Deutsch

Deutsch

An addiction epidemic has increasingly become a priority of concern over the past decade, as more awareness focuses on people’s mental health, the increased use of prescription drugs, and the decriminalization of select drugs. Addiction treatment centers (“ATCs”) have experienced significant volume expansion due to such factors. With increasing recognition and decreasing stigma each passing year, ATCs are claiming a prominent role within the behavioral health sector. In this outlook, we discuss the key drivers affecting these centers, trends in the sector, the leaders in the behavioral health space, and the outlook for investment in the sector.

Background

ATCs can pursue various modes of operations or focus on specific patient populations, and such characteristics may vary from facility to facility. Such factors include:

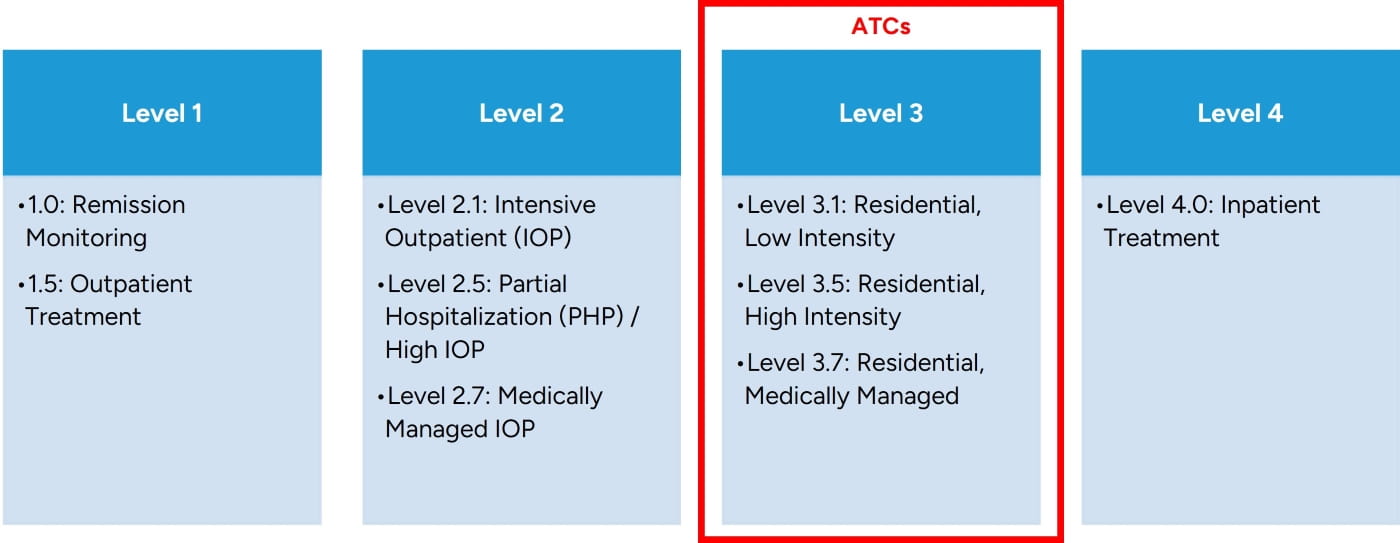

- Levels of Acuity Treatment: American Society for Addiction Medicine (ASAM) Levels of Care provide a formal framework for outlining what substance use disorder (SUD) services are provided to patients at an ATC.

Figure 1: ASAM Levels of Care

Patients can receive services on an outpatient, residential, or inpatient basis depending on the acuity of their needs. Many ATCs may find that they are able to expand their services by introducing either partial hospitalization programs (PHPs) or intensive outpatient programs (IOPs), such as care at Level 2, which can provide attractive rates of return without intensive capital commitment.

- Payor Base: Some ATCs focus on a particular payor base, such as primarily Medicaid, while others may elect to accept only cash pay from patients. Although less common, certain ATCs may also operate under out-of-network models with commercial payors.

- Network: While a single, standalone ATC may be able to offer only a few levels of care, larger networks of ATCs may provide a continuum across substantially all levels of care, which afford it a pipeline of patients as they gradually progress through treatment.

Key Regulations and Developments

Behavioral health providers have broadly looked to regulations and government policy to improve the business economics of ATCs and ensure access to patients needing such care. Much of the recent announcements and developments serve to bolster legislation from decades ago.

The Mental Health Parity and Addiction Equity Act of 2008 (MHPAEA) allowed behavioral health facilities to expand access to care due to increased protections offered to patients. The MHPAEA built upon the Mental Health Parity Act of 1996 (MHPA), whereby large group plans could not impose annual or lifetime dollar limits on mental health benefits that are any less favorable than any such limits imposed on medical or surgical benefits.1 Specifically, the MHPAEA further bolstered the protections of MHPA by:

- Ensuring the financial requirements (deductible and copays) and treatment limitations (days of coverage or number of visits) that apply to mental health/substance use disorder (MH/SUD) benefits must be no more restrictive than predominant financial requirements or treatment limitations that apply to medical and surgical benefits;

- Requiring that MH/SUD benefits may not be subject to any separate cost sharing requirements or treatment limitations that only apply to such benefits;

- Providing out of network MH/SUD benefits if out of network benefits are also available for medical and surgical care; and

- Requiring disclosure of processes for medical necessity determination and reasons for denial of any benefits tied to MH/SUD benefits.

Taken together, the MHPAEA attempts to alleviate gaps in behavioral care access by mandating equivalent coverage and benefits with those of traditional medical care. With these protections, more patients are likely to receive coverage under their insurance plans, expanding the potential client base for facilities offering behavioral health services. President Biden’s administration took efforts to increase and improve the mental health parity requirements to help the 150+ million Americans with insurance by mandating the following:2

- Inadequate Access Evaluation: Health plans are required to evaluate the outcomes of their coverage rules to make sure people have equivalent access to both mental health and medical benefits. Analyses like this will show where plans are lacking appropriate access and force plans to improve access by including more mental health professionals in their networks and reducing red tape to receive care.

- Limit Barriers to Accessing Care: Under the rule, health plans must equally apply medical management techniques and manage similar breadth of networks between MH/SUD and medical/surgical benefits. Additionally, plans must use similar considerations in setting out of network payment rates for mental health and substance use disorder providers as they do for medical providers.

- Expanded Scope of Enforcement: MHPAEA did not require non-federal governmental health plans to comply with its requirements. Closing this loophole adds additional insurance beneficiaries to those protected under MHPAEA.

However, under President Trump’s second term in 2025, many of the expected impacts to MPHAEA have been reduced or scaled back, as indicated by a May 2025 pause pending litigation.3 Nonetheless, President Trump has also indicated that mental health will continue to be a priority (particularly for children) for the foreseeable future, as stated in a February 2025 executive order.4

On balance, the regulatory outlook for mental health is uncertain. The Department of Health and Human Services also announced plans in March 2025 to combine several offices together, including the Substance Abuse and Mental Health Services Administration (SAMHSA),5 likely to result in thousands of layoffs for SAMHSA staff.

Broadly, the federal government has since taken action to reduce expenditures related to mental health and substance use treatment, including a $1 billion reduction to the budget for SAMHSA,6 the elimination of federally-funded grants for school-based mental health provider networks,7 and reductions in research for mental health and substance use at the National Institutes of Health.8

Demand for Behavioral Health and Addiction Treatment Services

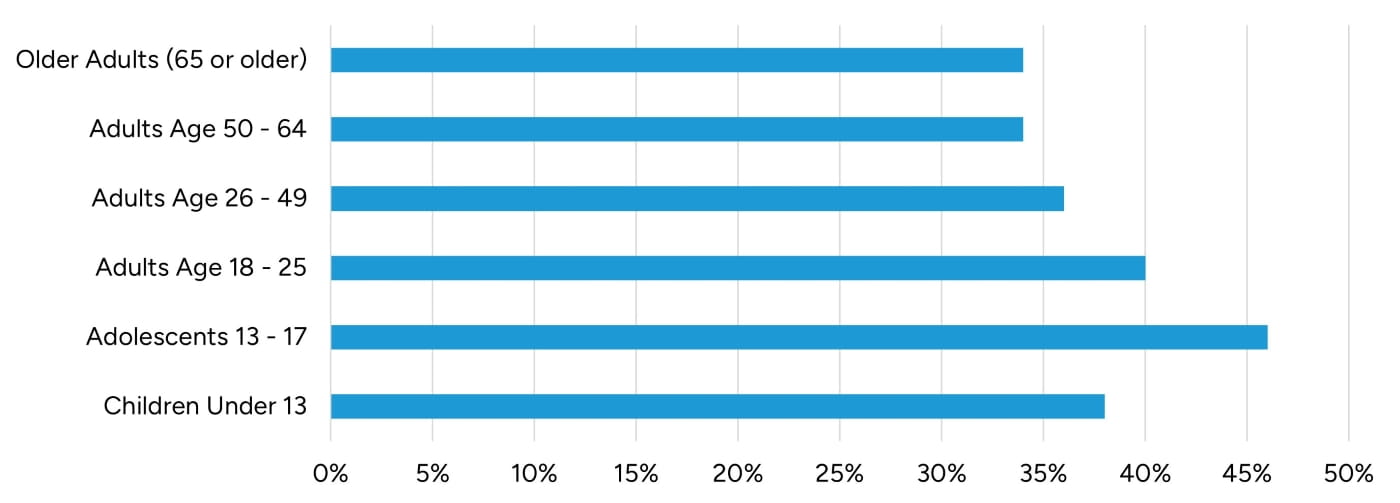

The COVID-19 pandemic had a lasting effect on the population and a negative impact on behavioral health as a result of unexpected deaths, isolation from others, and fear from the unknown. Accordingly, there has been a rapid increase in demand for behavioral health services since 2020. From American Psychological Association’s 2022 COVID-19 Practitioner Impact Survey, 79 percent of psychologists reported seeing patient volume increases in anxiety disorders, while 64 percent saw increases in trauma-related and stressor-related disorders.9 Furthermore, younger generations have been responsible for the largest increase in behavioral service demand with adolescents (ages 13 through 17) leading the way followed by those ages 18 through 25. As a result, behavioral health services are in high demand now and are expected to continue to be in high demand for the coming years.

Figure 2: American Psychological Association's 2022 COVID-19 Practitioner Impact Survey: Changes in Patient Demographics

Behavioral health facilities have always achieved high bed utilization efforts due to the demand for their services. According to SAMHSA’s 2020 National Mental Health Services survey, facilities were utilizing 90 percent of designated hospital inpatient beds and 93 percent of designated residential beds. There were 85,948 beds designated for inpatient treatment and 46,828 beds for residential treatment.10 In 2018, 109,241 beds were assigned for inpatient treatment and 62,253 beds were designated for residential treatment, representing broad declines of over 20 percent. The bed count decline is correlated with the lack of available providers and/or nurse staffing. However, by trimming bed counts, fixed overhead expenses are allocated to fewer beds, causing financial pressures for such operators. To combat this decline in bed counts, many certificate of need (CON) states are reforming such regulations for the behavioral health facilities in their states. For example, in North Carolina, House Bill 76 (2023) removed psychiatric hospitals and “chemical dependency treatment facilities” from needing CON approval to increase the number of beds.

Ever higher demand for behavioral services counterplays a dearth of providers. According to a survey from the Kaiser Family Foundation (KFF), the United States only meets 26.4 percent of the need for mental health care professionals.11 An additional 6,200 practitioners are needed to meet the current mental health demand. According to National Alliance on Mental Illness (NAMI), there are three general groupings of mental health professionals: assessment and therapy; prescribe and monitor; and “all-other.” The assessment and therapy group are composed of psychologists, counselors, and therapists, who offer guidance and assess patients for mental health conditions. Professionals in the prescribe and monitor group are psychiatrists and psychiatric/mental health nurse practitioners. These professionals can offer the same services as the first group, but also prescribe medication, which is typically a key component of addiction treatment. Primary care physicians sometimes work in tandem with mental health professionals to determine an individual’s best treatment plan according to NAMI. In all other categories, social workers and pastoral counselors can offer support and help in non-medical ways (e.g., by helping a person set goals).

Along with the lack of current practitioners, most practitioners cannot handle additional patients beyond their current workload. Sixty percent of psychologists reported having no openings for new patients according to the same American Psychological Association survey previously referenced.

Industry Trends

Medicaid Redetermination

At the start of the COVID-19 pandemic, Congress authorized the Families First Coronavirus Response Act (FFCRA). The FFCRA included a requirement that state Medicaid programs keep people continuously enrolled through the end of the COVID-19 public health emergency, temporarily suspending recertification requirements. Continuous enrollment ended on March 31, 2023, and states started to unwind coverage the following month. KFF’s current estimates indicate that approximately 17 million individuals have been disenrolled through August 2025, by which time most states had completed disenrollment.12 Redeterminations impact behavioral health facilities (including ATCs), as Medicaid is the largest payor of behavioral health services in the United States.13 In some cases, though, ATCs had pro-actively limited Medicaid patients in favor of higher-reimbursing commercial payors.

Medicaid Spending and Regulatory Uncertainty14

On May 14, the House Energy and Commerce Committee, which oversees the Medicaid program, passed a reconciliation bill out of committee that released preliminary estimates showing the proposal would reduce federal Medicaid spending by $625 billion. There are three policy changes that account for the vast majority of cuts: requiring states to implement work requirements for the expansion group, increasing barriers to enrolling in and renewing Medicaid coverage, and limiting the state’s ability to raise the state share of Medicaid revenues through provider taxes. The $625 billion cut will force states to choose between maintaining current spending by raising taxes, reducing spending on other programs, or cutting Medicaid spending by covering fewer people, offering fewer benefits, or paying providers less.

The Congressional Budget Office estimates the bill would decrease Medicaid enrollment by 10.3 million people in 2034, suggesting most of the savings will come from reduced enrollment. The effects of the cuts will vary year by year and grow over time. For example, the work provision accounts for over $300 billion in savings but will not take effect until 2029. Congressional Budget Office estimates that, in aggregate, states would replace roughly half of the federal funds with their own funds. Although no cuts to Medicaid are solidified as of this writing, the political landscape has shifted to some sort of cuts, which is likely to decrease Medicaid beneficiaries’ access to ATCs.

Reimbursement Rates

Reimbursement trends for addiction treatment facilities had benefited from recent tailwinds, which were observable from public company operators. However, such reimbursement trends currently range from nominal growth to moderately elevated levels. During Acadia’s third quarter 2025 earnings call, CFO Todd Young stated:

Same-facility revenue grew 3.7% year-over-year, driven by a 2.3% increase in revenue per patient day and a 1.3% growth in patient days…

CEO Chris Hunter elaborated:

Stepping back, we recognize that our operating environment has faced increasing headwinds as we moved through 2025, particularly with regard to pressures on managed care companies and increased uncertainty on Medicaid funding at the state level.15

Universal Health Services’ outlook on rates is more positive, as the limited supply is met with burgeoning demand, allowing for outsized rate increases. During Universal Health Services’ third quarter earnings call, Steve Filton, CFO, stated:

Turning to our behavioral health results. During the third quarter of 2025, same-facility net revenues increased 9.3% on a reported basis… Same-facility revenue growth was driven by a 7.9% increase in revenue per adjusted patient day as compared to the prior year.

Same-facility adjusted patient days increased 1.3% as compared to the prior period's third quarter with volume growth modestly improving as compared to 1.2% in the second quarter and 0.4% during the first half of 2025. We expect further volume improvements during the fourth quarter, although we now believe a reasonable expectation for same facility adjusted patient day growth should be in the 2% to 3% range with our near-term expectations at the lower end of this range.16

In prior quarters, Universal Health Services was terminating contracts with their lowest payors who did not sufficiently increase their rates. Acadia and Universal Health can leverage the current behavioral health environment where each company can only treat a limited number of patients. This ability to be selective in their patient and payor base should lead to increased profitability for both public companies, as well as private operators of ATCs given the ongoing expanded demand for constrained SUD treatment services. However, Medicaid remains a wild card in the current political environment, in terms of both reimbursement and volume of patients.

Labor Bottlenecks

According to KFF, 158 million Americans live in a mental health workforce shortage area,17 representing a systemic constraint that hampers the ability of ATCs to effectively recruit and retain sufficient professional providers. The workforce shortage is slowly recovering with high, but slowing, wage inflation. During Universal Health Services’ fourth quarter 2024 earnings call, Steve Filton disclosed that the company had issues filling positions on the behavioral health side, curtailing volume growth to some degree. More recently, though, the company has observed continued improvement in premium pay over the past year and has seen continued gradual improvement. As labor supply continues to improve in the behavioral health space, companies should see increased volumes, growth, and profitability.

Opioid Settlement Payments – First Wave

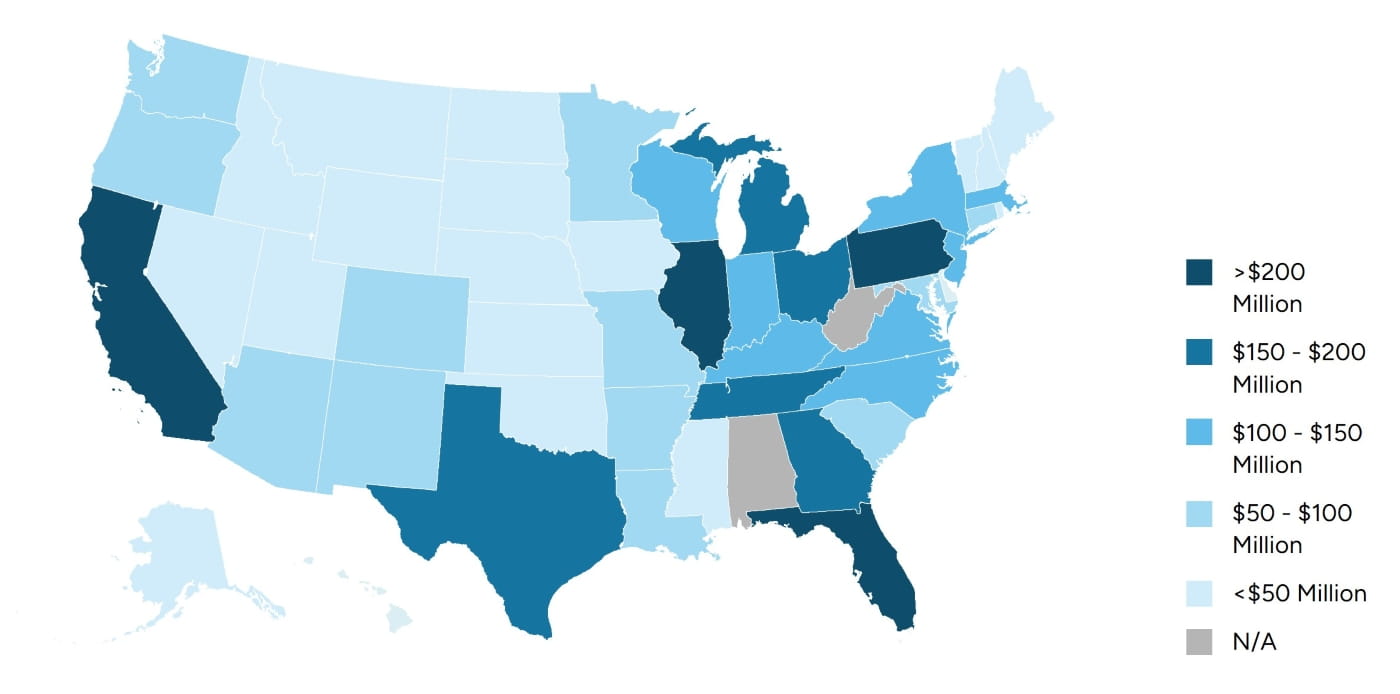

In recent years, COVID-19 was not the only epidemic affecting the U.S.; the opioid addiction crisis has similarly impacted millions of Americans. In July 2021, a consortium of companies, including Johnson and Johnson, McKesson, AmerisourceBergen and Cardinal Health, made a $26 billion offer to the states to resolve their liabilities in 3,000 opioid crisis-related lawsuits. Johnson and Johnson will pay $5 billion, and the remaining “big three” pharmaceutical distributors will pay $7 billion each. Forty-eight states agreed to participate in this settlement and drop their own litigation attempts. However, there are stipulations to the payments, as the settlement is set as a base payment plus incentive payment. The states had to convince individual cities and counties to drop their suits as well to receive the incentive payments. Ninety percent of eligible counties surrendered their suits, which nearly doubled the base payment. States started to receive the payments in September 2022. Figure 3 itemizes the total amount paid to each state as of March 4, 2024.18

Figure 3: Settlement Payments by State

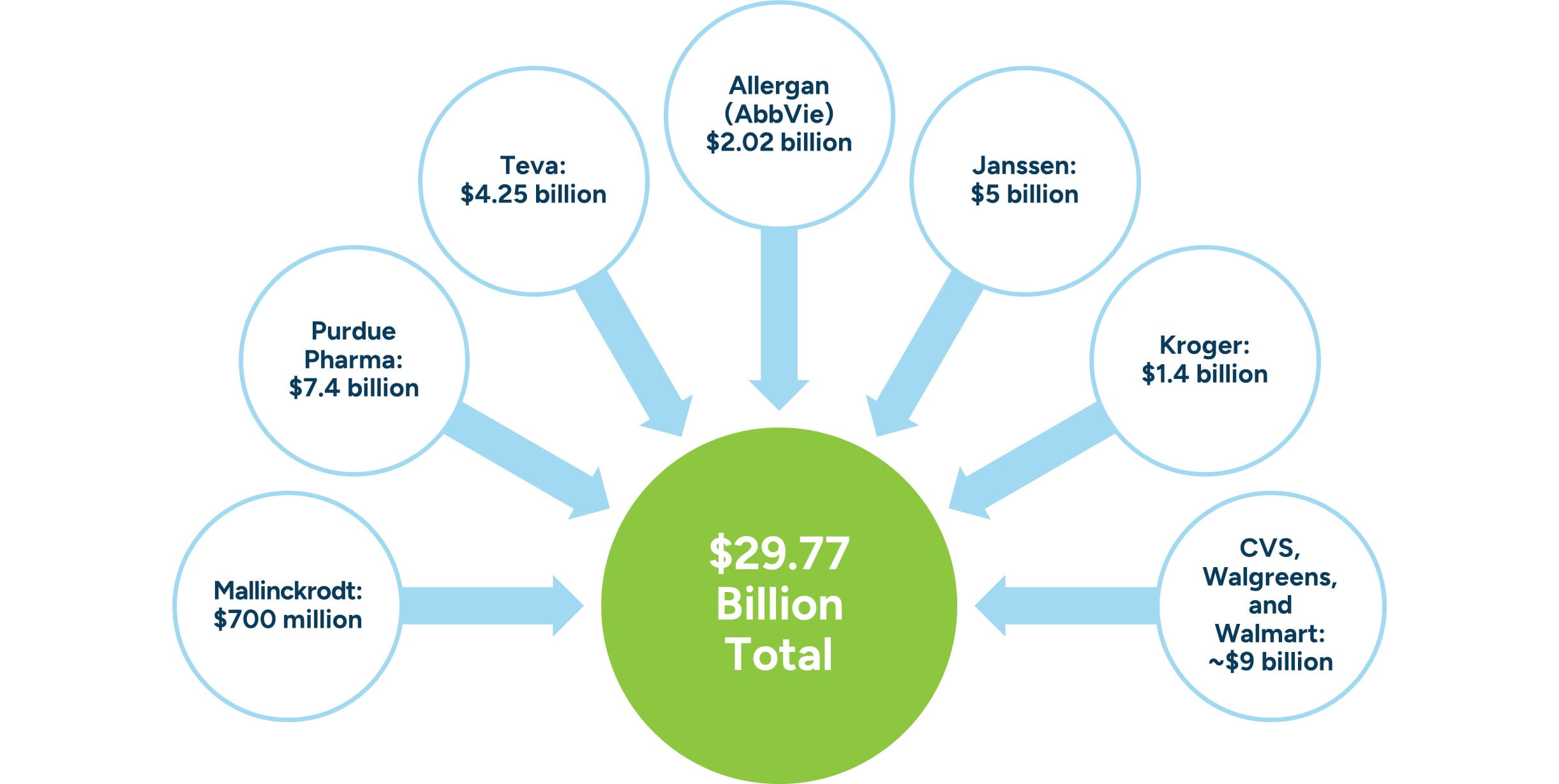

Opioid Settlement Payments – Second Wave

After reaching agreements for $26 billion, the states and local governments were not done, moving on to reach agreements with many of the largest pharmacies, such as CVS, Walgreens, and Walmart.19 These settlements range between $12.59 billion and $13.62 billion in aggregate. Along with making settlements with big pharmacies, the states agreed to many smaller settlements with other companies.

Figure 4: Settlement Payments to States and Local Governments

Figure 5: Spending Priorities by State

States' Options with Payments

According to National Academy for State Health Policy, 17 states have announced spending priorities or decisions for an initial portion of national settlement funds through approved spending plans as of June 2023.20 Figure 5 depicts where some states will focus on spending their money.

Ultimately, how each state spends its funds will likely vary. Furthermore, the level of transparency regarding the ultimate expenditure also varies. States like California, Florida, and Massachusetts are expected to be fully transparent at some point, while other states, like Texas, Mississippi, and Nebraska, do not expect to make any expenditures publicly available.21 However, the vast majority of funds are expected to directly address the epidemic. Such uses may manifest in additional law enforcement, housing, school awareness programs, as well as treatment programs, which may most directly benefit ATCs.

Medicare Physician Fee Schedule Changes

In addition to regulatory developments, the federal government encourages changes to the behavioral health and addiction markets via reimbursement under the Medicare Physician Fee Schedule (MPFS). Behavioral health benefited in the 2024 final rule from increased reimbursement rates for psychotherapy and behavioral health assessment codes. CMS intends to increase work values for these services by 19.1 percent over a four-year period.22 Starting in 2024, mental health counselors were able to bill Medicare directly for their services at 75 percent of the MPFS amount.23 CMS is also adding additional codes for psychotherapists to bill. New “G” codes titled “Social Determinant of Health Risk (“SDOH”) Assessment” are examples of such codes that practitioners will be able to utilize. CMS finalized their proposal for two new codes describing community health services performed by auxiliary personnel, such as community health workers, allowing such providers to bill incidentally. These expansions will help behavioral health providers to bill more accurately for their services while increasing their productivity and reimbursement, both of which should contribute to higher revenues for ATCs.

The 2025 final rule further adjusts reimbursement for addiction treatment, primarily by enabling periodic telehealth billing, even with audio-only interactions between providers and patients. First allowed during the COVID pandemic, CMS temporarily permitted telehealth visits to prescribe controlled substances to avoid unnecessary interactions. CMS is also proposing to reimburse efforts to evaluate addiction treatment patients’ social characteristics upon intake in order to increase the efficacy of the treatment program. Over the coming years, we expect continued changes to the Medicare program, which will likely result in increased access to addiction treatment and behavioral health services more broadly, particularly through the use of telehealth.

Leading Public Companies Insights

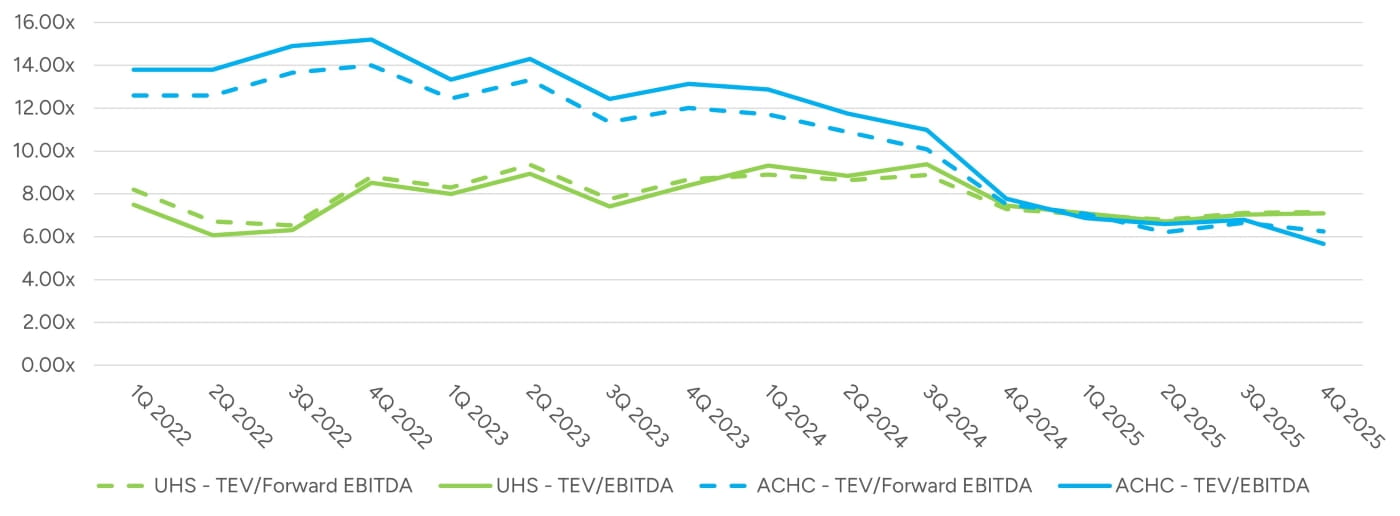

Addiction treatment in public markets is represented by two large, flagship companies: Acadia Healthcare Company (NasdaqGS: ACHC) and Universal Health Services, Inc. (NYSE: UHS). Although neither is a “pure-play” addiction treatment center, examining these two companies can provide useful information into trends for behavioral healthcare and addiction treatment.

While valuation multiples can provide insight into how the market is pricing the value of behavioral health businesses, there are some limitations in relying upon public company multiples. First, the companies outlined in Figure 6 are much larger in size and scope than a singular business, implying a less risky business.

Figure 6: Enterprise to EBITDA Multiples

Additionally, UHS operates in many different spaces outside the behavioral health industry. This diversification of revenue sources also decreases each company’s risk profile. Executives from each firm have provided relevant commentary in conference calls, investor presentations, and other filings. Acadia, while previously focused on growth, has since scaled back capital expenditure budgets for the foreseeable future. Multiples for Acadia have generally declined over the past two years as Acadia adjusted their revenue and EBITDA guidance downward due to slowing growth, regulatory and legal scrutiny, and market conditions.

Acadia

On its fourth quarter earnings call of 2024, Acadia remained committed to growth in its Comprehensive Treatment Centers (CTC) service line, which helps patients obtain treatment for opioid use disorders by providing multiple levels of care. Over $500 million annually was expected to be spent between the construction of new inpatient beds and CTC facilities along with joint venture partnerships and acquisitions. However, management had expected this level of expenditures to materially taper by late 2025 or early 2026. Acadia will focus its efforts on completing pending projects, ramping up utilization at existing facilities, and achieving margin expansion into 2026.24

Universal Health Services, Inc.

Universal Health Services, Inc. (Universal Health) holds a large behavioral health portfolio, in addition to its general acute hospital segment. Universal Health’s 2025 third quarter 10-Q report stated that it owned and operated 182 inpatient behavioral health facilities and 102 outpatient behavioral health facilities in the United States. Behavioral health facilities account for approximately 43 percent of Universal Health’s net revenues for year-to-date fiscal year 2025.25 Universal Health forecasts growth in its behavioral segment for the upcoming year between 6.5 to 7.0 percent, driven by reimbursement growth of approximately 2.5 to 3.0 percent.26

While Universal Health is not as active in the acquisition market as Acadia, Universal Health is still growing its behavioral health segment through continual investments in its services, new facilities, and joint ventures. One such example is the development of a 120-bed behavioral health hospital in Missouri, slated to open by the end of 2026.

Transaction Activity

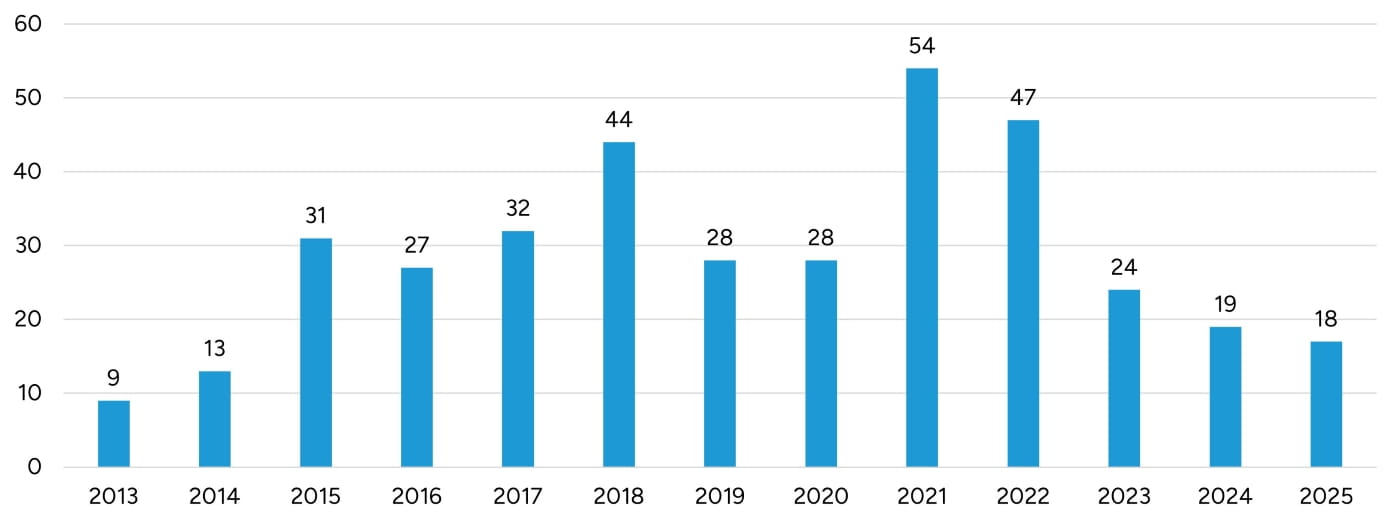

Given the rapid increase in demand for addiction treatment facilities, transaction activity has also generally increased compared to a decade ago. As outlined in Figure 7, 2021 was the most active year of mergers and acquisitions for addiction treatment centers, which was an extremely active year of healthcare transactions in all industries.27 Activity slowed significantly in 2023 due to diminished activity from financial buyers. Such buyers have represented about 50 to 65 percent of buyers over the past five years. A rise in interest rates over the past few years is also to blame for decreased transaction activity. Transaction volumes appear to have remained stable from 2024 through 2025.

Figure 7: SUD Facility Transaction Volume

Developments in Addiction Treatment Centers

Telehealth

As previously discussed, during COVID-19, telehealth grew exponentially due to the access and safety it provided - allowing physicians to treat and communicate with their patients while avoiding physical proximity, including the ability to prescribe controlled medications to their patients. In January 2025, the Drug Enforcement Agency (DEA) announced new rules that attempt to cement telehealth flexibility originally established during the COVID-19 pandemic. Broadly, these rules allow wider ability to prescribe certain controlled substances via telehealth visits (as opposed to stricter legacy requirements necessitating in-person visits), which could expand accessibility for patients to receive care, even if physically distant from a provider. With a scarcity of practitioners already, this change will positively impact patients looking to obtain treatment. Furthermore, the Medicare Physician Fee Schedule 2026 final rule expands the ability of behavioral health treatment to be reimbursed via telehealth. As such, we expect telehealth to be leveraged more frequently in rural settings where no local providers may be available.

Artificial Intelligence (AI) and Electronic Health Records (EHR)

Artificial intelligence has the power to help transform behavioral health. At the current moment, AI has shown promise in identifying different mental illnesses in patients or complementing a provider’s ability to diagnose patients. One such company is Limbic, which has a chatbot that can assist in accessing mental health support anywhere. AI can help by its immense power in accessing relevant information from a patient from various sources, such as medical records, internet searches, wearable devices, and social media, pinpointing patterns in the data to detect abnormal behavioral habits.

A primary problem with AI in mental healthcare is the dehumanization of healthcare. The human aspect of treating mental health is extremely important given the fragility of mental health. Discussing mental and addiction treatment issues with artificial intelligence removes the human aspect of treatment, as AI is unlikely to relate to mental health issues. AI must be used as support in unison with providers to improve patient care. A long-term goal for AI is to cut costs and reduce diagnosis times. Polypharmacy, or the simultaneous use of multiple drugs to treat a single condition, is one area already seeing reduced costs. Magellan Health has partnered with tech startup Arine to develop inforMED.28 This program utilizes AI to generate optimal care plans with treatment recommendations and to reduce polypharmacy, thus decreasing healthcare costs for patients.

Another issue with the potential use of AI in addiction treatment is the lack of electronic health records. EHR has been slow to adapt to mental health use due to the privacy and sensitivity of the issues of patients. There is also a lack of standardization of mental health data given that the data is more qualitative than quantitative in nature. Health information is core for the improvement of patient diagnoses and reduction in diagnosis time. Improvements in EHR should increase the benefits from AI as well with better records. Higher quality data will subsequently lead to better clinical differential analysis and pattern discovery. These technological tools can help improve the efficiency of behavioral health facilities - a positive for both patients and providers.

Behavioral Health and Employers

With awareness around addiction treatment becoming more openly discussed, people who did not consider seeking treatment are more likely to do so now. This has forced employers to offer more options regarding mental health and addiction treatment for employees. Some companies offer employees a free subscription to apps, such as Headspace. Companies may also offer their employees mental health days as a benefit. While these benefits provided by employers may increase demand, we believe access to ATCs will continue to be difficult, given bottlenecks in labor and ATCs broadly.

Conclusion

ATCs will continue to benefit from strong demand, with the primary challenge being their ability to increase capacity or efficiency. Secondarily, reimbursement growth has tapered from higher rates in recent years, but ATCs can still benefit from the lack of capacity to leverage themselves favorably with payors. However, the political landscape surrounding Medicaid remains a heightened uncertainty. ATCs should also benefit from improvements in technology and increased awareness around mental health. These factors should continue to drive interest within the transactions market for these facilities, as well as favorable demand trends for existing and new addiction treatment facilities.

Ben Cloutier materially contributed to this report

- “The Mental Health Parity and Addiction Equity Act (MHPAEA),” Centers for Medicare & Medicaid Services, webpage, last modified on September 10, 2024.

- Fact Sheet: Biden-Harris Administration Lowers Mental Health Care Costs by Improving Access to Mental Health and Substance Use Care. September 9, 2024.

- “Statement of U.S. Departments of Labor, Health and Human Services, and the Treasury regarding enforcement of the final rule on requirements related to the Mental Health Parity and Addiction Equity Act,” Employee Benefits Security, May 15, 2025.

- “Establishing The President’s Make America Healthy Again Commission,” presidential actions, February 13, 2025.

- “HHS Announces Transformation to Make America Healthy Again,” U.S. Department of Health and Human Services, press release, March 27, 2025.

- “HHS Budget in Brief,” U.S. Department of Health and Human Services, webpage.

- S.2938 - Bipartisan Safer Communities Act, Congress.gov.

- “Technical Supplement to the 2026 Budget: Appendix,” Office of Management and Budget, Executive Office of the President.

- Psychologists struggle to meet demand amid mental health crisis, 2022 COVID-19 Practitioner Impact Survey.

- The 2018 bed utilization calculation includes partial hospitalizations/day treatments. 2020’s utilization calculation does not include those treatments.

- Kaiser Family Foundation, Mental Health Care Health Professional Shortage Areas, December 2024.

- “Medicaid Enrollment and Unwinding Tracker,” Kaiser Family Foundation, January 5, 2026.

- Madeline Guth, Heather Saunders, et al., “How do States Deliver, Administer, and Integrate Behavioral Health Care? Findings from a Survey of State Medicaid Programs,” Kaiser Family Foundation, May 25, 2023.

- Rhiannon Euhus, Elizabeth Williams, Alice Burns, and Robin Rudowitz, “Allocating CBO’s Estimates of Federal Medicaid Spending Reductions and Enrollment Loss Across the States: House Reconciliation Bill,” Kaiser Family Foundation, June 4, 2025.

- Acadia Healthcare Third Quarter 2025 Earnings Call.

- Universal Health Third Quarter 2025 Earnings Call.

- Heather Saunders, Madeline Guth, and Gina Eckart, “A Look at Strategies to Address Behavioral Health Workforce Shortages: Findings from a Survey of State Medicaid Programs,” Kaiser Family Foundation, January 10, 2023.

- Aneri Pattani, “Localize This: Public Reporting of Opioid Settlement Cash,” Kaiser Family Foundation Health News, December 18, 2024.

- “National Opioid Litigation: Settlement Agreements as of January 2025.” Congressional Research Service.

- Sam Mermin and Katie Greene, “An Early Look at State Opioid Settlement Spending Decisions,” National Academy for State Health Policy, June 12, 2023.

- Opioid Settlement Tracker, OpioidSettlementTracker.com.

- “2024 Physician Fee Schedule final rule released,” Office of Healthcare Financing, American Psychological Association, November 17, 2023.

- “Marriage and Family Therapists & Mental Health Counselors,” Centers for Medicare and Medicaid Services, webpage.

- Acadia Third Quarter 2025 Earnings Call.

- SEC EDGAR Database, UHS Form 10-K Filing for the fourth Quarter 2024.

- UHS Third Quarter 2025 Earnings Call.

- From LevinPro Healthcare transactions database up through December 31, 2025. Such transaction data from a singular source is useful for inferring trends within the broader market.

- Gina Shaw, “Machine Learning Reduces Polypharmacy in Behavioral Health,” Pharmacy Practice News, February 22, 2024.