中文

中文

The following metals industry update analyzes Stout’s custom public company indices and proprietary M&A transaction database of North American metal-forming transactions. Targeted companies include casting, extrusion, finishing, forging, machining, stamping, and various other processing and fabrication businesses across a wide range of end markets.

2017 M&A Activity and Valuations Forge Ahead

Last year’s metal-forming merger and acquisition (M&A) activity mirrored robust conditions in broader M&A markets, supported by abundant equity and debt financing as well as strategic buyer M&A programs designed to accelerate growth. Further, high valuations for public companies and M&A targets indicate investor confidence in continued strength across most end markets. In the absence of any unanticipated geopolitical or economic surprises, M&A activity is expected to continue unabated in 2018.

Key Q4 Takeaways:

- Surging public equity markets and solid economic conditions continue to drive valuations and earnings

- The mix of metal-forming acquirors has remained evenly split between both strategic and private equity buyers

- Strategic buyers are utilizing strong balance sheets to accelerate growth through M&A

- Private equity firms benefiting from ample availability of capital are both active buyers and sellers of metal-forming companies

- The Commerce Department’s Section 232 investigation is fueling steel and aluminum price increases – the impact on metal-forming company margins will be determined by their ability to pass costs through to customers

Public Company Performance

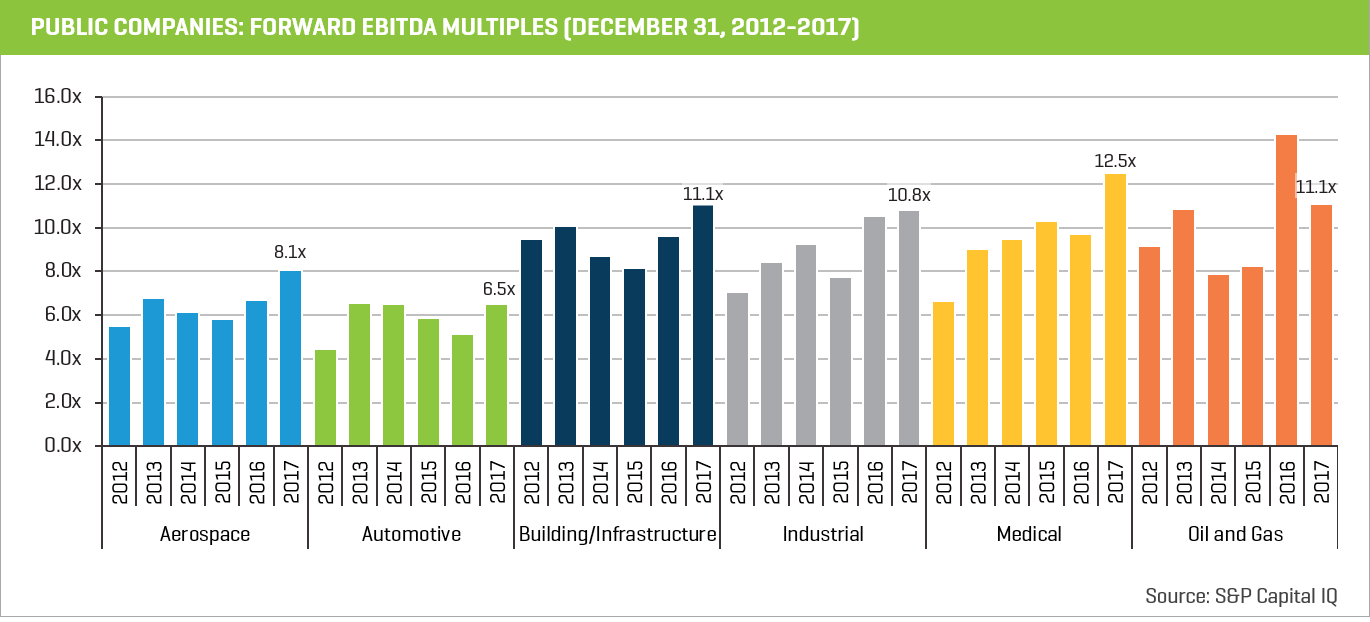

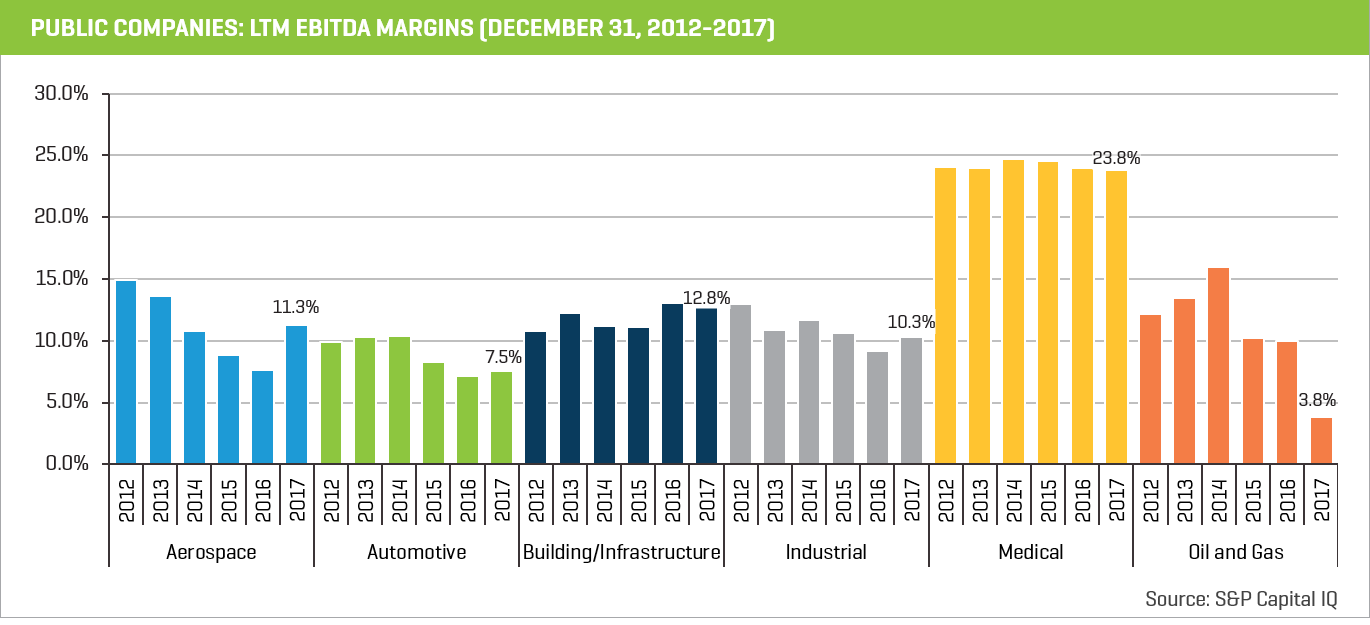

Public company valuations are at or near multi-year highs as equity markets reach record breaking levels. With the exception of companies serving the oil and gas market, metal-forming EBITDA margins ticked higher in 2017 with favorable economic conditions and end market demand. Metal-forming businesses have been modifying their supply chains and pricing policies to mitigate the potential margin impact of rising steel and aluminum prices brought on, at least in part, by the Commerce Department’s Section 232 investigation.

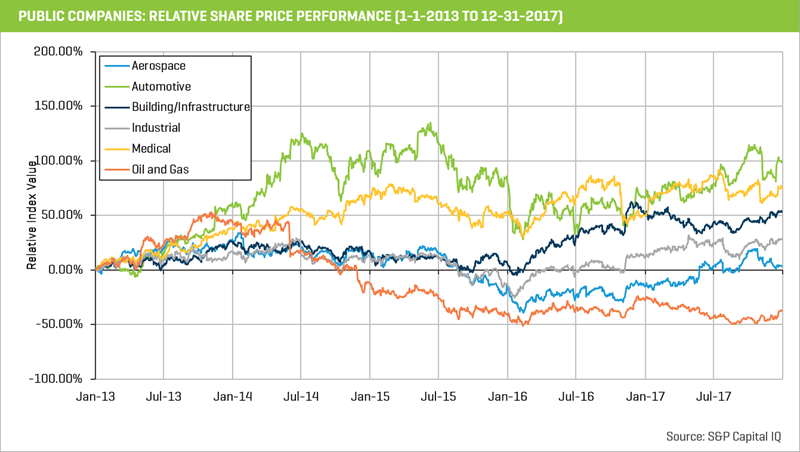

Public company share price performance within Stout’s proprietary metal-forming indices have generally faired well over the past five years, led by the automotive, medical, building/infrastructure, and industrial sectors. Aerospace company share prices are back near 2013 levels, while oil and gas companies have lagged the other indices as drilling activity remains below record levels.

M&A Activity and Target Valuations

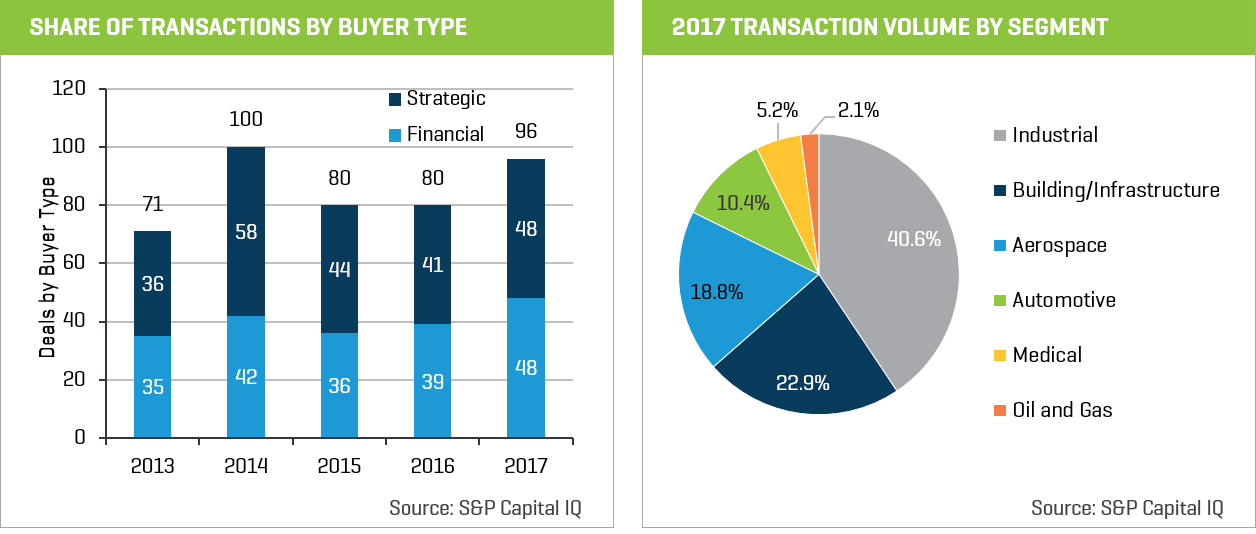

In 2017, 96 M&A metal-forming transactions were announced or completed, which represents a 20% increase over 2016. Financial buyers, including sponsor-backed strategic buyers, accounted for half of 2017 transaction volume as investors continue to deploy record amounts of equity capital. In terms of exits, financial sponsors represented 27% of sellers in 2017.

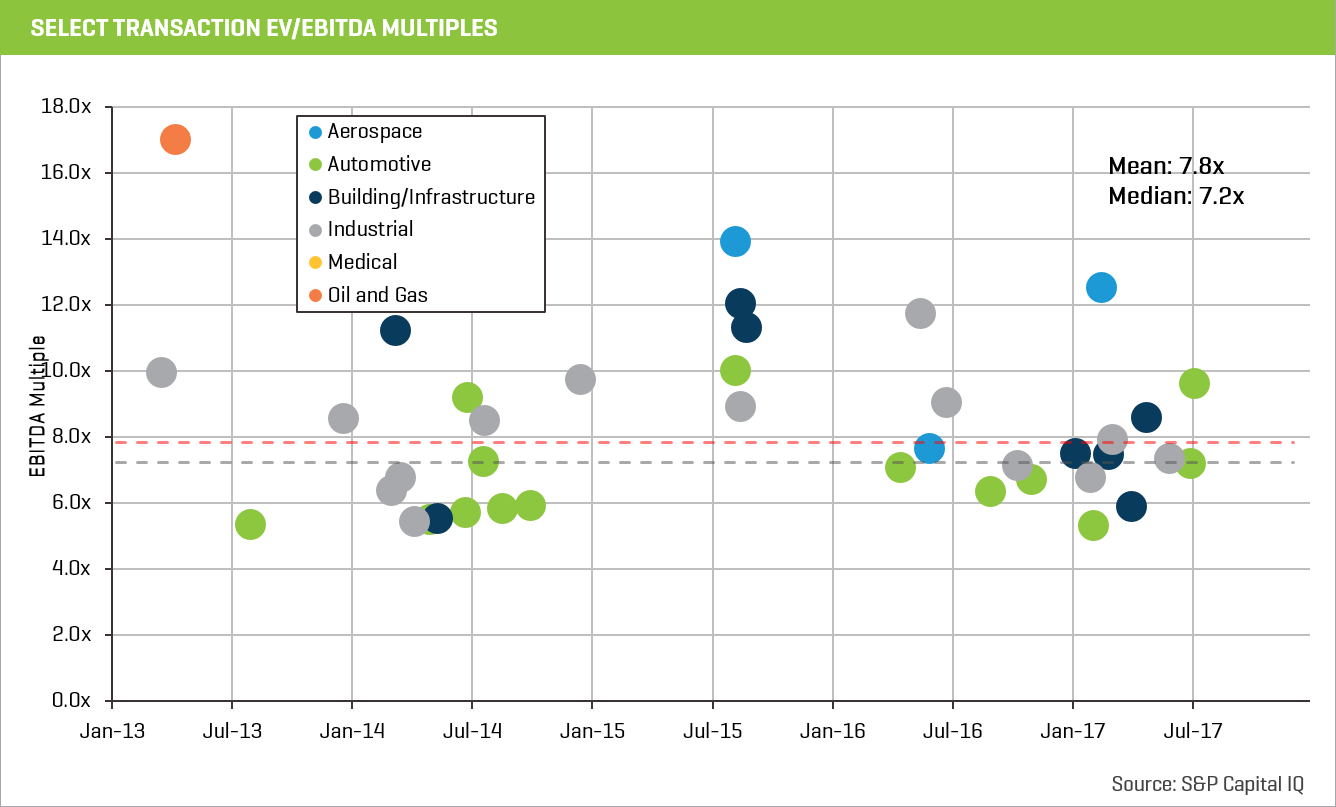

Transaction valuations for target companies over the past two years were clustered between 6.0x to 8.0x EBITDA, in line with the five-year median value of 7.2x EBITDA.