Deutsch

Deutsch

Changes in senior management, shifting corporate strategies, material acquisitions, restructuring activities, and other major corporate events can trigger significant changes in a company’s operations.

Furthermore, such events may often necessitate that a company change its reporting composition.

We describe the prevalence and common triggering events behind goodwill reassignments across the broader U.S. market. We also discuss relevant accounting guidance and present a case study example.

Goodwill Reassignment

When an entity that follows U.S. generally accepted accounting principles (GAAP) reorganizes its reporting structure and changes the composition of one or more reporting units, goodwill is reassigned to the reporting units affected using a relative fair value allocation approach. Specifically, this approach is similar to that used when a portion of a reporting unit is to be disposed of pursuant to Financial Accounting Standards Board Accounting Standards Codification (ASC) 350-20-40-1 through 40-7.1

Prevalence of Goodwill Reassignments

We reviewed annual reports of U.S. companies filed with the Securities and Exchange Commission (SEC) for fiscal year periods ending January 1, 2018, through December 31, 2022. Specifically, we screened for companies that matched all of the following criteria:

- SEC registrant was domiciled in the United States

- The company maintained goodwill on its balance sheet at some point during the 2018 to 2022 time period

- One of the following phrases was included within an annual report filed with the SEC during the applicable time window:

- Goodwill reallocation

- Goodwill realignment

- Goodwill reassignment

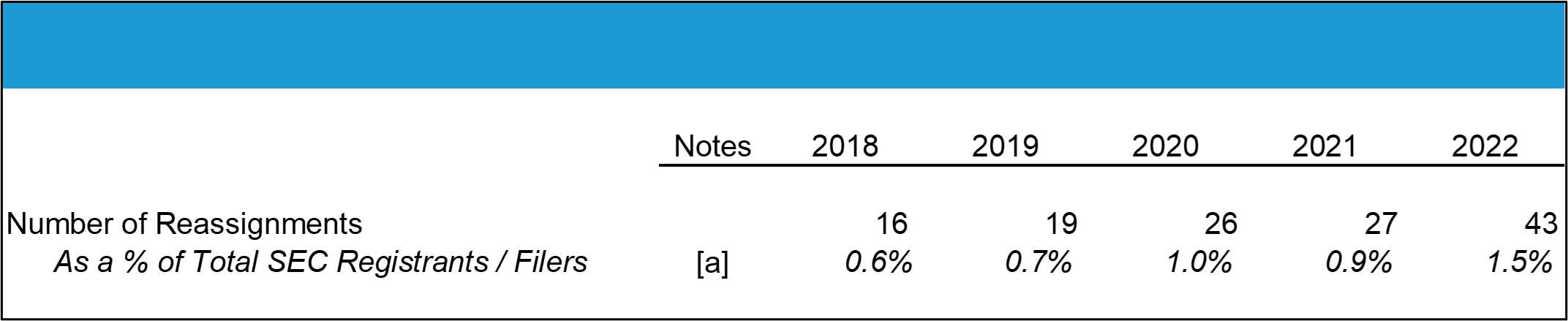

Based on the screening process above, we identified 131 instances of a goodwill reassignment within the data set of U.S. companies. Furthermore, the data suggests that the frequency of goodwill reassignments has increased steadily over the five-year time window that we analyzed (Figure 1).

Figure 1. Annual Goodwill Reassignments

[a] Only includes the SEC registrants / filers that maintained goodwill on their balance sheet during the respective calendar years.

The most common cause of goodwill reassignments was a “change to organizational structure,” which most frequently resulted in an increase or decrease in the number of reporting units. Although the underlying reason for the organizational structure change was not always discussed in the SEC filings, common reasons include the following:

- Recent acquisitions or divestitures

- Changes in strategy or realignment of management teams

- Restructuring activities or facility closures

- Realignment of product lines between segments

- Reclassification of net sales or segment profit between segments

- Transfer of other assets (liabilities) between segments

Although the total number of companies performing a goodwill reassignment typically hovered around 1% of total U.S.-based SEC registrants that maintain goodwill, many companies will encounter one or more of the organizational changes referenced above at some point.

Accounting Guidance

The accounting rules for goodwill reassignments focus on a relative fair value allocation approach. There is no explicit definition of this term within the ASC literature, but the guidance includes the following simplified example within ASC 350-20-40-3:

- Business is being sold for $100

- The fair value of the reporting unit excluding the business being sold is $300

- 25% of the goodwill residing in the reporting unit would be included in the carrying amount of the business to be sold

- The 25% amount is calculated as $100 divided by [$100 + $300]

This process requires a fair value assessment of the reporting units that are affected by a change in the company’s reporting structure. Traditional valuation methods include an Income Approach, Market Approach, and Cost Approach. For going concern businesses that are expected to generate positive future cash flows, the most common valuation methodologies employed are the discounted cash flow method (a form of the Income Approach), the guideline public company method (a form of the Market Approach), and the merger and acquisition method (also a form of the Market Approach). These three methods were also the most common valuation approaches cited within the SEC filing data for the registrants’ goodwill reassignments.

While we focus on the reassignment of goodwill, the guidance in ASC 350-20-35-39 through 35-40 is also used to reassign other assets and liabilities to the reporting units affected by a change in a company’s reporting structure. According to ASC 350-35-40, the methodology used to determine the amount of the assets and liabilities to assign to a reporting unit shall be “reasonable and supportable and shall be applied in a consistent manner.” This may range from a high-level allocation based on revenue, expenses, or employees to a more sophisticated fair value-based assessment.

One other point that is worth noting is related to the guidance in ASC 350-20-35-3C, which provides various examples of events and circumstances that could be deemed a “triggering event” which requires a company to perform an interim goodwill impairment assessment. In particular, “events affecting a reporting unit such as a change in the composition or carrying amount of its net assets” and “a more-likely-than-not expectation of selling or disposing of all, or a portion, of a reporting unit” are referenced. In our experience, a company reorganization that results in a reporting structure change such that goodwill shall be reassigned is deemed a “triggering event” that requires an interim goodwill impairment assessment. Therefore, the fair value of the legacy reporting unit(s) must first be determined as of the goodwill reassignment date to assess whether there is an indication of impairment before the reassignment. After that determination is made, the assets and liabilities of the legacy reporting unit(s), including the incorporation of goodwill impairment (if any) from the interim test, is allocated to the new reporting unit structure.

Case Study

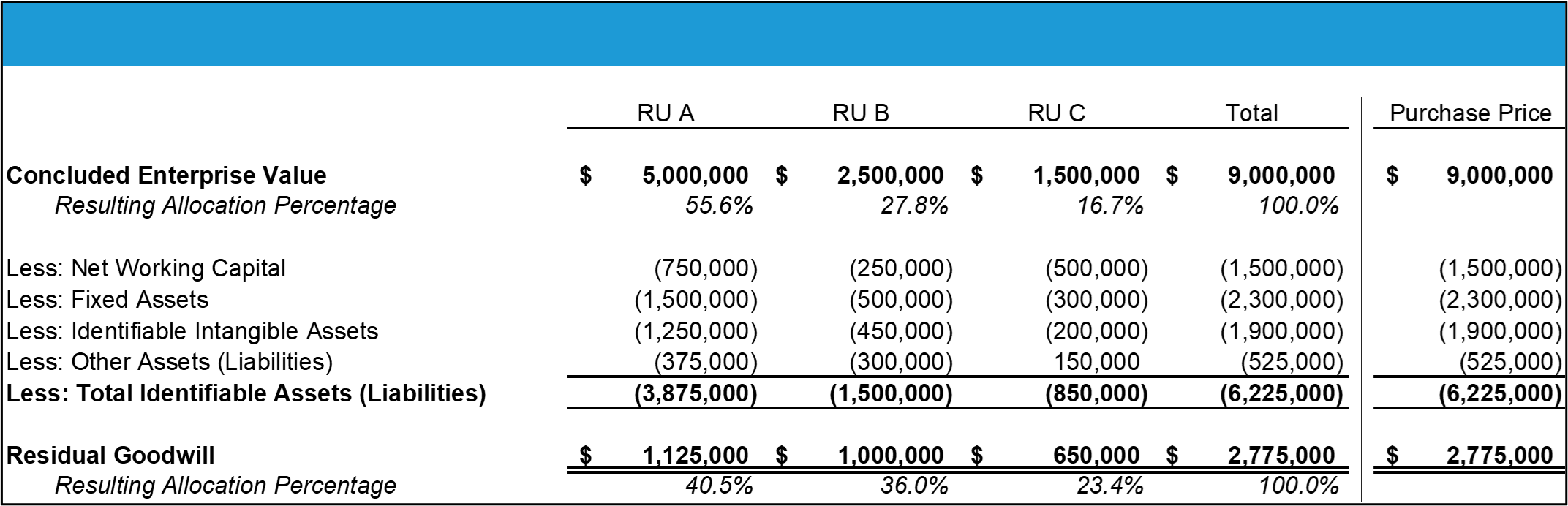

In the following example, a company’s legacy reporting unit has a fair value of $9.0 billion and a goodwill balance of $3.2 billion. Following a reorganization of senior management and the corresponding shift in strategy, the legacy reporting unit will be split into three new reporting units: New A, New B, and New C. As goodwill reassignments follow a relative fair value allocation approach, the company hires a third-party valuation specialist to determine the fair value of New A, New B, and New C. The specialist relies upon a discounted cash flow method and a guideline company method to yield a fair value of $5.0 billion for New A, $2.5 billion for New B, and $1.5 billion for New C. Therefore, the implied reassignment of goodwill would be as shown in Figure 2.

Figure 2. Goodwill Reassignment (in thousands of U.S. dollars)

In part, the relative fair value allocation approach in Figure 2 is consistent with acquisition accounting in the context of an acquired business that has multiple reporting units. For example, let’s assume the same company were acquired for $9.0 billion (consistent with its consolidated fair value per Figure 2) and its reporting structure post-acquisition aligned with the new two reporting units. If that were the case, a relative fair value exercise would need to be performed in conjunction with the acquisition accounting procedures to determine the residual goodwill to be allocated to each reporting unit. The first step in this process would be to determine the relative fair value of each reporting unit to determine the portion of the purchase price to be allocated to each reporting unit, as shown in Figure 3.

Figure 3. Acquisition Accounting (in thousands of U.S. dollars)

However, in the context of acquisition accounting, the fair value of all other acquired assets and assumed liabilities is determined and allocated to each reporting unit, as shown in Figure 4. Often, the residual goodwill allocated to each reporting unit (on a relative basis) differs from the allocation percentage implied by focusing on the relative fair value of each reporting unit due to differences in asset composition or other factors.

Figure 4. Acquisition Accounting (in thousands of U.S. dollars)

Because the asset composition of a reporting unit could materially impact the residual goodwill amount allocated to a reporting unit under acquisition accounting, we contend that other assets and liabilities should be considered in the context of goodwill reassignments.

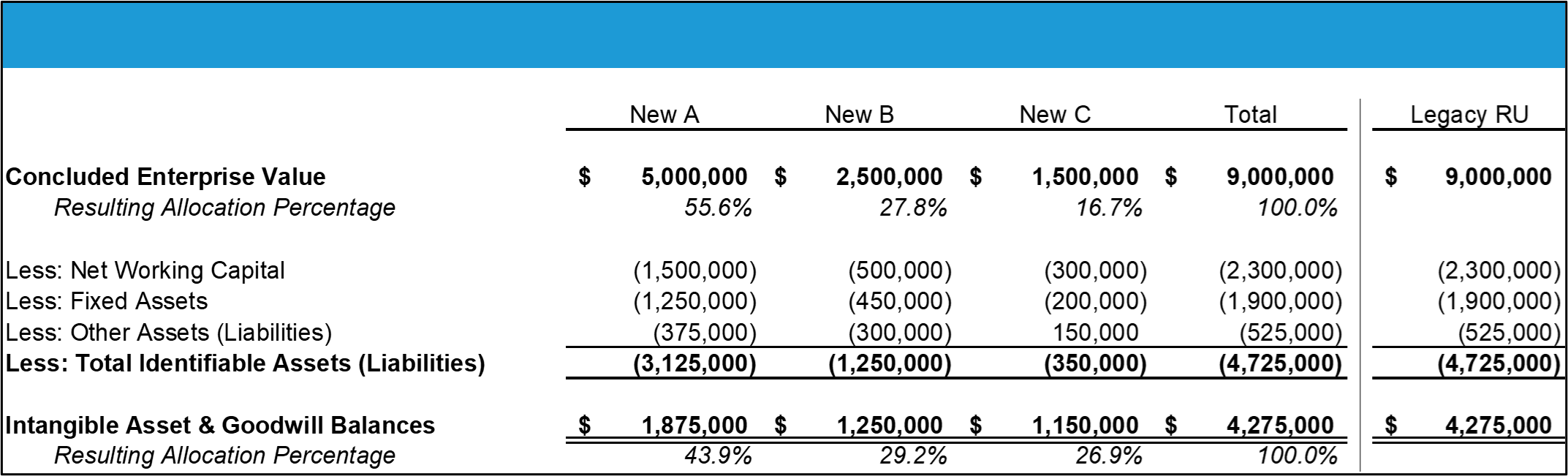

While the revaluation of all identifiable tangible and intangible assets at fair value generates the most accurate reassignment, this is not required. Instead, we suggest adding one simple step to the analysis presented in Figure 2 (as shown in Figure 5) that can more accurately derive an appropriate goodwill reassignment allocation percentage that considers the asset composition of each reporting unit. Thus, the analysis would then more closely resemble the process for determining the original goodwill amounts booked from previous acquisitions.

Figure 5. Goodwill Reassignment (in thousands of U.S. dollars)

As outlined in Figure 5, the net book value (NBV) of net working capital assets (liabilities), fixed assets, and other assets (liabilities) is subtracted from the concluded enterprise values to yield an implied balance of identifiable intangible assets and goodwill. Although NBV is rarely equivalent to fair value, the NBVs provide a proxy for the relative asset composition of the reporting units before considering intangible assets and goodwill. In the case study discussed herein, the implied allocation percentage differs materially after this adjustment is considered, as New A is more asset intensive than New B.

Corporations commonly encounter events that may lead to reorganizations or other operational changes that could impact an existing reporting unit structure. Understanding the accounting implications and valuation requirements associated with a goodwill reassignment amid a reporting unit structure change is important for proper planning and the avoidance of potential missteps during the process.

This article was originally published in August 2018, but has been updated with more recent data as of September 2023.