Deutsch

Deutsch

For many companies, COVID-19 and its accompanying disruptions in the marketplace led to a triggering event for impairment testing. Now, faced with the potential for a post-COVID downturn in the market, companies again need to consider whether a market downturn constitutes a triggering event for purposes of their goodwill, intangible asset, and fixed-asset impairment testing.

Impairment Testing Requirements

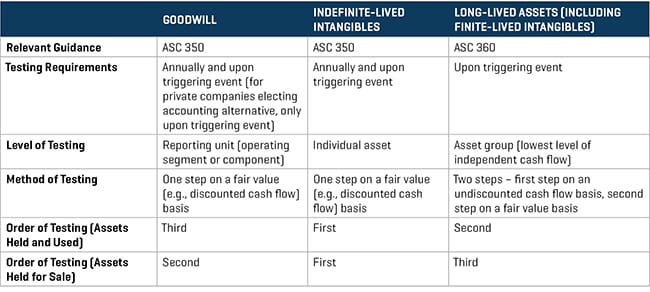

Before we delve into potential triggering events, a quick recap on impairment testing requirements under U.S. generally accepted accounting principles (GAAP) for various asset classes would be helpful.

Triggering Events

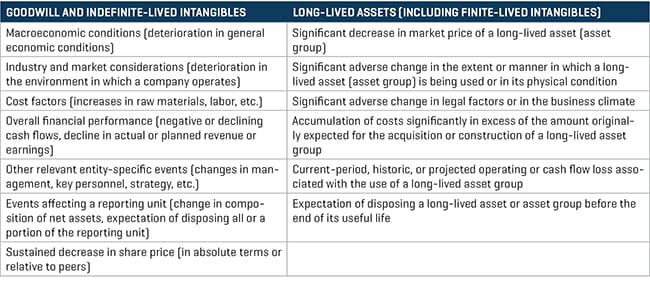

Triggering events differ for goodwill/indefinite-lived intangibles and long-lived assets. That said, an impairment of goodwill or indefinite-lived intangibles may trigger the need to conduct impairment testing for long-lived assets. Additionally, and while not specifically identified in ASC 360, significant entity-level events may trigger impairment testing for long-lived assets. Below are examples of triggering events for goodwill/indefinite-lived intangibles and long-lived assets, respectively.

Macroeconomic conditions such as a deteriorating on in general economic conditions, limitations on accessing capital, fluctuations in foreign exchange rates, or other developments in equity and credit markets.

A deterioration in macroeconomic conditions — namely, a downturn in the market — can qualify as a triggering event for impairment testing when assets may see their value affected. Companies will need to consider whether the value of their long-lived assets may experience impairment as a result of wider shifts in the economy.

Industry and market considerations include elements such as a deterioration in the environment in which an entity operates, an increased competitive environment, a decline in market-dependent multiples or metrics (considered in both absolute terms and relative to peers), a change in the market for an entity’s products or services, or a regulatory or political development.

Certain industries are more resistant (or more susceptible) to market downturns, so specific industries will have a greater need to consider impairment testing when the market recedes, perhaps even prior to their annual testing date. In determining whether a triggering event has occurred, companies should consider all facts and circumstances, including the near- and medium-term outlook for demand for products and services in their particular industry.

Overall financial performance includes such factors such as negative or declining cash flows or a decline in actual or planned revenue or earnings compared with actual and projected results of relevant prior periods.

Downturns in the market can lead to companies experiencing earnings that are lower than forecasted. Once companies are able to assess impacts to actual and forecasted results as a result of declining cash flows, they should consider whether such impacts represent a triggering event.

In doing so, the threshold for determining whether a triggering event has occurred may differ by reporting entity. For example, reporting entities that consummated a recent material acquisition or had a recent occurrence of goodwill impairment are at more risk, because any decrease in future cash flow expectations would likely cause an incremental impairment as opposed to a reporting entity that passed its most recent impairment test by a wide margin.

If applicable, a sustained decrease in share price (consider in both absolute terms and relative to peers).

To be clear, a decline in the overall stock market is not, in and of itself, necessarily a triggering event. The stock market can be highly volatile and the intent of the guidance is not to induce a wave of impairments every time the stock market swings. This is why ASC 350 specifically uses the phrase “sustained decrease.” Unfortunately, the guidance does not define or prescribe what is meant by “sustained.” Certain companies and industries may already be able to assert, with a high level of confidence, that their current share price declines will be “sustained,” but we do not have the requisite data set to determine whether this will be true for the overall market or less directly impacted companies and industries.

Regardless of whether or not it is determined that an immediate triggering event has occurred, it is important that public companies include appropriate disclosures as to the risks presented by the current economic environment. To the extent that such conditions persist and become an impairment trigger, the SEC will expect that companies have provided an appropriate level of foreshadowing in their public filings.