中文

中文

A relentlessly hardening insurance market in the downstream sector and a dismal record of recent property losses have created serious difficulties for refinery risk managers and their insurers alike. Both are intensely focused on developing a deeper understanding of the risks they manage in the midst of this challenging environment. One manifestation of this is the pursuit of greater transparency among the array of inputs that influence risk transfer arrangements. The total replacement cost estimate of a property is one such input. It influences the total value to be insured, premium amounts, the amount of risk being transferred versus retained, estimated maximum loss (EML), and probable maximum loss (PML) estimates.

These replacement cost figures are commonly self-reported by refineries; however, that practice is beginning to face greater scrutiny from insurers and underwriters as they navigate downstream property losses that remain high relative to previous years. For their part, refiners have experienced double-digit insurance rate increases year-over-year, and this trend does not appear to be subsiding. Global insurance brokerage Willis Towers Watson has predicted rate increases for refineries in the range of 30%-40% in 2020.[1] The situation has been made even more difficult as a result of these trends playing out amid a punishing economic environment for the oil and gas industry.

In the past, owners of refineries have used a few common approaches to estimate replacement costs for their properties. In the sections below we describe these approaches and their drawbacks that can diminish the quality of estimates. We also provide some suggestions and workarounds that can help mitigate the inherent weaknesses of each approach. Acknowledging and addressing these limitations will lead to more informed risk management decisions. After all, decisions can only be as good as the information on which they are based.

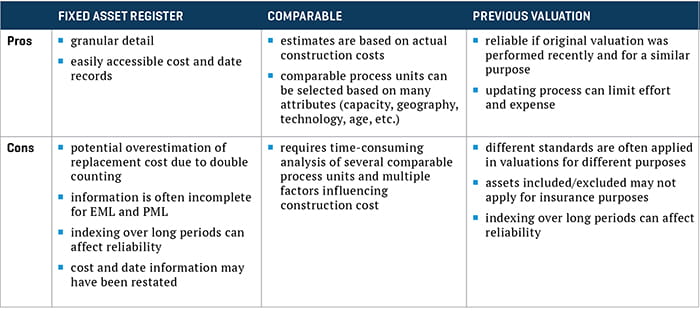

The Fixed Asset Register Approach

The fixed asset register for a refinery might contain hundreds or even thousands of individual line items, costs and capitalization dates, asset and account descriptions, and much more. Fixed asset registers are typically readily accessible and a good starting point for understanding a refinery’s asset base. They can be used to estimate current replacement costs by adjusting historical cost data for changes in buying power over time. However, the overwhelming volume of detail within the register can sometimes mask its limitations as a useful source for estimating replacement costs.

One of the main problems with the fixed asset register approach is the issue of double counting, as it can lead to overestimating replacement costs. Major refinery turnarounds are usually the primary source of this error. Because these substantial turnaround expenditures are often a mix of asset replacements, improvements, and additions, the way in which they contribute to the overall replacement cost will vary. Further complicating matters, the original assets that were replaced or improved are often still retained in the fixed asset register. Using this approach effectively requires an in-depth review of turnaround costs to ensure that replacements and improvements are not being counted twice in the overall estimate. This of course requires a substantial investment of time and effort far beyond simply summing the costs of assets as they are stated within the register.

Another relevant issue lies within the level of location-specific detail found in the fixed asset register. Process unit level replacement cost estimates serve as a key input in EML and PML calculations. Situations in which assets lack sufficient descriptive detail can lead to variations among process unit level estimates, which can in turn affect the reliability of loss estimates used in the underwriting process.

Lastly on the topic of asset listings, refineries might, over time, encounter situations such as mergers, acquisitions, bankruptcies, or impairments that necessitate a restatement of accounting records. In these instances, cost and date information within the asset listings are also typically restated or written down. Given the age of most refineries, this is not at all uncommon. Still, the fixed asset register approach should not be exclusively relied upon if cost and date information has been restated.

After negotiating any issues within the asset register, the next step using this approach involves adjusting the historical asset costs for changes in the buying power of the currency. This is usually done by utilizing indexes that capture price movements for refinery equipment over time. These indexes are a useful tool and certainly have their place in the valuation process when applied correctly; however, it is important to realize two things about their use. First, inflation-adjusted value estimates can lose precision when applied over long time periods. Second, these indexes capture average refinery-wide equipment cost behavior over time, and not all process units at a refinery will follow this average pattern. Relying too heavily on these average indexes can be a source of inaccuracy if the subject refinery meaningfully differs from the sample of refineries upon which the indexes are based.

The Comparable Approach

Estimating the value of a property based on the value of a comparable property is one of the most fundamental methods of valuation. This technique can be used to determine the replacement cost of one process unit based on the cost of a comparable process unit at another refinery. Though seemingly straightforward, this process rarely involves one-for-one comparisons. An array of different factors influence refinery construction costs, and these need to be carefully addressed to produce reasonable estimates.

Location

All refinery construction costs are influenced by location-specific factors in the same way that a house built on a remote mountainside would cost more than a similar house built in a typical suburb. Elements such as labor costs and availability, labor productivity, material costs, tax rates, shipping and freight charges, regulatory costs, and exchange rates all play a role in location-based cost differences. Interestingly, these factors can vary across different locations as well as for the same location over time. For example, the cost of a refinery built during a period of extreme labor shortage might far exceed the cost of a similar refinery built in the same location today, when labor is readily available.

Capacity

The relationship between cost and capacity is analogous to the concept of economies of scale. As capacity increases, cost also increases, but at a lower rate. The relationship between cost and capacity is commonly described by a scale factor, and these can differ among refinery process units due to the characteristics of their design and construction. Differences in capacity should always be taken into account, and scale factors specific to the process unit in question should be investigated.

Feedstock and Processing Requirements

Differences in feedstock type and processing requirements necessitate differences in design and construction that can heavily influence costs.

Refinery Configuration

The construction process may be more efficient, and therefore less costly, at a refinery with ample available space compared with another that is confined within a densely packed site.

Process Technology

There are often several different technologies or designs available for an individual refinery process. The cost differences between available process technologies can vary greatly and should thus be appropriately evaluated.

Purchasing Power

Adjustments for changes in the purchasing power of currency over time are necessary when using cost data from the past to estimate current costs.

The Previous Valuation Approach

Over the course of a refinery’s existence, there may be several occasions when valuations are performed. As replacement cost is often the starting point for most refinery valuations, this figure may be reported for previous acquisitions, tax purposes, insurance, financing, or engineering and feasibility studies. These prior replacement cost estimates are frequently relied upon for insurance purposes. If relying on prior valuations, pay close attention to the issues of applicability and timespan, as these can diminish the quality of insurable value estimates if unchecked.

Applicability is essentially the extent to which the purpose of the original valuation aligns with the current use as an estimate of insurable value. Valuations for unrelated purposes may have adopted wider margins of error, less scrutiny, or a more restricted analysis of replacement cost. These attributes might be perfectly reasonable in the context of a valuation where replacement cost was not the final conclusion, or where it was only a minor component of a larger project. Nonetheless, extracting an estimate from its original context can introduce ambiguity when the details of that original estimate are obscured beneath several layers of analysis.

The timespan over which a prior valuation is updated is somewhat less important than the manner in which the update is performed. That said, one of the most common approaches involves updating a prior year estimate for changes in buying power and making adjustments for any asset additions or disposals. Over time, the underlying assumptions and data inputs of the original valuation can become outdated. Across multiple iterations, this approach also increasingly relies on the asset listing, which can introduce issues of overestimation stemming from turnaround and improvement costs. It is good practice to periodically revisit the approaches and assumptions of the original valuation, as this can help recalibrate replacement cost estimates and mitigate issues that emerge when using a more cursory annual updating process.

Distilling the Approaches

Improving the Process

Whether using one or several of the methods discussed above, there are some common strategies that can be followed to improve reliability in the estimation process.

Guidance

Provide specific guidance to those responsible for developing replacement cost estimates. Determine the applicable approaches to be used, lay out the steps to be followed within those approaches, provide access to reliable cost-estimating data sources, and establish a system of review.

Validation

Any time one approach is used in isolation, the possibility for unchecked error can exist. Perform a validation on a sample of assets whereby the estimates derived using one approach are compared to the estimates derived using a different approach. If meaningful discrepancies exist, further investigation is warranted.

Scope

While it may seem obvious, defining the scope of assets to be valued can sometimes slip between the cracks. Provide the individuals responsible for estimating a clear indication of the assets that should be included for insurance purposes and those that should be excluded.

Delegate

The fact is, sometimes it just makes sense to delegate valuation to an outside specialist. Perhaps the internal estimating process has become too burdensome and unreliable, or insurers are pushing for an independent appraisal. A competent valuation specialist will consider the approaches described above, among several others, and will substantiate their findings with reliable data. They can efficiently identify critical issues at the outset of a project, work to develop solutions, and provide a consistent level of integrity in their estimates through comprehensive validation and review processes. Enlisting outside professionals can save time and effort and provide transparency for complex risk management decisions.

“What do we have to lose?” This fundamental question needs to be carefully considered before any risk can actually be managed. Quantifying an answer to this question based on unreliable or inconsistent methods can leave the true extent of exposure hidden from view. Improve your process for estimating replacement cost and you will develop a deeper understanding of the risks you manage.

- “Insurance Marketplace Realities 2020 Spring Update – Energy,” Willis Towers Watson, 2020.