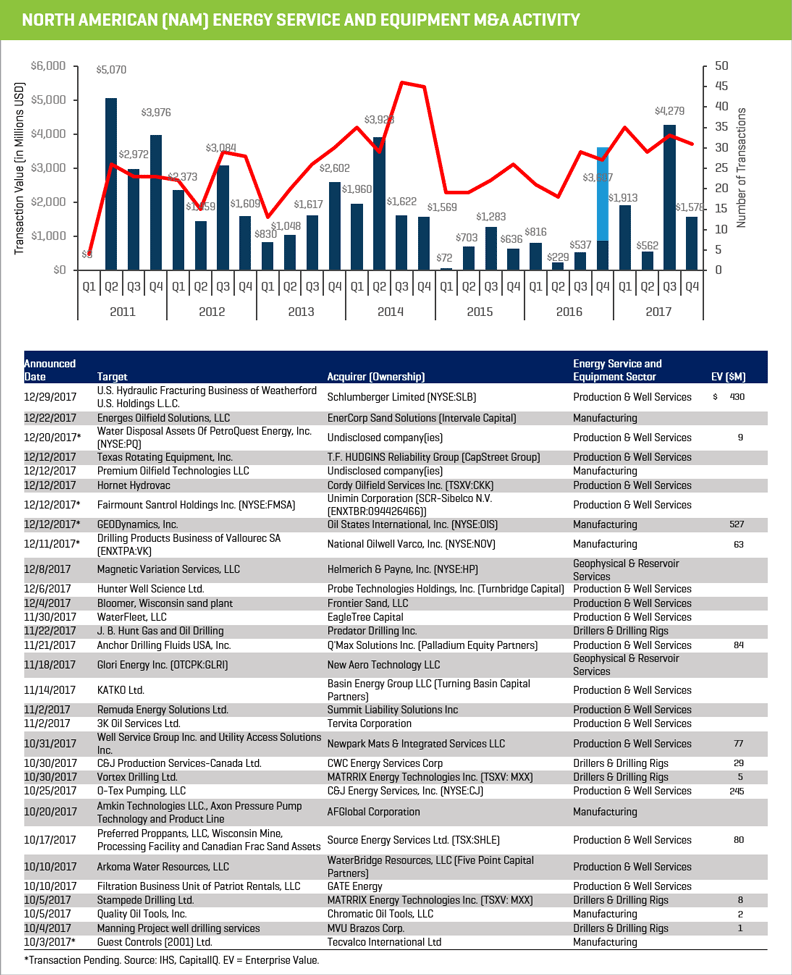

Energy service and equipment M&A activity remained relatively stable (by count) in the fourth quarter compared with prior-quarter levels, while dollar volumes fell (due to several larger transactions). Overall 2017 activity totaled 128 transactions, a 35% increase compared with 2016 activity while transaction value reached $8.3 billion versus $5.2 billion in 2016 (a 60% increase).

(click to view larger chart)

LOOKING AHEAD IN 2018

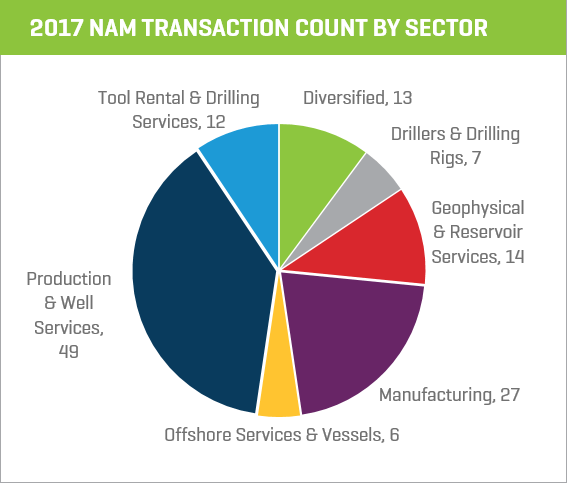

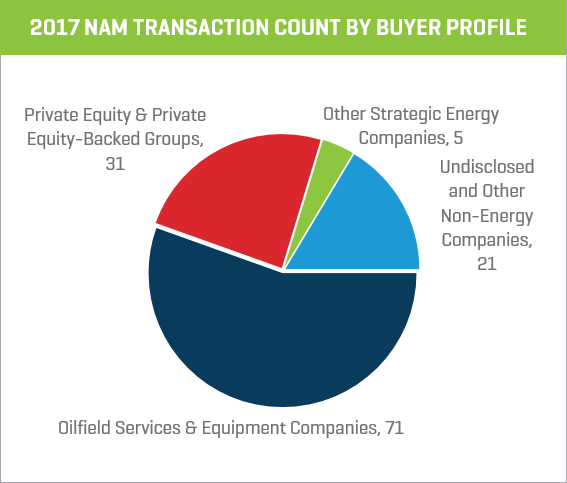

The outlook for 2018 M&A activity in the sector is positive as i) many companies require growth capital, ii) private owners are looking to derisk after weathering the downturn, and iii) better financial performance makes traditional valuation metrics relevant again. Production and well services transactions have remained the most active OFS sector in NAM by transaction count and dollar value. Energy equipment manufacturing also remains very active by number of transactions. Drilling and offshore services and vessels have continued to represent the weakest sectors (by transaction count). Strategic acquirers were the most active amongst energy service and equipment businesses during 2017 (55% of all transactions) with private equity (PE) and PE-backed groups, the second-most-active buyer segment (24% of total deals) accelerating their acquisitions during the second half of the year.