Deutsch

Deutsch

Decisions issued by the Delaware Court of Chancery (the “court”) illuminate the court’s perspective on a number of specific legal and financial topics under dispute. In certain cases involving business equity valuations, the court’s decision will necessarily delve into business valuation matters, addressing fundamental differences between petitioners’ and respondents’ experts’ valuation conclusions in order to explain the court’s decisions and remedies. Within this subset of court decisions, certain disputes feature disagreements between valuation experts regarding the applicable long-term growth rate to be used in a discounted cash flow (DCF) analysis to determine the fair value of the subject company. In these cases, the court’s written decisions provide deeper insight into its selection of an appropriate long-term growth rate and the associated rationale.

Impact of Long-Term Growth Rate on DCF Analysis

The selection of a long-term growth rate is one of the key assumptions made when performing a DCF analysis. The fair value of a business derived by a valuation expert via DCF analysis can vary significantly depending on the long-term growth rate assumed in the analysis.

DCF analysis entails use of a multiple-period model in which the value of a company is based on the present value of its expected future cash flows. Projected annual cash flows are typically calculated based on an analysis of revenue, expenses, and other cash flow adjustments such as capital expenditures, depreciation expense, and incremental working capital requirements. Projected cash flows are analyzed in two components:

- annual cash flows during a discrete period (typically five to 10 years following the valuation date)

- terminal period cash flows projected from the end of the discrete period into perpetuity

Discrete period cash flows are explicitly projected on an annual or other periodic basis and may vary in growth or profitability from period to period. Terminal period cash flows beyond this period into perpetuity are assumed to grow at a constant, stable rate – the long-term growth rate. Because the long-term growth rate applies into perpetuity, even seemingly modest variances in the long-term growth rate applied by valuation experts can have a significant impact on the value of the subject business.

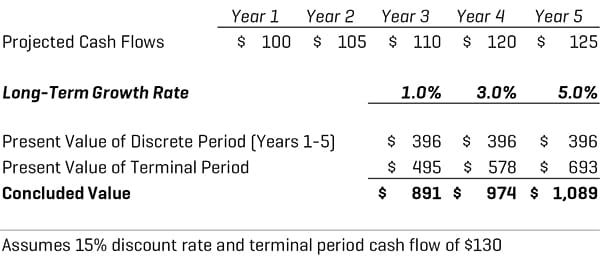

Figure 1 illustrates three hypothetical DCF analyses that differ only in the long-term growth rate applied (1%, 3%, and 5%) in order to demonstrate the impact that the long-term growth rate has on the resulting fair value of a company. Changing only this element of the analysis, the resulting fair values vary by over 22%. Clearly, the selection of a long-term growth rate requires significant scrutiny by the valuation expert when conducting a DCF analysis.

Figure 1. Long-Term Growth Rate Sensitivity in DCF Analysis

Long-Term Growth Rate in Recent Decisions by the Court

Within court decisions involving business valuation disputes, a majority of cases apply the DCF method. Within these disputes, valuation experts, even when provided with and using the same discrete period cash flow projections for the subject business, frequently disagree regarding the appropriate long-term growth rate in the terminal period to capture growth into perpetuity, resulting in significantly different valuation conclusions, as demonstrated in Figure 1. Moreover, valuation experts point to myriad explanations and data sources to support their assumed long-term growth rates, including, but not limited to, historical trends, industry research, analyst reports, economic growth, inflation figures, company management, or professional judgment. The court is tasked with parsing experts’ opinions to make a conclusive determination of the applicable long-term growth rate.

Generally, in reviewing the court’s recent decisions addressing long-term growth rates, it is evident that the court’s perspective has solidified in recent years, establishing a “floor” long-term growth rate based on inflation expectations and a “ceiling” long-term growth rate based on the overall growth of the economy.

Review and Analysis of Recent Decisions

We begin with Delaware Open MRI Radiology Associates, P.A. v. Howard B. Kessler, et al. (“Delaware Open MRI”), decided in 2006. In Delaware Open MRI, Vice Chancellor Leo E. Strine, Jr. wrote that respondent’s expert “essentially assumes no real growth in the value of Delaware Radiology after the projection period, which I believe is unduly pessimistic,” instead adopting petitioner’s expert’s assumed long-term growth rate that was 1.0% higher. As “real growth” refers to growth in excess of the rate of inflation, Vice Chancellor Strine’s assertion that a long-term growth rate reflecting no real growth is too low implicitly asserts that the long-term growth rate should be higher than inflation – at least for Delaware Radiology – suggesting that the inflation rate may reflect a lower bound.

Vice Chancellor Strine further emphasized a relationship between long-term growth and inflation in his 2010 decision Global GT LP and Global GT Ltd v. Golden Telecom, Inc. (“Golden Telecom”), opining, “A viable company should grow at least at the rate of inflation and, as [the respondent’s expert] admits, the rate of inflation is the floor for a terminal value estimate for a solidly profitable company that does not have an identifiable risk of insolvency.” Vice Chancellor Strine elaborates, “Although the relevant factors might have supported a terminal growth rate equal to the long run growth rate of Russia’s [gross domestic product (GDP)], [the petitioners’ expert] used a 5% terminal growth rate. [This] rate is the midpoint between the forecasted long-term Russian nominal GDP growth of 6.2%, and a forecasted inflation rate to 2030 of 3.9%.” Vice Chancellor Strine selected a long-term growth rate based on this midpoint, developing the construct for an instructive range between inflation and nominal GDP growth

Vice Chancellor Strine’s affirmation in Golden Telecom of a long-term growth rate tethered between inflation and nominal GDP growth established a precedent referenced by the court in numerous decisions to follow. Two cases in particular were decided in 2013:

- Towerview LLC; Hartz Capital Investments, L.L.C; Metropolitan Capital Advisors, L.P.; Metropolitan Capital Advisors International, LTD.; Jeffrey E. Schwarz; and Metropolitan Capital Advisors Select Fund, L.P. v. Cox Radio, Inc. (“Cox Radio”)

- Merion Capital, L.P., Magnetar Capital Master Fund Ltd., Magnetar Global Event Driven Master Fund Ltd., Magnetar SC Fund Ltd., Hipparchus Master Fund Ltd., Compass Offshore HTV PCC Limited, Compass HTV LLC, and Blackwell Partners LLC v. 3M Cogent, Inc. (“3M Cogent”)

In each of these cases, Vice Chancellor Donald F. Parsons Jr. cited and adopted the court’s position from Golden Telecom that, “the rate of inflation is the floor for a terminal value estimate” for a financially stable company when determining long-term growth rate in each case.

In the same decisions, Vice Chancellor Parsons cited valuation treatises bolstering the court’s Golden Telecom position that nominal GDP growth establishes a ceiling for the long-term growth rate. In Cox Radio, Vice Chancellor Parsons cited Shannon Pratt’s Valuing a Business: The Analysis and Appraisal of Closely Held Companies, explaining, “Some experts maintain that ‘the terminal growth rate should never be higher than the expected long-term nominal growth rate of the general economy, which includes both inflation and real growth’” ultimately selecting a long-term growth rate “slightly higher than the inflation rate.” Similarly, Vice Chancellor Parsons cited Bradford Cornell’s Corporate Valuation: Tools for Effective Appraisal and Decision Making in 3M Cogent: “A terminal growth rate should not be greater than the nominal growth rate for the United States economy, because ‘[i]f a company is assumed to grow at a higher rate indefinitely, its cash flow would eventually exceed America‘s [gross national product].’”

Beyond Cox Radio and 3M Cogent, the court would go on to cite and adopt Golden Telecom’s precedent in numerous other recent decisions as the basis for its long-term growth rate determinations, specifically including:

- In Re Trados Incorporated Shareholder Litigation (“Trados”), decided in 2013

- Nathan Owen v. Lynn Cannon, Bryn Owen, Energy Services Group, Inc., a Delaware corporation, and ESG Acquisition Corp. (n/k/a Energy Services Group, Inc.), a Delaware corporation (“Owen v. Cannon”), decided in 2015

- Merion Capital LP and Merion Capital II LP v. BMC Software, Inc. (“BMC Software”), decided in 2015

- In Re: Appraisal of Dell Inc. (“Dell”), decided in 2016

- Merion Capital L.P. and Merion Capital II L.P. v. Lender Processing Services, Inc. (“Lender Processing”), decided in 2016

- ACP Master, Ltd., et al. v. Sprint Corporation, et al. and ACP Master, Ltd., et al. v. Clearwire Corporation (“Clearwire”), decided in 2017

- Domain Associates, L.L.C., a Delaware limited liability company, James C. Blair, Brian H. Dovey, Brian K. Halak, Kim P. Kamdar, Jesse Treu, and Nicole Vitullo v. Nimesh S. Shah (“Domain”), decided in 2018

In each case, the court concluded on long-term growth rates representing a premium to inflation, but below nominal GDP growth.

In Owen v. Cannon, the petitioner’s expert selected a long-term growth rate of 5.0% on the basis of a modest premium (0.5%) to the midpoint of three estimates of nominal U.S. GDP growth. In contrast, the respondent’s expert applied a 3.0% long-term growth rate based on a premium to projected inflation. Chancellor Andre G. Bouchard stated in his decision that two “well-reasoned principles” guided his analysis. First, a terminal growth rate should not exceed the nominal growth rate of the U.S. economy, citing 3M Cogent. Second, the rate of inflation is the floor for a terminal value estimate for a profitable and solvent company, citing Golden Telecom. Moreover, Chancellor Bouchard proffered that, “There also is considerable precedent in Delaware for adopting a terminal growth rate that is a premium, such as 100 basis points, over inflation.” With this perspective, Chancellor Bouchard dismissed the petitioner’s expert’s long-term growth rate and adopted the long-term growth rate of the respondent’s expert.

Following his decision in Owen v. Cannon, Chancellor Bouchard issued decisions in In Re Appraisal of DFC Global Corp. (“DFC Global”) and John Douglas Dunmire, in his capacity as Trustee of the John Douglas Dunmire Revocable Trust, et al. v. Farmers & Merchants Bancorp of Western Pennsylvania, Inc. (“F&M Bancorp”) in late 2016. Chancellor Bouchard wrote that the court often selects a long-term growth rate based on a reasonable premium to inflation, citing Owen v. Cannon. In DFC Global, Chancellor Bouchard added that, “Although one suggested ceiling for a company’s perpetuity growth rate is nominal GDP … economists have cautioned … that the long-term growth rate should not be greater than the risk-free rate.” In both cases, the court determined a long-term growth rate approximating the risk-free rate (as measured by the 20-year U.S. Treasury yield).

Vice Chancellor J. Travis Laster’s decision on Lender Processing drew from the court’s recent decisions on Golden Telecom and DFC Global. Vice Chancellor Laster summarized that (i) the court often selects a perpetuity growth rate based on a reasonable premium to inflation, (ii) once an industry has matured a company will grow at a steady rate that is roughly equal to the rate of nominal GDP growth, and (iii) the risk-free rate is a viable proxy for expected nominal GDP growth. On this basis, Vice Chancellor Laster selected a long-term growth rate slightly below the risk-free rate.

In In Re Appraisal of SWS Group, Inc. (“SWS Group”), decided in 2017, Vice Chancellor Sam Glasscock III accepted a long-term growth rate of 3.35% deemed to be reasonable by both valuation experts. Vice Chancellor Glasscock provided little additional commentary except to acknowledge that the selected rate reflects the midpoint of the long-term expected inflation rate and the long-term expected economic growth rate of the economy at large.

Vice Chancellor Laster issued the Clearwire decision in late 2017, noting that the respondent’s expert “adopted a perpetuity growth rate of 3.35%, which represents the midpoint of inflation and GDP growth. [The petitioner’s expert] used a perpetuity growth rate of 4.5%, which represents expected GDP growth.” Vice Chancellor Laster adopted the respondent’s expert’s 3.35% long-term growth rate, elaborating that it takes into account all possibilities from success to financial distress.

In early 2018, Vice Chancellor Glasscock issued a decision in In Re Appraisal of AOL Inc. (“AOL”). AOL was composed of three operating segments: two rapidly growing and one mature. The respondent’s expert used a 3.25% long-term growth rate citing a premium to inflation, while the petitioner’s expert used a three-stage DCF model to capture a remaining period of “hypergrowth” beyond management’s four-year projections. Vice Chancellor Glasscock rejected the use of a three-stage model or any other attempt to make projections beyond management’s four-year projections as “brazen” for a fast-paced industry with significant fluctuations but acknowledged a need to capture AOL’s elevated growth prospects remaining at the end of management’s projection period. Accordingly, Vice Chancellor Glasscock selected a 3.5% long-term growth rate, exceeding the risk-free rate by 50 basis points, to account for AOL’s elevated growth prospects.

Finally, in Domain, the petitioner’s expert assumed the subject company would continue operating into perpetuity, but did not apply a long-term growth rate. The respondent’s expert used a 3.0% long-term growth rate. Vice Chancellor Laster adopted the respondent’s expert’s 3.0% long-term growth rate as “reasonable” and cited Golden Telecom’s position that the inflation rate should be the floor for the long-term growth rate for a profitable company without identifiable risk of insolvency.

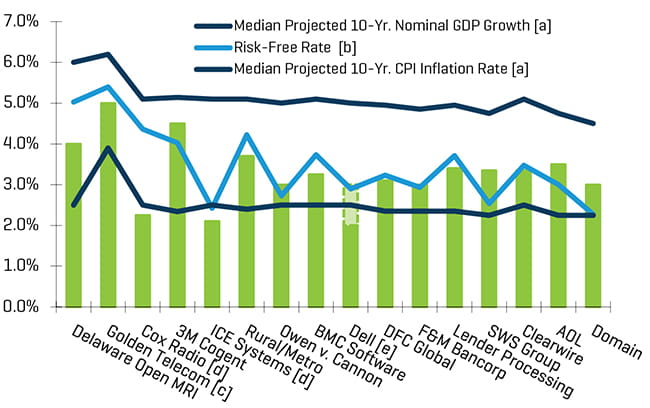

Figure 2 presents a visual trend of long-term growth rate decisions by the court issued in the aforementioned cases.

Figure 2. Delaware Chancery Decisions Addressing Long-Term Growth Rate (Compared with inflation, risk-free, and nominal GDP growth rates)

[a] Nominal GDP is calculated based on the following formula: Inflation Rate + Real GDP. The median projected 10-year CPI inflation rate and the median projected 10-year real GDP growth rate are based on the applicable valuation date for each case, as published in The Livingston Survey by the Federal Reserve Bank of Philadelphia.

[b] Based on the 20-year U.S. Treasury yield, except as noted.

[c] Concerns a Russia-domiciled subject company. The risk-free rate reflects the market yield on 10-year generic Russian government bonds. Russia inflation and GDP growth rates were provided in the court's decision.

[d] Selected by the court based on inflation, or a slight premium thereto.

[e] Vice Chancellor Laster opined that a 3% long-term growth rate was appropriate, but nevertheless used 2% since it was the higher of the rates applied by the respective experts. The lighter-shaded box reflects the 1% difference.

The previously discussed cases illustrate a consistent pattern supporting long-term growth rates at or inside of a range extending from projected inflation as a lower bound to nominal GDP growth as an upper bound. In many cases, we observe the court has dismissed experts’ long-term growth rate estimates outside of this range. More compelling, Figure 2 illustrates a close relationship between the long-term growth rates selected or accepted by the court and the risk-free rate as of the applicable valuation date in each case, particularly in the decisions issued in the last three years (i.e., since Owen v. Cannon).

By recognizing that long-term growth rates for certain industries and companies may not comport to the trends illustrated by the court’s recent decisions for various reasons, valuation experts conducting income-based analyses should be cognizant of the court’s perspective. As the court issues future decisions, Stout will continue to monitor trends in the court’s determination of long-term growth rates and other contested elements of business valuation analyses.

The decisions discussed in this article are exclusively from Delaware Court of Chancery fair value cases. The contents of this article may not be relevant or reliable in other jurisdictions, under different standards of value, or in other situations generally.